In 1999, I began saying the tech bubble would eventually spark a recession. Timing was unclear because stock bubbles can blow way bigger than we can imagine. Then the yield curve inverted, and I said recession was certain. I was early in that call, but it happened.

In late 2006, I began highlighting the subprime crisis, and subsequently the yield curve again inverted, necessitating another recession call. Again, I was early, but you see the pattern.

Now let’s fast-forward to today. Here’s what I said last week that drew so much interest.

Peter [Boockvar] made an extraordinarily cogent comment that I’m going to use from now on: “We no longer have business cycles, we have credit cycles.”

For those who don’t know Peter, he is the CIO of Bleakley Advisory Group and editor of the excellent Boock Report. Let’s cut that small but meaty sound bite into pieces.

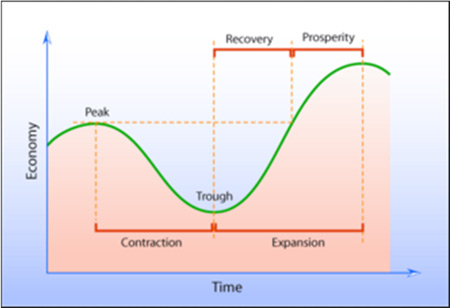

What do we mean by “business cycle,” exactly? Well, it looks something like this:

Photo: Wikispaces (Creative Commons license)

A growing economy peaks, contracts to a trough (what we call “recession”), recovers to enter prosperity, and hits a higher peak. Then the process repeats. The economy is always in either expansion or contraction.

Economists disagree on the details of all this. Wikipedia has a good overview of the various perspectives, if you want to geek out. The high-level question is why economies must cycle at all. Why can’t we have steady growth all the time? Answers vary. Whatever it is, periodically something derails growth and something else restarts it.

This pattern broke down in the last decade. We had an especially painful contraction followed by an extraordinarily weak expansion. GDP growth should reach 5% in the recovery and prosperity phases, not the 2% we have seen. Peter blames the Federal Reserve’s artificially low interest rates. Here’s how he put it in an April 18 letter to his subscribers.

To me, it is a very simple message being sent. We must understand that we no longer have economic cycles. We have credit cycles that ebb and flow with monetary policy. After all, when the Fed cuts rates to extremes, its only function is to encourage the rest of us to borrow a lot of money and we seem to have been very good at that. Thus, in reverse, when rates are being raised, when liquidity rolls away, it discourages us from taking on more debt. We don’t save enough.

This goes back farther than 2008. The Greenspan Fed pushed rates abnormally low in the late 1990s even though the then-booming economy needed no stimulus. That was in part to provide liquidity to a Y2K-wary public and partly in response to the 1998 market turmoil, but they were slow to withdraw the extra cash. Bernanke was again generous to borrowers in the 2000s, contributing to the housing crisis and Great Recession. We’re now 20 years into training people (and businesses) that running up debt is fun and easy… and they’ve responded.

But over time, debt stops stimulating growth. Over this series, we will see that it takes more debt accumulation for every point of GDP growth, both in the US and elsewhere. Hence, the flat-to-mild “recovery” years. I’ve cited academic literature via my friend Lacy Hunt that debt eventually becomes a drag on growth.

Debt-fueled growth is fun at first but simply pulls forward future spending, which we then miss. Now we’re entering the much more dangerous reversal phase in which the Fed tries to break the debt addiction. We all know that never ends well.

So, Peter’s point is that a Fed-driven credit cycle now supersedes the traditional business cycle. Since debt drives so much GDP growth, its cost (i.e. interest rates) is the main variable defining where we are in the cycle. The Fed controls that cost—or at least tries to—so we all obsess on Fed policy. And rightly so.

Among other effects, debt boosts asset prices. That’s why stocks and real estate have performed so well. But with rates now rising and the Fed unloading assets, those same prices are highly vulnerable. An asset’s value is what someone will pay for it. If financing costs rise and buyers lack cash, the asset price must fall. And fall it will. The consensus at my New York dinner was recession in the last half of 2019. Peter expects it sooner, in Q1 2019.

If that’s right, financial market fireworks aren’t far away.

Corporate Debt Disaster

In an old-style economic cycle, recessions triggered bear markets. Economic contraction slowed consumer spending, corporate earnings fell, and stock prices dropped. That’s not how it works when the credit cycle is in control. Lower asset prices aren’t the result of a recession. They cause the recession. That’s because access to credit drives consumer spending and business investment. Take it away and they decline. Recession follows.

If some of this sounds like the Hyman Minsky financial instability hypothesis I’ve described before, you’re exactly right. Minsky said exuberant firms take on too much debt, which paralyzes them, and then bad things start happening. I think we’re approaching that point.

The last “Minsky Moment” came from subprime mortgages and associated derivatives. Those are getting problematic again, but I think today’s bigger risk is the sheer amount of corporate debt, especially high-yield bonds that will be very hard to liquidate in a crisis.

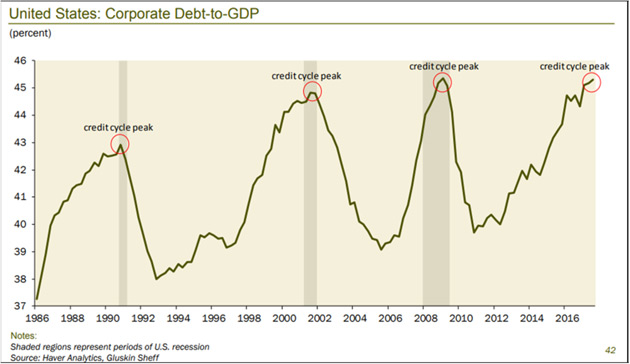

Corporate debt is now at a level that has not ended well in past cycles. Here’s a chart from Dave Rosenberg:

Source: Gluskin Sheff

Source: Gluskin Sheff

The Debt/GDP ratio could go higher still, but I think not much more. Whenever it falls, lenders (including bond fund and ETF investors) will want to sell. Then comes the hard part: to whom?

