Bank balance sheets are complicated things. But depositors rely on them to ensure their money will not only be serviced (with some meagre interest), but more importantly the funds can be accessed and returned if necessary.

The Reserve Bank is making an effort to make bank balance sheets more accessible and comparable with their Dashboard tool.

But that tool is also quite dense and too intricate for most bank customers.

We want to take a simplified look at what that data shows, from a bank depositor point of view - whether you just have a current accout, or have savings parked there.

What follows isn't full technical analysis - it however should help you with an initial assessment of how your bank can repay you the funds you have with them.

But first, a bit of technical stuff you should understand. When you move money to a bank, they aren't holding it for you in cash. Your funds in the bank are no longer there - all you have is a claim on the bank for them. You are a creditor of the bank, unsecured at that. This isn't quite as scary as it may sound, almost all bank creditors are unsecured and all rank equally and ahead of the shareholders.

Banks keep very little cash on hand these days to back up depositor claims on them like yours. As you will be well aware, society have moved well away from banknote currency being important. Its all electronic these days. In fact, only a few people can actually remember when banknotes were important. (It seems like it is the informal and underground economy are the only sectors left using them. In fact, the Reserve Bank has been wondering whether banknotes still have a place in our financial system.)

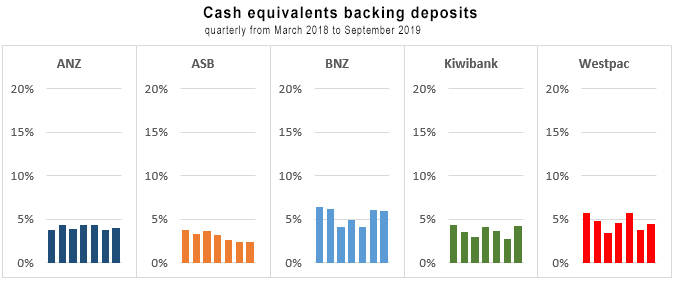

This is how much cash (Notes, Coin, and other cash-equivalent accounts) each of the main banks have on hand to cover your deposit. It's not much.

| Cash equivalents backing for deposits | |||||

| ANZ | ASB | BNZ | Kiwibank | Westpac | |

| Mar 2018 | 3.7% | 3.8% | 6.4% | 4.3% | 5.7% |

| Jun 2018 | 4.4% | 3.3% | 6.2% | 3.6% | 4.9% |

| Sep 2018 | 3.9% | 3.6% | 4.1% | 3.0% | 3.5% |

| Dec 2018 | 4.4% | 3.2% | 4.9% | 4.1% | 4.6% |

| Mar 2019 | 4.3% | 2.7% | 4.1% | 3.6% | 5.7% |

| Jun 2019 | 3.8% | 2.4% | 6.0% | 2.7% | 3.8% |

| Sep 2019 | 3.9% | 2.3% | 6.0% | 4.2% | 4.4% |

And even through it is tiny, it is actually still decreasing.

If we ever have a bank run, there would be little point lining up at the teller windows.

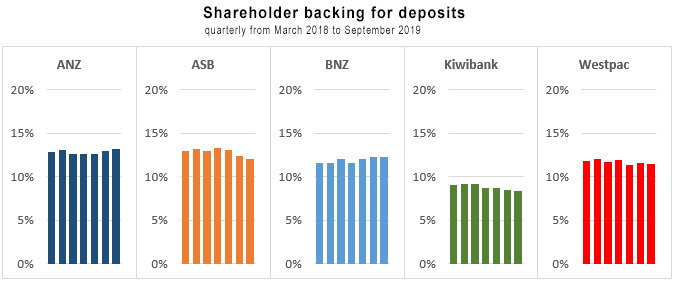

Bank deposits make up the vast proportion of how a bank is funded. You might otherwise think that shareholders supply capital to fund bank operations, but that is hardly significant either. Banks are highly leveraged organisations and to extract very high returns, shareholders don't like to invest much capital. This is in fact why the Reserve Bank is cracking down on them, requiring more and better quality capital from bank shareholders. Still, even after these reforms, the levels will be low - although higher than they are now. The following indicates why the Reserve Bank has been uncomfortable with bank shareholder investment levels.

