A growing proportion of new mortgage money is being fixed for longer terms.

According to the latest monthly figures in the Reserve Bank's recently introduced data set on new lending fully secured by residential mortgages, the one-year fixed term remains most popular for new owner-occupier mortgages, followed by the two year term. But the three-year term has surged in popularity in the last couple of months.

This would appear to have been prompted by major banks starting to offer appreciably lower rates for the three-year term in comparison with shorter terms.

This particular data series, only introduced three months ago, covers new lending or facilities loaded in the reporting month. This is different to other RBNZ series on mortgage lending, which report new mortgages on the basis of when they have been committed to, rather than when they've actually been taken up.

The RBNZ said total monthly new residential lending was $6.2 billion in June, up 7.9% from $5.8 billion in May. In comparison with June 2022 new residential lending fell 1.7% from $6.3 billion.

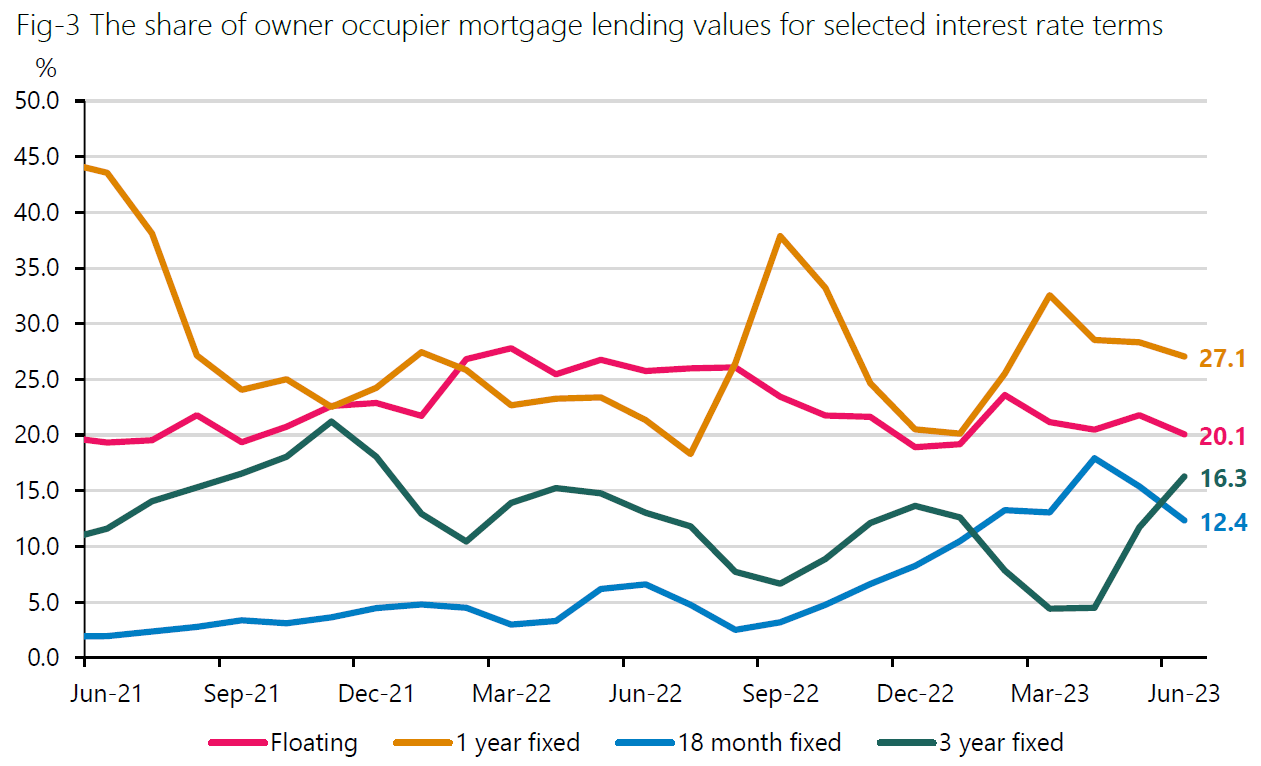

The share of total new residential lending on fixed interest rate terms rose from 77.9% in May to 79.6% in June. The share on floating terms fell to 20.4%.

