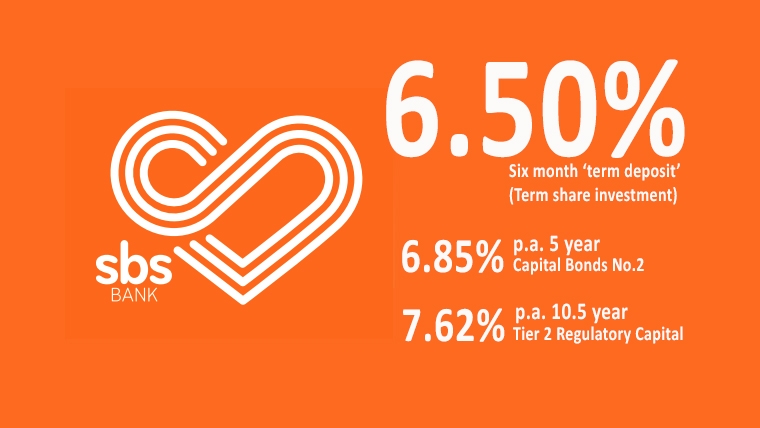

SBS Bank has launched a new 'special' term deposit rate: 6.5% for six months.

This offer is for "a limited time".

At the same time, they have reduced their one year rate to 6.05%, down -10 bps.

However, the six month term will be attractive. Savers have show their preference for shortish term deposit terms. This new SBS Bank rate is a full +50 bps higher than any main bank for that term.

SBS Bank has regularly offered attractive term deposit 'specials'. The most notable one was 6.7% a few months ago, for a one year term. That was a short promotion from late October to early November, 2023. If this one also draws significant funds, it might be short too.

SBS Bank term deposits (formally, "Term share investments") can have interest paid as frequently as monthly, which if you are well organised to reinvest the interest can be a slight benefit - although for a term as short as six months, it won't be much. There's a $5 mln upper limit on what they will take from any one investor, but you can get in with only $1000.

The SBS Bank credit rating is BBB, at the bottom end of investment grade.

Interestingly, the bank just raised $60 mln in a tier 2 capital bond, paying 7.62% yield to maturity over 10.5 year for those funds from bond investors.

And they have open for retail investors a 5 year, 6.85% pa offer for their "Capital Bonds No.2". It might work effectively as an upsell for yield-hungry investors.

Overall, bank term deposit rates have been static for a while, although about two weeks ago some of the majors tweaked some rates lower.

And on the lending side, there has been a minor slippage in carded home loan rates as banks fine tune their market strategies in the midst of a misfiring summer real estate selling season.

Those moves were in contrast to the generally firming wholesale rates as evidenced in the swap and bond markets. They rose again yesterday (Friday). The longer term rises are responding to global forces, but the short rates are responding to the RBNZ's hawkish signals about inflation indications which aren't reducing as they would want. Those signals induced the ANZ economists to suggest the RBNZ might hike the OCR in the next two reviews. ANZ is not saying that is what the they want the RBNZ to do; they are saying the RBNZ could well do it based on those inflation signals. Those ANZ observations themselves had the effect of firming up short term wholesale rates.

With ubiquitous 6% plus rates for the terms where almost all the term deposit rates are concentrated, and with prospects the OCR will rise from here over the next three months, savers could reasonably expect that retail term deposit rates might firm from here. If the present 5.50% OCR actually does become 6% by May, some of this increase could well flow through to retail TD offers, especially by challenger banks.

However, if rate rises also push up short term borrowing rates, the usual extra mortgage demand during the February to Easter real estate selling season could either shift borrowers to longer fixed mortgage terms that don't get this pressure (say three year fixed terms), or it could quell demand for buying houses because of the affordability stress from higher rates. In that case, banks will avoid having to pay extra for deposits because the loan demand isn't there.

A quick check of the swap rate chart below shows how fast wholesale markets are responding. In fact the +40 basis points jump in February so far for the one year swap rate is the largest rise following a long stable or easing period, since 2014.

The latest headline term deposit rate offers are in this table after the recent increases.

| for a $25,000 deposit February 24, 2024 |

Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 4.30 | 6.00 | 6.00 | 6.10 | 6.00 | 5.75 | 5.50 |

| AA- | 4.40 | 6.00 | 6.10 | 6.10 | 5.90 | 5.65 | 5.35 | |

| AA- | 4.30 | 6.05 | 6.10 | 6.10 | 5.90 | 5.65 | 5.35 | |

| A | 4.40 | 6.05 | 6.10 | 6.15 | 5.70 | 5.35 | ||

| AA- | 4.30 | 6.00 | 6.10 | 5.90 | 5.80 | 5.50 | 5.30 | |

| Other banks | ||||||||

| Bank of China | A | 5.20 | 6.10 | 6.20 | 6.30 | 6.10 | 6.10 | 6.00 |

| China Constr. Bank | A | 5.20 | 5.70 | 5.80 | 5.90 | 5.85 | 5.65 | 5.50 |

| Co-operative Bank | BBB | 4.20 | 6.10 | 6.10 | 6.15 | 6.00 | 5.80 | 5.55 |

| Heartland Bank | BBB | 5.50 | 6.05 | 6.15 | 6.30 | 6.10 | 6.10 | 5.85 |

| ICBC | A | 5.00 | 6.10 | 6.15 | 6.15 | 6.05 | 6.00 | 5.55 |

| Kookmin Bank | A | 4.40 | 5.60 | 5.70 | 6.00 | 5.00 | 4.60 | |

| A | 5.05 | 6.15 | 6.20 | 6.30 | 6.10 | 6.10 | 5.90 | |

| BBB | 4.20 | 6.50 +0.45 |

6.15 | 6.05 -0.10 |

6.00 | 6.00 | 5.90 | |

| A- | 4.25 | 5.90 | 5.90 | 6.00 | 5.90 | 5.75 | 5.50 |

Term deposit rates

Select chart tabs

Daily swap rates

Select chart tabs

Term deposit calculator

4 Comments

Rates up and go...

What happened to all the talk of them dropping?

Rates are still down from a few months ago, ASB were offering 6.26% for 12 months so I grabbed that. Looks like rates will still be hovering about 6.3% at the end of 2024.

They are just getting in early before the OCR hikes. Pretty soon all the other banks will be offering similar.

someone is anticipating a rate increase, which is a good possibility. SBS is a challenger bank, however if the OCR is at 5.5% and they and offer 6.1%, then if it increases .25%, they could offer 6.35% short term TDs and still maintain their margin.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.