By Cameron Preston*

Homeowners pay premiums in return for a promise that they will be compensated in case of a disaster.

In order to keep their side of the promise, insurers need to have sufficient financial resources available.

The recent hypocritical finger pointing between the minister responsible for our public insurer, EQC, and the chairperson of our largest NZ owned private insurer, Tower, boils down to one simple issue: neither had the financial resources to keep their promise.

From Tower’s perspective the problem started simply enough. It funded its promise via reinsurance, but did not purchase enough.

So it had to fall back on its capital instead.

In a memo dated 17 March 2011 authored by the RBNZ’s Head of Prudential Supervision, Toby Fiennes to then Minister English, Fiennes noted that Tower “might have exceeded the top level of catastrophe cover”. However he went on to observe:

“Tower group had net assets of $440m…. needed to support the other 3 Tower insurers. At the recent AGM, Tower disclosed they are considering a return of some capital. We therefore expect they would be able to meet any shortfall from wider group resources.”

As it transpired Tower cosolidated its three insurers and returned some capital, but instead of quickly honouring its promises to its policyholders and returning the capital to them, Tower gave it back to its shareholders instead.

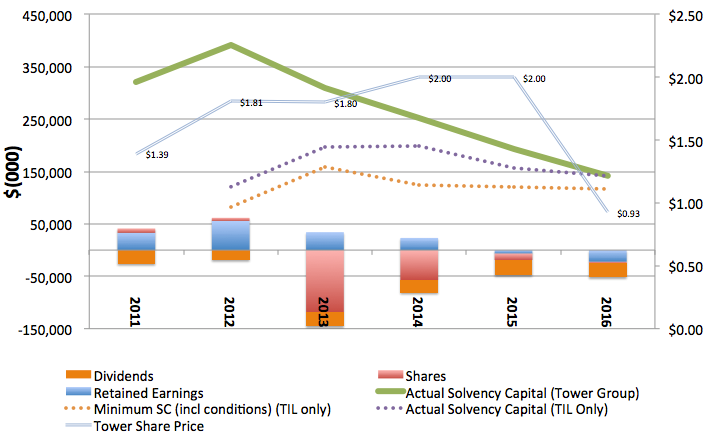

Between 2011 and 2016, Tower Group returned capital of $327mln to its shareholders in the form of dividends and share buy backs:

In 2013 the Board excited its shareholders with catch phrases like “delivering value to shareholders” by operating an “efficient capital structure while delivering strong returns”, meanwhile its patient policyholders were completely unaware that poor corporate governance was steering their insurer towards the situation Tower face today.

So who was entitled to any ‘excess’ capital first? the policyholder or the shareholder?

Did the policyholder take a bigger risk when buying their promise from Tower than a shareholder did when buying theirs?

Tower obfuscate by indicating that the policyholder and the shareholder would have both got their respective promises had they had a more timely view and access to their claim exposure from EQC and that the Board had acted “prudently” in the circumstances, which is akin to “the dog ate my homework”.

However EQC and its Minister are no better.

Sir Roger Douglas noted in EQC's first corporatised Annual Report in 1988 that EQC had now become “an independent Corporation controlling its own finances”. In fact the opposite was the case, and the government began draining EQC of its premium income and investment capital at ‘arms length’, by diverting it into government stock and taking massive dividends and lieu payments.

Between 1988 and 1996 $1.5bln of premium income was extracted from EQC under the guise of a ‘reinsurance fees, payemts in lieu of taxes’ and straight dividends. Worst still EQC’s remaining $6bln “Natural Disaster Fund” was almost inclusively diverted to be invested in government stock.

That cash was spent on more pressing priorities such as crime prevention, healthcare, bigger ministerial limos and alike. So when EQC went to its safe in 2010, all it found were some old IOU’s and a Minister that wanted to create a ‘repair programme’ to slow its capital return down. Politicians seem to treasure EQC’s premium income stream, capital and expense control – it is all useful to them.

The point being there is always someone who wants to use your capital elsewhere. Warren Buffet calls it ‘float’ and he has made a lot of money from it.

The Board and shareholders of Tower failed badly in their capital management, and blaming the government who is equally guilty of its own capital management games with our public insurer is both hypocritical and peeing into the proverbial.

Insurance isn’t just a promise, arguably the product is actually an effective and enduring way of safeguarding sufficient financial resources required to fulfil that promise in a timely fashion.

From history this seems to boil down to both regulating the promise and protecting the resources from the from the wandering hands, interests and aspirations of politicians, boards and shareholders alike.

While I can’t offer any one great solution, I know the prudential supervisor of the private sector is ineffective and often too late to the problem, depending too much on insurers own ‘appointed actuaries’ (as opposed to ‘independent actuaries’).

Meanwhile our public insurer is at the complete mercy of political interests, both before and during a catastrophe, only made worse by the thin veneer of an ‘independent Board of Commissioners’.

In my view the model is more ‘broken’ than is currently discussed, and addressing these fundamental issues should underpin, if you excuse the pun, any review of the EQC Act or wider catastrophe insurance model in New Zealand.

As we approach the 6th anniversary of the Christchurch Earthquake, there are still many thousands of policyholders that are still asking themselves the question: are we still on a promise, or are we just getting screwed?

*Cameron Preston is a Christchurch accountant with outstanding quake claims.

10 Comments

Thank you for the insight. Those creating their own opportunity with other people' money is a problem du jour.

The possible reasons for such behaviour, executed by those believing they are entitled, demands exposure on a wider basis at the public level.