In terms of new owner occupier lending this rose to $4.8 billion in June, up 8.3% from $4.4 billion in May.

The most popular interest rate term for new owner occupier mortgage lending was still the one-year fixed, accounting for 27.1% of all new owner-occupier lending. However, this share has been falling from a recent high of 32.6% in March. Two-year terms were next most popular in June, accounting for 18.3% of the owner-occupier, down from 18.4% in May and a recent high of 24.8% in March.

Lending on 18-month fixed terms fell to 12.4% of new owner occupier lending, from a recent high of 17.9% in April.

But the three-year fixed term mortgages have continued to rise rapidly from a situation in which they were barely being considered by borrowers.

In April, just 4.5% of owner-occupier mortgage money was taken up for three year terms. That surged to 11.7% in May. And now in June some 16.3% of new owner occupier lending ($775 million-worth) was locked in for a three-year term.

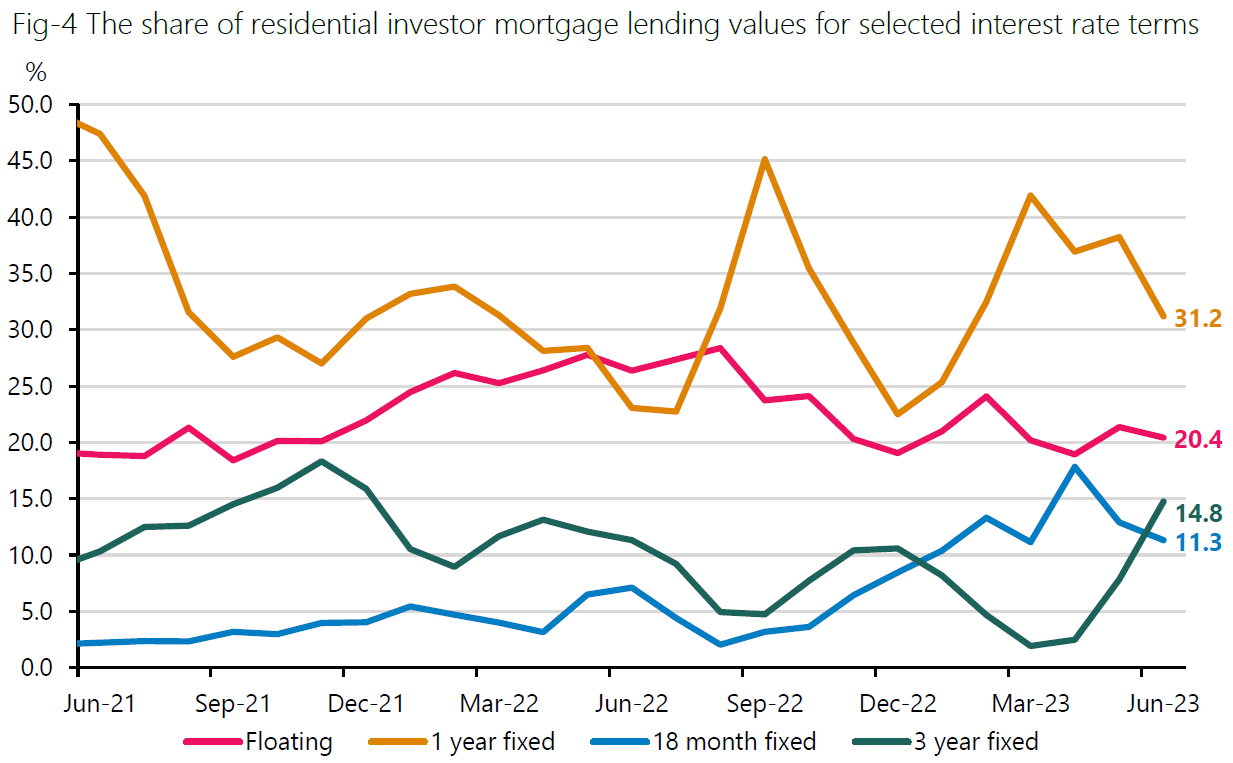

It has been a similar story in the past couple of months for the housing investors too.

