One of the few economists warning of impending doom before the financial crisis is doing so again. His views are easily discounted because the false prophets of doom, including an IMF former chief economist, have too often rolled out predictions of imminent doom.

There is an impressive array of global threats. But one thing holds them off: low interest rates. For most of the time since 2008 I have advised clients that things would muddle along globally because central banks had the incentive and tools to ensure this would be the case. Low interest rates and QE held things together.

But as Glenn Stevens, former Reserve Bank of Australia governor warned not too long after the financial crisis, there is the risk central banks will ultimately overdo it. This point has been reached in the US, NZ and probably the UK while Australia is slowly heading down the same path.

This Raving focuses most on the US where Trump's browbeating of Fed chairman Powell to back off plans for more hikes delays what I suspect will be the trigger of the next global crisis or minicrisis. On the other hand, it increases the odds of painful interest rate increases later; increases that will shock markets and more.

Most people warning about an imminent global crisis have been wrong, but …

Nouriel Roubini was one of a handful of economists who forewarned of the financial crisis. He was at it again in September 2018 by listing 10 reasons why there will be another crisis by 2020.

Professor Kenneth Rogoff, ex-chief economist at the IMF got lots of media coverage in January after warning about imminent global threats emanating from China. He also issued warnings in 2017, 2016 …. It is unlikely Rogoff issued warnings every year since 2008; I didn't bother checking. But he reminds me of a NZ commentator who has warned about a China crisis regularly for what seems like forever.

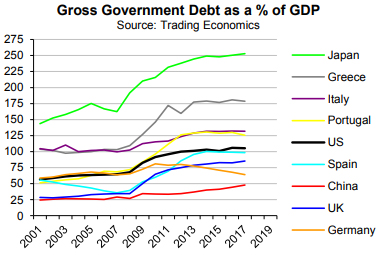

High debt in many areas not just government debt increases the likelihood of problems (chart below for government debt and this link for insights into how global debt has been evolving).

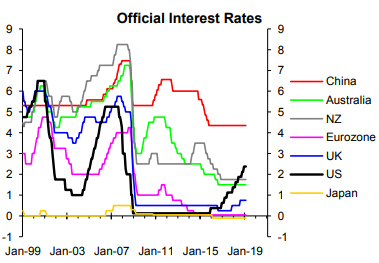

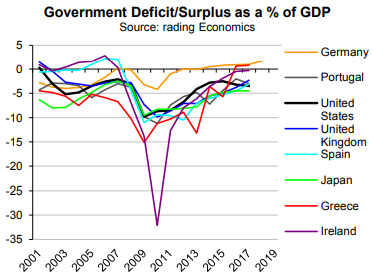

Lower interest rates now compared to prior to the financial crisis reduces scope for central banks to respond to another crisis (chart below). And fiscal deficits reduce the scope for governments to deliver fiscal stimulus when the next crisis arise while in some countries, like Japan, the fiscal deficit is high enough to mean government debt is still increasing as a % of GDP (second chart).

China is a concern and one day it could spark a crisis. Some focus on the Eurozone as a potential spark to a crisis.

If the BOJ ever succeeds in underwriting higher GDP growth and hitting the 2% inflation target it could expose the mega debt problem; it wouldn't take much resulting upside in interest rates to be a real threat. Too many people have lost credibility predicting imminent problems in Japan; making me wary of doing the same despite Japan clearly being a "wacko" economy.

The one that binds all the global threats and could trigger the next global crisis

I believe one of the risks Roubini highlights links the most important US/global threats and is likely to be the trigger of the next crisis: Fed hikes (and hikes by central banks in general).

Low interest rates have made super-high debt levels "manageable" even in the extreme case of Japan. They have helped fuel share, housing and junk bond market booms and played an important part in fuelling the increase in debt.

Fed hikes and the US-China trade war spoked markets in late-2018; they have partly recovered this year (charts below). This is just a taste.

Since the financial crisis I've been advising clients that the global scene would muddle along, largely because central banks had one job: make sure they did. But consistent with past cycles, the Fed will go from saviour to villain. As covered in our pay-toview reports, the same will happen in NZ. The RB is in the process of making a better job of mucking up than the Fed; although it won't have the same global consequences as the Fed's misjudgement that is being sponsored by Trump.

Talk of "normalising" US interest rates is wrong; they will have to go above neutral

Before Trump threatened the Fed Chairman with sacking if he continued to hike, Powell's plan was to increase the Fed Funds Rate towards "normal" or "neutral". In short, the level that is consistent with keeping inflation low over the medium-term. No one knows what that level is with certainty. It is lower now than before the financial crisis. But it is probably above the current rate (2.375% mid-point of the 2.25-2.6% range - see the black line in the top right chart of the previous page).