You see, it’s not just borrowers who’ve become accustomed to easy credit. Many lenders assume they can exit at a moment’s notice. One reason for the Great Recession was so many borrowers had sold short-term commercial paper to buy long-term assets. Things got worse when they couldn’t roll over the debt and some are now doing exactly the same thing again, except in much riskier high-yield debt. We have two related problems here.

- Corporate debt and especially high-yield debt issuance has exploded since 2009.

- Tighter regulations discouraged banks from making markets in corporate and HY debt.

Both are problems but the second is worse. Experts tell me that Dodd-Frank requirements have reduced major bank market-making abilities by around 90%. For now, bond market liquidity is fine because hedge funds and other non-bank lenders have filled the gap. The problem is they are not true market makers. Nothing requires them to hold inventory or buy when you want to sell. That means all the bids can “magically” disappear just when you need them most. These “shadow banks” are not in the business of protecting your assets. They are worried about their own profits and those of their clients.

Gavekal’s Louis Gave wrote a fascinating article on this last week titled, “The Illusion of Liquidity and Its Consequences.” He pulled the numbers on corporate bond ETFs and compared it to the inventory trading desks were holding—a rough measure of liquidity.

Louis found dealer inventory is not remotely enough to accommodate the selling he expects as higher rates bite more.

We now have a corporate bond market that has roughly doubled in size while the willingness and ability of bond dealers to provide liquidity into a stressed market has fallen by more than -80%. At the same time, this market has a brand-new class of investors, who are likely to expect daily liquidity if and when market behavior turns sour. At the very least, it is clear that this is a very different corporate bond market and history-based financial models will most likely be found wanting.

The “new class” of investors he mentions are corporate bond ETF and mutual fund shareholders. These funds have exploded in size (high yield alone is now around $2 trillion) and their design presumes a market with ample liquidity. We barely have such a market right now, and we certainly won’t have one after rates jump another 50–100 basis points.

Worse, I don’t have enough exclamation points to describe the disaster when high-yield funds, often purchased by mom-and-pop investors in a reach for yield, all try to sell at once, and the funds sell anything they can at fire-sale prices to meet redemptions.

In a bear market you sell what you can, not what you want to. We will look at what happens to high-yield funds in bear markets in a later letter. The picture is not pretty.

To make matters worse, many of these lenders are far more leveraged this time. They bought their corporate bonds with borrowed money, confident that low interest rates and defaults would keep risks manageable. In fact, according to S&P Global Market Watch, 77% of corporate bonds that are leveraged are what’s known as “covenant-lite.” We’ll discuss more later in this series, but the short answer is that the borrower doesn’t have to repay by conventional means. Sometimes they can even force the lender to take more debt. In an odd way, some of these “covenant-lite” borrowers can actually “print their own money.”

Somehow, lenders thought it was a good idea to buy those bonds. Maybe that made sense in good times. In bad times? It can precipitate a crisis. As the economy enters recession, many companies will lose their ability to service debt, especially now that the Fed is making it more expensive to roll over—as multiple trillions of dollars will need to do in the next few years. Normally this would be the borrowers’ problem, but covenant-lite lenders took it on themselves.

The macroeconomic effects will spread even more widely. Companies that can’t service their debt have little choice but to shrink. They will do it via layoffs, reducing inventory and investment, or selling assets. All those reduce growth and, if widespread enough, lead to recession.

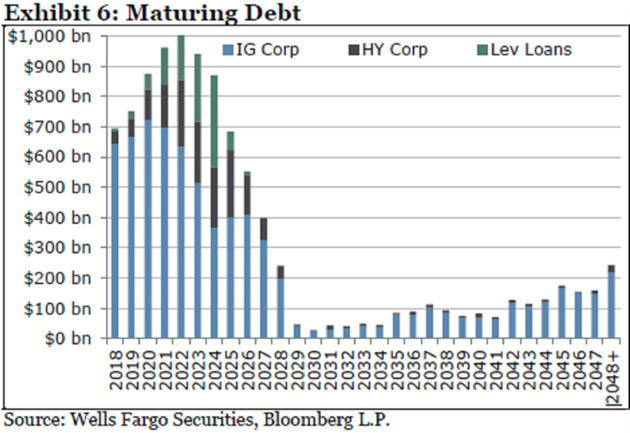

Let’s look at this data and troubling chart from Bloomberg:

Companies will need to refinance an estimated $4 trillion of bonds over the next five years, about two-thirds of all their outstanding debt, according to Wells Fargo Securities. This has investors concerned because rising rates means it will cost more to pay for unprecedented amounts of borrowing, which could push balance sheets toward a tipping point. And on top of that, many see the economy slowing down at the same time the rollovers are peaking.

“If more of your cash flow is spent into servicing your debt and not trying to grow your company, that could, over time—if enough companies are doing that—lead to economic contraction,” said Zachary Chavis, a portfolio manager at Sage Advisory Services Ltd. in Austin, Texas. “A lot of people are worried that could happen in the next two years.”