As we know, the residential investor mortgage market has been pretty quiet. But the preferences for fixed terms have mirrored those with owner-occupier mortgages.

The amount borrowed by the investors remained at $1.3 billion in June, the RBNZ says.

"As with loans to owner occupiers, one-year fixed terms were also the most popular, making up 31.2% of new lending. This share is considerably lower than a recent high of 41.9% in March."

The two-year term was next most popular, but it was only just ahead of three-year, of which 14.8% of the money (nearly $200 million) was fixed.

23 Comments

Does the time series in the charts only go back to June 2021? Really needs to go back further to draw any real insight.

More people are locking in longer because it’s cheaper or because they can’t afford for it to go higher.

Adding the series for Floating+1Y and they 2Y+3Y (short vs long) would probably provide a clearer picture.

The reluctant “investors”, those that can’t sell, will all be keeping short too to avoid any break costs.

I'm not sure why people are still going for the one year rates, with those rates now around 7.2%. In a year, the one year rate will still be around 7%. I would only go for a one year rate if I was looking at selling, and in fact it would make more sense to go for a 6 month rate if that was the case. I'm surprised more people aren't fixing for 4 or 5 years, and surprised also that this data isn't included in this article.

House price’s down around 20% in last 18 month and looks like this downward path will continue. Its amazing that people are so conditioned that they would buy while house price’s are falling 10k a week, best to just wait or you will join the many in negative equity with rather large mortgage payment for next 30 years.

From a NZ property investor perspective, the mental conditioning is a bit like Pavlov's dog - see the house for sale and start dribbling. Even if the meat has gone rotten.

There are very few investors out there buying property at present. However, the data is showing FHBs still very active, and accounting for nearly 25% of the market. They can only buy if the bank lets them ( based on 9% stress test) so clearly there are people out there wanting to live in their own home and managing to find an affordable home for themselves.

Maybe the real estate 'industry' has more in common with Pavlov than his dog did. After all, it's the results that matter.

Pavlov removed the esophagus of his lab dogs, and created a hole in their throat. When the dogs ate, it would simply fall out of the hole and not make it to the stomach. Fistulas (holes) placed further along the digestive system, attached to tubes, allowed him to collect, measure, and study the gastric juices. As an added bonus, he also collected the juices and sold it as a cure for indigestion. To make extra money, he also hired an assistant to gather up gastric juices from the "gastric juice factory" - five large dogs harnessed to a crossbeam and attached to a container by a tube coming out of their fistulas. They were placed on an angle so that they were facing a bowl of mince meat in front of them, which the dog would eat (before it fell out of their neck holes onto a collection plate). The dogs did not last long.

https://www.iflscience.com/pavlov-s-dog-experiment-was-much-more-distur…

Yes, the addiction is killing them, but they come back for more.

Another theory - females, and their love for houses. They go nuts on handbags priced the same as a small car. Applying that purchasing logic to houses, we end up where we are.

You lost me with that theory.

The theory is that the housing market in New Zealand isn't always rational. It's emotionally driven. This theory is correct.

I'd be very surprised if there are any rationally justifiable buying opportunities available currently.

Types of buyer...

Oldies ( near death) - plenty of dosh, buy what they love no matter the cost or time.

Oldies ( down sizers) - as above if wealthy, if poor wait for market to fall?

