By Gareth Vaughan

The Reserve Bank is still holding out hope that a tool with debt-to-income (DTI) threshold limits for borrowers could be added to its macro-prudential toolkit.

"The Reserve Bank’s view is that a serviceability restriction, eg, a debt-to-income threshold limit for borrowers, at which banks can only make a certain percentage of new lending would be a useful addition," the Reserve Bank says in a paper released on Wednesday.

The paper, Macroprudential policy framework: Mitigating the likelihood and severity of boom-bust cycles, was authored by Piers Ovenden, an adviser in the Reserve Bank's financial system policy and analysis team. Ovenden notes other macro-prudential instruments may be added to the macro-prudential toolkit over time, and there could be a role for such tools as the financial system and risks evolve.

"The Reserve Bank has suggested that a serviceability restriction, eg a DTI instrument, would be a useful addition to the tools specified in the Memorandum of Understanding. The Reserve Bank published a consultation document on this issue in June 2017. It is intended that this proposal will be revisited as part of the Phase 2 review of the macroprudential framework," the paper says.

"A DTI instrument would be particularly useful when used in combination with LVR [loan-to-value ratio] restrictions. It would give more effective control over banks’ loan origination standards and would improve the resilience of the financial system, where housing market vulnerabilities exist. Combining multiple transactional instruments, e.g. complementing LVR restrictions with a DTI restriction would also reduce efficiency costs."

The Reserve Bank's five year-old macro-prudential toolkit is being reviewed this year as part of the Government's review of the Reserve Bank of New Zealand Act. Whether the Reserve Bank can get the government backing it requires for a DTI ratio tool remains to be seen. Prior to the 2017 election Finance Minister Grant Robertson, then opposition finance spokesman, said Labour didn't support DTI ratios for first home buyers.

In 2016 the Reserve Bank formally requested that a DTI tool be added to its Memorandum of Understanding (MOU) with the Finance Minister on macro-prudential policy. However, in February 2017 then-Finance Minister Steven Joyce kicked the DTI tool issue to the curb until after that year's election by requesting a full cost-benefit analysis and consultation with the public before he would consider whether to amend the MOU.

The Reserve Bank subsequently said the key benefit of a DTI tool would be reducing the costs of a housing and financial crisis. It also estimated restricting the DTI ratio of some mortgage borrowers could prevent about 10,000 borrowers from buying a house, reduce house sales volumes by about 9%, trim house prices and credit growth by up to 5%, and shave 0.1%, or $260 million, off Gross Domestic Product.

In an interview with interest.co.nz last year Reserve Bank Governor Adrian Orr expressed interest in having a DTI ratio tool added to the regulator's macro-prudential toolkit.

