By Greg Ninness

The benefit of falling interest rates on mortgage payments is now being more than offset by rapidly rising house prices, as prices increase at a greater pace than interest rates are falling, according to interest.co.nz's latest Home Loan Affordability Report.

This raises serious questions about the economic benefits of continuing to cut interest rates to stimulate the economy.

Mortgage interest rates have been in more or less steady decline since 2008 but have fallen particularly steeply this year, with the average of the two year fixed rates charged by the major banks declining from 3.30% in April to 2.58% in November, as the Reserve Bank moved to slash rates to stave off a severe, COVID-induced recession.

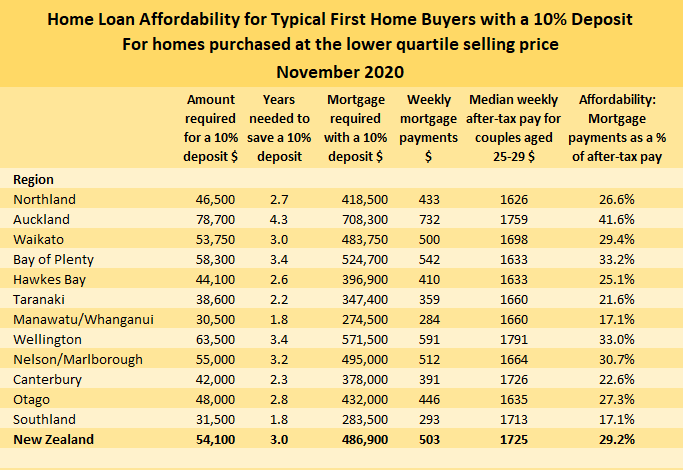

According to the latest Real Estate Institute of New Zealand (REINZ) figures, the national lower quartile price declined from its previous peak of $480,000 in March this year to $446,000 in May. Combined with the slow decline in interest evident at the time, this benefited first home buyers both in terms of the amount they needed to save for a deposit and their mortgage payments.

But that all came to an end in May when the average two year fixed mortgage rate dropped from 3.30% in April to 2.88% in May, causing lower quartile prices to immediately start spiralling upwards, rising from $446,000 in May to $452,000 in June, then to $475,000 in July.

By November the REINZ's lower quartile selling price had hit $541,000, meaning it had increased by $95,000 since May, a 21% increase in six months.

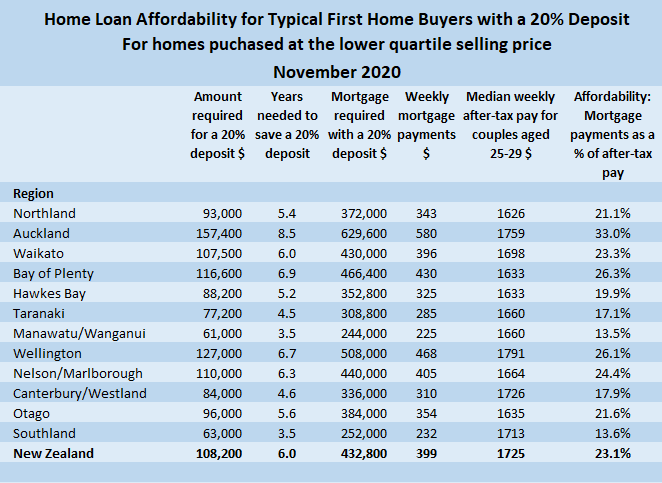

That pushed the amount needed for a 10% deposit on a lower quartile-priced home from $44,600 in May to $54,100 in November, an increase of $9500 in six months, while the amount needed for a 20% deposit increased by $19,000, from $89,200 to $108,200.

Of course it also sharply increased the amount first home buyers would need to borrow to get into their own home.

With a 10% deposit, the size of the mortgage needed to buy a lower quartile-priced home increased from $401,400 in May to $486,900 in November, while for those fortunate enough to have a 20% deposit, the mortgage needed would have increased from $356,800 in May to $432,800 in November.

The size of those mortgage increases means they have more than offset any benefits from lower interest rates on mortgage payments.

If first home buyers had purchased a lower quartile-priced home in May with a 10% deposit they would have needed to set aside around $446 a week for the mortgage payments. By November that had increased to around $503 a week, leaving them worse off by almost $60 a week.

The rate at which house prices have increased over the last six months has not only erased the benefits of lower interest rates. It has also eaten up the increases in wages over that time.

According to the Home Loan Affordability Report, the estimated combined, median after-tax pay of couples aged 25-29, who both work full time, increased from $1708 a week in May to $1725 in November.

But over the same period, the amount they would need to set aside for the mortgage payments to buy a lower quartile-priced home would have increased from 26% of their take home pay to 29% (with a 10% deposit).

These figures suggest the cuts to interest rates that have occurred over the last six months have led directly to higher housing prices, which have more than offset the impact of the lower rates on mortgage payments and any increase in wages over the same period.

