Every few days banks announce home loan and term deposit rate increases.

One year term deposit rates have been cracking 3% recently, first by Kiwibank, and now both ANZ and ASB among the main banks. Others are sure to follow. BNZ has raised rates too, but didn't adopt the 3% rate for one year. Challenger banks have been at that level for a while.

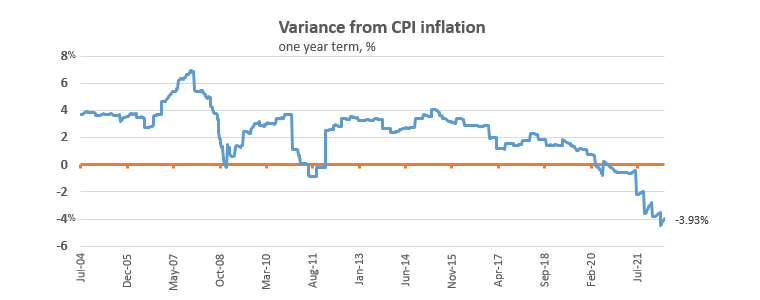

And 3% is a whole lot better than the 0.8% that applied for a main bank one year rate at the end of 2020, and into early 2021.

But let's not forget that back then, CPI inflation was officially 1.4%. (After it had fallen to 0.3% in March 2015.)

Now it is 6.9%, and rising.

As this tracking shows, the latest 3% term deposit rates are much 'worse' on an inflation-adjusted basis than then, in fact probably ever.

And also lets not forget these comparatives are before taxes. After tax, things are worse.

But the alternatives? The NZX50 is down 11% in a year. Bitcoin is down -40% (in NZ dollar terms), although gold is up +16% on the same basis. And now it looks like house prices are in for a serious downward correction; any 'investment' now could show capital losses in a year, made worse by leverage.

Savers and investors face tough choices - it is a matter of being active to make the least-worst choice. It's a time where the return of your capital probably takes precedence over the return on your capital. Bank term deposits have an advantage on that basis that many risk-averse savers like. Yes, they know about 'repression', but the chance for capital losses seems higher at present.

So more of us are sticking with term deposits. The amount invested has been rising again recently and is now up to $85 bln, and a higher level than a year ago after a long period of shrinkage.

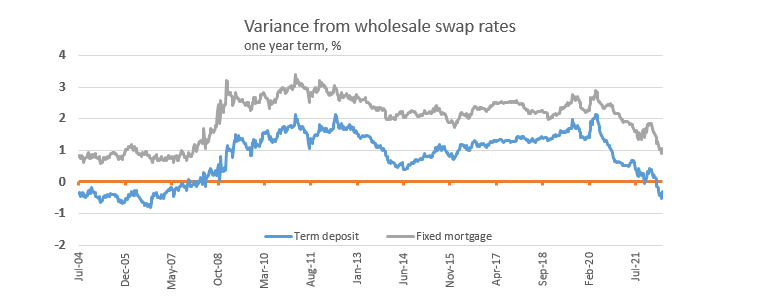

A similar analysis actually shows that savers have been getting a premium for their term deposits over and above the wholesale swap rate. That has probably been induced by the Reserve Bank's Core Funding Ratio regulation, which started in 2010. Without that, you might think that home loan rates would be at a premium to wholesale rates, and term deposit/savings rates would be at a discount. But with that regulation in place, savers have actually benefited. (Feel better now?)

Investors can get a +25 basis points to +35 boost in returns by using a top-offering challenger bank over a main bank. And that is generally so even in the six month to one year time frames.

One thing the swap rates signal however is that the track is relentlessly up. And that suggests tomorrow's offers will be higher than today's offers.

An easy way to work out how much extra you can earn by switching is to use our full function deposit calculator. We have included it at the foot of this article. That will not only give you an after-tax result, you can tweak it for the added benefits of Term PIEs as well. It is better you have that extra interest than the bank.