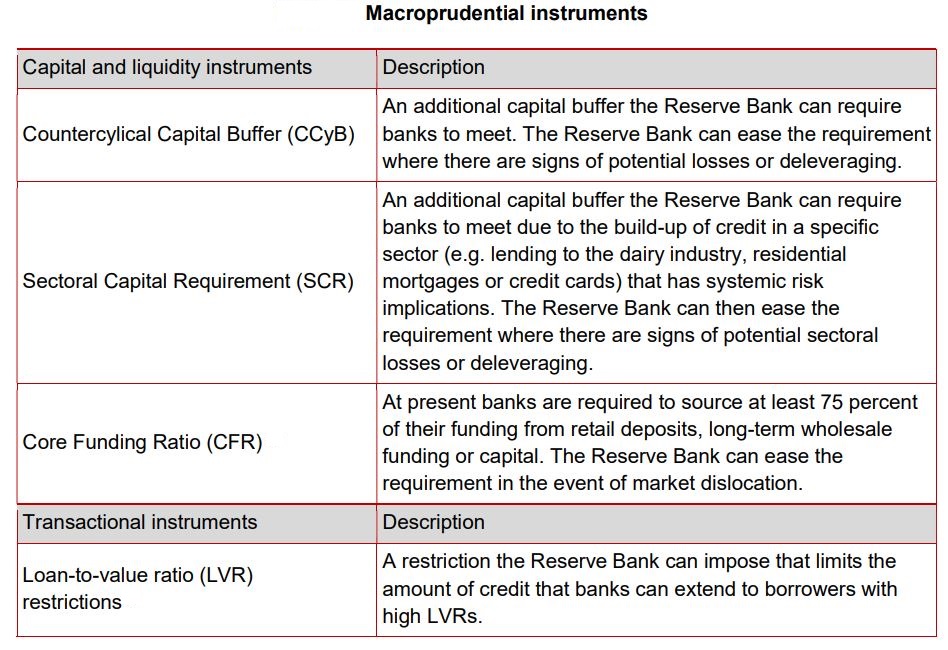

The MOU was signed between then-Reserve Bank Governor Graeme Wheeler and then-Finance Minister Bill English in 2013. The four tools in the macro-prudential toolkit are detailed below.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

36 Comments

Good on them for bringing this to the fore again. An absolute no brainer.

A shame on all politicians of the past for not pushing this (which means including the current crop).

Banks lending money at levels to someone who can barely afford the repayments when the times are good is going to struggle when a disposable income disruption comes along leaving all parties scrambling. The borrower in tears and the lender charging a bigger margin to the rest of their clients to cover their reckless behaviour losses. Again hitting the lower income section of society the hardest.

Grant this is your chance to make a difference and in line with your party's well being mantra.

A LVR is only a tool for keeping the bank safe when they are not considering the DTI of their client.

Should probably be called DTDI, Debt To Disposable Income, ratio and enforced accordingly.

I’ve always maintained that a debt to income ratio should be 2.5 to 3 times income! This goes back to my banking days in the late 1980’s.... This enables house prices to be contained at sensible levels, allows a buffer if interest rates go up and allows cashflow for other types of investment and spending in the local economy. What we now have is lending at unsustainable levels at very low interest rates but less disposable income because of our high cost of living. I would welcome a debt to income ratio but I fear that it would be too high!

Ah . . . yes lets have a nanny socialist state that dictates and controls our lives.

The above argument gives no credit to either competent individuals or banks being able to make their own decisions regarding borrow/lending. Banks aren't reckless - in their own self interest they are simply not going to lend where they perceive that their is risk and it is my understanding that banks already have policies to ensure that the level of lending reflects this - they are currently factoring in risks related to both the borrower (e.g. employment risk) and some down turn in the property market. It is bollocks to generalize that banks are lending to those who can't afford repayments let alone pose a future risk.

Yes, there are about 3,000 insolvencies a year which has been relatively stable over the past 20 years. So, let us control and dictate to the wider rationale population for those who can't manage their own risk and debt.

How many of these insolvencies are due to inability to meet mortgage commitments? I suspect the vast majority of who are failed business owners, those unfortunates who get sucked in by loan sharks, and young (yes those under 25 make a significant number of bankruptcies) who voluntarily do so to clear student loans.

Lets have a DTI to clamp down on start-up businesses - yes, that is really going to help both those with imitative and the wider economy.

I really wonder if a DTI ratio was introduced, how significant it is going to influence current levels of insolvencies.

Too much anti-bank and FHB sentiment in the above argument.

LVRs are designed as an implicit stress test not for use in normal market conditions but when dislocation starts to hit the system.

The whole idea is not to protect the bank bit the public at large by preventing a banking crisis and publicly funded bailouts.

Since black swan events are starting to appear on an increasingly regular basis the LVRs are more important now than they have ever been.

You are relying rather too much on individual's competence when borrowing or investing - most people simply don't understand the risks and intricacies. I work with a dozen highly qualified Scientists with a couple of degrees each, and still only a small fraction have got their heads around personal finance and/or are investing in anything more complicated than term deposits and their own home.

Those of us with a decent understanding of these things are very much in the minority and it's dangerous to assume others will be as careful as you or I might be. I would fully support you if you took this as evidence that we need better financial education in this country, but while that is filtering through more sensible regulations are a net good as far as I'm concerned.

This is true.

As evidenced by my work in finance and lending with many people in their late 50's nearing retirement buying rentals.

When asked what their motivation was, most had no clue, had done no research, didn't know what gross or net yield was and assumed capital gains go on forever.

Pretty disturbing.

Eh, this sounds like you're describing a world in which neither the GFC nor South Canterbury Finance occurred. The reason why the RBNZ is pushing for measures like this is because of the possibility that the taxpayer will be left holding the can again in NZ too.

