Research analysts with investment services company Forsyth Barr are seeing a potential "return of animal spirits" in the second half of next year - and a number of things, including house prices, could benefit.

In a year ahead equity strategy review, research analysts Andy Bowley, Aaron Ibbotson, Rohan Koreman-Smit and Andrew Harvey-Green have focused on five investment themes for 2023. One of these five is: "Inflections and the return of the animal spirits".

"These inflections have the potential to ignite the animal spirits of the market should they arrive on time and in full," the analysts say.

As well as looking a five investment themes for the year, the analyst have also identified five "inflections" they are looking at that could spark up a recovery in the second half of the year. These are: Inflation, interest rates, GDP, house prices, and government.

For those who've been watching house prices sink all year this year - the bad news is that of the five "inflections", the Forsyth Barr analysts are least confident the housing market one will come to pass.

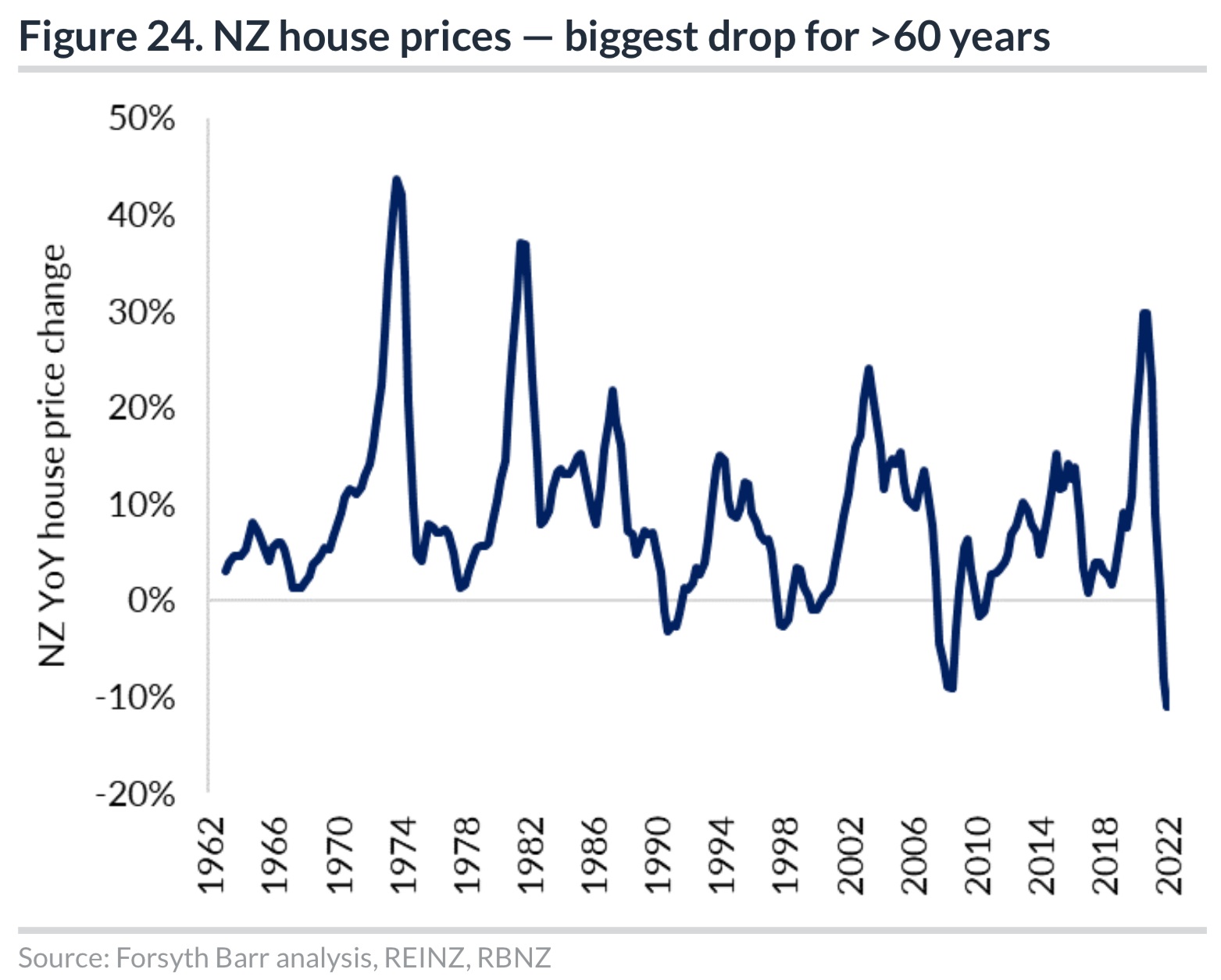

"House prices are the most difficult inflection to call and the one we have the lowest confidence in 2023," the analysts say.

"The continued difficult backdrop for affordability suggests that house prices could come down a long way still. Our base case is for prices to drift down through the year.

"However, this theme is about the return of animal spirits and if we position ourselves towards the end of 2023, we believe there is a decent probability that an inflection will either have happened, or be anticipated shortly," the analysts say.

In terms of background they say NZ has experienced approximately 12 months of continuously falling house prices, "and in nominal terms we have already seen the biggest drop in 60 years".

"We are already closing in on the longest continuous drop in 40 years (18 months over the GFC).

"If house prices fall until the end of 2023, NZ will also have had the longest nominal drop in house prices since at least the 1960s.

"Assuming a pace of [about] 1% per month and inflation in-line with [the Reserve Bank] RBNZ's forecasts, there will be a peak to trough real house price drop of [about] 30%.

"All in all, this is starting to look like a trough to us. If we and the market are broadly right about interest rates."

On interest rates, the analysts say the wholesale interest rate market is currently 'pricing in' a first RBNZ Official Cash rate cut in October 2023 versus the RBNZ's expectations of mid-2024.

