By Terry Baucher*

There’s a lot to chew over in the Tax Working Group’s (TWG) Submissions Background Paper released on Wednesday.

The relative narrowness of our tax base, the implications of the gig economy and technological change, and the international pressure for lower corporate income tax rates to name a few. For me three areas stand out: the scale and potential impact of demographic changes underway; the potential role of environmental taxes; and the taxation of capital and savings.

But my biggest initial impression is how the decision to exclude consideration of taxing the family home, or the land underneath it from the TWG’s terms of reference, hangs over the paper like Banquo’s Ghost.

A demographic timebomb?

My first major conclusion from the Submissions Background Paper is how much the coming fiscal pressures of an ageing population really need to be kept front and centre when considering changes to the tax system.

The paper begins by setting out key risks and challenges for the tax system over the next 30 years or so. A key baseline is the Government’s fiscal objective of maintaining taxation at the historical level of 30% of GDP over time. At the same time the paper identifies the pressure of changing demographics and an ageing population. For example, for the current year to 30 June 2018 New Zealand Superannuation is expected to cost $13.7 billion, “more than all other benefit payments combined”.

As a result of these pressures, the paper projects the Government will have a primary deficit of 1.2% of GDP by 2030 (about $3.4 billion based on current GDP), rising to 4% of GDP in 2045 or $11.4 billion based on current GDP. Very clearly then as the paper warns;

“If the Government is to continue providing healthcare and superannuation at current levels, then the level of taxation will need to increase, or spending on other transfers or publicly provided goods and services will need to fall.”

Against this backdrop the work of the TWG and the recommendations it will make are hugely important. Change is coming and therefore the tax system needs to be ready for that.

Taxing the environment

The environment is hugely important to the New Zealand economy whether it is liveable or for our two largest export earners agriculture and tourism. New Zealand is committed to reducing net emissions 30% below 2005 levels by 2030 so the Background Submissions Paper suggests;

“Using the tax system to ensure that consumers and producers face the costs of emissions and other environmental harm could be one way we can meet our international obligations.”

The paper also notes that New Zealand had “the second highest level of carbon emissions in the OECD per dollar of GDP in 2017”, an alarming statistic which suggests action is needed sooner rather than later if we are to maintain the idea of being clean and green.

At present environmental taxes such as petrol excise duties and waste levies amount to approximately 4.2% of total tax revenue, or about 1.3% of GDP. This puts New Zealand at the low end compared with other OECD countries. For example, almost 15% of Denmark’s total tax revenue is made up of environmental taxes and these represent just over 4% of GDP. Across the Ditch, Australian environmental taxes are just over 2% of GDP, representing 8% of all taxation.

A recent OECD paper noted that in 2015, outside of road transport, 81% of emissions were untaxed. The report concluded tax rates were below the low-end estimate of climate costs (€30 per tonne of CO2) for 97% of emissions. New Zealand at €0.48 per tonne of CO2, was sixth from bottom of the 42 countries surveyed.

There would therefore appear to be significant opportunity for shifting some part of the tax burden onto environmental taxes. However, as both the Background Submissions Paper and the OECD notes many environmental taxes are “poorly designed and targeted.”

Wealth inequality and savings

The TWG’s terms of reference may have excluded taxing either capital gains from the family home or the land underneath the family home, but considering the taxation of savings is within its remit. So too is the issue of inequality and the Background Submissions Paper has a wealth (pun intended) of charts illustrating the issue of income and wealth inequality. (See Figures 12-19 between pages 33 and 38 of the report).

Ominously, the paper comments that over the past three decades the “inequality-reducing power of the tax and transfer system on market income inequality has steadily declined”. Furthermore, the inequality-reducing power of the tax-benefit system is now below the OECD average.