The lie was simply that they could monetarily transform the risky into the riskless, and further that they could do it with almost anything. Read more

Share buyback & excessive dividends AFTER 2010/11 EQ's when Tower must have been aware they did not have anywhere near enough re-insurance & at the same time were assessing claims ridiculously below the true cost of them! Ask yourself, the only way out of that is to make the claimants pay. There it is.

So who was entitled to any ‘excess’ capital first? the policyholder or the shareholder?

Did the policyholder take a bigger risk when buying their promise from Tower than a shareholder did when buying theirs?

I think the answer is clearer when you identify the shareholders with Tower. As in, the shareholders didn't "buy a promise" from Tower, they bought Tower. That's what it means to be a shareholder. The shareholders are Tower.

There was an internal "promise", between the shareholders and the management that they hired to carry out the business (that they would run the business at a profit, and that would be disbursed when available).

With that in mind, when the management "returned capital", passing the available cash across the one-way firewall of limited liability, they were effectively engaging in fraud or theft against the policy holders on behalf of the shareholders. The only defence against this being fraud is the claim that they didn't realise that they weren't going to be able to pay out on the policies (hence the part you describe as "dog ate my homework").

Did they know? Probably. Should they be held accountable? I think so.

Agreed. The rapidly growing awareness of insurers exposure, highlighted by AMI's situation, would have led to some serious thinking. A very creditable game plan resulting from that would have been to run down the capital before the final story became clear, and before anyone realized how dirty the games against policy-holders were going to become. The smart or better informed shareholders back in 2011/2012 would have picked this up, and acted accordingly.

Determining whether Tower directors knew the extent of likely claim reserve movements is hard to pin down. You'd need to know what actuarial assumptions were applied when the overall number was calculated. You'd then have to know what 'adjustments' (if any) were made by the directors, to the actuarial advice.

Claims handlers adjust individual claim reserves as new information becomes available. Every finalised claim makes your overall outstanding event reserve that little bit more reliable.

Stiassny boasts Tower is ahead of the rest of the industry in claim resolutions, which should mean they have the most reliable outstanding reserve figures of all insurers ie, the new incoming claims from EQC should affect Tower proportionately less than other insurers. But is that the case?

The 'new claims from EQC has caught us by surprise line' doesn't stand up to scrutiny as insurers have known for a long time that a large number was still to come.

Towers actuaries should have made provision for this known trend along with all the other permutations they factor in. If they failed to, is Tower taking action against them? If the actuaries did identify this group of claims and Tower hasn't sufficiently provisioned for them, this raises further questions about guidance provided to the market.

Cam Preston is again beating his old drum that insurers should have known the extent of their liabilities when calculating their regional maximum probable loss and buying reinsurance. My lifetime insurance industry immersed view is that it couldn't be done with the modelling tools available at the time. The best reinsurers in the world got it wrong. But the accountant and I will never agree on that so no point in banging on. The argument is really only of academic interest unless, as labcoat asks, should they be held accountable.

My view is you'd struggle to show the industry got its overall values at risk estimations wrong but I wonder about how those estimates were interpreted when decisions were made on how much reinsurance to buy. Which is part of the point Preston is making. Were heroic assumptions made in order to provide a competitive pricing edge, especially on the likelihood of repeat events?

This article, is an eye opener. And while the commenters appear to understand how the Insurance industry works, i cannot help but feel they cannot see the wood for the trees.

Insurance is about offsetting risk. Insurance companies know to a reasonable level of accuracy, through statistical analysis and in the modern age of technology allowing virtually instantaneous communications around the world, the chances of any event occurring.

We can expect low level events to occur relatively frequently, but major ones less frequently to rarely, but they WILL happen. Policy premiums are supposed to account for these, where un expended income left over from covering the frequent events, should be invested to provide for the major events. Buying re-insurance does not meet this requirement! It merely allows insurance companies to avoid their fiduciary responsibilities to their policy holders. For too long Insurance companies, EQC included, have taken as profits, premiums paid in that were supposed to be retained as cover for major events.

Fraud, yes - they claimed to cover events they could not, theft yes - they've taken as income premiums as profit that were supposed to be used as cover for major events.

Murray86. I largely agree with you Murray, but I don't get your objection to using re -insurance. Seems to me that some of these companies should have done more, but cut costs by not getting reinsurance, which put them selves and thus us at risk. Could you explain.

I suspect that the departure of the previous CEO CFO and a Director indicates they knew that Tower management had made some bad decisions and Stiassny as a Liquidator should have calculated the risks given his alleged experience. Yes hold them all to account but won't hold my breath as NZ is the "least corrupt country" !!

Many have tried and failed but you cannot change history and Tower's operational and financial history is far from pretty particularly over the last six years or so.. For better or worse let's all hope that this Canadian lot will take over Tower and provide both a new broom but more importantly capital sufficient to resolve all the longstanding and overdue EQ claims. Other contributors to these columns have complained too about the culture and conduct of certain Tower claims staff, their agents and lawyers. Hopefully they will be the first to go & the resulting new concern will be better for all of us. Wouldn't exactly hold your breath on that though.

This thread of input is revealing but one needs to go back several years to when GPG Plc owned 34% of Tower at a time when they were looking for cash and Tower sold-off subsidiaries and distributed the proceeds to shareholders. Not only did GPG walk away with cash in their pocket but the Christchurch Earthquakes had already occurred and Tower therefore had claims liabilities to identify and apportion for. We all now know this was not done accurately and as a result, claimants have been strung-out and short-changed. Will Canadian owners change this .....no guarantees have been given to outstanding claimants.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.