BNZ's economists warn that over enthusiastic investors could push house prices to unsustainable levels.

The bank's head of research Stephen Toplis is warning that falling interest rates have had a surprisingly strong effect on house prices.

"The apparent effect of falling interest rates on the housing market has certainly caught us by surprise," he says.

"We had thought that, by now, house price appreciation would have been a thing of the past.

"It clearly isn't."

Toplis says that although other factors such as the supply of new housing and unemployment levels also influence the housing market, it's clearly interest rates that are the main driver of the current surge in prices.

This raises the possibility of a widening wealth gap, where "the owners of assets [such as houses] fare disproportionately better than non-asset holding folk."

There's a danger, if current trends continue, that house prices could become unsustainable.

"Whatever the justification for current (and future prices) we caution there will become a point in time when over-zealous investors push prices to simply non-sustainable levels," says Toplis.

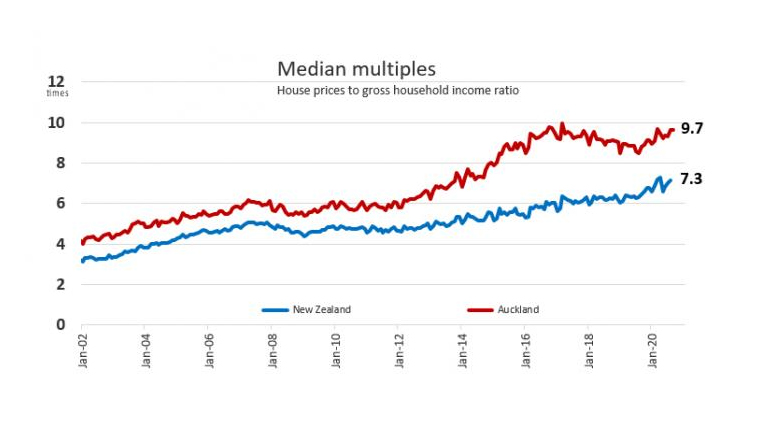

"If house price-to-income and rent ratios blow out, then owning a house will simply become an untenable option for a greater proportion of the population."

September sales data from the Real Estate Institute of New Zealand showed the strongest September sales volumes in 14 years, and a record high national median price of $685,000.

The comment stream on this story is now closed.

92 Comments

"The apparent effect of falling interest rates on the housing market has certainly caught us by surprise,"

...and he calls himself "Head of Research"!

Beat me to the punch. Lowering interest rates is the single biggest factor in our house price growth as he states. If he couldn’t see this surge coming then I’ll be damned.

Would it happen if supply and demand were in balance? i.e. there was no housing shortage.

It will be interesting to see if the border stays closed for another couple of years while building completions are still high, whether the pent up demand will be satisfied and the heat go out of the market.

As long as credit is easy and cheap the demand won't easily dissipate

The RBA and RBNZ are largely doing the same thing, but house prices on either side of the ditch seem to be diverging. Any thoughts as to why?

Compared to GDP, NZ is spending way more on wage subsidies and other kick-can-down-road spending. eg. this from March:

https://theconversation.com/new-zealand-outstrips-australia-uk-and-us-w…

New Zealand outstrips Australia, UK and US with $12 billion coronavirus package for business and people in isolation

We will pay later.

Good article re NZ vs Oz https://www.newsroom.co.nz/pro/as-safe-as-houses

In short tax distortion is massive vs foreign equities in NZ

That's especially true when new zealand already has a wealth tax on foreign equities.

We are not supposed to talk about the 1.65% wealth tax on foreign equities

One reason, I think, is they are a larger and more diversified economy.

Maybe too it's psychological, perhaps people here feel a bit more bullish about the economy and life in general right now.

I wonder if there’s a psychological effect from the different unemployment rates? NZ 4%, Australia 6.9%, even though we know NZ’s number is hokum.

Australia builds a lot more houses than we do.

Large housing estates built fast. Building materials are cheaper.