"A rate cut in 2023 should be in the price. However, we believe the first actual rate cut this cycle has the potential to act as a catalyst for both the housing market and the yield heavy part of the equity market."

The analysts say Inflation "is the defining characteristic of this bear market".

"Without an inflection in inflation sometime in 2023 it is difficult to envisage an inflection in any of our other focus areas and, by implication, in the market."

But they say while they note the signs wage inflation is getting entrenched, they point to easing petrol prices, slowing rent growth and easing new house costs.

"Overall, we share the RBNZ's view that CPI is likely to stay high in the December and March quarters, but believe there is a chance of an inflection during the March quarter."

On next year's general election, the analysts say they suspect that "a change of the guard" in Wellington "has the potential to at least temporarily reignite the animal spirits in the business community".

"Whether it lasts will depend on what happens next in Wellington, but more importantly in the country overall."

As stated, higher up, the 'inflections' section of the Forsyth Barr report is just one of five investment themes for 2023. In summary those themes are:

- We expect increased gearing and balance sheet scrutiny, given higher interest rates. We would not be surprised if a few balance sheets need repairing.

- Labour availability and labour costs. We expect continued labour market tightness across most sectors but pockets of easing pressure as the year unfolds.

- The New Zealand macro environment looks uncharacteristically weak relative to the rest of the world. Companies with offshore exposure are preferred.

- The travel recovery is likely to continue with gradually increasing aviation capacity.

- Inflection and the return of animal spirits. We consider five potential positive macro inflections for a 2H23 recovery; namely — inflation, interest rates, GDP, house prices, and government.

The analysts say the RBNZ "has done its best to make sure none of us approach 2023 with any illusions of good times ahead".

"Mortgage rates have hit a 10 year high, inflation is expected to remain stubbornly elevated, and the icing on RBNZ's economic cake is its forecast of four quarters of declining GDP. This bleak backdrop will clearly influence 2023 to a large degree.

"But 2023 is 12 months long, and towards the end of the year we see numerous potential positive inflection points. Less bad is often good enough for the animal spirits to return and a year-end market rally is not off the table."