The latest headline rate offers are in this table after the recent increases.

| for a $25,000 deposit May 12, 2022 |

Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 1.50 | 2.30 | 2.40 | 3.00 | 3.30 | 3.40 | 3.70 |

| AA- | 1.50 | 2.20 | 2.45 | 3.00 | 3.30 | 3.35 | 3.60 | |

| AA- | 1.50 | 2.20 | 2.40 | 2.90 | 3.00 | 3.60 | 3.70 | |

| A | 1.50 | 2.30 | 2.40 | 3.00 | 3.65 | 3.80 | ||

| AA- | 1.50 | 2.20 | 2.40 | 2.80 | 3.00 | 3.30 | 3.60 | |

| Other banks | ||||||||

| China Constr. Bank | A | 1.80 | 2.50 | 2.75 | 3.25 | 3.25 | 3.45 | 3.85 |

| Co-operative Bank | BBB | 1.15 | 2.15 | 2.40 | 2.90 | 3.10 | 3.55 | 3.80 |

| BBB | 1.75 | 2.60 | 2.60 | 3.00 | 2.75 | 3.05 | 3.40 | |

| HSBC | AA- | 1.40 | 2.10 | 2.20 | 2.65 | 3.00 | 3.10 | |

| ICBC | A | 1.80 | 2.60 | 2.85 | 3.35 | 3.35 | 3.50 | 3.85 |

| A | 1.40 | 2.45 | 2.65 | 3.05 | 3.15 | 3.35 | 3.80 | |

| BBB | 1.40 | 2.15 | 2.30 | 3.10 | 2.90 | 3.40 | 3.60 | |

| A- | 1.50 | 2.20 | 2.40 | 3.00 | 2.90 | 3.30 | 3.55 |

Term deposit rates

Select chart tabs

Term deposit calculator

27 Comments

The "variance from CPI inflation" graph is a fun academic exercise, but it doesn't really tell us anything about changes in the value of our savings. A currency is not suddenly worth less just because the price of cauliflower goes up.

The rate of change in savings is measured by the rate of interest minus the rate of monetary inflation, which is not what's being measured by the CPI. The CPI measures the change in prices of consumer goods, some of which may be due to monetary inflation, some of which may not be. We don't know how much without digging deeper, but we can safely assume that much of the current CPI figure is due to price inflation, caused by supply chain issues, commodity prices, war, pandemics, etc.

In short, that graph probably makes things look a lot worse for savers than they actually are. When risk is high we should be focusing on return of capital, rather than return on capital. Even though savers are not likely to be making any money in a term deposit, they're certainly not losing it as fast as they would be in shares, property, or crypto.

I like the way you put "return of capital" I feel a lot safer knowing my money is in the bank. And so long as your business keeps ticking over why risk free capital.

Savers and investors face tough choices - it is a matter of being active to make the least-worst choice.

Always has been, very little is beating inflation right now. Picking up an extra tin of baked beans might end up the best investment decision you make over the next few months.

Enjoyed the article.

About 15 months ago I bought a decent amount of building supplies for a project I haven't got around to starting yet. Quite possibly the best investment I've made in the past few years.

I mentioned this on another thread, but: How about 'investing' in tangibles you know you will want in the future? Or can trade ditto?

The disjoint between debt-issued forward bets, digitally registered - money - and real stuff, is widening. Until the system collapses - which it will through mass disbelief, at some point - inflation will render your proxy ever-more poxy.

I've long reckoned stagflation, but if positive-rate interest-charging cannot be supported (by the reduced activity due to reduced energy input) then are we not looking as deflation as a possibility? Prices reduce to get people to buy, but nobody can afford to buy, so prices are reduced............. to the point where the extractors/suppliers of the energy, cannot get the next capex proposal past their bank.

Seems to me society can no longer afford itself; that above say $80/barrel, it needs to amass unrepayable debt, but capex is up around $120/barrel next-best-option. Investing in that scenario? Buy solar panels. Seeds. Tools. While you can.

Agreed. Hard goods have intrinsic value, which will be important once the imaginary value we assign to a lot of other things disappears. We are far too complacent about this given how vulnerable we are to supply chain disruptions.

I also agree that deflation is the much bigger threat. We consider this imaginary value to be real, essentially treating it as money. As this "value" disappears (which is happening right now in stocks, bonds, crypto, real estate, derivatives etc), the money supply contracts, which is deflationary by definition.

In the past when the 5 yr Mortgage was around 6% the 5 yr TD was about 4.5%. At the moment ANZ is 3.9 and Kiwibank is 4%. They seem to be about 0.5% low at the long end. The 1 yr looks about right. Soon to change though, 0.5% OCR rise in less than 2 weeks.

When would be a good time to move from Bonus Saver to Term Deposits? I'm thinking shorter term until interest rates stop increasing? Some three, some six months after the next hike? Or wait for the one after that?