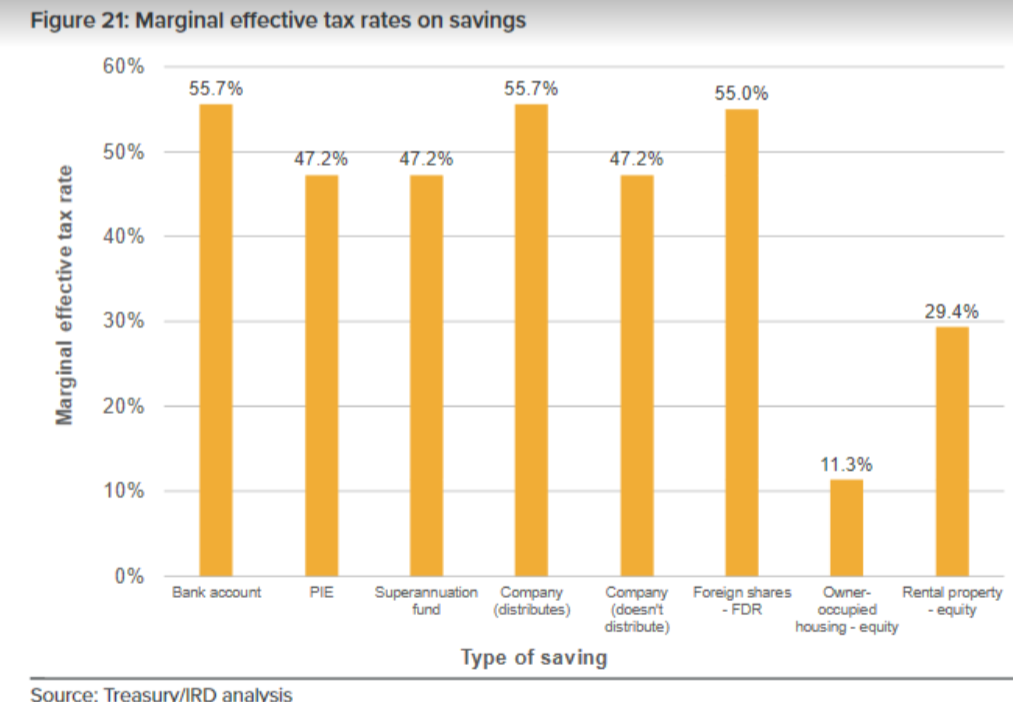

Tied into the issue of inequality is the taxation of household savings. It’s here that the impact of the terms of reference loom largest. After assuming a risk-free rate of return of 3%, inflation of 2% and a 33% tax rate to determine a marginal effective tax rate, the Background Submissions Paper then applied this to calculate the marginal effective tax rates of various asset classes. Its conclusion: “owner-occupied and rental housing is undertaxed relative to other assets.” The extent of the under-taxation is starkly illustrated by Figure 21 (reproduced below).

At 55.7% the marginal effective tax rate on bank savings is almost five times that of the 11.3% rate applicable for owner-occupied housing equity and nearly double the 29.4% rate for rental property.

The Reserve Bank estimated the value of housing as at 30 September 2017 to be over $1 trillion. Even excluding residential rental property (perhaps a third of the total), this is a huge amount of capital to be left essentially untaxed. The holders of that property are mostly older and wealthier, a growing number of which are receiving New Zealand Superannuation. As Andrew Coleman noted last year, changes to the tax system in the late 1980s established a huge incentive in favour of housing. This created an inter-generational timebomb which will need to be defused at some point.

Much of the immediate debate on the Background Submissions paper has been about the efficacy and impact of a capital gains tax, but there’s been little discussion about the ongoing fiscal impact of continuing to exclude maybe $700 billion of capital from taxation with potentially very adverse outcomes for future generations.

Overall the Submissions Background Paper includes plenty of thought-provoking material to consider. The paper also underlines what was apparent from the outset; excluding the taxation of the family home created a big hole at the heart of the review.

Whatever the final recommendations of the TWG are for addressing the future sustainability of the tax system there’s a danger it will be found as Macbeth warned after killing Duncan to “have scotched the snake, not killed it”. Only time will tell.

------------------------------------

*Terry Baucher is an Auckland-based tax specialist and head of Baucher Consulting.

(Submissions to the Tax Working Group close on April 30 and can be made online here).

45 Comments

you can not tax your way to equality, the stick approach does not work

by the same token removing the tax burden on the lower incomes would work, and i would favour the first (up to the amount paid on the dole) as tax free.

that would reduce government administration, and costs

WFF is an example of badly designed policy, how much of my dollar is eaten up by government administration costs before it is redistributed?

With modern computers it is possible WFF is not a major admin cost. However some one will know what how the cost is split welfare : admin. The admin cost is not just the financial element but the lost opportunity of using the same investment of money and people in a way that is productive for NZ.

Maybe the problem with WFF is the policy and its critics are not in the segment of society that benefits. There seems to be nobody willing to push the advantages of a universal child benefit; surely the cleanest way of investing in NZs future.