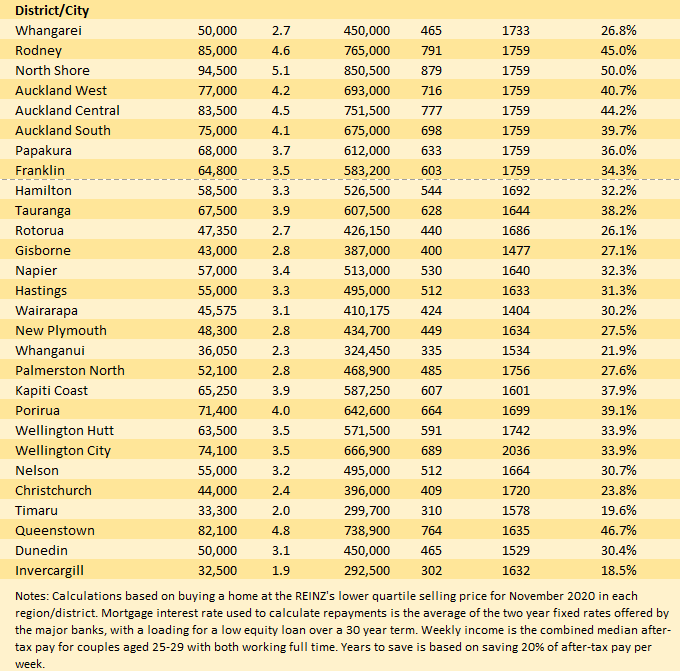

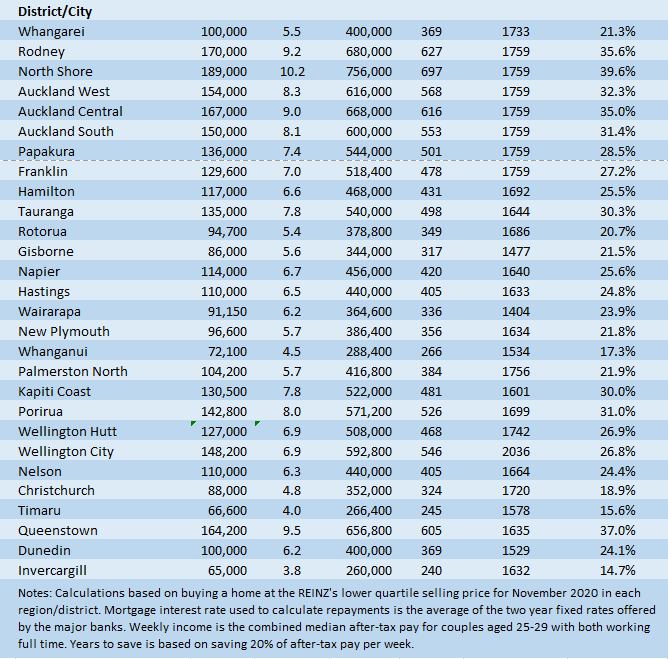

The tables below show the main measures of affordability for typical first home buyers with both 10% and 20% deposits in all main urban areas of the country.

The comment stream on this story is now closed.

196 Comments

Are we in asset bubble territory?

Nope, Jacinda and Grant have everyone's back. Nothing but 'moderate increases' to come! It's only fair - people expect that!

It's only fair - people expect that!. Indeed!!!!

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

Don't worry about it, the banks will be bailed out even though the government has no money for the poor or hungry.

It'll be their own depositors first. That would be a laugh.

According, to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

John Key is asking for this to be delayed so obviously he thinks National wouldn't require this and is hoping they get voted back in.

But lets face we have hyper inflation in housing so this thing could blow off in six months and a house in Otara might be worth $2m.

Someone has to be able to pay that 2 million. That same house could be worth 500k if none was willing to pay more than 500k for it.

Without the leverage of a bank loan?

Many are unable to see past rent as a source of retirement cash and tax free gains. The pull of tax free capital gain is simply too great. The only winner is the banks shareholders leveraging vapor cash. The speculator takes all the risk, and the tenant is proposing it up with govt support.

There is nothing unusual about the current stance of the property market, in the context of the last 70 years of NZ property markets.

It has happened like this before, but ever so slightly different (to do with the current account), and will continue to happen. To solve it, the Govt could just do one very large helicopter drop to push nominal gdp upwards, and that would be the end of that.

Many people will now be regretting that they didn’t purchase a property during 2017/2018 when the housing market was flat - with scarcely any movement in prices and relatively low sales volumes.......

Undoubtedly, timing counts for much.

TTP

Excellent hindsight there about timing.

Now tell us, will many people regret not buying a property in January 2021 when prices were rocketing? Or were you suggesting that its better to wait until the next period of stagnating prices?

Not hindsight at all, Beanie!

I strenuously encouraged people to buy during 2018/2019 - arguing that the flat market could not be expected to last long and that there would be no “crash”.

Further, in early 2020, when COVID-19 surfaced, I stated here numerous times that the housing market would remain resilient - and that, post-lockdown, people would be surprised at the magnitude and speed of the recovery.

Few here, however, are prepared to acknowledge my foresight - despite them being well aware of the accuracy of my predictions.

TTP

Imagine a convicted price fixer being an expert on prices.

Hi Brock Landers,

Who is the "convicted price fixer" that you refer to, above?

Please provide some clear details. If you can't do that we shall assume that you're no different from certain other people here - i.e. full of bullshit.

TTP

You didn't predict anything- you sat on the fence

Beanie

The reality is that 18 months ago there were those - yes, including me - who were saying that there were indications that the Auckland market was bottoming out and FHB should be actively seeking properties.

There were also those - actually a majority - on this site rubbishing posters such as TTP, Yvil and myself for suggesting such things and they were claiming bubble burst. Amongst them was Retired Poppy who strongly advocated FHB hold off and put there savings in TD - how ill advised could that prove to be.

This was all before Covid, but the reality was that in the six months prior to Covid the market did take off. Retired Poppy has since disappeared from this site but there are others still around singing from the same song sheet.

For those that held off - that was their decision so they live with it and don’t have grounds to gripe.

Yes, the dgm could have been right, but they weren’t and there is good reason for that. Those calling bubble burst - and continue to do so - are invariably one line slagging-off comments void of any rationale and invariably rubbishing recognised economists such as bank economists and others such as Tony Alexander. Perhaps if they gave more thought, justified at least to themselves, and took note of those such as bank economists, they wouldn’t have lost out as they did.

TTP may have been fortunate in being right in this instance, but his comment is not about hindsight but rather both considered rationale and experience. It’s about time those who like to slag-off put a bit of thought into things rather than wishful thinking.

I find it interesting that those who make outlandish comments get lots of up-ticks; well their predictions of 50% Covid bubble burst may have been popular but that is worthless.

I have posted my view as to the future of the market and it’s not continuing inflation as currently - so I’m not a spruiker as has been claimed.

The thing is, P8, you're talking as though your predictions were the result of greater insight and intelligence, when really it was just luck. No one in 2019 could have predicted covid, or the resulting govt intervention. It's all very well claiming to be right in hindsight, but its not because you somehow foresaw all that would happen in 2020.

To be fair to P8, the market had already turned up prior to covid. From memory he then said he would sit on the sidelines a few months to see how the pandemic planned out and what the government response would be. After the lockdown P8 correctly called rising house prices, but recently posted that he sees a prolonged period of flattish prices coming up. You may not always agree with P8 but you would be wise to at least consider for yourself his reasoning, as well as weighing up the opposing arguments which also have merit.

That's fair - but it also in part proves my point. It turns out that sitting on the sidelines for a few months to see what would play out would have been a terrible idea. People who bought in April or May would be very pleased that they didn't follow that advice.

P8's correct predictions were precisely because of greater insight, it's obvious to see. Anyone with half a brain would think, "I should listen to this guy" but not the posters on Interest, nope, not here to learn, only to argue even if it's against the blatantly obvious, never open your mind up, under no circumstance, just dig in and entrench into your position, no matter if it's detrimental to yourself, you'd rather try to be right at all cost rather than be open minded and learn something that's beneficial to you.

Yvil

I do not claim to get it right all the time. However one can improve ones chances by reading those who are recognised and considering the variety of opinions and their rationale and coming to one’s own (informed) conclusions.