You already want to be in for 9 to 12 months. To much lag in them rising at present. By the time they raise the 12 month, the old rate then applies to the 9 month and you have already had your money in for 3 months. No point waiting you get zilch in a standard account. Go a year or less, its only going one way. Mine has gone from 1% to 2.3% to what I expect will be over 4% come Feb 2023.Basically it will double evey year and 8% is not out of the question.

I've recently sold an investment and now I'm cashed up, no debt. Trying to position for maximum return, minimum risk, but not sure I want to lock in for 12 months, there are too many unknowns. Trying to forecast further out than a few weeks / couple of months is futile in my opinion. I would think at least waiting for the next OCR would be worth it. Look what happened to Term rates after the last one.

Took a couple of months to even move after I put mine in in February, was not worth waiting. Things do seem to be moving much faster now at the banks however, there did seem to be some hessitancy as to which way the market was moving but now that has clearly gone and its up, up and up at least into next year. The next 50+bps move should see rates at 1% above what I'm currently getting. Dont really care, sure beats 1% returns.

Banks are unlikely to offer higher TD's if they have sufficient funds to cover current borrowing demand especially if their policy is to reduce demand further by imposing more restrictions and high service test levels, I suspect all these factors contribute to current poor return on Tds although at present TD's seem a safer bet than other assets,

If the economy starts to tank and banks are getting stressed are Kiwi Bonds an option? Is there anything more secure that has a better return?

Hey I purchased some kiwibonds in early 2020 when other people were burying cash in their backyards or hiding it in freezers!

Rate was terrible but slept well at night knowing if there was a banking issue, I wouldn’t take haircut on that money.

Looking great to me, will be able to buy a new car next year and still get the same return from the TD. Rates are really starting to move now, 3% for a year, this is triple my last term of 1% and I fully expect it to be over 4%, possibly even closer to 5% in Feb 2023. Banks were very slow to move but clearly we are on a roll now. Next RBNZ hike will be at least 50bps. Happy days.

I agree - 5% by next Feb is quite likely indeed.

Already 3.6% for 3 years and we have not even got going yet. My pick is 4.8% for 1 year in Feb 2023.

I am thinking likewise Carlos. Hang on to your cash. Free capital means you can move when the time is right. And I have forest that needs pruning and thinning, all good for local labour which in turn feeds in to the local economy.

As counter-intuitive as it seems and as hard as it is to do, now is actually the time to load up on equities.

As an earlier poster said 'fortune favours the brave'. Some people get very rich during recessions.

I bought up large during the C-19 crash, with pleasing results. But now the US looks headed for a bear market, and sometimes these can last years. Mind you, Warren Buffett recently spent about US$50 billion on shares...

rastus,

If you're that certain, then good luck to you. I have been in the game professionally and personally for the best part of 50 years and the most I would do right now is add a little to a few defensive stocks with decent dividends.

My bet is on markets still going lower.

Yes it is. It just takes cold blooded thinking. I am buying some stocks now, even if I know that this is probably not the bottom of the cycle yet, and there is still room for downward pressure, but I have missed the 2020 dip and I do not want to miss this one too.

Rastus - do you have evidence that equities will continue to rise medium term or are you just buying the dip?

It seems that commercial property, especially industrial, is the only investment left now with good income returns and capital gains.

But could that be next to tank, given the spiralling costs and pressures on the businesses that lease these premises?

Some commodities are doing well too obviously, but I'm not sure which NZ trading platforms offer these (preferably via PIEs) - any pointers?

I love commercial and industrial property. I have not sold any investments of mine in this area, as I am planning to ride this cycle.

By the way, you can trade many EFT's (not all) on the NZX and ASX online with ASB securities. "Superlife" also gives you a reasonably good variety of EFT's.

Nice analysis. The issue you have with the first chart is that the CPI figures are backward looking whereas TD rates on offer make assumptions about future inflation. If you could get implied break even inflation (from the difference in yields between government nominal and inflation indexed bonds, since these are regarded as the best predictors of inflation), that would be a more meaningful assessment of how poor the real returns on TDs currently are.

Alternatively, you could lag the actual CPI data to match the TD rate offered 12 months earlier but this won't tell you how things are placed at the moment, only how well TDs have returned in the past.

As you say, after tax the results are pretty unappealing and reflect financial repression.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.