The analysts say in choosing their five stocks to watch in 2023 they have leaned on companies with the majority of their exposure overseas - (Infratil [IFT], Vulcan Steel [VSL], KMD Brands [KMD]) or with attractive valuations (Oceania Healthcare [OCA], SkyCity [SKC]) "where we think that the bad news is firmly in the price".

"We have done our best to avoid companies that we see as particularly exposed to labour shortages, or have debt concerns."

16 Comments

Some good analysis in that article....

"We are already closing in on the longest continuous drop in 40 years (18 months over the GFC).

"If house prices fall until the end of 2023, NZ will also have had the longest nominal drop in house prices since at least the 1960s.

"Assuming a pace of [about] 1% per month and inflation in-line with [the Reserve Bank] RBNZ's forecasts, there will be a peak to trough real house price drop of [about] 30%.

As we are already seeing auction dev sites sell 30% off cv at 2k per sq m, I expect that we may see this down around 1k per sq m at the very bottom.

It seems like every day the plunge protection squad is out in force writing articles about how we are nearly at the bottom.

We aren't.

blink and you'll miss it.

Sir John Key unveils his predictions for the economy in 2023 | Newshub

"7% mortgage rates, guaranteed"

Coming from a bank chairman...

They understand there is a risk that things turn non-linear....

Things turn non linear very fast above a certain mortgage rate. Pretty sure 8% would wipe most people out who have bought a house over the last 3 years or so. The RBNZ can only push the rate so far and hence this is why they have been so slow to do so with multiple warnings along the way because above a certain threshold its wipeout.

His explanation and reasoning for why things were happening was easy to understand and digest for the financially illiterate like myself.

A very good interview imo.

Or, an alternative opinion:

The world economy is lurching toward an unprecedented confluence of economic, financial, and debt crises, following the explosion of deficits, borrowing, and leverage.... overborrowing has been going on for decades, for various reasons. The democratization of finance has allowed income-strapped households to finance consumption with debt. Center-right governments have persistently cut taxes without also cutting spending, while center-left governments have spent generously on social programs that aren’t fully funded with sufficient higher taxes.....The explosion of unsustainable debt ratios implied that many borrowers—households, corporations, banks, shadow banks, governments, and even entire countries—were insolvent..... Once the inflation genie gets out of the bottle—which is what will happen when central banks abandon the fight in the face of the looming economic and financial crash—nominal and real borrowing costs will surge.

https://www.marketwatch.com/story/high-debts-and-stagflation-have-set-t…

Great article.

The upshot of all this is that those same forces which were inflationary on the way up, are going to be deflationary on the way back down. These huge mountains of debt will either be paid back or defaulted on, but in either case the debt will be extinguished. This is deflation by definition, and is going to cause all sorts of problems, both economically and socially.

Not bad analysis, I broadly agree. As I have stated many times before, I think house price declines will have bottomed out by late 2023. But I think the extent of the decline will be higher than 30% in real terms - I think around 35% is more likely.

I am certainly more bearish than them on the domestic economy and employment, though.

All this optimism explicitly assumes an inflection point in inflation that allows CBs to reverse gear.

Why? What inflationary force will be defeated by then, and how?

it reads to me like generic, consensus, return-to-the-mean thinking. Mild recession and CBs pivot next year. It’s the most bullish conjecture one can make without sounding like an outright idiot, so it’s what we get.

The main inflationary force CB’s need to defeat is wage rises, so any inflation reduction must be focused on that. The method of course is orc rises until the economy is starved on money.

when: after a substantial amount of people have had to roll over to very large interest rate increases. Probably mid 2023

Its reasonable to think that CB’s will win that fight, but at what cost? That’s the real question.

How hard the fall.

I like that graph. Next time someone tells me house prices double every 10 years I'll show them that. They regularly have periods of high growth that tapers off. so most of the growth in that 10 years is actually based on that initial 2 years of large increases.

Insane behaviour=severe repercussions.

Unless you are a reserve bank guv'nor

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.