Sadly I note a number of posters who make unsubstantiated claims or simply read the report headline (e.g. housing inflation outlook) without reading the rationale on which it is based. Yes, even RBNZ and bank economists don’t get it right all the time - and they would not claim to be making exact predictions - but their rationale is well worth noting.

Unfortunately there are many posters making unsubstantiated posts that simply try to appeal to the popular narrative. An example of this is Foreign Buyer who simply posted that all landlords are parasites . . . and got 60+ likes.

Maybe some really need to read Interest.co tag line - “Helping you make financial decisions”. That is sound informed decisions.

That's basically my point, P8. The RBNZ and every major bank economist were predicting major falls. They gave excellent rationales for this. They turned out to be wrong. You turned out to be right. One explanation for this is that you are of superior insight and intelligence to all of those economists. Another explanation is that the situation was complex and unpredictable, and changing quickly.

Yvil, anyone who decides that they should blindly follow the predictions of anyone - especially an anonymous commenter on a forum- is an idiot, even if that commenter has made predictions that turn out to be right.

You know they are the same person, right?

al123

Providing a rationale is a sign of intelligence and not simply luck.

Pity your comments and other posters can’t recognise it. Maybe then they would have greater success in calling things.

Cheers

al123

I need to clarify that claim of intelligence.

It was hammered home to our 5th form history class - when asked, to simply say one agrees or disagrees can be stated by a five year old but to justify that is a sign of intelligence.

Too many posts on this site fall into the category of the former.

Cheers

Sure, but there were a number of experts who predicted the market would fall, and they had excellent reasons for thinking it would. They just turned out to be wrong.

Care to tell what all those bank economist stated? around Q1 2020? including RBNZ & treasury, including even T/Alexander.. in one of his stuff.co.nz article.. mentioning about .. the rise, rise and rise.. 'unless/IF another lockdown to occur', why the darling RE economist even put such second condition? when on other article he clearly mentioned that RBNZ & govt won't let it happen. People hold off buying for listening to them in the first place, now when the price is already out of their reach, suddenly the U turn from all your favorites economist.. but not the price isn't it? Peoples followed them, and they got it wrong. Now quick changes of tune? should people still followed them? and somehow is sure that they don't get it wrong again this time? Like you've said everyone in NZ knew that the housing price inflation is not part of CPI, so the best to happen next for NZ is clearly negative OCR, I'm into agreement to stimulate the economy, more QEs for carbon neutral & Insurance bail out/disaster zone and FLPs into housing managed specifically by credit union & building society. NZ is still far away from house price ceiling, still by the wall level right now.

Indeed, gotta laugh at the folk coming out of high school and university now while we all toast our own foresight to be born earlier. Heaven forbid we address our policy-driven wealth redistribution to asset owners.

Rick

Re: Those without the “foresight to be born earlier”

What a lame pathetic comment.

Born at the wrong time?

Maybe my grandfather. Part of the 23rdReinforcements in WW1; served in the trenches, saw action at Passchendaele, lost mates, suffered shell shock in the winter. Shipped back home and lost his fiancée in the Spanish Flu pandemic. Struggled during the Great Depression on a work scheme. Lost a son in WW2.

How about that cab driver of yours? A New Zealander now, but born in Cambodia in the early 1970s. Lost most of his family under Pol Phot but escaped under fear of being shot or tortured to death. Struggled in NZ due to language difficulties, teasing at school, and inability to get a good trade and since worked his butt off at two jobs to support his family.

What about that kid born in Otara. Brown, dysfunctional family living in a garage, no support to do well due to family and peer pressures.

Well I think those young folk now coming out of high school and university have it a hell of a lot better and much to be thankful for.

Yes, for young it is tough being a FHB. That is the reality of what they are now currently facing but it is not something that is not achievable - unless they have that lame pathetic self-entitled attitude. There are many who have been and are currently a lot worse off - they are likely not homeless and living in a car nor working at two jobs to keep the family feed.

Yes, something needs to be done about housing affordability but postulating lame pathetic rationale as born at the wrong time achieves absolutely nothing other than excuse finding.

Yes, you have already got lots of up-ticks but for heavens sake don’t ever think that is a measure of the validity of one’s posting.

So why is home ownership at the lowest levels in 70 years? Nothing to do with people being born too late?

Nzdan

Absolutely nothing to do with being born at the wrong time.

I suggest that you go think why there is a problem and what could or needs to be done. The only starting point that has any rationale for solving the problem.

You are wrong there. Luck and timing, including when (and where, and to who) you were born, has a significant part to play.

Although granted it is not the be all and end all.

Oh come on, P8, you display some remarkable willing blindness to NZ society for someone who only a few posts further up was celebrating his own astuteness. You simply cannot willfully ignore what we have done to society, to home ownership rates, and the current wealth transfers via policy.

In very recent news there was clear coverage of the amazing ride folk have received from this transfer of wealth from preceding and succeeding generations since 2000.

"Yada yada yada, it's always been hard, I grew up in a hole in the ground" posts don't change that.

There's a problem because every simpleton with a bit of equity is piling into property, nothing else is providing returns.

My suggestion: Stop people leveraging off imaginary money. It's a Fu*king ponzi. FFS.

"Stop people leveraging off imaginary money"

Only for housing? what about consumer goods eg car or is that too close to the bone

Item on tv news last night showing the queue of pretty flash looking cars lining up for the food bank...

Hi Beanie,

Look a little closer next time. The flash cars were being driven by people who were donating food...... The recipients of food were walking.

TTP

What aboutery on steroids here, folks

To be fair, I don’t even think the market has risen. I think it’s still in a downturn.

Nobody even noticed the downturn in property, it actually started in 2014.

I think about it a lot differently to everyone here

Can you please explain this further? Why do you think it's still in a downturn that started in 2014 and how do you think about it differently to others?

You have to adjust it all for purchasing power, not meaning CPI when I say that. It takes a bit of work but you can strip out various factors which show a pretty horrendous market underlying everything.

By one measure, the property market is actually currently around 40% lower than it appeared in 2013, and started that decline from around 2014-ish.

Thanks, Greg, for confirming what most of us old cynics have felt in our water for - oh, a decade now.....

yes exactly, talk about stating the bleeding obvious.

It happens for two reasons.

1. The amount of savings made by a fall in interest rates can be leveraged, eg save $5,000, can borrow an extra $50,000.

2. The extra demand this causes, without an increase in supply just adds monopoly non-value-added costs into the system.

And as you state, this always has been happening, it's supply and demand economics 101.