| Shareholder backing for deposits | |||||

| ANZ | ASB | BNZ | Kiwibank | Westpac | |

| Mar 2018 | 12.8% | 12.9% | 11.6% | 9.0% | 11.8% |

| Jun 2018 | 13.1% | 13.1% | 11.6% | 9.2% | 12.1% |

| Sep 2018 | 12.6% | 13.0% | 12.0% | 9.2% | 11.7% |

| Dec 2018 | 12.6% | 13.3% | 11.5% | 8.8% | 11.9% |

| Mar 2019 | 12.6% | 13.1% | 12.1% | 8.7% | 11.4% |

| Jun 2019 | 13.0% | 12.4% | 12.2% | 8.5% | 11.6% |

| Sep 2019 | 13.2% | 12.1% | 12.3% | 8.3% | 11.5% |

While that is more than the cash backing, it is also surprisingly meagre.

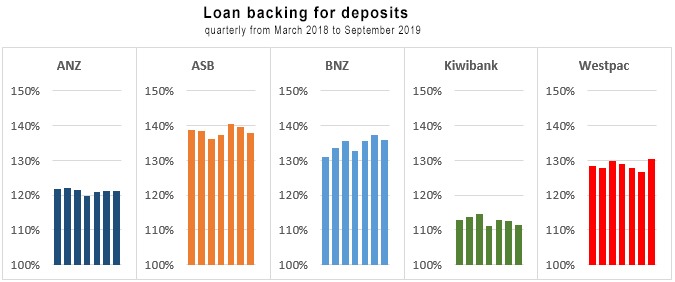

And of course, your deposit is the source of funds banks use to make loans. (And that is somewhat circular - the borrower will then deposit the loan funds in a bank until they need the money, creating more deposits on which more loans can be made. Individually, the effect is tiny and short, but all together, this is the basis of 'credit creation', and the basis of much misinformation and conspritorial confusion over the process. Here is an excellent primer on how it actually works.)

Bankers lend. Those loans are funded primarily from customer deposits, but also wholesale borrowing supplies about 30% of bank funding. So you need to know how much each bank has in loans to cover your deposit. It varies by bank. And the systems works so that depositors supply the capital for loans while the shareholders take the profits.

| Loans to deposits ratio | |||||

| ANZ | ASB | BNZ | Kiwibank | Westpac | |

| Mar 2018 | 121.8% | 138.7% | 130.9% | 112.8% | 128.3% |

| Jun 2018 | 122.0% | 138.5% | 133.7% | 113.6% | 127.7% |

| Sep 2018 | 121.5% | 136.3% | 135.7% | 114.7% | 129.7% |

| Dec 2018 | 119.7% | 137.3% | 132.7% | 111.3% | 128.9% |

| Mar 2019 | 121.0% | 140.3% | 135.7% | 112.7% | 127.7% |

| Jun 2019 | 121.3% | 139.6% | 137.3% | 112.5% | 126.6% |

| Sep 2019 | 121.3% | 137.8% | 135.9% | 111.3% | 130.4% |

There are Reserve Bank limits on how much wholesale funding (Core Funding ratio, Covered Bond limits, etc.) is allowed. This has the effect of keeping demand for local depositor funding higher than it would otherwise be, and deposit interest rates higher than they would otherwise be.

Sunlight is supposed to be healthy. Knowing how your bank uses your deposit, and what they have backing it up should be one factor you can consider when choosing what bank to park your hard-earned funds at.

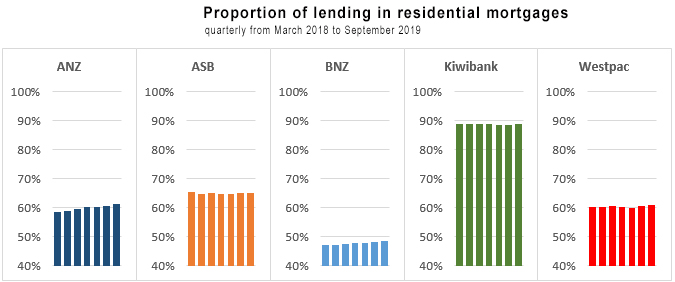

And finally, you might have a view about how concentrated bank lending is toward residential housing. In fact, most main banks aren't real banks, they operate now more like mortgage banks, the exception being BNZ which has the most balanced lending profile. But if you think like a banker, you may be comforted by high exposure to the housing market, a sector that can be more liquid than business or rural lending. Or excessive concentration may concern you.