Smart regular/poor people - play the market

Smart rich people - GAF or DGAF

Dumb rich people - DGAF just buy on emotion

poor people - council flats motels and cars for them

Do you own? Or are you still waiting for the “right time”?

TL,DR:

A noisy data series has gone up and down between 2021 and now, and is now back to its 2021 value.

The heavy selling by bank economists that "rates will be higher for longer" is clearly paying off.

Other economists have quite divergent views. Why? Perhaps because their salaries and bonuses are not tied to bank profits.

The Commerce Commission has a lot of work to do.

And after that some main stream media outlets need to be held to account for why they only parrot the views of bank economists. (Case in point today where in one article the NZH quotes just one bank economist and references two other banks when concluding "rates will be higher for longer".)

So at the end of the day who do we believe.

Adrian Orr?

Bank Economists?

Hawkes Bay and DGM with their "10% guaranteed"?

The mythical "Prophet"?

TTM? (Who seems to have vanished)

The amateur commentators in here seem to be closer to reality.

Bank economists aren't pushing predications, they're just pushing.

Do what I did. Do a few Economics papers at Uni each year. Or even just one each year. Especially the Economics History papers which are actually extremely interesting.

It makes it much easier to filter fact from fiction in an arena where there is ZERO REGULATION or ACCOUNTABILITY.

The really interesting thing about this data is how many mortgage holders are yet to pay current prices. Still quite a few on 2020, 2021 rates, and others on lower 2022 rates - most will be progressively rolling over onto much higher rates over the next 9 months. Highlights OCR rate change lag, that things will get tougher for a while yet, and that even when OCR starts reducing the same lag will occur (or prob worse as banks reduce rates much more slowly than they increase them).

Correct, any OCR reduction will lag a lot because higher rates are forcing people to fix. I doubt it will be much but even 1% will make a difference.

Corporate hedging profiles taper of a lot post 5 years for that exact reason, fixing for too long puts a lot of risk in the business.

There's a lot being said about people rolling over to the higher rates, but no facts. It's all guess work. Mostly based on past survey data, statistics and historical trends.

Here's some facts.

I fixed for 5 years at the start of 2022 for 4.89%. I have no idea what the rate offers will be like at the beginning of 2027, and I don't care. As an OO, I will make it work, and I have another 4 years of paying down the principle.

I do have a small separate mortgage top-up with a 5 year term that is fixed for 3 years at 5.39%, but I have increased repayments on that to finish it by the end of the fixed rate period in 2 years. When it's done, that money will go to my regular mortgage, knocking 4 years off it and saving a lot in interest.

Do I see interest rates being significantly lower than 5% over the next 2 to 4 years? Absolutely not. They will be lower than they are now, but still above 5%. Even if the OCR and/or swap rates drop, banks will only be quick in dropping deposit rates, not loan rates.

Obviously this is my situation, and it ain't that bad. Other mortgage holders will have their own. Maybe better. Maybe worse. What is not known for sure is how many are going to be royally stuffed when they re-fix.

Bit of anecdotal evidence ... I was at a bank a few days back talking about refinancing and asked the senior banker whether they re-fixed at 5 years when rates were at 2.99% for 5 years. They said no. They went for 3 years. I asked why not 5. They said they didn't expect rates to be this high now. So I asked, what rate did they expect after 3 years. .... Blank look. Then the penny dropped. They looked really, really miffed. Pissed-off would be a better description. They went for 3 years based on their bank's economists recommendation that was provided with absolutely no reasoning whatsoever.

I don't know why most of financially educated borrowers or mortgage brokers did not push to lock in 5 year rates which was 2.89% - 2.99% at the time.

If only 30% of borrowers did that the banks would be crying now...

I fixed in Feb 2021 for 5 years at 2.99% expiring in 2026... I get 5.9% on term deposit now..

I always heard the brokers always pushing thru 2 year rates...

Only 5% did what you have in the first quarter of 2021.

DP

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.