By David Hargreaves

Oh, do you remember how it was when you were a kid and you SO much wanted something for Christmas that you almost felt physically ill?

Sympathies then for a Reserve Bank that is scarcely able to contain how desperate it is to slip debt-to-income ratios into its goodie bag of macro-prudential tools before everybody begins filling themselves with Christmas Pud.

It's becoming clearer and clearer that the RBNZ seriously missed a trick when it didn't move to get DTIs incorporated into the macro-pru kit when this was signed off by Finance Minister 2013.

Now, having made extensive use of the LVR tool from that kit, the RBNZ is gagging to get DTIs into the mix too - but the Government is resisting.

It was therefore interesting to hear RBNZ Governor Graeme Wheeler explicitly state, when releasing the latest Financial Stability Report, that he's due to have another meeting with Bill English in about two weeks time.

Ramping up the pressure

Whether it was intentional or not, by stating that there will be a meeting, Wheeler has ratcheted up the pressure on the Government to make a decision before Christmas.

This has now ensured that English will get microphones stuffed up his nose and be invited to state a view on whether the Government will acquiesce.

So, why the rush from the RBNZ?

Well, if it doesn't get agreement in principle from the Government before Christmas to the DTIs, then nothing will happen till well into February - such is the nature of the politicians' summer holiday. Then the next excuse (for yes, the Government is clearly making them on this), would be 'wait for the Budget' - in May. And then, well, it will be too close to the election.

The reality is, it's pretty difficult to see the RBNZ getting agreement to DTIs before the election if it doesn't get the Finance Minister to sign off on them before Christmas.

Remarkably, so keen has the RBNZ been to get agreement to the DTIs that it has explicitly said it won't use them at the moment. As a body independent from the Government it doesn't theoretically have to make such promises. But clearly, it has said that because it realises its chances of getting the DTIs into that macro-pru toolkit before the end of next year are receding rapidly.

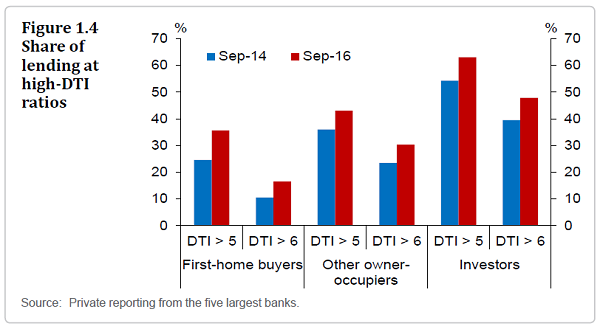

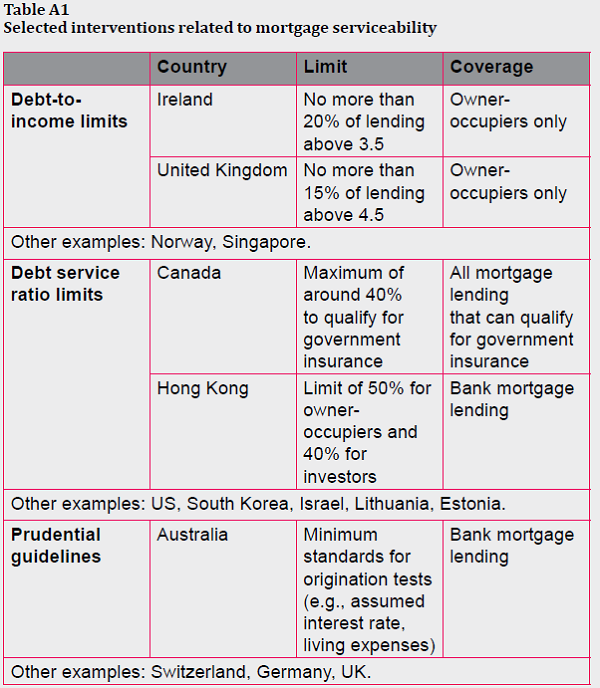

Given this kind of background, perhaps it's not surprising that the latest Financial Stability Report looks in part like a marketing document for DTIs, complete with graphs showing the rise of DTI ratios and what has been don in some other countries.

I could be wrong but I get the distinct impression that our central bank is quite keen on the rules as applied in Ireland - that is, a 3.5x ratio figure, with banks only allowed to lend 20% of new borrowing at above that ratio.

Such a ratio would undoubtedly have a heck of an impact.

While the RBNZ has basically promised it wouldn't use the DTIs at the moment, I somehow can't see the Government now wanting to risk giving our central bank such potentially heavy-hitting weaponry before the election.

With the latest iteration of the LVRs policy (the 40% deposit rule for investors) seemingly, just at the moment anyway, having a dampening influence on the housing market, the Government is going to be thoroughly justified in delaying any decision on DTIs.

