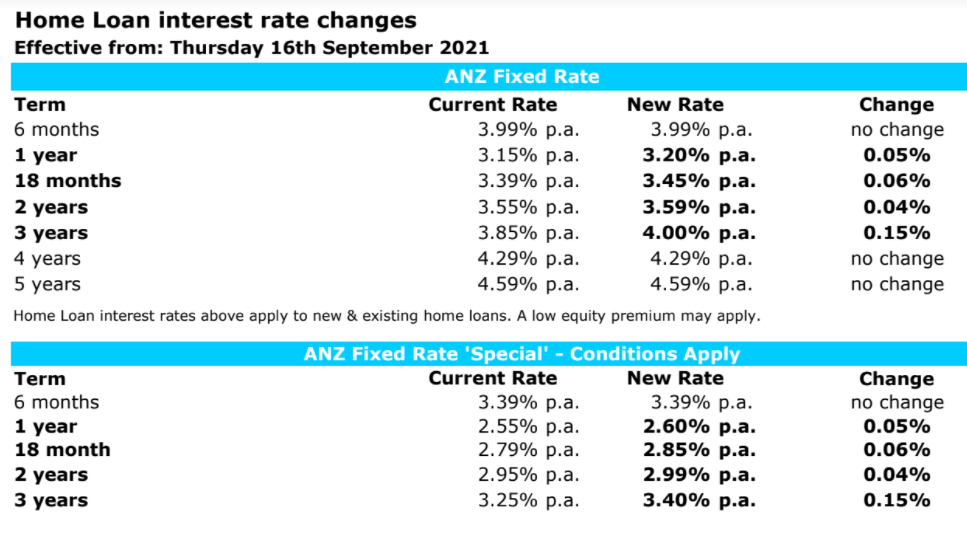

ANZ NZ is increasing both its "standard" and "special" one-year, 18-month, two-year and three-year home loan interest rates.

The increases range from four to 15 basis points, and are effective from Thursday (today), September 16.

With its one-year special rate rising five basis points to 2.60%, ANZ's now above the 2.55% offered by ASB, BNZ and Westpac NZ. And most smaller banks are lower than that.

ANZ's new 18-month special, at 2.85%, takes it above ASB and BNZ's 2.79%. And its four basis points increase to 2.99% with the two-year rate, takes ANZ four basis points above ASB, BNZ and Westpac with several other banks lower still.

In terms of the three year rate it's more of a mixed picture, with some banks below ANZ's new 3.40% special, and some above.

Separately, Kiwibank also hiked mortgage rates earlier in the week.

See all banks' carded, or advertised, home loan rates here. The tables below outline ANZ's changes, with details of what's required to get a special rate below.

15 Comments

So they backtracked after jumping the gun a few weeks ago… and then backtracked on their backtrack?

Apparently the RBNZ is indicating they are going to lift rates on the 6th October -Level 4 or no Level 4. ANZ is just preempting this. Huge fears in the RBNZ on the inflation and GDP numbers and they are losing patience with the continued housing market growth.

Yes, it's fascinating. Courtesy of the elimination strategy, we are a "closed circuit" economy effectively ring fenced from the normal drivers of the global cycle.

The most obvious thing is that the local economy is running at maximum capacity, due to supply constraints and the lack of our usual immigration cheap labour buffer. Consumer behaviour now shrugs off lockdowns, we can't spend money overseas so splurge here, and any cash flow gaps for individuals and businesses are plugged by the government.

This is a recipe for sustained inflation above 3% and the RBNZ know it.

Perhaps they just jumped the gun on backtracking.

Is everyone switching to BNZ then?

Ill go where ever I can get the best rates. Having loyalty to a bank.....

They seem to be pricing themselves out of the competition ? Or is the demand coming down for home loans ?

The demand for new home loans just has to come down. There is an ever increasing gulf between those that can afford a house and those that cannot. There must be now a big gap that has been created in a very short time, its just math. If you didn't buy a house in the last 12 months because you couldn't afford it, effectively you have now been priced out of the market by at least 5 years. Its time for banks to start making more money out of those that could afford the mortgage to cover the loss. Banks are not interested in those still stuck in the gap and remember every business expects to make more profit each year than they did the last.

what is the "loss" that you refer to that the banks need to cover....perhaps my memory is going but I don't recall any of the big four actually making a loss since the early 1990s? happy to have this clarified

I think it would take some effort to make a loss. They have permission to magic money into existence and lend it out with interest, secured by an ever inflating asset.

Pricing themselves out of the competition, or reducing their exposure to the insanity?

Take 2 steps forward, take 3 steps back. Take 1 step forward, take 2 steps back.... *rinse & repeat*

There's never been a better time than to be ANZ Bank. Earning more interest with the same amount of work.

Maybe the banks are spooked. Praying the CCP will paper over this company's $300 billion, that it is unable to make payments on.

Massive profit margins on the cheap money they've got available

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.