Yet the politicians seem surprised that when they add costs into a system, the price goes up.

Saw the article on the unremarkable old 3brm houses in Otara going for $1m+. Hilarious

The media likes to advertise outliers, because it causes more FOMO. This gets them more clicks ad helps our their advertisers / agents to keep the market popular.

People used to talk about TV programs around the water cooler at wqork, now it is house prices, and how much more their house has made them, than they have made working in their job.

To obtain insight as to why things are happening the way they are, it is necessary to focus on the interest rate for fixed deposits. It is the sharp decline in those rates that is creating reluctant landlord investors.

Keith W

A friend who owns a small piece of commercial real estate and 2 rentals (freehold) did exactly that last week. For the last 5? years he has been putting money into ETFs from a wide array of sources wanting to reduce his property holdings. He became disillusioned with the nominal return on his limited term deposits and opted for a 1-bedroom apartment in Ellerslie. Unfortunately we are not as well capitalised as he is, and after 10+yrs of good growth in stocks have opted to sit tight with a partial move to kiwibonds (away from trading banks) and see how the next 1-3 yrs pan out.

Same hete. I have funds coming off term early 2031 and am already looking for a rental. I don't want to outbid a fFTHB however can"t take 1% (pre tax) as I rely on the interest for my retirement.

I assume you mean 2021.

How about shares? My dad who is 80 has about 400k in a nice package and gets dividends throughout the year which supplements his pension.

LOL - yes 2021. I am also looking at shares but cashed in a lot so I could have a strss-free life as even 3% was ok for me. I read this site daily and reading any and all suggestions - thanks.

Buy BTC and sit back and relax

EdwardD,

You must do what you feel comfortable with. I have both a share portfolio and a rental which I have owned for over 20 years-no mortgage. It is in Mount Maunganui, so its value has risen greatly and my tenant has been there for almost 11 years now.. My portfolio is primarily in good quality dividend paying companies and I am in no doubt that it has outperformed the rental. Unlike the rental, I do not have maintenance costs which in some years are significant, nor do I have rates and insurance, both of which increase each year. I also do not need to comply with changes to the tenancy provisions-most of which I support.

There are a lot of costs involved with owning a rental, and a lot of work. Many people have mainly benefits due to the capital gains, rather than the actual rent it makes.

Yes.

I'm guessing a lot of these reluctant first-time landlords will be feeling the pain of being one sooner or later... no pick-nick at times.

Maybe we need a new season of the tv series "Renters" concentrating on the disasters of these reluctant landlords getting lumped with awful tenants by property managers hobbled by rules that are based on the fiction that everyone deserves a house to live in.

Or reverse Landlords who dont realise that they are running a business and treat renters as lowlifes. Example just moved into a expensive flat in Wellington that the previous tenant had not cleaned the day before (moving out) leaving the place filthy including mouldy curtains. Landlords response..."there are different levels of clean" and you can always terminate the lease?

So you went "there are different levels of payment, either full or partial" haha

Exactly & this is why you need intelligent monetary policy. The "market" has worked out that the true inflation rate run's higher than the 1.5% CPI the govt try's to sell us. When you can only get 1% on your money with a term deposit (.7% after tax) even if you don't want to deal with the many hurdles of managing investment property you have no choice to. Otherwise this inflation will destroy these savings.

It is truly a national tragedy that a retiree is relecutanly forced to outbid a first home buyer to protect their savings. No winners here. The system is broke.

Agree, completely dysfunctional - regulation is required.

#rentcontrolnow.

How would rent control solve this? Curious

It protects those who do not own assets from the asset price inflation we are seeing in relation to housing.

And prevents us from having to implement the even more draconian moratorium on evictions as per the US;

https://www.cnbc.com/2020/12/21/stimulus-deal-extends-national-eviction…

Great question JLM, the simple answer is, it doesn't

Or you could just change fiscal policy to target the money supply, or close the capital account, like the periods 1900-1990. Money supply growth, capital gains and nominal prices all moved together.

Can’t have an open capital account and expect property not to rise relative to GDP. Unless you expect the country to save money.

House prices don't matter as much if you have rent controls in place.

Yes they do, as they’re the intermediation asset of the banking system. Intermediation assets must always rise else banking sector assets become threatened and the supply of credit is constrained, at which point import prices rise, or risk premia, or both (e.g those who you were trying to protect with the controls begin to feel more pain)

Rent controls are not the panacea you think they can be, they have serious economic and social effects.

Yes, and unaffordable rentals have serious economic and social effects as well;

https://www.rnz.co.nz/news/national/433415/trade-me-figures-reveal-new-…

And as I've pointed out - get to that point and what does the regulator do? They regulate for never-ending non-eviction rules;

https://www.cnbc.com/2020/09/08/most-evictions-in-the-us-are-now-banned…

So do banking crises or decades of deflation. Far more pain than the last 30 years (excluding pre 1995)

Just raise the savings rates, that’s called good government policy. Invest in infrastructure, exports. The only reason property rises is because TINA, and 30 years of no savings.

Develop the debt markets, raise the savings rates, invest in infrastructure and exports.

Rent controls are a backwards solution that solve nothing, as they aren’t the core problem. The core problem is backward productivity rates, poor government fiscal policy, and lack of capital to the cumulative tune of around 60% of GDP! 60%!

If you think it’s bad now and are calling for action to change, I’m all for it, because if NFL’s unwind then it will make COVID look like a walk in the park.

Agree with all that. And agree rent controls are not the core problem for the economy as a whole. But they are the core problem for those of us least able to weather the storm that you point out is coming; and they might even raise the savings rate as you suggest needs to be done.

..

I think you are way over-stating the potential effect of rent controls.

Less than a third of households in NZ rent, and of those, previous findings suggested only 30% of those renter households were paying in excess of 30% of their income on housing costs;

https://www.hud.govt.nz/news-and-resources/statistics-and-research/hous…

More over, only a very small percentage of the lower end of the rental property market were properties purchased recently (i.e., in the past 1-2 years) at these highly inflated prices.

Hence, only a very small percentage of property investors might need to sell because of the introduction of rent controls. Hence, no house price crash, of the kind you are implying, is even a remote possibility.

We can't carry on "having it like now" as the cost of the Accommodation Supplement continues to rise; the state house waiting list continues to grow; food banks are stretched to their limits; and employment becomes less certain for many (with the prospect of household incomes falling).

The accommodation aspect of the cost-of-living for non-asset owners needs to be brought into line with what is affordable, particularly for those in the lower quartile household income bracket.

,.