In the end, depositors can't make specific sector exposure choices by parking their funds at a retail bank. But they can do so with their eyes open.

Every investment carries risk. It is up to you how you assess that, including where you bank your funds.

Here is the link to the RBNZ Dashboard from where the data for this article was sourced. Here is a link to our tool as an alternative way to compare that data.

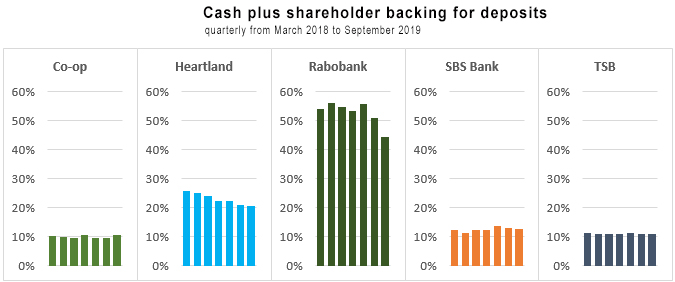

And for the record, here is the combined cash plus shareholder backing for five smaller retail banks in New Zealand. (Be careful of the scale because it is different to what has been used above.)

(Rabobank NZ isn't strictly comparable in this simplified way, so you should investigate those differences. But it does have interesting variations.)

37 Comments

Here is an excellent primer on how it actually works.)

There is actually no evidence fractional reserve /money multiplier banking operates in New Zealand.

There were two major evolutions in money and banking that seem to fall outside the orthodox narrative. The first was a shift of reserves and bank limitations from the liability side to the asset side. The second was the rise of interbank markets, ledger money, as a source of funding rather than required reserve balancing: replacing the old deposit/loan multiplier model. Courtesy of J. Snider from Alhambra

Furthermore:

If textbooks are, for example, really still teaching the money multiplier as the dominant approach to money, so much the worse for them. But as I pointed out to him, that was his problem (as an academic working among academics): I wasn't aware of any floating exchange rate central banks that worked on any basis other than that, for the banking system as a whole, credit and deposits are created simultaneously. He quoted the Bank of England to that effect: I matched him with the Reserve Bank of New Zealand. Link

Thanks for the illumination Audaxes to an otherwise excellent interest dot overview.

Try the official information act requests replies on the reserve bank website.

It is a pity that the Depositors don't have any united muscle to demand higher returns from the banks and more safety and are dependent on RBNZ and the Government to safeguard their funds. Totally contrary to what the Banks demand from the borrowers when they lend money. There must be some alternative. Why have the Tech Companies come up with some path breaking innovation yet ?

Negative interest: Why are deposit rates persistently low?

Market regulation

In this article I argue that the persistently low interest rates are neither explained by the saving habits of an aging population, nor by the policy of the ECB. The cause lies in the structure of the monetary-financial system of which the central bank is the cornerstone. This structure lacks sound market processes for deposit rates. Deposits are created by the banks themselves and are automatically available to them as funding. Depositors have no real negotiating power vis-a-vis the banks. To realize proper market mechanisms for deposit rates the market regime needs adjustment. That is the responsibility of the legislator, not of the central bank.Safe alternative

The adjustment starts by giving depositors a safe alternative to the bank account. That gives them real negotiating power vis-a-vis the banks. Presence of this safe alternative also makes it possible to gradually phase out deposit guarantees and other state aid to banks, and to raise risk awareness among depositors concerning lending money to a bank. These are the ingredients for applying appropriate market processes to deposit rates. Link

Yes. And I will highlight the following:

There is no safe depository for cashless money. Those who do not want to lend their savings to a bank must withdraw them in cash and keep them in a safe. The inconvenience, the risk and the costs thereof leave room for negative interest on savings. In the absence of an alternative, savers have little room for escaping the banks’ market power. They will ultimately accept negative interest on their deposits, whether they like it or not.