It helps keeps house prices going up as rapidly when you can buy a new one. Obviously not in all areas but South East Queensland just grows and grows with more houses built. $650k gets you something nice. $1.2k really nice

The exodus from this basket case will be something to behold over the coming years.

The weather is generally better and the people much friendlier too. Feels more like New Zealand was twenty years ago.

I feel bad for my parents not being around for their grandkids growing up, but they will have a much better life than in this dysfunctional s***hole.

Yes if I was younger without children I would bail too.

I have lived in US, then UK and finally Australia before returning here in 2006. It has gone down hill but perhaps I was not aware of certain issues in NZ when I was younger.

Then again if there is a wealth tax I will bail again.

In my experience and opinion, NZ is great for well off people and pretty average for middle income earners. Aus is generally better for the middle income earners, apart from if you live in Sudney.

I'm disappointed in this comment. I'll be retiring in a few years and I really need you guys to hang around and pay tax to the NZ retirement village.

So, yeah, a bit less selfish me-me-me stuff please.

Thanks

BL - Well just go then !

If you had listened to some of the commenters on this website predicting the rise in values rather than obsessing over the great debt rest you wouldn’t be in such a bad position. No one to blame but yourself.

We have solved that with an inflow from other countries. Plenty of people want to come to NZ.

So... does this mean the RBNZ isn’t quite the villain it’s being made out to be?

Maybe supply-side measures such as house building rates, land use restrictions, material costs etc and demand-side such as tax (no capital gains/stamp duty), immigration (nz’s per capita rate almost double Australia’s), are much more important factors?

What’s the alternative? Raising interest rates, appreciating the dollar and hammering our export industries?

I think most of those downsides are a product of our small economy, and not solvable.

RBNZ are the villains.

Should have done nothing or very little. Let the market clean out the debt fueled.

Let house prices fall. Would have been a good thing for NZ to see a 20 to 30% fall in house prices.

Should have kept LVR rules. If making loans with no equity was a good idea why did most countries bring in LVR type rules.

The dollar going up and down is exaggerated in terms of our exports. They still buy the stuff. Also its the 10th most traded currency in the world. Its movements are driven by cocaine fueled traders when we are all asleep as much as what is happening locally.

I agree they should of keep the LVR’s, probably should of brought in the DTI limits back in Key’s day.

Personally I think it’s 30 years of wrong turns that have got us to this point. The housing market is now too big to fail. The collateral damage would be huge. It’s difficult to see any pleasant way out of this.

New Zealand should have debt to income restrictions.

Instead they removed LVRs and boasted about how they want house price inflation so wealth can "trickle down"

They are evil.

Less reliance on and encouragement of property investment for wealth generation in

Australia due to capital gains tax on investment property, stamp duty (tax paid by buyer), less supply constraints and much stronger employer funded superannuation system. Also RBNZ has dropped OCR by a greater degree in response to COVID than RBA.

This is true if supply is not allowed to equal demand. But that was not the question asked.

If supply is allowed to meet demand, then the fuel that is the house is never allowed to ignite into a supply shortage.

Without ignition, then all those accelerants, like lower interest rates, and immigration etc. have very little effect.

Texas is a classic example of low-interest rates, high immigration, but because they allow supply to equal demand in developer real-time, then houses are approx. 3 to 4 times median income, half the price of what they are in NZ.

Dallas Fort Worth is nice. I use to live there. Arlington is the fastest growing city in the US and new houses are built very fast keeping prices reasonable. You can get a mansion for less than what you pay for rubbish damp and cold houses in Auckland.

I lived in Austin for three years working for a property syndication company.

People in NZ don't understand what a rip off NZ is compared to a properly run Govt.

Nice.

Sixth street Austin. Wahoo

The best southwestern music scene, and Margarita slushes, especially watching the bats leaving the Congress Avenue bridge.

Go Long Horns!

I enrolled to attend UT Austin but came back to NZ and went to uni here.

Far too many distractions there.....