I really appreciate the discussion, so thanks for engaging. I've looked a bit at overseas experiences, e.g.,

https://www.brookings.edu/research/what-does-economic-evidence-tell-us-…

And where I would differ in implementation is that I would suggest a universal rent control (weekly maxima) mechanism (as opposed to a 'designated rent controlled property' one). I've suggested that universal mechanism would be based on a formula such as: (RV/1000) +/- x% - where 'x' is determined on a regional basis (depending on the revaluation cycle and market conditions at the lower quartile of accommodation choices).

Annual rent increases would be aligned to CPI and the 'market' increase in accordance with RV adjustments, would occur once every three years. The 'x' variable might need adjustment at that time as well regionally, again, depending on whether or not valuations are still running well ahead of inflation.

I think our current state housing market, where rents are pegged to household income, is likened to 'the neighbourhood effect' as detailed in the study above. It aligns more to overseas experiences where only certain 'designated' properties are subject to rent controls.

I haven't seen any studies linking the implementation of rent controls to CPI rises and general system instability - and yes, would be keen to read material on that if you have any links.

I'm really only concerned about a formula that addresses cost-of-living / accommodation at the lower quartile end of the rental property market - as it seems at the higher end, that markets rents are already more aligned to ability to pay (i.e., the market is more functional in that regard).

Email me and I will explain. My email is attached to my profile if you can see that. Would prefer private discussion as is commercially sensitive, but interesting.

"The system is broke"

Give people what they want... plenty of housing choice, my development has languished for two years, it would provide housing for over ten households. Many hurdles but the biggest is council. Sometimes feel what a waste of time and money.

Council is is an easy scapegoat, are you confident your consultants have advised you well?

Councils are often challenging but in my experience poor consultant design and advice is as much a problem.

The absence of consultant accountability often leaves council with egg on their face. It's unfortunate as it is endemic in all industries

Council said they would accept straight residential but the architect wants to draw up mixed use based on what the district plan says and his interpretation. That is the problem that the district plan is very prescriptive with council trying to micro control everything. We know what we want and what will work but others like to tell you whats what and what to do. Earlier decades weren't like this and the result was more output ie developments. Its easy to get caught up paying huge consultancy fees and going no where, as what happened on an costly earlier project.

'His' opinion- he's an architect, not a planner or lawyer. Architects often get themselves and their clients in trouble because of their arrogance. They need to stick to their knitting, they are not planning experts, nor engineering experts etc even though they often think they are.

Did you have a planner advising from the outset? Developers often don't and for the sake of saving a few thousand bucks often get in to all sorts of strife.

Seen it many, many times.

Oh yes we have a trusty planner already. The development process though is painfully slow, I realize that I am not that experienced yet but also judging from what others say. We dealt with nzta on another property a high profile commercial property we were looking at buying and everyone warned us that nzta would be massively protracted and the outcome far from certain. Actually our discussions with nzta were quite positive. There was other factors too such as dealing with the iwi for a cultural assessment and they wouldn't even return calls to our consultant. The seller refused to make the agreement subject to getting consent so we pulled out after due diligence. A year later its still on the market which says a lot. My wife and I just drove past today and she remarked the agent probably fibs there was an agreement that didn't get finance. We have done a few good jobs now but I am.getting a lot of experience now of failing to get off the ground and other developments struggling to get consent

There's good and bad planners, just like any profession. Hope you got good, and honest, advice.

A previous planner was completely useless for us and talked waffle while billing is plenty although I guess it depends. Is that your field fritz.

Related field. Just like any profession there are good and bad planning consultants. In my opinion far too many are overly optimistic. Sometimes that means better ones get less work, but their credibility attains better longevity.

I know a farmer ... he is out standing in his field. I jest, but imo council rules and govt legislation has become more and more and more complex with more groups who feel they have a right over others freehold property. The previous property I mentioned, and my planner handled the meeting with council superbly, but council was saying we needed cultural assessment as well as something from I think heritage nz for a piece of dirt next to a main road intersection that had been rolled and graded etc ... there could have been evidence of early European and/or significance to Maori. Probably not but council want to cover their butts. End result property not sold not developed no economic growth or output no jobs no income. People here wonder why I want someone to blame for it and why I want things to change

RBNZ has cut OCR in half five times since July 2008, which prompts the already rich to capitalise rising discounted present values of future residential property asset cash flows.

{kind=link}

Furthermore, if one has a recurring annual $10,000.00 liability in need of funding, deposit $100,000.00 in a one year bank deposit account paying 10% annually.

If annual interest rates are cut in half to 5% during the deposit term, how much does one have to deposit for one year next year to be in receipt of $10,000 to liquidate the same value annual liability?

Yes, $200,000.00, hence the adjusted PV discount factor for the original $10,000 cash flow @ 10% for the cut in half 5% rate is 0.95 x 2 = 1.9 x $100,000 = $190,000.00

Much easier and less capital intensive to add annual liabilities to the mortgage.

We have been financialised to suit a purpose. Impoverish the children comes to mind.

One man's asset is another's liability/opportunity-cost

What are the affects on risk perception from manipulation of risk-free rate in the market? Does the whole curve flatten and how does this work for those seeking higher returns?

Impoverish the children comes to mind.

When coupled with the efforts previous generations post-WW2 went to that created affordable housing supply, we've truly seen a few generations mooching off the wealth of the preceding and now succeeding generations. While patting themselves on the back for standing on their own two feet.

Auckland house prices are now just silly, even though I had enough money to buy one you simply cannot justify the cost of it. Loving the move to Tauranga, everything factored in including the lifestyle, house prices are "Half" the cost of Auckland. Looks pretty easy to control house price increases to me, just start raising interest rates.

The justification came to me with the announcement of the FLP and the Orr vs Robertson Monty Python skit. At 2.5% my mortgage payment (if I borrow the amount I got pre-approved for) will be just $50 pw more than paying rent on a similar house. Combine that with the squeeze in term deposit rates and the clear display of ZERO intention from govt to fix the issue and the conclusion is pretty straightforward.

I'm not saying you are making the wrong decision but I hope you are taking rates, insurance, and maintenance into your equation which are not collectively insignificant costs of homeownership.

Rises in Council rates are a bit of a wildcard to factor into the mix as well. Might be difficult to pass on those costs to renters in the future if the rental market is at the maximum it can pay.

You're right. If landlord costs dictated rents you'd have seen falling rents with the falling interest rates recently.

Yep took that into account as well. Interest + rates + insurance combined together cost less than what I'm paying as rent, so it makes sense to buy. Maintenance will obviously depend on the house - so far, after almost 6 years of renting, the total maintenance on the places we rented was about $500.