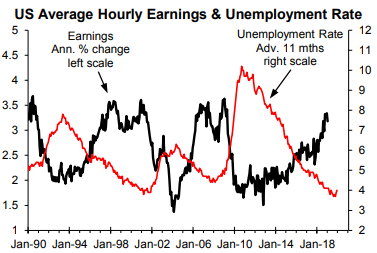

The Fed's aim is too low. The unemployment rate has already fallen to a level that has boosted wage inflation above the level consistent with the Fed's inflation target (chart below). The unemployment rate is advanced or shifted into the future by 11 months reflecting it taking almost one year for it to impact on wage inflation. Trump twisting Powell's arm is part of a pro-growth policy that will result in a tighter labour market and, allowing for the roughly normal lag, even higher inflation.

It isn't a case of one hike in time saves nine but there are parallels. The more the Fed allows the unemployment rate to fall below the level consistent with low price inflation the more interest rates will ultimately have to be increased to cool the labour market. Interest rates will have to be increased above the neutral level to slow GDP growth below average; with this being needed to restore balanced bargaining power in the labour market.

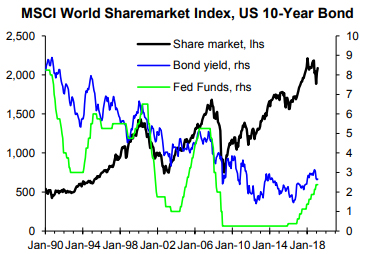

The experience over the last year highlights that interest rates are a threat to global share markets. They are also a threat to junk bond markets. The chart below shows the late-2018 increase and subsequent fall in yields on junk bonds, the more significant increase and fall as a result of the escalation of the Eurozone crisis in 2015 and the huge increase following the financial crisis.

The real threat is when interest rates increase enough to be painful. Higher interest rates and lower GDP growth that will hurt corporate earnings are what will cause share and junk bond market pain. Trump's intervention has stalled fallout from rising US interest rates, but at the cost of even larger future increases; large enough to mean more than just a bit of a slowdown in GDP growth.

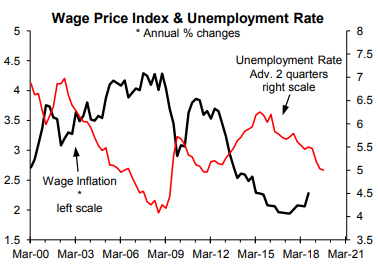

There are some parallels in Australia where the RBA Governor has decried low wage inflation as a bigger threat to economic growth than falling house prices. His comments seem to overlook that wage inflation is responding to the fall in the unemployment rate (chart below). The RBA has much more leeway than the Fed but is heading down the same path to an inflation problem.

In the case of NZ, as covered in our pay-to-view reports, the RB is a bit further down the path of allowing an imbalance of bargaining power in the labour market than the Fed. The problem in NZ will be made worse by the government policies aimed at directly and indirectly boosting wage inflation.

At face value NZ's labour market imbalance implies interest rates will end up increasing much more than any of the economic forecasters including the RB predict. It looks like largely being a repeat of the RB's misguided pro-growth experiment last decade that culminated in 13 OCR hikes and a recession that arrived before the start of the financial crisis in 2008. But the mistake the RB is making needs to be viewed alongside the global threat as we do in the pay-to-view reports and plan to do in seminars that will be announced next month.

In the UK Brexit fallout has overtaken "normality" for the Bank of England; but the UK unemployment rate has probably already fallen below the level consistent with keeping inflation low (chart below). The BOE was moving to "normalise" interest rates before fallout from Brexit temporarily changed the focus. But the Brexit diversion could mean the BOE allows the unemployment rate to fall further into inflationary territory, etc., etc.

34 Comments

Many people who comment here have echoed the same message. This is again essentially about bank behaviour - continuing to lend at a level that while fine at low interest rates, becomes unsustainable at higher rates. The only question is where that break point is. It will vary from instance to instance, but once a few get bitten, forcing banks to call in their security, because theses loans will be or should be secured, the total collapse will likely cascade.

Again this is about banks being able to fully and correctly identify and measure risk to ensure that loans are sustainable. What will they do if they are proven to have got it wrong? The media and public's knowledge of them is much better today than it was in 2008 for the GFC. So will they sit idly by while Pollies sign off on the OBR being activated and savers getting a haircut to bail out the banks?

It is a very nasty mechanism, part natural cycle, part manipulation by interested parties. The three main groups of interesting parties being banking; politicians and their backers; and bureaucrats. Each of these groups looks after their own interests but supports the others in a group effort to parasitise on productive capital and productive labour.