Playing down LVR success

In this light and in the general mood of DTI marketing that appears to be going on, it has been interesting to note how much the RBNZ is currently playing down the present impact of the LVR moves - when it wasn't particularly shy in pointing to their success through the 2013-14 period.

In fact the whole Financial Stability Report was rather more downbeat than I would have expected, given improvement in the dairy outlook and the recent lessening of pressure in the housing market.

For the record, I'm supportive of the idea of DTIs but would personally prefer to see them introduced instead of LVRs. Whether the limit needs to be set as low as 3.5, which is what the RBNZ may or may not have in mind, is a debatable point.

A giving Finance Minister?

However, unless Bill English is feeling in a particularly giving and festive mood, this is perhaps going to be academic. Unless the DTI approval comes before Christmas, I reckon we can forget all about it for next year.

This is a pity, I think. You have to take chances while you've got them in this life. And 2013 appeared to be the RBNZ's chance for DTIs. Unless our central bank gets a bit of pre-Christmas good fortune, it might have to wait a little while for another shot at this one.

23 Comments

If the RBNZ has answered the minister's questions there really isn't much excuse to not add the DTI to the toolkit. The RBNZ has laid out the basic rationale for DTI being different to LVR in today's update. I wouldn't discount the possibility of English signing it off before Christmas or early in the new year.

I think the RBNZ will implement DTI across all lending (including investor) and probably at a multiple of 6 initially. All of their material references the 6x multiple and they will be aware that implementing a 3.5x multiple will push the economy into a depression (because it is so dependent on private debt growth and the construction sector, using the home as an ATM, etc).

I see in the news Bill is going to give us a continued supply of immigrants for Xmas, should help keep property prices and bank lending up.

That's the thing - I'm not convinced that immigrants are responsible for the house prices rises. Currently houses in Auckland are not selling as well at all - yet immigration is still high. Borrowing - well banks are now "rationing" credit.

I think people have been telling themselves lies and believing it - now reality has got in the way......

I think houses in desirable areas will continue to become more expensive. Globalisation is the cause. A desirable location is not too hard to identify. Primarily a place where you can settle in safety, send you children to good schools, find employment or a means to make money and near an international airport. Places that have high levels of individual freedom and reasonable climates. Places that have good medical facilities and stable governments. Places that have a British heritage will have an edge because of the English language and highly civilized institutions. Places that have established ethnic infrastructure, especially Indian and Chinese. Places that have high levels of trust and little racism or xenophobia.These places will be people magnets.Every city on the planet that has most of these features has seen property prices rise dramatically in the last few years.

With greater numbers of people flowing across borders these sorts of locations are going to attract extraordinary interest.Huge numbers of people in many parts of the world have become wealthy however they live in places that are overcrowded, polluted, superstitious, restrictive, corrupt and very competitive. Their children's welfare will be a concern where even schooling itself is a living hell with its highly competitive atmosphere. Social hierarchies, restricted human rights and long standing and stifling social institutions will continue to push people to seek more pleasant cities and cultures to live in.

The potential number of buyers for a house in the desirable locations is huge but the number of houses are limited. This is why even a poor house in Manurewa is now extraordinarily expensive.

*These cities even come with no obligations for the new residents. There is no compulsion to integrate or even to physically defend them when it comes down to it. There is even ample opportunity to rail against any perceived injustice and take advantage of all local resources including the people. All you need is some money.

Yawn - yes we known your views the only problem is they are unprovable - a wishy washy theory with no definite and definable outcomes that are provable - much like most of macroeconomics. You must be confused. On the one hand you are an ardent Trump supporter ( a paleo-conservative ) - and Trump advocates protectionism and isolationism and on the other hand you are relying on globalisation to prop up your inflated house prices - how do you reconcile this difference or are you just an opportunist who doesn't really believe in anything. Just curious....

Be careful what you wish for - the increase in any particular cultural group may just result in their criminal element coming as well (e.g. the Chinese Triads) .

I didn't say I was wishing for it. In fact I am against it. My prediction is that this will be the natural result of globalisation. However if we are going to do it I suggest we restrict immigration to only the wealthy, the skilled and the beautiful. Build my Elysium.

Your comment above about immigration not being part of the cause of house price inflation in Auckland is weird. Auckland's immigrant population is huge. Most people in NZ want to live in Auckland and naturally most immigrants do as well.

Your comments are just the same thing over and over again much like mine as to house prices.