Lol

CJ, good on you for getting your own place, it would have been immensely more beneficial to listen to the horrible, greedy, selfish, parasitic specuvultures on this site and buy 6 years ago but good on you for buying now, you won't regret it.

Yvil, you have no idea about my situation back then. I wasn't even living in NZ 6 years ago. I had about 10000 euros to my name, which was all spent on relocating to NZ. I had 0 dollars to my name early 2015, and actually owed my parents $5000 until I got my first few paychecks here.

This is exactly what you guys keep ignoring: young people weren't in a position to buy 5-10-15 years ago.

Don't bother, they don't get it and don't want to get it.

I wish you luck i think its a good decision but it's a shark tank/ zoo out there. I say get the crapiest house you can find and make it the best house for the least amount of money. Something that has min 600sqm land that your kids or you can enjoy and you can plant an avocado tree. Everyone must have an avocado tree to do the one finger salute to those know it all economists.

You just don’t know when to stop digging do you Yvil?

Do you regret not buying a couple of residential property investments then?

We just bought the house we were renting for the 18 months as it's basically the same cost as renting it. BTW you'll get lower than 2.5% if you've got the deposit....

Where did you get lower than 2.5%?

Gen can advise but speaking for myself we got 2.39% recently for one year from BNZ

Thanks, Fritz. I guess they'll all respond to a wee bit of pressure, maybe.

We got 2.39 from ASB :)

Cheers!

It sounds the only way prices can go down is if FHBs start to deliberately boycott the market and/or leave the country. No other ways, young people have too many interested counterparts which are quite powerful in this market ( if the word ‘market’ still applies, which I seriously doubt)

We will just keep doing what we have always done: import lower skilled workers to replace them and add professional occupations to the skilled shortage lists so they can keep middle-class wages down. We already have 1m people living overseas, there's no incentive for young people to stay and no one is really interested in doing anything about it. The ones you should pity are the ones stuck here for family/medical reasons and who couldn't leave even if they wanted to.

If we were going to do something about it, things would never have been allowed to get as bad as they are.

Orr use real inflation numbers.

I have been running the numbers as it has all been unfolding. Repayments at the moment for many properties on the North Shore of Auckland are now on par or even higher than they were in 2018 on 4% interest rates. For many we have seen a year or two's worth of gains in just a few months. Pretty crazy to see so many Kiwi's taking on these mountains of debt when the Global economic storm is only 10 months in and there is no quick fix to this Virus situation.

Too big to fail comes to mind.

Serious question: what will be the impetus for increased lending rates?

- could we have another Credit Crunch scenario?

- oil shock? Other supply shock?

- I see trade is becoming increasingly problematic with supply-chains jammed up...

My current guess on the impetus question is either:

a) Rapid acceleration in loss of confidence in the US dollar

b) War

So 20% increase in 6 months is 40% annually and still Mr Orr and Jacinda Arden are thinking and worried BUT no action.

When it was the other way round that house price may fall....it was all action and more action......

This sums up the thinking of people in power in NZ.

The economy is absolutely humming considering the global conditions, herein lies the conundrum

Jacinda doesn't have the cognitive fortitude to think in depth about numbers and her being "worried" is just a schtick for the fools who still don't see through her pantomime act.

The truth of the matter is that New Zealand is irredeemably screwed with a totally out of control asset bubble and Jacinda lacked the character to do the right thing instead of the easy thing.

Inflation and global interest rate increases will come before not too long and it's not going to be pretty when they arrive.

One thing you can be certain of is that the levers will be pulled and twisted to dump the consequences on the young and the poor. It's the kiwi tradition.

I can't see much inflation on the horizon.

Hence I don't think interest rate rises of any real consequence are likely over the next few years.

Six months from now the virus will be history in the developed world. An economic boom is coming and monetary policy will need to be tightened before long.

Maybe...

Personally I don't see a boom coming, there will be residual damage and governments will need to be tighter with their spending.

Yes. But this covid nonsense has been a massive handbrake that will be released in the next few months in the northern hemisphere and there is a lot of pent up demand to add into the mix.

Anecdotally, I've been through this mess in the UK and everyone is gagging to live again and very few are going to prioritize counting pennies when the time comes.

Sure. But I just think that pent up demand will be balanced out by other factors.

If you think the nz property market is crazy, wait until the borders reopen and more people want to come live here. Foreigners/non nz citizens are still allowed to buy homes in certain cases

We've seen limping along based on more and more debt, and cheaper and cheaper debt...where will the growth boom come from?

It won't have anything to do with inflation, but everything to do with unavailability of credit.

There could be supply shocks inflating prices.

Credit could be issue if mistrust ensues and becomes systemic e.g. over exposure in asset bubble real-estate.... but hey, good old taxpayers come to rescue again

It seems like there must be some sort of scientific formula to determine house prices. Some iron law of accounting. At any one point there must be a certain percentage of property investors that will sink into negative equity as soon as there is a downturn and be financially ruined. There will never be a situation where everyone is 'braced for impact' as it were.

In a sensible world when there has been a pandemic and an economic jolt and the country has pulled through, dodging a bullet, the sentiment would be to get better prepared and save even more for a rainy day and build equity. But not in this world, in this world we 'double down' on debt.

And so it must be, that we cannot protect everyone, indeed it may be dangerous, against nature, to do so. Those that don't prepare for a rainy day are taking a chance and in doing so may win big. Or they may lose their shirts.

https://www.newshub.co.nz/home/politics/2020/12/people-have-given-up-ev…

Watching that smug POS Ashley Church sit there smirking whilst the other presenter tells of her experience being outbid at auctions is enough to make me want to vomit (all over him)

Watching that smug POS Ashley Church sit there smirking whilst the other presenter tells of her experience being outbid at auctions is enough to make me want to vomit (all over him)

The same Ashley Church whose predictions for 2020 (published in Granny Herald in Nov 2019 https://bit.ly/37EIawF) returned 1 correct out of 7?

It doesn't take much to be a media darling in NZ.

He is employed by the duplicitous snakes to run the NZME property spruiking site.

BL...One Roof... modern day pornography at its' most vile.

Starring Anne Gibson, Ashley Church and Ron Hoy Fong.

Ohhhhh the mental imagery....

J.C... I personally emailed Ashley to ask how he attained the title "property expert", which is so often accorded him. Self proclaimed would be the only justification I can think of. He often can't even accurately "predict" the past. If you think his commentary on property is ignorant and biased you should listen to some of his stuff on the Israeli/Palestinian problem. It truly shows him for what he is.

karl....follow this link..it might enlighten to what is going on

https://app.companiesoffice.govt.nz/companies/app/ui/pages/companies/11…

Watching him touch her on the shoulder, between all the smirking and commentary on how great rising house prices have been for the country, made me gag a little...