The problem is that much of the $2 trillion in bond ETF and mutual funds isn’t owned by long-term investors who hold maturity. When the herd of investors calls up to redeem, there will be no bids for their “bad” bonds. But they’re required to pay redemptions, so they’ll have to sell their “good” bonds. Remaining investors will be stuck with an increasingly poor-quality portfolio, which will drop even faster. Wash, rinse, repeat. Those of us with a little gray hair have seen this before, but I think the coming one is potentially biblical in proportion.

Casey Jones via Wikimedia Commons

Blowing the Whistle

As you can tell, this is a multifaceted problem. I will dig deeper into the specifics in the coming weeks. The numbers seem unbelievable. I truly think we are headed to a staggering credit crisis.

I began this letter describing the coming events as a train wreck. That comparison came up when my colleague Patrick Watson and I were on the phone this week, planning this series of letters. Patrick and his beautiful wife Grace had just come back from Tennessee, and he told me about visiting the Casey Jones birthplace museum in Jackson.

For those who don’t know the story or haven’t heard the songs, Casey Jones was a talented young railroad engineer in the late 1800s. On April 30, 1900, Casey Jones was going at top speed when his train tragically overtook a stopped train that wasn’t supposed to be there.

Traveling at 75 miles per hour, Jones ordered his young fireman to jump, pulled the brakes hard, and blew the train whistle, warning his passengers and the other train. Later investigations found he had slowed it to 35 mph before impact. Everyone on both trains survived… except Casey Jones.

His heroic death made Jones a folk hero to this day. Many songs told the story and even the Grateful Dead and AC/DC paid tribute decades later. (Trivia: He actually tuned his train whistle with six different tubes to make a unique whippoorwill sound. So, when people heard his train whistle, they knew it was Casey Jones.)

Right now, the US economy is kind of like that train: speeding ahead with the Fed only slowly removing the fuel it shouldn’t have loaded in the first place and passengers just hoping to reach our destination on time. Unfortunately, we don’t have a reliable Casey Jones at the throttle. We’re at the mercy of central bankers and politicians who aren’t looking ahead. They can’t simply turn the steering wheel. We are stuck on this track and will go where it takes us.

------------------------------------------

*This is an article from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. This article first appeared here and is used by interest.co.nz with permission.

90 Comments

A self-propelled and the US and USD centralized circle:

US prints more USD ---> More USD get spent on the US military ---> More advanced US military guarantees the superiority of the US ---> US prints more USD and so on....

This circle is now slowly breaking down.....

It can't break until they have no more "Enemies".

I think they even realise this, hence the war in Afghanistan is taking 4 times longer than all of WW2.

Thats why it's called a war on "Terror". When you kill one "Terror" you only need to create another one and off you go. This "war" is designed to cost money, lots of it and they are being very successful.

... the Nazis were able to mobilize their troops and tanks , then roar across most of western Europe , conquering and slaughtering as they went .... then barrel headlong into the middle of Russia , whilst bombarding London at the same time ....

And all in far less time than its taken us to re-build one modest sized city , Christchurch ...

... and they maintained a smart military look , attired by Hugo Boss .... not a single hi-viz yellow vest in sight ...

Many have said maybe the catalyst for GFC2 will be coporate debt

I suppose it’s his daughter writing this these days while he plays golf

Broadcom's scuppered $US 100 billion bid to buy Qualcom is one helluva lot of corporate debt ....

... and , after Trumpy blocked that deal ( too many Singaporeans with Chinese sounding names ) , Qualcom themselves borrowed heavily to swallow NXP Semi .... for a cool $US 44 billion ....

Gosh ... a $ billion here .... $ 10 billion there ... $ 100 billion .... it soon starts to add up to some real serious amounts of credit ...

I was reading a fascinating article today. Professor Steve Keen wrote a 2017 submission to the British Treasury Committee on household finances imploring the government not to run a surplus. A government deficit will mitigate the effects of a private credit contraction.

Quite remarkable that the Deutsche Bundesbank put out this youtube video. There's a battle of ideas going on and some heavyweights are now backing modern monetary theory.

Fat Pat

There are differing opinions by the financial experts primarily because the world has never had so much debt

Nobody has a clue how to unwind from these extreme debt levels hence the sometimes radically differing opinions on the subject.

Some commentators here on this blog fail to understand that regardless of what happens to the NZ dollar

NZ is still a safe haven. The only corollary might be the extreme property market debt in NZ but even that may prove manageable

Some commentators here on this blog fail to understand that regardless of what happens to the NZ dollar

NZ is still a safe haven. The only corollary might be the extreme property market debt in NZ but even that may prove manageable

Care to explain why or is that just your sentiment?

NZ's debt is concentrated in property, the problem is when one part of this global house of cards fall so do all the rest and that incls NZ housing values.

No I dont agree NZ is a safe haven in a financial context that is your un-supported opnion IMHO, but please do justify it and I'll consider changing my position if your facts and data add up.

For those interested in the song mentioned above. We may as well Rock On, until the derailment! https://www.youtube.com/watch?v=Cm4hkZ0ooYE

Interesting article. Not convinced by exhibit 6 however. Wouldn't this graph always take this shape, historically and in the future, based on 'average' bond maturities of about 5 years?

Exactly

Of course others will state the sky is green

Good read. Thoughtfully I'd suggest that this is only true if income growth remains low for ordinary consumers. When income out-paces debt credit risk recedes but no one seems to have an eye on all of the gauges.

First of all an excellent article.

Squishy: income growth is flat. In the US incomes have not grown much since the 70's! In New Zealand it is barely above inflation for the last 30 years.

You see signs of income growth lagging everywhere. Europe, the US, South America, China.

