By Gareth Vaughan

According to Statistics New Zealand's Consumers' Price Index (CPI) inflation is running above 7%, its highest level since 1990. The Reserve Bank, tasked with targeting CPI inflation of between 1% and 3%, has been aggressively increasing its Official Cash Rate, which means higher interest rates flowing through to borrowers and savers.

Given the importance of the CPI as a measure of the changes in the price of goods and services for NZ households, do we have its settings right? What's in it, how is this determined and measured, and is a quarterly CPI release frequent enough?

To address all this we spoke with Bill Rosenberg in a new episode of interest.co.nz's Of Interest podcast. Rosenberg, now a Commissioner of the Productivity Commission, is the former Policy Director and Economist at the Council of Trade Unions. He was also one of nine people Statistics NZ appointed to a committee to independently review the CPI 10 years ago.

Rosenberg notes mortgage interest payments are excluded from the CPI. And while housing rentals and purchases of newly constructed dwellings excluding land are in, sales of existing houses are not. The CPI is "an index is designed for the Reserve Bank," Rosenberg says and the Household Living-Costs Price Indexes (HLPI), another Statistics NZ series, is a better measure of inflation for NZ households. It includes mortgage interest payments.

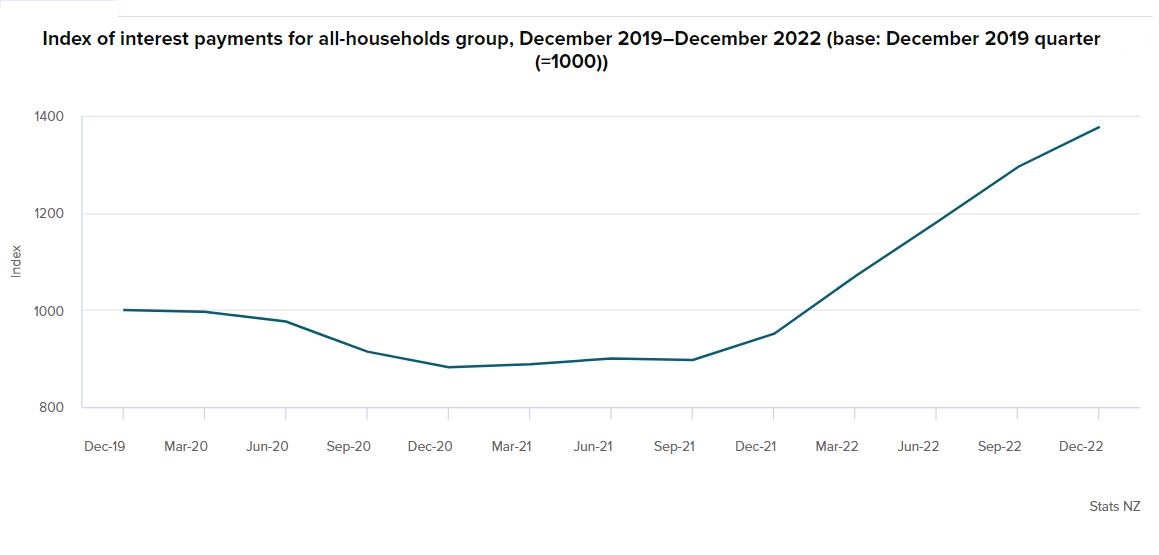

The latest HLPI figures show the annual inflation rate in the December quarter for all households was 8.2%, significantly higher than the CPI's 7.2%.

The HLPI breaks out different indexes for all households being the average household, beneficiaries, Māori, superannuitants, highest-spending households and lowest-spending households. The CPI, in contrast, measures how inflation affects NZ as a whole.

Thus the HLPI is able to show highest spending households experienced the biggest annual inflation increase of 9.4% in the December quarter because they spend more on interest payments than other household groups.

"I think there should be more focus on the HLPI, the Household Living-Cost Price Index," Rosenberg says.

"It's more representative of the costs that people face and people can actually go to it and see 'roughly speaking I'm [a] middle income household, I can see how my costs have been changing'," he says.

For much more on how inflation is measured listen here.

You can find all episodes of the Of Interest podcast here.

27 Comments

(Personal insult removed, Ed. Stick to the issues please).

???

Basically, it's nonsense to use an inflation index that also measures the tool you are using (interest rates) to control inflation. Obviously that would lead to the RBNZ increasing interest rates when inflation is low in order to stimulate inflation, and lowering interest rates when inflation is high - the absolute opposite of what it should be doing. And don't cast aspersions on the Productivity Commissioner when you post.

Yep, this was immediately obvious to me. If they want to use HLCI then the RBNZ would need some new levers to pull. Or exclude interest costs, and hey, we're basically back to using CPI.

Edit: but its interesting to imagine if the did switch to the HLCI and retained the OCR as the way to control inflation. Inflation increases, so they drop the interest rate, but due to the time taken for mortgages to roll over it does nothing perceptable for 6 months+, so they keep dropping the interest rate, then it catches up with bit of a rush and we get into deflation, so they start jacking up the OCR to raise us back up. A bit like a poorly loaded trailer on the motorway, small wobbles then larger and larger, then you're looking into oncoming traffic and surrounded by a cloud of tyre smoke..

Tell me you don't understand control theory without telling me you don't understand control theory.

Given much consumer spending is via cards or online and supermarkets, car yards etc. publish current prices on their website we should be able to do some CPI measure in real time by just scraping data. If we could just get better data resolution on CPI than quarterly updates I'd be placated.