He is a shining example of all that is wrong with our country, I can't believe the media promotes his message. He is scum.

He sums up the person who's lived off the wealth of surrounding generations by receiving affordable housing from previous generations, then voting for government and policy that transfers wealth from succeeding generations through asset inflation and artificial scarcity. Amidst much self-congratulation.

Tone deaf alright delighting in others misfortune. For his own safety he should at least pretend to be concerned with a frown and head tilt.

I think his pretense at genuine concern, would likely be even harder to watch than his usual open display of apathy.

He is a shining example of all that is wrong with our country, I can't believe the media promotes his message

You might not be aware of how Robert Shiller was accused by journalist George Will of potentially losing people money by suggesting that markets were being dictated by irrational exuberance. Do not rely on the media if you can't think independently. Most people in NZ can't. This is why we have Ashley Church and Mike Hosking.

He's awful.

I would have Hosking over him any day. At least the Hosk occasionally shows some balance and humility. Occasionally.

Thanks, lol

Agree.. Is he on drugs? Or is it just a horrendously over inflated ego??

If I was young I'd book a ticket and leave. New Zealand has a population of 5.2 million but sufficient housing and infrastructure for about 4 million.

"Better pack her up and go, Detroit or Buffalo..." - Barbara Keith.

House price problems are raging almost everywhere now. Maybe not as bad as here granted.

Money goes much further in Brisbane, Adelaide , Perth and even Melbourne

Those numbers aren’t that astonishing to me. $500 a week isn’t that much for a couple is it? Even if both on minimum wage soon to be $20hr they are earning $1600 before tax a week. Difficult for someone that is single granted but that has been the case for decades.

If wages kept pace with house prices, then sure, easy peasy lemon squeezy

It’s not really much worse than when we bought our house 15 years ago, probably about the same inflation adjusted. I guess the difference is that our house is in Auckland while that is the national average.

The problem is that in the cities with most of the jobs the outgoings are much higher than that, yet income isn't necessarily higher.

Another challenge is losing an income, even for a couple of years, when kids come along

if they are earning minimum wage then they aren't taking home $1600 a week...closer to $1100 after tax

i read the stuff article this week...they have a new measure...a couple on median wage can save for a house in 224 weeks if they save 30% of their gross wage...what a joke

if you take 25% of the wage packet in tax, then 40% of what is leftover is used for rent...you still have 35% left over but you have to cover food, clothing,car/public transport, student loan repayment, medical, something of budget for entertainment unless you want to live as a monk and never see your friends for five years...the numbers just simply don't stack up...there is nothing left over to save 30% of your gross income....its a ponzi!

please enlighten me if you see the numbers differently

1600/wk. That's for 2 people, so $800/wk each or $41.6k/year each.

41.6k gross = 37.7k net, or $667.73/week

https://www.salaries.co.nz/cd/tax-calculator/41600/dollars

667.73 x 2 = $1335/week net

Add in WFF and they'll be getting close to $1600/wk

???

Add in WFF and they must have children, in which case that isn't a lot of money...

I was just replying to gnx's comment to show that $1600 gross a week on two incomes brings in a lot more than $1100 after tax. At least $1335, maybe more.

That should give an opportunity to save, at least outside of AKL/WTN. Not saying that it's easy.

Yes and in 10 years they will have a deposit that would have been enough 10 years prior.

If two people are still on the minimum wage after 10 years working then should they really expect to be able to buy a house?

It's a bit of a moot point as wage inflation has never matched housing inflation recently (and likely never will) and any wage inflation that is produced will be eroded by consumer inflation.

You're assuming a 40-hour week. Most minimum wage jobs are 30 or less, in which case, assuming KiwiSaver contributions at 3% (and why wouldn't you to get the extra money from the Government per year?) and no student loan (since if you've got a student loan, you're probably not working in a minimum wage job), you'd be getting $1000 / week take home as a couple.

Take off $500 for the mortgage, $50 for rates, $25 for insurance, $100 for groceries, $50 for utilities, $25 for transport, you end up with $250 / week to pay for everything else, including house maintenance, clothing, health, et. al.

its called Raiding the Balance Sheet ... through leverage

replacing real Income for paper gains on assets

The NZ housing Ponzi has reached such ridiculous levels, especially in international terms, that it is not even funny any more. It is so inflated now that just defining it a bubble does not even start to describe it.

The Japanese never thought they were in a bubble (equities and property). Mind you, very few in the West thought Japan was in a bubble. History shows it was definitely a bubble.

Japan has never fully recovered.

One way in which we may be different is that Japan had and has very low immigration and an aging population. We have an aging population we provide much social welfare to, but we run very high immigration and I'd see both National and Labour only increasing this in future. Occasionally one or other liar will campaign halfheartedly on pausing it, but the economic advice behind the throne will be that NZ's economic model (pump assets, welfare for oldies etc.) can't do without it.

Yep that's a critical difference.

Another big difference is the respective savings cultures.

One way in which we may be different is that Japan had and has very low immigration and an aging population.

What are you trying to say? That positive migration can prevent asset bubbles from bursting? Secondly, the demographics of Japan never prevented their bubble from happening. Demographics can be forecasted over 50 years quite easily. Never prevented the Japanese bubble. Your argument is that the bubble can be preserved. I'm skeptical that there is a willing tide of migrants ready to millions of dollars for houses in suburban NZ.

This is an argument I've heard countless times before. It is not a well thought-out argument.

Fair point, although remember that Japan's population grew moderately strongly from the 1960s to the late 80s / early 90s

Fair point, although remember that Japan's population grew moderately strongly from the 1960s to the late 80s / early 90s >

Based on whose benchmark? Source your data and claim. Japan was already concerned about an ageing population in the early 90s. Massive demographic shifts don't occur overnight or over a change in birth rates over a time frame of 10 years.

Common historic knowledge, and I just checked and saw a graph that shows it was just under 100 mill in 1960 rising to about 120 mill or so by the mid 1980s.

It may not have been massive population growth, but it was significant. It certainly would have underpinned housing demand.

I don't think you get it. Japan's property bubble and its demise was not caused by demographics. It was caused by loose and easy credit and the dissipation of that loose and easy credit.

Why the passive aggressiveness?

I know a lot about Japan, I lived there for a couple of years in the 90s and my first degree was in Japanese history.