The housing "crisis" in New Zealand is a great sign. There is not a shortage of housing in New Zealand, there cannot be or rents would have moved in line with capital appreciation, over the last 20 years. How can you have a shortage of something and the cost to buy it sky rockets but the cost to rent it stays flat?! If there is a shortage of something than surely the cost to rent or buy should move more or less in line with one another. The Government paid 2 billion in housing subsidies last year and the people applying for housing assistance is increasing (which is a subsidy for inflated house prices in itself, and a disincentive for companies to pay more as well). The knee jerk reaction is to say that there aren't enough houses and we should build more houses. I heard Mr Twyford say yesterday that in Auckland, just to stand still, we needed 12000 houses built last year and we only built 8000 homes. No one seems to call people out when they say these things, it's absurd! Lets say 2 people live in a house. Where are these 8000 newly homeless people? And that is just last year? If building has been as short as everyone seems to agree it is, there must be tens of thousands, even hundreds of thousands of people with no homes no? Where are they all? If they are all sleeping in cars or garages in poorer areas.....it would still be bloody obvious. I mean come on!! Why isn't their lack of housing causing them to flood the rental market and send rents skyrocketing like house prices have? I would say because they don't have enough income either way. You have to have money to buy, even leveraged. You can be poor but still rent. But if rent goes up a little bit and your wages are flat......then you need help from the government for rent or you get food from the city mission because you have spent all your money on rent. The landlord can only move rent up a little bit, and the government and charities support the difference. And business pays the same. Doesn't this better fit what we are seeing?

So how about this scenario....house prices are in a bubble. New Zealanders are obsessed with home ownership, so they don't question it too much. Prices have grown far faster than inflation and far faster than nominal GDP. Historically they move roughly in line with these figures.

So housing is in a bubble and a lot of our GDP "growth" has come from this and associated credit growth. It hasn't come from business investment or stockmarket investment, or some paradigm-shifting technology or anything that might create true wealth and allow us to pay people more. So we don't. Wage growth has remained flat.

So you have people maintaining their standard of living by selling houses to each other and spending the credit created. This appears as GDP growth, GDP being a worthless measure of wealth in any case but that is a separate argument. So everyone thinks things are going fine. Wages stay largely flat and are completely left behind by credit growth. At the upper / middle end people are willing to accept flat wage growth because they feel a wealth effect from their house prices going up (even at this historic low in house ownership it is still around 62% so a clear voting majority). At the middle / lower end they don't own but they want to (it's clearly an easy way to make money) so they don't want anything to change in case they miss out. And at the low end they are poor and have no voice and are forced into benefits, subsidies and handouts so big companies don't have to pay them enough to cover their expenses. In all cases there is no pressure on wage growth.

Look at the kiwi fruit growers in the news recently. They can't find labour so whats their solution? Not pay more they ONLY pay the minimum wage. It's get the government to change rules so that migrant workers can do it. Put pressure on WINZ to make unemployed do it. Get National Radio to report on it. Label local youths as useless and lazy (perhaps they are I don't know). But surely, in a functioning market, if there is a lot of demand for labour the price should go up. The simple fact is kiwi fruit growers need their fruit picked. The market is telling them the price they are offering for labour is not high enough for them to get the fruit picked. So they have to pay more. Maybe that is double the minimum wage, maybe more, maybe less. But instead of meeting that price the government gives them a way to pay an artificially low price for the labour. Does this sound stupid to anyone else?! Especially given that the same government wants to drastically increase minimum wages? Now I am going to speculate a bit but how much of those kiwifruit are backed by credit? If they are in line with other parts of the agricultural sector and given the damage wrecked by PSI not long ago than it is fair to assume leverage is pretty high. So we have a product that is leveraged to some extent and is experiencing massive demand and yet STILL wages at the bottom are not being pushed up. I'm no communist but it seems labour is not being treated fairly here. As it hasn't been for 40 odd years. % of companies earnings going to labour has been steadily decreasing since the early 80's (although only at the bottom, CEO payments have completely blown out) while % going to shareholders has been increasing. And it is creating inequality. And resentment.

We have a leftist government promising to build affordable housing that is clearly not affordable for most people!! And still no one questions the ridiculous "there are not enough houses" narrative. Or what it really means to owe 750k. And the status quo continues.

Eventually we reach a point where credit begins to choke the economy. There is nothing left to buy and assets are so inflated in price and the returns are so small nobody wants to buy anything. "Pushing on a string" is my favourite description of the effect of too much debt. It's what we are starting to see here. We have massive amounts of debt and by personal debt measure New Zealand is down with the PIGS. Make no mistake we are in trouble here.

I think the mother of all credit crises is the least of it. The sort of situation we have seen since the GFC favours those with access to credit, who are generally the already well off. They use that cheap credit to make themselves wealthier and inequality increases. It is inequality that is always the most dangerous thing for societies. People will accept being poor if the wealthy aren't that much wealthier. But you can understand the frustration of the person working gruelling work for long hours, for the minimum wage, unable to make ends meet, while someone else is making a lot more money by not really doing or creating anything. Just moving credit around. "How is that fair?" they ask. I don't have a good answer for that question. Does anyone else?

Everyone will eat bread for awhile but eventually they will want some of that cake they see others eating too. And if the person who has eaten cake the whole time tries to tell them they can't have any..... or they should just be happy with bread.....well, at some point, they will smash that person and everything they stand for.

This is how humans work, this has all happened before, many times. And the tension is building again, the rise of populist politics shows that. I am sure John will talk more of this further in his series.

Be wary people. Losing money might be the least of our problems.

A very thoughtful comment. I think the only way to solve the problem is to bail out the people. Not the banks.