Made a curry yesterday. Kumara, chickpeas, onion, garlic, coconut milk, spices, rice. Took half an hour, tasted amazing. 6 portions for about $10. Froze half of it (family of 3) so that's one "takeaway night" taken care of.

Someone used to work for me was always broke, has 3 take out coffees each day, would describe her hobby as "tapas" and is well paid for what she does.

Yes that ignores a lot of circumstance. I'm still convinced that you can budget your way through just about anything. We have so much entitlement around lifestyle.

Its not what you earn, it's what you spend.

Only to a degree before things are terrible. For example, if you want to save money by living in your car, eventually you're going to be in a situation where you get fired, get too sick to work, or something else, or you can't get work because your lack of access to a shower and an iron means you can't get work.

There's only so much you can cut. Earning more while retaining the cuts in spending is how you get ahead.

Agree. Basic family economicsc are no different from any business: control/lower the bottom line & increase the top line until you can see clear daylight.

Its a great idea. Probably the best time to do this would have been over the last 10 years - when accomodation prices were skyrocketing. - it would have forced the RBNZ to address the asset bubble - if it was based on true inflation being very high then.

One gets the feeling that if changed now we may end up with a biased inflation number based on RBNZ preferred calculation - and an attempt to protect the overleveraged or lower the OCR too early by somehow including falling asset values in the equation.

Given the current situation it seems best left alone.

interest rates are back to where they should be.

if the inflation target is 2% and interest rates are 2% then debt is free.

If interest rates are 2.99% and inflation is 7%, as is the case today, borrowing money is wonderful!

Very few had the wisdom to borrow at 2.99% for 5 years, because the consensus at the time was that "Mortgage rates have to go lower from here. They could even go Negative!". And just like today, when the 5 years Fixed is ~7%, the same thinking applies. So very few will lock in here.

And the chances are that those who do, will look back to say the same thing in a couple of years time - "If interest rates are 7% and inflation is 17%, as is the case today, borrowing money is wonderful!"

(My opinion remains the same today as it was back in 2021. Anyone with the capacity should be borrowing anything they can and sticking it into a qualifying Offset Account. Zero cost and give you the liquidity tomorrow at today's, still, elevated asset prices to borrow against)

Is an offset account kind of like a overdraft on your mortgage? Genuine question. Can you expand on your theory? Is it that you borrow the money on the mortgage but keep it in the bank not paying interest but can use it as a hedge if mortgage rates go up?

Kind of.

It's not a hedge against interest rates doing anything in particular. They could go to 2% or 20% and the Offset interest on a 100% Offset Balance is still the same - zero.

What it is a hedge against is Asset Prices Falling and, especially, a Credit Crunch (Liquidity)

If today you can borrow, say, 80% against your property, and it's valued at $1m = $800k in the Offset Account.You control that liquidity. If asset prices halve, and you wanted to borrow against that same property in the future you'd only get 80% of $500k = $400k - that's IF you can borrow at all.

(In the UK some years back, I owned a property outright. I wanted to refinance it for other purposes and borrow 50% of the value at 6% when the rental income was already paying me a net 12% (rented out to a Dutch law firm for a London staff base). My bankers looked at the figures and politely said "Looks good. But, sorry about that. We aren't lending to the residential property market at the moment". The property market was in free-fall at the time. That's sort of experience tends to stick in my mind)

That makes sense. Any advice for someone in cash looking to buy in the next few years or when the market starts to feel like its hit the floor?

I thought this piece could have gone a bit deeper, there are some vital facts missing.

First of all, the cost of land, existing houses, and the cost of servicing a mortgage were included in the CPI until removed by Shipley and Bolger. In the US, it has been calculated the CPI would be twice that reported if the same methodology were used now as in the 80's.

Second, blue collar wages are generally tied to CPI (although I have seen companies use the wage price index where that benefitted them). As housing has been excluded from CPI over the last 40 years, during a time of exponential money growth, and hence housing costs, real wages are going down.

This is why people struggle to survive.

By removing those components from the CPI, house prices can rise unconstrained by higher interest rates, with the added bonus workers wages decrease in real terms.

The system is so stacked against workers in favour of property investors, they now have no chance.

The HLPI is broken down in income categories and expenses (renter, mortgagor) categories but why is there a race category in it?

Oh dear, I give it 4 levels of posts down from this before somebody is called racist, and then another 3 levels deep before Godwins law applies.

Because including demographics such as race gives more focused detail about how inflation is affecting different communities within our nation. Ideally, the data would be so refined it could be viewed at the neighborhood or even individual level.

So, its to support racist assumptions that ethnicity defines you & determines how poor you will be.

Correlation is not causation.

"Because including demographics such as race gives more focused detail about how inflation is affecting different communities"

OK, but there is only one race, or community that has the privilege of getting the detail you speak about, why?

If we do want to have a better understanding of inflation on demographics, why only have a Maori category? Why not an Asian or Polynesian or European etc.. category? It's like having an age category, but only for say 30-40 year olds, but no other age group.

give him some credit for not dragging climate change into it

My issue is that we're mixing a "race" category, together with "finance" categories such as the income source or amount or the expense. For example a Maori person has to be part of the other categories anyway.

Sure the HLPI has it's place if we're trying to analyse households costs and their impact to the economy... but it is ludicrous to consider this factor as something that the RBNZ should be looking at when targeting inflation.

You would get into a spiral of feeding an ever increasing debt monster, when in fact what we need is less debt!

Only once house prices have bottomed out, and we have acceptable DTI ratios in place, we can have the discussion about house prices (REINZ HPI) being included in inflation measures.

Full house prices should be put back into the CPI. They are the biggest consumer good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.