Productive capital needs productive labour, just as much as productive labour needs productive capital. When they play well together the result is a civilised productive society, particularly when the banks and politicians and bureaucrats all work to support them.

When times are leaner, everyone seeks to protect their own interests, The banks, the politicians and their backers, and the bureaucrats, find they can work together in this. They find reasonable sounding theories to explain why they must be protected, and are a cunning lot, setting the rules (credit rules are especially powerful) and dispensing favour where it suits. Productive labour is hardest hit and turns on productive capital, egged on by the lawyers. Productive capital flees France for England.

In a downturn, it is better to have a government job. It may be boring and frustrating, but it pays the bills, you are part of a protected group, and the pensions are excellent.

Centralisation of power may be the enemy, whatever it is, something is clearly rotten in the West. If we don't figure it out we will continue to decline.

With the political systems the west has it's no wonder. It's always a two horse race. MMP for example let's in parties like Act with 0.3% of the national votes yet TOP or the conservative party are kicked out with 2-4% of the national vote.

Easy, just lower the threshold to 1.667% of the vote.

Good post.

And we can see this model playing out in the way that these powers have cajoled and convinced populations to allow them to erode and eliminate the taxes that had been on capital (including land tax) in earlier decades and instead foist the entire tax burden on labour productivity while exempting capital. Forgetting the role the earlier balance played in circulating capital through the economy and enabling more to participate more fully in capitalism.

Productive labour was what did the work historically. It's responsible for less than 1% of the work, now.

Nouriel Roubini was one of a handful of economists who forewarned of the financial crisis. He was at it again in September 2018 by listing 10 reasons why there will be another crisis by 2020.

The link "10 reasons" is broken.

I am an employer but I don't see a problem with New Zealander wage earners getting significantly higher wages. New Zealand needs progress in the use of capital, productivity and technology.

As an employer who would like to pay higher wages, what factors currently limit your ability to do so? Are there regulatory, tax, or other changeable factors limiting your ability to source and/or use capital and technology to improve productivity in your business?

He’d like to see other employers increase wages.

I think he is wrong in saying interest rates will rise, too many central banks at play pumping credit into the system to ever allow that to happen

David Stockman also believes interest rates will go up...a matter of time.

https://video.foxbusiness.com/v/6005320309001/#sp=show-clips

He like many is locked into the grow for ever business model, he's wrong IMHO. We are now in the era of shrinking, raising rates will make that faster.

But can they put it off forever? Low interest rates as we have seen, effectively encourages more people to take on [more] debt, and ultimately that cannot be sustainable. Wouldn't it be better to slowly increase interest rates to both deter new, unsustainable debt, and encourage people to address that which they already carry?

Banks are like drug addicts, can they even say NO to anyone wanting to take on some/more debt?

No, they were merely kicking the can down the road - that's the only skill they know.

The net energy going into the system is plateauing. So-called productivity gains are only energy efficiencies, and they tend to tail off, not exponentially increase. So I've long argued tha the only interest-rate that fits over the top of the curve is zero, and thereafter it has to be increasingly negative, And if banks are creaming, it has to be at the expense of someone else - presumably an ever-more indebted middle-class.

Whose collateral is all getting older......

the USA is trying to do that and they are already backtracking as they see a slowing down ahead,

you are correct there is a huge worldwide debt mountain now and that is the problem how do you service repay it if you raise interest rates without causing a recession or worse

as the latest article on interest.co states the RBA will lower interest rates this year to stave off a housing lead recession in australia

...begs the problem. How to fight a wave of inflation or support a dropping dollar without raising interest rates? Check mate. Gonna pay the piper one day.

The answer they think is to run slightly hot inflation, specifically through wages, as it reduces debt in real terms. Why fight 3% inflation? There is almost no evidence that 2% is the correct level.

There will be no sustained wave of inflation.

Could the dollar tank? yes certainly what does that do to export prices v import prices? not all bad.

We'll be seeing that OBR policy kicking in. I wonder if it will apply to accounts that are holding business funds for the financial tax year? The IRD certainly aren't going to let the OBR get in the way of businesses paying their full tax for the year in spite of the OBR giving SME accounts a haircut.

As hard as i try I don't see this as a likely outcome. In the past twenty years we have seen substantial asset appreciation which is not counted as inflation. The dollar you earn buys less when you need a house.

as interest rates fall assets go up in value and the return falls. My farm was Gv 620k in yr 2000, now gv just under 3m, the return has stayed around 60k maybe a bit more this year, rates have gone from 2.2k to 8k.