How do you bail out the people? You give them each a house, for free. After that, the poor can then save a much more significant portion of their income, and invest a portion of that into the productive parts of the economy.

Everyone strives to own a property or two in NZ. It's the biggest investment class here. Because of this, there is this ridiculous massacre going on with people taking on jumbo debt, stampeding over one another and robbing each other blind to buy... ... a clapped out weatherboard house in Bromley, Christchurch.

The responsible thing to do is to bail out the poor, by simply giving them each a house. We may have to increase our sovereign debt to do so, but the savings could be found by the improvements in our health and crime statistics as a result of improving the lives of many poor.

I think a universal basic income is a better solution and it has very good economic foundations.

In the meantime, why tax the poor? It seems pointless, there should be a zero band between 0 - 15k, or something like that. Otherwise we just take with one hand and give back with the other....and spend a lot of money on admin in between.

I agree with zero tax up to $15k earnings, a very helpful & fair proposition. I employ part-time cleaners (and I proudly pay them more than minimum wages), still with 15-20 hours work per week I feel bad deducting PAYE from their wages and I wonder how they make ends meet.

A universal basic income will never be effective in solving problematic debt, unless the recipients are forced to first pay off their debt with that money. There is otherwise no control over what the recipient of a UBI will spend their money on.

A zero tax band will only up the stakes for professional tax dodgers who will try to make their incomes appear so small that they pay no tax. A zero tax band is also not a UBI.

Instead, the poor should be given an asset (such as a house) that they would otherwise never be able to buy on their own, thereby saving them from taking on the crushing debt that they will most likely never be able to service in their lifetime.

If you can't stomach giving the poor a house, then the best alternative is to eliminate all the incentives that create a price floor in the housing market at the moment, such as the Home Start Grant, the Kiwisaver withdrawal, Welcome Home loans et cetera. I would advocate this latter step as a first one, to purge the market of all the policy signals that cause its malfunction.

Thanks for you comments Jock.

A universal income is not meant to solve problematic debt. Either debt is paid back, it is defaulted on honestly by not paying it back at all, or it is defaulted on dishonestly via inflation. Those are the only ways to solve debt, whether it is problematic or not.

A UBI could help inequality and it could also help efficiency, as it is less complicated than the hodge podge of fixes for the poor we have at the moment, both public and private. It also gives a basic level of worth for all people in a society. That is probably not a bad thing for people who feel otherwise worthless.

I don't understand your point on upping the stakes for professional tax dodgers. The band would apply to everyone surely.

It is the complexity of the tax system that allows for the exploitation of loop holes not where the bands start or finish.

I have no problems with helping the poor it is our social responsibility. Anyone with basic empathy should see that. However I don't see that giving a poor person a house helps them much more than giving them a lump of cash....or a basic income for life.

You're right, I forgot about inflation having the effect of eroding debt.

And you're right about the UBI fixing a whole raft of regulatory problems, for example, it could enable this man to continue his education: https://www.radionz.co.nz/news/national/357536/man-told-he-must-quit-fr…

Also, in Finland where they are experimenting with a UBI, a friend of mine there who is a blacksmith and a carpenter by trade had started a jewellery business as a side gig. It wasn't profitable, it was more like a hobby and he used the business as a vehicle to formalise transactions, limit liability and pay tax. He was recieving a benefit, but the government forced him to choose between running his business which he couldn't live off and collecting a benefit. A UBI could have helped that guy with his living costs while running a small enterprise.

This is where I think a UBI could be powerful to help people who want to be productive in these intangible ways.

Totally agree Jock. I think UBI offers empowerment. It should be just enough to meet the basics. Then you virtually remove the entire welfare state in one swoop. It would have helped in both the examples you give, at least in theory. And as it is not a benefit, it is simply what everyone gets there would be no stigma or shame, people could just get on with things other than living hand to mouth and jumping through endless hoops to get help. A huge issue with the poor, particularly the generational poor is the lack of self esteem. There is no shame in getting something that everyone gets anyway. No one would look down on you. You wouldn't feel those stares that judge you as "lazy or work shy". Not all poor people are lazy or workshy and we really need a way for society to even out good and bad luck. I had tremendous luck in my life to be born where I was with the parents I had. If I didn't have that luck I would hope someone would be thinking about how I might be given a chance to make up for that. And if you want more than the basic go out and find a way to get it.......

Plus think of the women trapped in the abusive relationship or the artist clinging on to try and write that great work. I think society as a whole would benefit greatly. And given that it is very simple to implement, the amount of bureaucracy it saves alone is quite considerable. I have seen good studies that find it almost revenue neutral, that maybe a bit wishful but it I do think, on the whole and over time, it would probably be close to neutral.

Ultimately poverty is a waste of resources.

I don't think giving people things works. Look at the colossal failure of aid programs, virtually everywhere. Give a man a fish..........

Steven Keen had a better solution a modern debt jubilee. Basically give everyone $100k but that has to be spent paying off [mortgage] debt first.

And those without debt get $100k for a new Maserati?

No, they must invest it in a compulsory savings/investment scheme, such as Kiwisaver.

Well said - "pushing on a string" I like it.

Many NZer's have kidded themselves that they're wealthy by shifting credit around for some time.

"Look at the kiwi fruit growers in the news recently. They can't find labour so whats their solution? Not pay more they ONLY pay the minimum wage. It's get the government to change rules so that migrant workers can do it....." Absolutely agree with this observation +100

When my wife and I heard about the kiwi fruit harvesting issue we both said "pay them more" but now Business has other options apparently - change the rules, leverage imported labour, buy a robot.