I worked in insolvencies, No Asset Procedures (NAPs) and Summary Instalment Orders. You can't use these processes to clear student loans.

But I agree with you 100% that the majority - once again, do not need to be penalized in their aspirations by the few.

printer8: In case you have not noticed it, the vast majority of current FHB's have no clue about money, quite possibly a result of their parents having had it too good for too long and who forgot the lessons taught by their parents. If they did not forget they mostly forgot to pass them on. It certainly can't be due to a lack of teaching at school as there never was any.

What we don't know is how many insolvencies are prevented by the BoMaD.

When a bank can offer someone with absolutely no income a credit card facility with a 10K limit it shows, to me anyway, what they are willing to do to earn a buck when flush with liquidity.

Banks do not understand start up businesses, if you have a good story they will provide up to 80% of your collateral and you have virtually no choice but to go with the bank you already have your mortgage with. Not going beyond 80% leaves them with enough margin when it turns to custard.

In case you wonder, all of the above are personal experiences.

But yes it does sound like a socialist nanny state and that is sad enough.

It is also sad to see that despite a more educated society common sense is the victim and an ever larger segment of the population needs protection from, and can't think for, themselves.

That building in Wellington is quite aptly named and those in it are working hard to create such a society.

But in regards to the financial system the resilience is out of it and all that we can do now is trying to limit the damage from the next shock. More prudent lending practices will help.

Don’t think they have a hope. If the RBNZ got a DTI at any reasonable level it would have a big impact on house prices and that can’t be allowed to happen...

The point is they could start it at a level now (e.g. only a small proportion of lending allowed >6x income) and progressively taper it down over time.

It doesn't have to be enacted straight away at an apocalyptic level.

In the near term it would at least act to keep a lid on asset inflation if they cut the OCR further (assuming the cuts get passed through).

Good - we need this. Getting a little tired of these 'look! housing is now affordable based on mortgage repayments! Forget the fact you're borrowing high six figures - look at the repayments! No interest rates won't go up!' articles.

With ya on that one. Everyone around me is borrowing massive amounts for houses as they can easily meet the mortgage payments over 20 years... I understand mortgage payments are lower but the sheer amount of debt is massive and will follow these people for years.

have a relative that did that wont finish paying off his new mortgage until he is in his 70's,

if he had been only allowed to borrow what he could afford he would have brought a cheaper house not a mansion.

Or that 'mansion' might have been priced to reflect fundamentals, like local incomes for example.

I know. A very strange, novel idea.

It is was one of the major contributing factors of reducing risk in UK housing and slowing the Casino effect. Pre crisis mortgages at 6 times household income were common but rarely above. We had 25%!of lending last year beyond 6 times and a further 18% between 5 and 6. In contrast 80% of lending in UK is capped at 4.5 now and 5 is pretty much the limit. That’s in an environment with lower mortgage rates and lower costs of living. The RBNZ are right to want to temper the risks building in our banking system.

I am in favour of exploring this further but I doubt the government would do it.

Obviously this is the best tool for sustainability and avoiding bubble & bust cycles.

Problem is its hard to implement at the top of the market.

2 options really.

1. put it in the toolbox ready to implement after a market crash

2. implement now at a high DTI (aligned to what actual banks are doing at the top end) and reduce marginally each year till you hit your target DTI

I also think the DTI should get lower through the age brackets, while you could lend say 6x for people in their 20s who have 40 years in the workforce but someone in their 50s (even though likely on a higher wage) only has 10 - 20 years left in the wrokforce, you might only want to lend 3x

No issue with the 2nd option - why is that so hard to implement? Even at the top of the cycle?

DTI a long overdue instrument to check reckless borrowing by those who wanted to ride the property bandwagon. Aided in no small way by equally reckless lending by banks.

But, given the current state of the property market & for the immediately foreseeable future, the stressed-out borrowers will gradually appear.

As they say, when the tide goes out, it will expose those swimming naked !!!

"...could prevent about 10,000 borrowers from buying a house, reduce house sales volumes by about 9%, trim house prices and credit growth by up to 5%, and shave 0.1%, or $260 million, off Gross Domestic Product."

What about potential impact on rents?

Any competent Year 12 economics student would eviscerate debt to income regulations as an effective tool.