Bank are money creators and they have created a lot since 2000, but it's only pumped up assets and left us with very high debts, inflation would be a nice way out but it's an unlikely outcome because most of the borrowed money is invested in speculative assets not productive ones. If They lift interest rates they will only find the bill cannot be paid.

"the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment.

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal.

Actually if rates fall then a dollar does buy the same amount of house, you have conflated a stock with a flow. You buy a house mostly with a flow. If you halve the interest rate then your dollar of flow buys twice as much house (ignoring principal for simplicity here). Doubling the value of an asset halves its return but thats not the same as halving its profitability to an investor. If the investors cost of funds halves then the asset is actually just as profitable to own as it was before.

So no, your axiom is false.

confused

You can look up stock vs flow in google.

It isnt inflation, its investment or asset inflation, simple.

No, "a security is nothing but a claim on a future stream of cash flows" its a claim on future energy flows, and there isnt enough energy out there to pay the debt today let alone in the future.

it isn't inflation or it isn't? Im still confused steven ,whats the difference between asset inflation and run of the mill inflation? You could believe that inflation is an increase in money supply and we have had that.

In terms of CPI it isnt inflation. Once a house is bought you dont pay more for it unless interest rates go up. In my case with no mortgage and savings I feel no effect of house price inflation.

I think the key thing to consider on asset inflation is its a one off purchase and not an ongoing increasing cost ergo it isnt inflation.

Even if it could be considered inflation as part of CPI its only one sector of an economy. So for sake of argument lets let house values inflate CPI what is the result? CBs put up their OCRs? yet unarguably before even thinking of that economies are already almost on life support now put up the OCR significantly, or even a bit and that would very probably roll the economy over into a recession if not a Depression (which is my outlook)

The central bank narrative has collapsed…here’s what happens now

https://citywireselector.com/news/the-central-bank-narrative-has-collap…

Lets look at that statement, clearly speculators cant survive (make lots of $s) in a low inflation environment.

So the response is,

So "In his speech, Dr. Werner also said investors need greater, local-level coordination to make sure central banks create the correct monetary policies."

ergo specualtors need to force CBs to put up interest rates in order to get "decent" returns? If so frankly its nuts IMHO, this would kill economies.

Also need to separate out real investors v the specualtors...

it's Okay, i'm outside looking at the full moon.

I think Snider is nailing this one.

"The obsession with inflation is grounded in historical fact. This is true both of our recent “conundrum” as well as broader circumstances surrounding slow burning structural changes. As to the former, last year the global economy was supposed to take off, concurrently signaled by accelerating inflation rates due to what are always claimed to be tight labor markets.

The worldwide LABOR SHORTAGE!!! was supposed to lead somewhere very good; an end to a decade of increasingly dangerous malaise."

https://www.alhambrapartners.com/2019/02/26/the-many-obvious-dots-of-ke…

The obsession with inflation is based on looking backwards and not forwards, or even around then at today. For 11 years inflation and even significant inflation has been whinned about and after a decade of QE and a "low" interest rate is no where to be seen so much so in fact I think is dead and buried.

Capital gains tax is essential for non owner occupied residential properties. Productive investments for the country like farming, shares, businesses and commercial property should be exempt.

Because of our over generous tax treatment for rental properties, money has been diverted away from business enterprises and anything productive.

Ikon companies like Trade Me, Tegal, Restaurant brands and Tip top to name just a few have been or will be sold to overseas companies who have got the capital.

Unfortunately, there will be even less capital here as profits move to overseas.

countries.

NZ has a low wage economy and this will not change unless we get production up which is not and will not happen under the present tax system.

New Zealand is on a downward spiral unless something is done to the tax system.

Vested interests rule this country.

Mostly rubbish. No, all asset gains should be taxed. Take a farm why is it bad to have a CGT? such doesnt effect the day to day running of the farm. Why then are farmers handed a tax free gift on retirement? also farmers dont pay for housing I believe? So 2 huge tax free gains one over a lifetime? cant see it.

Same applies to all the others.

Lots of impacts due on our economy like its small and un-competitive nature. Given kiwis actually work long hours then that reflects badly on the so called productivity. I mean some years back I was paid for 40 hours but expected to turn up and work Saturday mornings for free so in effect a 45+ hour work or a 11% gain for no cost to the employer. Then importers hold prices up at the MRRP making imports artificially expensive, Commercial property for retail has a very high $ per m2, yet more price gouging.

"Because of our over generous tax treatment for rental properties, money has been diverted away from business enterprises and anything productive." yet they are treated no differently as a business however their "low risk" nature has meant they can source loans way cheaper than any real business and you dont need any real skills to be a landlord unlike a real employer/manufacturer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.