UBI anyone?

I was reading somewhere recently that the average wage for fruit picking in the 80s was equivalent to about $25 an hour now. So wages for fruit pickers seem to have plunged yet orchard owners are blaming the youth for being lazy (heard another on the radio two days ago).

Good post. Would just like to add that excessive inequality not only breeds resentment and anger, it is also economically destructive. As inequality increases, the number of potential customers for businesses falls, with that come deflationary hazards.

Thanks Ocelot, I very much agree with you.

Henry Ford said it himself, "your workers need to be paid enough to buy the products they are making" (paraphrasing). Ford was a little odd to be sure, but I don't understand how you could argue with the logic of that statement.

Thanks for taking the time to write this detailed response. To some extent, I think your response is more thought provoking than the authors.

With the exception of the housing issue, most of the same thoughts have been rattling thru my head for over a year, particularly the Kiwi fruit growers example. Every time I hear a story on how businesses are desperate for workers, can't find them locally and so need to import more from overseas, I want to scream that they forgot part of the sentence that says ".....can't find them locally AT THE CURRENT WAGE..." Supply and demand doesn't work if you get to manipulate supply by keeping wages artificially low. Unfortunately I see this trend expanding. From laborers to engineers.....but never at the CxO office. Hmm.

I read a good article on what happens when the lower class is kept low for too long. It's written by a .01%er. It's called "The Pitchforks are coming....for us plutocrats". I thought it was insightful.

https://www.politico.com/magazine/story/2014/06/the-pitchforks-are-comi…

Very good post denature.

I definitely agree there's a major problem with stagnant wages.

I'd like to answer 2 questions you pose about housing, which is an area I know well (without sarcasm)

- "How can you have a shortage of something and the cost to buy it sky rockets but the cost to rent it stays flat?"

I think the answer is because of cashflow. House prices have risen dramatically because interest rates have reduced substancially, i.e. it costs no more to service a $700k mortgage at 4.5% today than it cost to service a $400k mortgage at 8% 10 years ago. Rents on the other hand depend on the wages the tenant earns.

- "If building has been as short as everyone seems to agree it is, there must be tens of thousands, even hundreds of thousands of people with no homes no? Where are they all?"

There are more and more occupants per dwelling, precisely to help make ends meet. If we need 12'000 new houses pa at avg 3 people per house = 36'000 people, but we build only 8'000 houses as you say, having 4 people per house on average sovles the problem, no one living on the street. (I'm not saying this is right but it's what's happening)

The $400k 4% mortgage now might not cost you more to service per week/month than it did 10 years ago at 8%, but because they are now taking on higher amounts of debt and paying it over a longer period, it's still actually costing them much more than 10 years ago. And that's without interest rates ever rising over the next 20-30 years over the lifespan of those mortgages. And then of course, unlike previous in cycles, wages have not risen. Household DTI's 10 years ago were 158%, now they're 168%

True, but human nature means that most can only see the "now" and discount the "in 10 years time". I still maintain my view that Joe Average will buy a more expensive house if he sees that he can afford it NOW due to lower interest rates, (and he won't worry about the future) and that is the reason for the rising values of houses

Thanks Yvil.

I take your point on cashflow. However what I think you are effectively saying is there it is an effect of the cost of money on affordability.....which is not the same as a shortage of supply (apologies if I have taken the wrong assumption from what you have said).

Certainly it is absurd that possibly the most important price in our societies (the price of money) is controlled by central banks (people). So in our supposedly free market, the most important price is fixed by whatever....I don't know, central bankers don't make a lot of sense to me. In any case it is not controlled by market forces or supply and demand.

There are good studies showing markets have been considerably less stable since the introduction of the federal reserve in the early part of last century.

I agree the obvious solution is that a lot of poor people are cramming themselves into smaller spaces. I am sure that is happening. But that does imply there is enough housing no? As they aren't actually on the streets. Of course the housing is inadequate and we should do better for our most vulnerable but it is there.

Like you, I do not think it is right that 9 poor people live in a wet, cold house that was built for 4 people. We know the poor are getting sick from their rubbish housing and if that does not hurt us because we are all human, it should hurt us because it costs us an absolute fortune, in health and lost productivity.

But building 650k houses will not help them. As I keep saying supply is not the issue, it is affordability. They are not the same thing. And I don't know how we expect to find a solution when we aren't even looking at the right problem!

"It is only when the tide goes out, that you discover who has been swimming naked" - Warren Buffett

The question this time might be... who, if anyone, was wearing togs?

..very few are swimming...most are standing on the bottom, waving their arms around and just pretending to.

Sometimes swimming and drowning can look like the same thing......

GingerMinja

You like me I think have been waiting for GFC2 & it’s been a wait for sure.

Robert Prechter of Elliott Wave fame has just noted there’s been no big upswing in the sharemarket coming off

the recent pullback and this could be a sign of trouble ahead.

Of course sentiment is primarily still oblivious to the world debt situation and we are just awaiting a catalyst

wherever it may appear This time could be corporate debt but who knows

https://fred.stlouisfed.org/series/T10Y2Y

Keep zooming out until you see the grey vertical squares, those are US recessions. When the wiggly line goes negative, a recession follows. It's heading downwards at the moment. It may yet pull out of a dive, who knows? But if it doesn't, then its recession time in the US.

I dunno what predicts conditions for NZ.

So going by that graph, its 14-18 months after it goes negative the US hits a recession.. so its not quite into the negatives yet, so a US recession is 2 years away if it doesn't do a U-turn shortly.