Reserve Bank, bank economists etc surprised that house prices have defied earlier predictions of a decline? After all the tinkering with market forces via mortgage deferrals, flooding the system with cheap money ,removal of LVR's, slashing of mortgage interest rates .... and consequently deincentivising term deposit holders with peanuts on their interest??? I may as well be surprised that a spark to tinder can cause combustible to flare up!!!!

If they fired all the economists at the RBNZ and Banks the same outcomes would be achieved and a lot of money saved.

The number one aim of central bankers around the world since 1944 has been to get all people and all nations into as much debt as possible. It looks set to continue according to this explainer video. https://youtu.be/enmHW4gCkAY. There is also the phasing out of Libor over to sofr which could have a very negative effect on the trillions of dollars in the derivatives market and ultimately the banking system. Perhaps we should all be reading up on Triffins Paradox! https://youtu.be/enmHW4gCkAY.

NZ is doing it’s very best following the rest of the world in getting it’s citizens to take on more and more debt hence the constant headlines on house prices. This is not only an NZ issue, it’s global. We are not different. We are so reliant on ever expanding debt that it just isn’t funny anymore. There may be trouble ahead.... but music and dancing will only lead us further into the debt dead end from which there is no return.

The same bank predicted 10~ 15% drop of house price just 5 months ago.

Most of the banks have pretty poor forecasting records, generally.

"If house price-to-income and rent ratios blow out, then owning a house will simply become an untenable option for a greater proportion of the population."

Meanwhile, our leaders continue to actively evade the subject and can barely acknowledge the issue when pressed (very lightly)...

"become" should be "is", just that the proportion will grow.

I've just got approval to go to auction on my first house (4th attempt at auction) they are now applying their own valuation and won't lend beyond that despite what your deposit or income might be. So that's good I guess from a control pov. However cashed up investors are paying huge money for houses, 2 of the previous 3 we've lost out on have sprung up for rent as soon as they are settled.

Interesting that you are still seeing investor enthusiasm here (for houses at least). It seems to be drying up in Oz.

What do they mean 'if'?

Do they really think a national average of 7.3 and an Auckland average of 9.2 is not already a blow out?

I think people showed how sick of it they are, by Nationals low vote. Also by Greens numbers, who see a wealth tax as some type of solution, even though it isn't targeting house prices. Basically if you want a new house in the Wellington region,eg 160 sqm huse 600sqm section, you are paying the best part of a million. From memory those same types of houses in the same area were in the 700's only a few years a go. Yes Labour have failed to do Kiwibuild, but National also had no answers, and denied there was a housing crisis for 9 years. They only called it a housing crisis after they got voted out, and before they go elected 12 years ago.

This is a property bubble that is being inflated intentionally, and there is so much FOMO. Will it pop, or will it just get worse and worse? Those savers (some will be older people) moving their money out of the bank into a investment house could end up losing some of their wealth if it does crash.

I have calculated that the total income from my relatively highly paid IT consultancy activities in the last 10 years has been greatly outstripped by the relentless inflating of my assets.

An economy that delivers such results just does not make any sense, and it shows dangerous structural unbalances.

Remember that central banks are still 'searching for inflation' though because they can't find any. So we just need to keep dropping interest rates and print some more money until we find it.

Yep, well that's their seemingly futile mandate.

But of course house prices aren't included in the calculation...

LOL.

Beautiful pic, by the way. I'd be happy to live under those trees on the right.

Its stolen from here https://www.islandpacket.com/news/business/real-estate-news/article2117…

Could be a copyright infringement!

Please let's this to continue, into first quarter 2021, after the initial FLP, RBNZ is certain to put OCR into negative and in absence of the Govt. financial restraining & prudent measures, The next QEs/LSAP/printing money is on the card by mid 2021 - The unemployment factor has been incorporated into their calculations. It is by design to hide the land & housing inflation from CPI report, the only way to keep the flame up on FIRE economy is to guarantee employment, the subsidy will be there, every tools avail will ensure this... Buy that RE!

Its certain is it? Did your crystal ball tell you so?