In many ways, depositors are serfs.

I did wonder what would happen if Grey Power got their act together and organised a rolling liquidity problem. Each week a different bank is targeted, maturing deposits being moved to another bank. Or something like that. Not enough to cause a crisis, but enough of an irritant to cause higher deposit rates. Following the idea of how powerful a mosquito in your bedroom is.

There is united muscle. Pull your money. Also instead of being a depositor you have the option of being a shareholder. You choose to deposit it with the bank instead of buying shares in the bank.

Except shares can go down. I have shares in a bank and they are worth less now than what I paid for them.

Is this person talking Nonsense

https://m.youtube.com/watch?v=TgDOVND3wgc

OR Sense

Exprts feedback welcome

“ Banks keep very little cash on hand these days to back up depositor claims on them like yours. As you will be well aware, society have moved well away from banknote currency being important. Its all electronic these days. In fact, only a few people can actually remember when banknotes were important. (It seems like it is the informal and underground economy are the only sectors left using them. In fact, the Reserve Bank has been wondering whether banknotes still have a place in our financial system.) ”

Societies are being passively herded away from cash to electronic by by Central Governments and the elites to protect their owns interests. Eg: The US no longer prints $500 green backs.

I wondered who David refer is referring to in this statement, as i consider cash to still be very important. A recent news article about the bush fires in Aussie highlighted the impact of a loss of power on the cashless business's - no business. And this statement - "society have moved well away from banknote currency being important" Society have been FORCED away from cash by the banks, supported by the Government. Doubt this? Ask to receive your pay packet in cash these days, they won't do it because the banks charge too much. The cashless society is not one done willingly but rather imposed and people have had to adapt or be made poor by the banks.

Sunlight is supposed to be heathy. Knowing how your bank uses your deposit, and what they have backing it up should be one factor you can consider when choosing what bank to park your hard-earned funds at.

In fact depositors and other unsecured creditors are in effect the only back up, beyond the collateral securing the loan contract - a promise to pay.

Despite the Reserve Bank's increased capital requirements, NZ banks remain highly leveraged. According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest. Put that way it doesn't sound a lot. But should the proverbial hit the fan, the public, the regulator and the regulated banks will probably all be glad it's there. Link

The depositors need a bigger share of the profits on the $100 of lending, in so much as their real, risk adjusted returns are just plain derisory, given they are unsecured creditors..

Is 1937 = 2020

The first YT video you post is a good explanation of Dalio's thinking (didn't watch the 2nd).

What Dalio says about gold in a portfolio is a bit difficult for NZers as the retail environment for gold is not great. Anyone interested might want to look at Perth Mint's offers (which are generally open to NZ citizens) or even GLD ETF. Now about high-dividend yielding stocks, you might want to consider Smartshares NZ Dividend ETF. If that doesn't grab you for any reason, look at the breakdown of stocks within the ETF's portfolio.

Individual stock in NZX can look at A2M, in ASX can look at MQG, SOL . JIN for high risk and for long term multibagger PBH.

If corrected in ASX than XRO, ARU, ALU, NEA, TNE, NUC.

If anyone following stocks and have some feedback on above mentioned stocks, will be interesting to read.

In the context of what Dalio says, why would you recommend any of those stocks?

Nothing to do with Dalio but when mentioning stocks, sharing it.

This is a great, well-researched article.

But it doesn't answer its own question.

Ultimately (although there may be several pass-the-parcel transactions in the interim) the purpose of the numbers in your digitally-tabulated bank 'deposit'- is to be exchanged for processed parts of the planet. Stuff. The backing therefore, is whether there are indeed going to be those parts available in the future, whether others can outbid you for the remaining ones, and whether there is enough energy feeding into the system to procure, process and proffer said planetary parts.

Those parts may be cucumbers or BMW's, or anything in-between. If they are no longer available, your 'deposit' is no longer underwritten. If you are out-competed, your 'deposit' has been rendered too dilute. And if there is a dearth of energy, you will likewise be out-bid.