There are a few warning signs around at the margins. Argentina, UK etc

Northernlights minja? ;-)

Waiting yes, although we've only recently cashed out of a few investments so its only from this point, if we're wrong, that the waiting could actually cost us (if there's a sudden growth spurt for example).

Economic contractions are nigh on impossible to time but debt levels are cray and I don't think it can go on too much longer. The world has become volatile. It's a perfect storm.

We're liquid. Debt free. Twiddling our thumbs.

So where did you put your money into gingerninja? The bank?

Yes and like me you have no where to hide your money from the coming OBR events.

Where can we put cash that's safe from being asked to bail out speculators?

Subtle, but I had a good chuckle. Perhaps it will stick.

Insightful read. Property bulls rich in unbanked equity today will be left high and dry tomorrow. Access to lifeline liquidity damn near impossible.

... they'll be beating a path to the finance minister's door , pleading their case for a bail out ...

There will be a long queue, starting with the OAPs.

Buffett - No debt and over US $ 135 B cash and T'bonds. Just waiting !!

So the end of 2019 at the latest!!!

Is everyone here ready for this? Its been on the cards for quite some time, but im sure the spruikers on here will continue to believe it could never happen or that we are immune.

Ladies and Gentlemen.... Brace yourselves! It will be upon us before we know it and I cant see us getting an easy ride through this one.

The good news is that it will be followed by a recovery.. at some point!

Interesting article. Not sure i'm completely on board with it, but it will be interesting if it does happen. The point about liquidity is definitely worth being aware of, I'm reassessing how liquid some of my investments really are, and whether I want to think about cashing them up to avoid a liquidity crunch.

It will take at least a year from the tipping point for the full effects to be seen, a lot of 2 year fixed rate mortgages will have to tick over to floating @8%+ before the full carnage is seen.

First paragraph, I agree except even if liquid how to dodge OBR events?

I am curious why you think floating would go to 8%, implying an OCR of 5.5%? Frankly in such a bad situation I see the OBR at 0.5%. Now yes the rate the banks can borrow at is another Q but isnt much of NZ banks money supposed to be NZers desposits these days?

I agree I expect there will be a time lag (any reason why not?) , to see the OBR I'd expect mass (like 20%) FHBer and property gambler defaults I can see that happening in a week or even 4, now 6 months? 12months? yes it takes time to lose jobs and get to being bankrupt.

More like a slow motion train wreck that takes place in front of ones eyes that theirs nothing you can do about it, should interest rates, housing supply, or unemployment increase.

There is something you can do - reduce debt. Everything is safer with lower debt. Just hope everyone doesn't do it at once as this will cause the crash :)

Its too far gone... investors are greedy and have lost site with blinkers on believing prices will continue to rise indefinitely, we dodged the 2008 GFC by reducing borrowing costs but absurdly inflated housing debt 9 to 12 times average income. We should have taken the hit back then but no one like to make a loss :(

I am debt free, I equally expect I'll go down the plug hole like the rest, just not the first..

.. geeeeeez ... that John Maudlin would be a fun guy to sit next to at a dinner party ....

But here's the go .... we here in Godzone have gorged ourselves on cheap credit .... and in the process , pushed our property market into the Kamikaze Zone ... we are set for the mother-of-all house price collapses ....

.... hang fire FHB's .... those " affordable " $ 650 000 houses which Taxinda thinks are a part of her Kiwi-Build , those hot little puppies will be available to you at 50 % off in the next 12 to 18 months ... it's better than buying at Briscoes .... hang it , it you can afford the $ 650 000 , we'll give you two for the price of one .... and a free set of gingzu steak knives ....

Perhaps Taxinda’s noble ideas to make homes more affordable could end up having the opposite effect. She is fast becoming the minister for unintended consequences.

Whilst I agree with the general idea of the article and have so for many for years the problem is in the timing of when events are likely to occur. The timeline maybe spot on but history shows people get these things right once perhaps twice but thats it. Predictions have a very very poor record "Daniel Kahneman Thinking, Fast and Slow" I can think of many seemingly rational major event predictions by "experts" in recent years none of which have occured todate.

Make predictions but never about the future .. Mark Twain.

Its been a debt fueled binge party for quite some time, is it cold turkey time soon?

Has to end or change at some stage and a removal of the main party drug (cheap debt) could very well be the tipping point. Either a property reset or a wage and price inflationary will be the outcome. You kind of have to pic one option at some stage, and I think the banks making less money and a normalization of asset prices including property is the least damaging path for the majority.

One thing is for certain though.. One day we'll wake up with a debt hangover, swear off debt for life.. then come the metaphorical Friday, we'll be back at the bar loading up again.

Chug-a-lug Donna.

It is going to happen sooner or later. Damn that greed thing.

Yep it's certain. How soon and how big are the important questions

How big, depends on the size of your debt.

Most peoples debts are out of control.

Not everyone is like you. Just because you are in the sh*t doesn't mean most people are.

We stay in Auckland coz we love it here. If you hate Auckland so much, leave.

Agreed. Traffic aside AKL is great ....if you have no/low levels of debt and security of habitation.

Those that were sold the interest only and tax offset dream from property investor seminars, and continued to inject cheap debt enjoying its artificial high may have a real problem if said cheap debt dries up. The reality is they have been providing the cash exit for property developers, and locking themselves in for all the debt and property operation risk. I am sure the developer and seminar/sales companies are enjoying their new Aston's etc.

I live in Auckland DGZ - the reason I don't leave is because of the interction with the lovely locals like yourself!

Most peoples debts are out of control.

Most peoples debts are out of control.

Speak for yourself, I'm debt free, have been now for 3 years.