What would they say, out of curiosity?

That intervention in free markets rarely works and that most who advocate it have a vested interest, but you already knew this right.

Would they argue wholesale against all banking regulations and licencing, or would they be nuanced enough to realise that some level of regulation is required?

You do realise that banks currently evaluate every mortgage application on it's debt servicing ability, deposit etc and that they are required to comply with responsible lending standards? But no, we need to lock first home buyers out and let landlords snap them up.

It would be interesting to see whether rental income counts as income in the DTI calculation - if not this would be a natural disincentive for landlords. Even if it is counted, DTI will still be a large roadblock for those wanting to leverage equity and build up a portfolio of rental properties, especially if it helps to moderate house prices.

If you're genuinely concerned about FHBs, there's always the possibility of different DTIs for different groups, with more relaxed settings for FHBs, perhaps tighter for landlords. This kind of approach is already used with LVRs and has had a very positive outcome on proportion of sales going to FHBs, at the expense of landlords.

How consistently have they been doing this, do you know? More or less the same as in Australia, for example?

Do you know anyone who has lost their house? Yes it does happen, and it's really unfortunate, but the outcome is far more likely to be positive with growing equity over time. Business's fail, people fail - that's capitalism. It's not perfect but it's the best we have. Every housing bear see's a crash around the corner, and they rarely eventuate.

We're talking about whether the lending practices of banks here resemble the practices of their parent business units. Not exactly too radical a possibility.

Ok, I'm talking about debt to income limits as a macro-prudential tool, like the article.

Ok, I was replying to your comment that was exactly as I described it:

You do realise that banks currently evaluate every mortgage application on it's debt servicing ability, deposit etc and that they are required to comply with responsible lending standards?

Hope that helps.

But my, it's heartwarming to see so much sudden and obviously very, very sincere concern for FHBs. What a marvelous turnaround.

I would imagine they would provide a textbook answer, concluded by the term "ceteris paribus", yes.

I think what some people are missing here, like everybody, is that some of the big wigs have spent so much on their accountant they have "zero income" operate at a loss, and have no assets as all they own is not theirs as it is held in trusts.

Therefore debt to income no good, all bad...

Income = zero

Loans recalled.......

Game over....

Extra Ball.... will not be good for politicians and their donors, therefore will not see daylight...

BAU: Business as usual...

Continue play... (last ball)

President of Property

While I am usually supportive of what the RBNZ is attempting to do, this one is one which I believe is problematical. While intuitively very attractive and having a good basis in theory, in practice it would be impossible to fairly and equitably implement. Furthermore, it has shadows of extreme moral hazard. Not only does the RBNZ have a view of LVR or loss given default, it is now saying to banks, each of whom have their own risk appetite, what the acceptable probability of default is.

So. Having a standardised rate will mean that high risk income, say for example acting income will be lumped into the same bucket as say a doctor or a nurse gets. Apart from health, the only difference in PD is based on the sector you are in.... or would each sector have a differing PD or debt to income ratio.

Furthermore, what is defined as income.... salaries, wages, allowances, profit from sales, sale of parts of land, pension, dividends, etc etc etc. wisdom of Solomon required for a standard regime.

And then, what is debt.... student debt, card debt, promises to kids, joint marital assets owed to each other, promises, contingencies, new debt, rolled over debt, foreign debt. Again, bigger brains than mine would have to solve it.

Then disviossions about debt servicing ratio. Only the debt with the current institution, others, the ird, etc etc etc

Theoretically possible, practically unworkable.

And then. SoRBNZ introduces the ratio, and the bank applies to, and the LVR and still there is a default and loss. Is the loss due to the bank following the rbnz rules. So is the loss on the government.

NOT A GOOD IDEA. But, a good idea for the banks to report on their assessment models to the rbnz, and the rbnz require the banks or directly impose an internal Capital Adequacy Add on if the assessment model is not near the norm for LGD and PD. Ie give banks that are conservative capital relief, and those that are liberal, capital add ons. Archive the social objective, without imposing another restriction.

ICAAP is there to add or reduce capital charges for ideosynchratic risk. Use it.

To late to implement. If they had kept the 3X that they had when I first started looking at houses 30 years ago I would have never got into a home. To rent or to buy is a lifestyle choice.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.