You are right that creating a tax free bracket would be effective, but you certainly can tax your way to better equality. If the broadest shoulders carry the load, that improves equality. It's not a stick, it's just those who are able doing their share.

I'd recommend some form of Land Value Tax to be the best solution to improve equality.

I also agree WFF is bad. You're better off with a comprehensive system like an NIT or a UBI to cover all bases with minimum administration and Kafkaesque harassment.

As long as you don't end up in a situation where people are forced into hardship because they own a house on valuable land but don't earn a great income.

At the moment it's basically been a case of making others' lives hard to protect these folks - including by keeping rates-funded infra investment under what it should be and (under the last govt.) even looking to circumvent the council's debt ceiling to put the burden on others.

I think we need to be more realistic about the fact that if being a global city means affordability issues for some young folk, surely being a global city also means that it may not be easily affordable to own a valuable piece of land in the central city without some correlating form of income.

We have to question the base assumption there that the second should be aimed for while the first should not - and that someone else should be funding infrastructure investment rather than the owners of the land.

What are you on about? Of course you can tax your way to equality. What you almost certainly can't do is develop a system which both delivers equality and maintains the incentive on individuals to work and create wealth.

The above makes the incentive clear. If I have savings then I'm best to 'invest' them in my personal residence. Maybe the marginal effective tax rate needs to be lowered on bank accounts so I save more rather than spend? As for NZ Superannuation, if it's so unaffordable, why did the COL double down with their Winter power giveaway? Plus how much tax does the Government receive back from the aged on their payment?. GST is a given and there must be other taxes as well.

The introduction of any form of wealth tax that excludes the family home or the land beneath it, and that also excludes inheritance tax (and presumably gift tax), is fundamentally unfair to all who are not yet home-owners, or who are home-owners in an area where housing has little value. It also seems likely to continue the incentive to invest in the family home rather than other forms of investment. This will push prices higher, ever further beyond the reach of those who do not have the means to buy into the housing market.

But there is still a way to use the family home to reduce, or even reverse, the growth in inequality between home-owning haves and non-home-owning have-nots. A person could be allowed a tax-free investment of an amount equivalent to, say, the value of the average inner-city Auckland house ($1 million, $2 million: take your pick). But offset this against the person's tax-haven share in a family home and the land beneath it. Let’s say every taxpayer is entitled to tax-free savings or investment (in any vehicles in New Zealand or overseas) of $1 million minus the value of their owner-occupied-home investment. So the single person who owns no home would be able to grow his or her savings tax-free till it reached $1 million; the married half-owner of the $100,000 home in Raetihi would be able to invest $950,000 and pay wealth and income tax only on the capital above that; the half-owner of the $3 million house in Remuera would incur wealth tax on every dollar invested elsewhere, as his or her $1.5 million share surpasses the tax-free investment allowance.

Such a tax-free allowance would reduce the disparity between the capital-growth advantage of investing in the family home and the land beneath it (excluded from the tax reform group’s consideration) and other forms of investment. This would encourage New Zealanders to look beyond the family home to more productive investments, which would help to reduce the rate of price increase in homes, and people who did not yet have enough money to buy a house, or who did not want to own a house, would enjoy tax advantages similar to home-owner-occupiers.

An obvious disadvantage is that the lauded simplicity of New Zealand’s tax system would disappear: the Inland Revenue Department would need to know the value of each taxpayer’s share of ownership of the house in which he or she lived, then assess how much tax from the taxpayer’s investments to collect or reimburse. However, the increased cost of a more complicated inland revenue collection might be a price worth paying to reverse the growing inequality among New Zealanders, with its unhappy social consequences.

Another difficulty would be the revenue shortfall if savings and investments now taxed cease to be taxed. The Government precludes inheritance taxes and any increase in income taxes or GST, so it must look elsewhere to maintain its tax take: environment taxes, transaction taxes, and perhaps the abolition of charities' tax exemptions.

My home has a supposed value of $2,500,000 jointly held. The home is in the top percentile of NZ values and you still can't get me. Seems like a lot of work to do what?

You have noticed that our tax system is skewed towards Auckland. So I have my wealth tied up in an average Auckland house and escape the taxes that would be imposed if it was in any other significant investment and I am surrounded by neighbours receiving accommodation allowances ($2b per year and increasing in April). The rest of the country is subsidising Auckland but as one of them I can assure you no Aucklander is saying 'we will pay for all our new infrastructure'; no they want the government to contribute to CRL, a new Harbour bridge, etc.