To answer your curiosity I see myself as,

Riding the Tiger

And the subject of this song,

Jokerman

What I am saying is that peolpe have continually been saying that house price inflation has been the result of immigration ( and one of those groups is students) yet now we are facing the situation where the Auckland housing market is showing signs of "distress" - falling auction clearance rates etc - yet we still have high immigration. Perhaps immigrants aren't the true source of house price inflation but "property investors" or worse irrational exuberance i.e. greater fool theory . If immigrants were one of the groups responsible I would still expect a strong market. - something doesn't add up - or as John Key would say - it doesn't pass the sniff test. It seems only since the LVR rules were introduced that the market seems to have softened Those rules mainly affected "property investors". And then there is the banks "credit" rationing - that shouldn't affect all these "cashed" up immigrants - something doesn't add up.

While I don't doubt Auckland's immigrant population is huge - correlation does not mean causation - I think you are confusing the two.

Re Riding the Tiger - ah enlightenment - man trying to fool himself that they are "better" than the caveman they come from. How many genocides have there been in the 20th century....

The Auckland housing market isn't distressed. Property investment is a long term thing. Just because it is not smoking hot like it was doesn't mean we are facing a problem. Banks are reluctant to lend money on the basis of income earned overseas and LVR rules have been introduced to suppress house price inflation so it is no surprise at all that the market has softened.

You may be no better than a caveman but I certainly am. It's all about ever expanding horizons, accumulated information and levels of consciousness not about capacity for destruction.

I think your last statement proves my point - you seem to be intellectualizing everything / over thinking.

I really have no idea what your point is.

I think you summed it up nicely.

Immigrants are very much to blame indirectly for house price inflation and a shortage of houses for families to buy.

Where I work, we have about 6 Chinese immigrants. They are all obsessed with buying as many rental properties as they can. Most have at least 4 rental properties, all bought over the last 2 years. Their equity in these properties is very low, but they have increased their wealth dramatically with the tax free capital gain.

They tell us they cannot believe how easy it is to make money out of real estate here with the "hands off " approach by the NZ Government. ie no regulations.

Chinese investment in NZ does not do any good for the majority of NZers, their money does not create jobs or go into anything productive.

Most Chinese immigrants here are accumulating numerous rental houses here to the detriment of young NZ families.

As above, I have personally witnessed this happening.

So you then have to ask yourself the simple question, why are Kiwi's not purchasing multiple houses ? The answer is pretty simple, wage inflation has been so low for the last 30 years that they can now no longer afford to buy a single house to live in. I think Kiwi's here really fail to grasp how much money the Chinese have at their disposal to purchase houses. We are all going Woo Hoo my house is now worth a million dollars when clearly there are Chinese coming in with tens of millions of surplus cash that they want to park the money in thats a safe bet. Sure they probably don't even care what job they do here as long as they get a foot in the door because like my last job, a quick calculation reveled that my house was making twice as much as I was per year.

I don't think the Chinese are any better at investing - I'm curious why the word "obsessed" was used - that scares me in the investing context - irrational exuberance .

Can create insane bubbles through sheer numbers. Kind of like boomers.

Just means a bigger pool of greater fools.

See this timely chart on ZeroHedge summarising the Chinese bubble journey over the last few years!

(http://www.zerohedge.com/sites/default/files/images/user3303/imageroot/…)

{kind=link}

I was thinking that they would set the DTI multiple at something high like 6 and could then very slowly dial it back to 3.5 making sure that the market goes sideways, rather than crashing it. possibly removing some LVR at the same time...

I disagree with your article David, Wheeler himself said today he would NOT use DTI's now,

3.5 is the long term average.

Hmmm try getting a house for that.

Yes rbnz needs to act

DTI would gut the Auckland investors. It would need to be 25-30 x to support the current price/income from the speculator ponzi. Yield went out the window many years ago. To quote Kiri Barfoot, "thank god for capital gains". What if that gravy boat has sailed for a while?

If there is to be no to low capital gains, and the yield is less that dirt in the bank, why would you take on the risk of property?

First point - So Wheeler wants the UK system.

But the UK system specifically does not apply to investors - only owner-occupiers.

So he wants the UK system but to apply to all borrowers!

Second point - do they work?

Is there any proof that DTIs have actually restrained property price inflation anywhere they have been applied?

How would they not work? Investors forced into actually making a return and not farming high levels of debt to minimise tax on other income. Overall price reduction would keep speculators on the sidelines. Even a 5 year fix has to be refinanced at some point and thats when the piper will have to be paid.

The new Nzers buying up property still have to rent and maintain it. The shine will come off very fast when capital gain goes into reverse and the vacancies and repair bills start. Wheeler doesn't need DTIs. Banks are already rationing credit to reduce risk, and that's all he's really worried about - systemic risk in the banking system - and as per yesterday's FSR report - dairy and houses are the big risks and both are coming into line to an extent.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.