This is where the planet is now. It is not just 'deposits' which are expectations of future processed planetary parts, it is all issued debt and all investments (plus, arguably, all profit-charging). Economists measure neither how much (nor of what quality) there is in the way of remaining planet. Nor of the grunt still available from the remaining energy-stock. I've just re-read Alan Bollard's Crisis - nice man, honourable man, but absolutely no clue as to the Limits.to Growth, or of the essentiality of energy.

My bet? A repeat of 2007-8, in which the remaining 'tools' in the 'toolkit' (which seem mainly to consist of pitching the level of confidence in speeches, injecting 'liquidity' - quaint term for printing money - and lowering interest-rates) get washed away in the flood. Nixon pointed to it on August 15, 1971 - the combined bets were set free from any concrete backing, and long after the possibility had actually vanished too. And they are fractionally-reserved, but not by planetary-part availability, which is reducing daily (100 million barrels of finite oil burnt today and every day until we can't maintain the supply rate). From then on, all bets are on your own cognisance - except that the move to eliminate cash is a move to remove private storage options. In Greece, they quickly reverted to barter - real planetary parts for real planetary parts in the main, maybe via services as an intermediate step.

In a practical sense, we are better buying now, what we anticipate needing tomorrow, perishables aside.

Guessing you're fully invested in that last few drops of precious oil then eh. Energy of course by definition is infinite.

Chuckle. Yes, but physically. I store things like alkathene pipe, and suggest that Local Authorities 'funding for depreciation' should also be asking whether the physical planetary parts will be future-available.

In practical terms, energy input is solar. Fossilised sunlight was a one-off bonanza, which economics chose to ignore.

PDK, what would you store instead of cash and gold ? Tools?

To understand the difference between price & value consider the following - global financial crash, little liquidity in the system, asset values uncertain where some use remains and the situation of two types of human resource. The Real estate Agent & Lawyer now that property and other business transactions are much diminished or no longer possible - there is no price at which either can trade so their value is zero. Now consider the plumber & electrician, leaking pipes & faulty or non working electrical equipment will still require repair, the price may have dropped considerably as also their tools & vehicles but the value remains the same. The former will suffer unemployment and poverty the latter a much lower living standard even if some form of barter is required to complete a deal. I have nothing against the former just an illustration that is easy to see.As John Mauldin has written about a great reset will likely to occur and whilst its timing & form is unclear the longer the current situation remains the more brutal the effect.

I wrote this as part of a response to an article on Central Banking published on this site on Thursday here.

Many years ago i was told this about interest. Money saved is put to work, for a return to the owner. this can be as simple as buying a tool, the return being the work the tool can do, or the saved time. Or it can be used to by a house, the return being shelter, security etc. So far fairly simple and easy to understand.

Expanding on this is the principle of Banks. Excess money is accumulated by Banks on behalf of the money's owners, and put to work for a return (invested). Banks focus on an economic return, thus this money generates a financial return. All contributors to the pool of money get a share of the financial return and this is called 'interest'.

This is a simple principle but the Banks have corrupted it severely. As the article implies there is some level of fractional operation in place where the banks lend out at ratios of their deposits (post the GFC it was revealed that some banks were operating in the 30:1 range - $30 lent for every $1 on deposit) which indicates even at low interest rates, they are making an awful lot of money from depositors funds ( with a fractional ratio of say 10:1, and loan interest rates of 3%, the ASB doesn't pay interest on deposits under $100K, but they will make $3 for every $100 dollars deposited, I assume the other banks will be the same or similar). So we ARE being thoroughly ripped off still!

@murray86

some banks were operating in the 30:1 range - $30 lent for every $1 on deposit

are you sure this is right ? If you see the loan-to-deposit ratio, it is ~130:100, right ?

Yes. I don't think it was NZ banks though. This came out in the wash from the GFC, so was most likely US banks. But even at 10:1 they are still making a killing on depositors funds that they don't pay the depositor for.

In the wash up though, so long as they manage the risk appropriately, I don't mind the fractional ratios, the problem is their management of their risk. They argue, as DC implies, that it is their money they are risking and this is where I have an issue. It should be depositors funds and the banks should be accountable for the risks they take on. As the GFC demonstrated they didn't manage or even care about the risk. They just passed it on to someone else through derivatives, and ultimately got away with it. Capital ratios don't really protect depositors, changing the legal status (ownership) of the funds would.