Well, there goes any career path Stephen Toplis though he had!

Unless.........

He knows for sure what's coming.

We have been blighted for several decades by Group Think. Everyone agrees with everyone else as long as it's the same idea. That way, no one can be wrong, just surprised, and career prospects remain intact.

Daring to question the status quo; something that led to massive development in our societies in the past has been replaced with a Fear of Being Wrong.

So. Either Stephen is looking for a new job or.....he's been told to get the First Class passengers into the lifeboats.

Yip but why are we raising this now and not for the last 10-15 years?

“ There's a danger, if current trends continue, that house prices could become unsustainable.”

As NZ history shows, if house prices look unsustainable or wobbly then just lower interest rates further. Works like a charm. What could go wrong?

and take away the LVR's for the banks so they can lend more , that helps as well

Well duh!

Such a revelation...

We are either governed by fools or complicit parties in the whole housing ponzi.

I favour the latter explanation.

How about 'complicit fools'?

The wealth gap will be increased a lot more when the property market declines than when it’s continuing to go up now and people are still buying very expensively:

“We’ll be buying up big': Sir Bob Jones sits on a stash of cash, waiting”

https://i.stuff.co.nz/business/property/123101150/well-be-buying-up-big…

He's a wise old fella WRT property. So he thinks a crash next year? He knows much more than me, but I have said for quite a while 2021 or 2022.

I worry for those buying now. Since I bought last November our value has likely gone up 10% and may go up another 5-10% before the crash, so that gives us a bit of a buffer.

he only buys commercial, so with the changing way people want to work and companies not needing the footprint sooner or later there will be surplus buildings. housing is different lots of other factors

He concentrates his activities in Wellington CBD doesn't he?

Wonder how much he has been affected by the earthquake strengthening compliance requirements

Every time there is a bit of a property boom I hear this. Gonna swoop in and pick up bargains! Never happens.

Tell me if house prices dropped 70 percent does cash still have value if you stockpiled it?

Housing backs the currency created by banks. So if housing collapses how does the cash maintain value?

This is the argument that we may be seeing the end of the current cycle of fiat currency. Central banks now are being forced to have a race to the bottom and devalue their currencies so that the mountain of debt can be serviced. But given that it appears to just be flowing into more mortgage debt here in NZ, I just don't see how it doesn't end up with some type of serious crash.

It's the currency that crashes. Debt will be inflated way. This 2% CPI targeting will be forgotten as soon as it's convenient. We will be told it's for our own good.

move to affordable regions?

Many of them aren't so affordable any more. More limited career opportunities too.

Yeah Queensland.

Pot calling kettle black

Stop

Lending

To

Speculators

Some of these new and over enthusiastic investors are going to take a bath in the next few years. And this is an old hand talking.

We've all been saying that for a long time now.

It never happens. Mortgage holders and property speculators are a protected class and the system is rigged in a way that would make the soviets proud.

They will debase the dollar in your pocket to nothing before they let house prices drop an inch.

So a guy who works for a bank that lends cheap money to the housing market says "Sheesh those house prices are high". He needs to have a look in the mirror when he gets home.

Central banks lowering OCR and flooding economy with cheap credit. I can't help comparing them to a debt-laden consumer getting another credit card so that they can use extra credit to pay interest on the existing maxed out credit card.

You... Don't... Say...

No worries though. House prices can never and will never fall. Never ever. Mary Poppins and The Fat Controller will see to it that the unsustainable is sustained.

If we can get some good unemployment numbers in March when Mortgage holidays end Orr, Robertson and Cindy wont be able to help you make principal repayments on your loan even with zero interest.

I am still hopeful of some good mortgagee auctions in April onwards.

Don't be silly. That will never be allowed to happen. Extend and pretend. Forever. The fat controller hasn't even got around to negative rates and funding for landlords programme yet.

The system is rigged. It's not going to change until it collapses under the weight of its own absurdities and takes out the currency.

I have seen it before and it can happen again.

Cindy, Robberson and Orr wont be able to save private sector jobs.