Little surprise that Auckland is sucking in new-comers from NZ and abroad.

The solution is amazingly simple , equitable , and very cheap to implement .... A comprehensive land tax !

... and I'd go one step further , and apply it to all of our nation's natural resources ... vest the ownership back to the crown , and annually levy all who use or have the use of our land , our water , our air ... no more free aquifer water for bottling plants shipping it off to China ... no more dirty dairying pooping up our fresh water systems ... a fart tax on livestock for their methane emissions ...

Let's clean up this country ... and get back to leading the world in " 100 % pure "

User pays !

Does "all who have the use of our air" include people who breathe?

"nothing can be said to be certain, except death and taxes."

I am just waiting for the tax on the dead.

After all, we could be better put to use as organic fertilizer rather than Cremated or just dumped in a hole. Many countries already charge fees to remain buried to alleviate overcrowding. I am sure we can change the application slightly.

The way the future is looking, dying might soon be something saved only for the rich as well.

Not just demographic change

Employment numbers will decrease as AI & robotics take over many jobs

You won’t need to buy the robots either they are available on lease at low rates here already

The tax system will require something far more forward thinking than this as the employment paradigm will change significantly. Law , Accountancy , Architectural all are just some of the professions that will not require

the same numbers of human employees either and it’s happening here now.

Why does 'aging population' sound so bad? Why not 'population increasing in wisdom'?

I believe I have greatly benefited from the so called aging population. When I was a young typewriter mechanic in the eighties there was a lot of talk of workers being over the hill when they were forty plus. This seems absurd now. An aging population and shortage of young workers is a good thing for many in society. There appears to be a lot less ageism nowadays and over sixty is now the new over forty.

Because there is no sign of increased wisdom, just increased need, expectation and demands. So the current numbers are around 13.6%? growing to 26%? (working from memory) and this means a huge increase in public health demands on numbers alone let alone advances in healthcare driving up per capita costs And yes I mean demands, grey power etc is only going to get more powerful politically as its numbers double while many young ppl dont seem to vote.

Steven: I only need one sign to prove you wrong. If you think I'm lacking in wisdom now well 50 years ago I was far dumber. In those days I had made no mistakes to learn from.

I've spent 50 years wondering why retirement and pension were not linked to life expectancy and I am still wondering. As you point out I expect many more pension years than I did when I started work.

Assuming you are under 50 you will have all the political fun when life expectancy can be bought and all the wealthy who influence our politicians will be paying to add another decade to their existence.

Right, seems like a consensus is growing that there's a lot of remedial action needed with the tax system.

Where the hell were National under Key and English? Polish ship yard?

Premature speculation. Put it to the electorate and then we will see where the consensus is. I'm all for someone else paying more as I already pay a lot.

First poster implied/stated,

a) there a problem, I would suggest clearly there is and a growing one, that is relly pretty much a fact as we can see it mathematically.

b) said "growing" not a "majority"

c) Your replay is not enough voters see there is a need to fix / change things

None of these are in-correct I suggest, stupid, yes.

d) "Pay a lot", depends if we are talking a lot in terms of a % of spare/disposable income or just a lump of $s you think is "enough" sounds like the latter to me. ie the poor in effect have almost none or no disposable income and hence in effect their % contribution is huge.

National made it worse by increasing GST and removing the top income tax bracket, which loaded up the poor with more of the tax burden.

Don't forget the 1.5 billion per year paid out by the poorest members of our society as tobacco excise. All highly regressive. Particularly in the context of John Key's 10 million tax free capital gain, made by selling his mansion to a Chinese citizen.

What is interesting is they got away with it. What is even more interesting is I dont see Labour backing it out right off the bat.

The marginal effective tax rates on saving shows very clearly the reason for New Zealand's difficulties. Decades of over taxation of savings relative to income. Who would have thought?

It makes complete sense to me, less savings means we have to "import capital" to pay for our consumption goods. This is the current account deficit, whereby as a nation we have spent more than we earn every year since 1973. The current account deficit has to be balanced by an equal capital account inflow. We either have to borrow more (allowing us to bid up house prices against each other) or sell assets to overseas owners.

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-current-account

The question is, what did we do with all that extra tax money in the meantime?

We spent it.

Yup, looks like they need to reduce the tax on all other savings classes until they match the marginal effective tax rate on owner occupied housing.