Loans to deposits ratio of ~125% does not look bad :-o so NZ banks are not at all stretched , like i was thinking. leverage ratio (of ~12% they say) does not include deposits ?

An unsecured loan to the bank, as a deposit, gets you 1.5% p.a. An unsecured loan from the bank costs you 17% p.a. (Kiwibank). And the banks are complaining about squeezed margins!

Banks don't need our money because they can create their own.

I agree with many of the commenters - Great article. But, also depressing. I'm making my way thru several of the linked articles, maybe I will find a ray of hope there somewhere....

The article also generated as many questions. Maybe someone in the community can answer:

o The article indicates that depositors are unsecured lenders. Are there "secured" lenders? The cynic in me says probably CxOs and Board of Directors.....

o I'm probably thinking about this wrong, but what is the RBNZ's logic in requiring mortgagees to put a large deposit down on a house (>5%) but allowing banks to hold a much smaller amount of capital (<5%) to secure a larger amount of (depositor's) money? Add to this the fact that if I default on my home loan, the bank still has a house as collateral. It may not be worth a lot, but I'll bet's it's worth more than the amount an unsecured lender is going to get if a bank defaults.

o How do the NZ capital requirements stack up to other 1st world countries? Aussie? US? Germany...etc?

I just did a calculation on the best case scenario for myself as an "unsecured" lender and how much I might get back if my bank goes into default. Have started to dig that hole in the backyard to put my money in..........

While digging might make sense for some period of time I think that the inevitable transition to cashless money will involve cancelling currency notes and going fully electronic. So, that’s a significant risk. EU is likely to be the first to do this so keep an eye on that...

Good point, but perhaps by then there will be a more viable option than a traditional bank.

Think of it like GoldCorp in the 80s

When there’s a run of depositors seeking their gold the vault was bare

Frankly it’s a disgrace NZ still has no bank deposit security insurance like US Canada Australia

and did deposit insurance save northern rock depositors - no.

I would rather have a robust fence at the top of the cliff than a sophisticated ambulance at the bottom!

What the RBNZ is doing is far better than deposit insurance - Require more capital - much more capital - and then ensure that Core Funding, One Week and One month ratios are really conservative - meaning proper liquidity management and proper funding - not all short term. RBNZ led with world with the CFR and other liquidity ratios - and now leads it in terms of requiring more capital - the right focus - good fence at the top of the cliff.

Ambulance at the bottom is about political expediency. Fence at the top is about sound systems

Northern Rock faced liquidity issues. Northern Rock was reliant upon wholesale funding to finance it's business. When credit markets froze due to the GFC, Northern Rock was unable to obtain funds from the wholesale market. Northern Rock was able to obtain emergency liquidity assistance from the Bank of England at penalty rates to avoid moral hazard.

In NZ, the NZ banks were also reliant upon wholesale financing to fund its operations. During the 2008 - 2009 period, the major banks in NZ also had difficulty in wholesale markets financing their operations, when these markets froze. The RBNZ provided emergency measures to support banking liquidity via the Term Auction Facility (on 12 November 2008, the weighted average of successful bids was 6.29% under the TAF (collateralised) vs 7.07% for 90 day bank bills) - so was it a penalty rate like BOE charged Northern Rock? The NZ banks were also fortunate that the NZ government provided a guarantee so that the banks in NZ could get their wholesale financing. If the NZ government, did not provide their guarantee and the banks were unable to obtain wholesale funding, just think what the counterfactual outcome would have been to 1) the economy 2) unemployment 3) asset prices 4) the financial system.

When the banks in NZ needed liquidity, where were the Australian owners of the big 4 banks to provide financial support to their NZ subsidiaries? They were likely unable to financially support their subsidiaries as they were facing their own liquidity issues, and their Australian parent banks had limits imposed on funding their NZ subsidiaries.

David

Its a pity your comparison to the smaller banks is not truely a comparison - It is in fact quite misleading. Please try and compare like for like.

From the RBNZ

"New Zealand’s financial system has two main vulnerabilities: our high levels of indebtedness (in the household and dairy sectors) and our reliance on foreign sources of funding."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.