They all cant work for the Govt.

Negative interest rates mean nothing if you cant pay the principal.

I agree it wont collapse but i can see 20% to even 30%. It happened in 2008 when credit dried up and banks told people to offload property.

Banks have shareholders and they will want a return

The bankers and politicians have wised up from 2008. It should have already happened.

Instead they handed out mountains of tax payer cash, printed money, tore up the rules on non performing loans, removed LVRs, introduced negative rates, and set up funding for landlords scheme. They are going to underwrite developers that can't sell cubicles for bubble prices, they have grants, you can withdraw your pension to spend on houses, rent to buy schemes, subsidies. No capital gains tax, no wealth tax, no nothing under the leadership of the empathetic invertebrate who does not want prices to fall.

It's completely and totally bonkers. But it's clear now that house prices are the only thing that matters and this country is beyond redemption.

Nothing will happen in April except that every social metric we use to measure the health of our society will be worse.

We are 100% on the same page and Cindy will stand up there with a big teeth smile and say how they have done so well.

Proposed policies will fail again and Cindy will say we will have a reset meaning we could not actually do it and we wont talk about it again after today!

Can't wait until my tax dollars are being pissed away on shared ownership and developer underwriting along with the accomodation supplement.

Every comment you make is an oxymoron. Good unemployment numbers etc.

Does it offend you for someone to have an alternative view to Cindy, Robberson and Orr?

One has to invert thinking. It has served me well taking the contrarian view in lots of aspects of life.

I want the housing market to tank 20 to 30% and stay that way. (not so I can buy). It will be better for the country and next generation.

With current QE Money printing the only way this will happen if we get great unemployment numbers and forced sales.

Alternatively we need Cindy to waive her socialist wand and introduce CGT on houses, farms, shares and businesses now she has some real power.

Hear hear the property market has to come down.. it is the only intelligent strategic move... The debt that NZrs are forced to take on makes us defenceless as the world strategic power shifts.

RBNZ Funding for Lending = "Hey RBNZ, we need to sell a mortgage but we don't have the 'goods', can the taxpayer stump up with the cash?"

The best and time-saving way of styling this year for Halloween is to go for the

Halloween Costumes with Jacket

. From giving you a fancy celebrity appearance to complimenting your spooky mood, this edgy costume choice will satisfy you by all means.

A stunning new insight from the Bank of NZ.

How do they do it?

"...could push house prices to unsustainable levels."

... Even before this NZ was already one of the most unaffordable housing markets on Earth. It could be easily argued that it was already at unsustainable levels. Ballooning household debt ratios and draining retirement accounts should be setting off alarm bells.

As term deposits are now too low, there appears to be a big group of people with savings moved to 'on call' that are now looking at buying a house or moving their money out of the bank. People don't just have their money on call for no reason as inflation will erode it's value. . But house prices can go down, or stay stagnant for a long period of time. A new average house today in the wellington region appears to be close to 1 million now. Are house prices going to be 2million by 2030?, or 4 million by 2040, which is what some people expect, where some people seem to think house prices double every 10 years.

Yes i am one of them.

Am considering be a ghost owner in Auckland on a couple of houses. Buy and lock them up alarmed and send a gardener once a month. No interest in renting them.

I don't believe they will double every 10 years dribble even if it has happened before.

Banks give zero return for maximum risk of an OBR event.

Wow. What a weird world we live in. And the DFA site mentioned Oz has 1.1m empty homes.

Central banks making moves to deal with the public directly instead of via retail banks, and people treating houses as banks.

What do you think of an empty room tax? I know that over in the Netherlands and some other European countries they have these. You are taxed on the number of empty rooms you have in your house, so it encourages you to have boarders or flat mates.

Surely that would work to discourage ghost owners and help lower prices?

Taxes create weird incentives. The tax on windows resulted in windowless houses.

I wonder what an empty room tax would incentivise - internal wall removal?

If the reserve bank has been caught by surprise... then they have been living under a rock for the past 20 years. Incompetent.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.