It may end up being the perfect storm but you still see kitesurfers out playing in it. The point is those that are prepared, know its coming and have the skills will get through it and still have fun at the same time.

I take it you were born in 1967?

I also have savings instead of debt, but I've also got no home. You're right that those of us that know it's coming can position ourselves accordingly. Hopefully the crash is decent and I can get a home at a reasonable price.

How long have you had savings for that allowed you to buy a house?

You are correct.

Let’s put some facts into the assertion that most people’s debts are out of control

Westpac Disclosure December 2017 - Mortgage LVRs as a percentage of their portfolio

0% ~ 60% is 41%

60% ~ 70% is 25%

70% ~ 80% is 26%

80% ~ 90% is 5%

90% ~ 100% is 3%

Pre 2008 mortgage LVRs are dynamically valued (I imagine that means they get data off a provider)

Post 2008 values are as at origination i.e. what the value was when the mortgage was taken out.

Of course LVR is not affordability, but it’s a reasonable approximation of debt stress.

BTW: 44% of home owners made no mortgage payments according to 2013 stats. Are there mortgage stressed people out there? Yes, there are, but they are not 'most'.

I think 168% household DTI in NZ is concerning. It means that households will be vulnerable to economic shocks when one inevitably comes along. Australia is even worse at 200% household DTI.

I'm not sure that LVR's are the best indicator of risk when house prices are extremely elevated. The LVR's are based on the elevated prices, so if it transpires that there has been a bubble followed by a correction, then those LVR's will change for the worse.

Given the actual debt servicing burden is currently at close to a 17-year low, all I think you can safely say is that some borrowers are vulnerable to economic shocks.

I'd be interested to know what average household debt is across those who actually own the debt. Last I checked average household debt across all households was ...170% of income? But many households are actually holding debt?

I don't think it's as high as 170% but if you've got a link for that figure, i'd be interested to read it.

NZ household debt is up 35% since 2012. The last peak (just before the GFC which had minimal affect on NZ compared to elsewhere anyway) it was at 159% so households are a good deal more vulnerable now, than they were then. Not to mention that after the GFC central banks could drastically lower rates to ease pressures, a tactic they have well and truly exhausted at this point.

It seems to me, that NZ was greatly shielded from the fall out from the GFC because of economic proximity to China and Australia, who themselves were far less affected than the US and Europe.

But should an economic shock occur that NZ is not naturally shielded from (in the way it was after the GFC) then I think there is a real chance NZ households will be hit hard. People have been lulled in to a false sense of security because the last crisis did not impact on them as hard as it did elsewhere and have some insane sense of invincibility. 168% DTI is the opposite of invincibility. Of course maybe there will never be another economic shock ever again. Maybe this time is different? Tra la la.

https://www.interest.co.nz/sites/default/files/embedded_images/Westpac-…

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

Somewhere between 160 and 170%

Currently the debt servicing cost as a % of disposable income is lower than during the GFC (peaked at ~14%, currently ~8%).. but of course if interest rates increase then that heads back up

Thanks, yeah, 170% was a top of my head faulty memory. Thanks you two for clarifying more accurately.

And houses are probably 30-40% over priced. Factor that back into your calculations and most people are under water.

How do you come to that conclusion from the facts available?

63% of Nz'ers live in their own home

44% of home owners have no mortgage so 56% do have a mortgage

The mortgages will be various ages, however if we assume that most had at least a 20% deposit, then a 30% drop will mean only buyers who bought within the last 10% of house increases will be under water.

It is a number of some level but it isn't 'most'

Great point expat.

I guess the problem is that mortgage debt is not the only debt in New Zealand. And mortgage values do not show the level of collaterilization.....all those forms approved because the person ticked the "do you own your own home box". And lets not forget that the algos controlling all the loan approvals have been shown to not do such bang up jobs in the past!

Given the level of froth in the last 10 years and given what has happened in past booms, it is very likely that corners have been cut in many places.

But in the end those things aren't even that important........

I refer to this chart a lot:

https://www.southbankresearch.com/wp-content/uploads/sites/9/2018/01/1T…

Apologies if it doesn't work, but it shows net foreign assets as a % of GDP. “Net foreign assets” is the totality of government sector, corporate sector and household sector assets held overseas, minus the value of domestic assets owned by foreigners.

New Zealand sits at around -50%. Why is that important? Because it's foreign asset holding that always do countries in crises. We can print NZD to take care of local borrowings. But we can't print USD, or GBP or yuan, to take care of those foreign denominated holdings. We are a debtor nation....we do not own enough foreign assets to balance out the foreign liabilites we have. So when things go bad.......even the printing presses won't help us.

We have borrowed to much. And we have squandered it on unproductive things.

{kind=link}

From Stuff. Zespri's bountiful 2016-17 kiwifruit season will go down as a cracker with the largest ever crop achieving record sales worth $2.26 billion.Growers with the kiwifruit co-operative enjoyed a season of increased yields as Zespri produced an after-tax profit doubling to $73.3 million.A record 137.7 million trays helped lift sales and grower returns increased for an average $68,868 per orchard hectare.

But no way we want to pay those ungrateful bludgers picking and packing our fruit 1 more cent than the law says we have to (less if we can get away with it). The laws of supply and demand don't apply to us.We have run out of exploitable workers. We should ask the government to arrange a charter from Africa.

Hell yes send the cows with Mycoplasma bovis in a ship to Africa and bring back some slaves in the same boat......win win for everyone.

Yeah its heading 3rd world faster in NZ for many people than anyone wants to admit. Cannot start thinking like that though, got to be all positive and keep those rose tinted glasses on.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.