Thereby encouraging sensible behavoiur, ie saving, rather than borrowing (to bid up house prices).

You can only save if you have "excess" money. Lowering the rates won't fix the inherent lack of wage growth.

in which cases adding taxes where there are no taxes achieves the same effect.

which in effect means no tax at all.

We absolutely must not encourage savings. Increased savings = increased inequality.

Just imagine that 2 fresh graduates work for a year for $45,000 each. One saves $10,000 and the other takes a holiday to Europe that costs $10,000. The result is $10,000 of wealth inequality between them. If neither of them saved the inequality would be lower

I will be interested to see how environmental taxes would work unless there will be a reward for good work as there is in many other countries. David Parker has come out and started talking about Green House Gases which I would have thought was the domain of James Shaw as Minister of Climate Change. James Shaw has been out on farm talking to farmers, David Parker has being notable for his absence. Are we going to see a clash with these two? Parker displays anti farming sentiments, especially dairy, whereas Shaw is willing to at least educate himself on what is actually happening in this space on farms and in regards to research.

In most countries that have environment taxes they also pay rewards for environmental work e.g. in farming numbers of trees, fallow land etc. A UK supermarket buyer was visiting kiwi farmers recently who have a supply contract with the supermarket. The buyer was all doom and gloom for the UK farming industry as so many farmers are only viable because of subsidies - especially environmental subsidies and once Brexit happens the subsidies will potentially fall away. It will be interesting to see how this settles out.

Many UK farms have been so sub-divided that they are too small to be viable and hence need huge subsidies, provided by the EU....when that goes.

I dont see there is a clash looming between the 2 myself. If anything maybe and its a huge maybe Labour is finally starting to think about "green" things, I wont hold my breadth though.

I abhor environmental taxes. Yes, they change behavior - but not in the way we want. Greed will always win.

Two things will happen:

1. The "environment" becomes to expensive to use for some/many (i.e. inequality increases) and/or

2. The profit from destruction exceeds that of the tax, thus "better" to destroy it.

Same for the "rewards"

Do we really want to destroy the entire amazon/Borneo/insert ecologically important forest here, because it is being balanced/rewarded (Carbon footprint wise and/or financially) by a good ol' Pinus Radiata plantation in NZ?

The reason there is such a high marginal Tax rate on Bank acct. savings is that there is NO depreciation allowance for the impact of inflation.

The natural solution would be to allow for depreciation... (this would align with "reality").

They will never allow this, as it will result in a loss of tax income.

Instead , they will want to tax the inflationary gains of other assets.... like housing. ... thus , bringing it all into line.

rather than an environment tax, why not simply focus on reducing pollution..?

I'm contemplating a bizarre future where a nest egg raiding tax regime incentivises me to trade my more than adequate home for a much flasher one, encourages me to convert equity investments in NZ companies to cash that I gift to my kids so they can also buy more expensive houses, and where the smart decision is to accelerate rather than prudently manage the spending run down rate of the remaining capital.

I would like to see a tax-free income threshold-say $10,000 per person on earned income. it would not apply to rent or dividends. Thus,as a retiree with both rental and dividend income,I would not benefit. I don't know what this might cost,but I would have no objection to the top tax rate return to where it was before Key cut it.

I would pay more tax,but would regard that as a small price to pay for a more equal society.

Imputed rental value of owner occupied housing (net of mortgage interest and some expenses) should be taxed as income. This was the case in the UK until the 1960's/70's, and in various forms in many other countries. It's explained on the internet - just Google it. No great mystery. The NZ policy makers are undoubtedly quite aware of it but choose to overlook it because it is politically very contentious. Clearly, failure to tax it amounts to subsidy to owner occupiers effectively capitalised into higher house prices. It is inequitable that rent payers effectively do pay tax at income tax rates on the rental value of the property they occupy (they have to find a gross amount of income and pay tax on that before having a net amount of income with which to pay rent). Until the 1980's the scale of subsidies tended to be received by a significant proportion of rent payers (i.e. various kinds of government social transfer payments received by beneficiaries) tended to complicate the inequality equation. But those subsidies have since greatly reduced - thus greatly reducing that complication. Introduction would broaden the tax base, remove a subsidy capitalised into higher house prices and remove a gross inequity. Introduction could be "neutral" on total tax take - through reductions in direct taxes - e.g. in GST. Quite practical to introduce this without being part of general wealth tax.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.