I never said the bubble wasn't largely about loose credit. I was merely addressing the population growth and housing demand question that had been raised.

That would have been a factor in the bubble, probably less than loose credit and pyschology, sure.

I'm not arguing it will necessarily work, just that it will be tried. Foreign buyer ban would be lifted, high-volume migration invited, foreign investor visas thrown at bolthole-wanters, anything tried to prevent property investors being affected. I could imagine that it may reduce a decline in prices, but I have no idea to what extent it would be effective. It's all conjecture.

However, there is certainly a massive volume of willing movers to NZ. We've seen that in recent years, let alone as quality of life declines in some other countries (e.g. the Philippines under Duterte).

Yeah I agree

After reading the small print I would say a lot are so heavily in debt up to there eyeballs i hope they have actually prepared for life's uncertainties. (30 year rate based on both working FT, on a 2 year average rate)..that's about as good as it will ever get, but experience tells a lot of us it won't be like that forever.

Haha, good ole Hamish Walker getting a piece of the action

I'm surprised Interest hasn't run an article on the latest Centrix data, mortgage delinquencies are beginning to increase, first time in a long time.

https://www.nzherald.co.nz/business/shaky-foundations-more-kiwis-missin…

Since 1980, rinse and repeat: do not intervene to counter market tendency for top 20% to steadily increase share of national wealth. Rest is that rents continue to rise and wages fail to keep up with productivity or living costs (esp housing.) Leads to demand deficit. Leads to more borrowing to finance the hole in consumption and ensure people continue to have ability to buy stuff they do not in fact need. When interest rates cannot be cut further and people will not borrow more (as % of monthly income) you have a problem: where is the demand to come from? This is why the current financial system, and including housing, is a Ponzi and why its sorry tale is approaching end game.

The demand comes from negative rates and money printing of course. Orr has still got plenty of brrrrrrrr left.

Jacinda and Grant are so allergic to DTI restrictions for a reason.

"The rate at which house prices have increased over the last six months has not only erased the benefits of lower interest rates. It has also eaten up the increases in wages over that time"

I have always claimed house prices react in direct opposite direction to interest rates. Now it seems house prices have over-extended the drop in interest rates and it seems increasingly that banks are getting tougher with their lending. Also we've been building more houses than before and we had almost no immigration compared to a year ago. So… I'm at a loss to explain the still incredible strength of the buyers…

Anyone care to explain why the RE market is still so incredibly strong ???

But they don't react in the opposite direction to interest rates. There's some correlation, but not causation.

Proof - NZ house prices in the early to mid 2000s increased a lot while interest rates increased.

You are applying rational logic to an irrational, deeply gullible and barely numerate general populace who have been brainwashed into thinking its impossible to lose with property.

The pathetic leadership of this country only reinforces it.

Therefore it doesn't matter how much you pay because it will always be worth more tommorrow. Bid the maximum the bankers will lend.

Minsky will have his day in the sun.

That's a good point. It's not rational, and defies easy logic and explanation.

Psychology is a huge part of housing bubbles. Heaven forbid, if a bubble pops the psychology is forever damaged.

That's probably the best explanation Brock, house price increases started because of lower interest rates but they are now over-extending because of herd mentality.

I'm actually happy to make another prediction on which you can hold me accountable on (Fritz). In 6 months time, there will be no more house price increases (HPI figures for June released in July) UNLESS there is another significant drop in interest rates to below 2%

"Anyone care to explain why the RE market is still so incredibly strong ???"

More buyers than sellers?

I speak to a few people in the UK and they are absolutely hating life. Brexit, hard lock-down and mid-winter - they want out. The perma-gloomy just won't accept that NZ and a few Australian States are Royal Flush's in a messed up world.

Meri Kirihimete everyone, safe travels.

In about three months all of those issues will have passed and NZ will still be ridiculously overpriced.

Sometimes our isolation and small size is a blessing, sometimes it is a curse.

With covid, definitely a blessing. I for one am grateful.

Could be a short bit of chaos as those who were sitting on the fence get in?

Could be investors finding there is no where else for their money?

Could be the failure of kiwibuild and Labour no longer trying to reign in prices?

Could be no more threat of property taxation?

Could be the relative desirability of NZ at present?

Could be Ashley and essentially free advertising on NZ herald?

Could be people upsizing as working from home?

Could be LVR easing?

Could be people more fearless due to pandemic?

Could be everything!

Related to your fourth to last point:

Could be people being more able and willing to work from home, supporting the market in outer suburbs.

Yvil - The strong market to date can be explained by extraordinarily low interest rates - which has destroyed income from term deposits. Plus the removal of loan to value restrictions by Reserve Bank, which allowed buyers into the market who were previously shut out as they did not have enough deposit. Last but not least, there was also the very high net immigration for the year ended March 2019 (lagged effect). As you have noted, all these factors have come to an end, or will soon be played out. Next year will be interesting.

They haven't really come to an end. Migration will pick up again. LVRs will be removed again. Interest rates will go negative. What the government need ot do is make building a lot cheaper, by removing GST, and provide cheap land. Plenty of land in NZ, it is just locked up. Try buying a piece of land in many towns now seems impossible, ether because there is little choice or the price is too high, and it seems to get drip fed into the market.

To all you pro- purchasers of property to gain investments and wealth... shame on you ya greedy huias. Who ya going to sell to, when all professionals, and trades come over to Aussie to actually be able to make a go of life... when I was in NZ the cost of living was so high, and rents so expensive that a deposit was near impossible to save for. Young NZers MUST get over here...unfortunately at the cost on NZs society. Like I said before... NZ has cut of its nose, lips, eyelids and testicles to spite its face....

I always suggested our young Jedi healthcare pro. to go to MelB, Brisbane, Adelaide, Perth, Sydney. NZ is unique place if you want to work hard and not getting the reward nowdays, specifically in the Healthcare area. But my guess is NZ future well deserved all those that being passed on with just 60-70%.. to look after them. Oh, be kind and Merry Christmas..

I know of someone who is thinking of listing their investment property at a really high price, just to see if someone will bite. If they don't get the price, then they will continue to rent it out, and it will only cost them a trademe property listing to do. When there is a lack of supply, then there are going to be some desperate FOMO people that may bite. This sort of thing IMO could artificially push prices up a lot, due to the current economic and world situation. I suspect there are quite a few people doing this, especially people with rentals, as the rules are about to get tougher.

How different would the outcome have been if the LVR restrictions had not been lifted at the same time as dropping interest rates?

Next up. Zoning. The magical 'ring' fencing of where banks will target lending to, or not. Just to be safe.

2021-25 will be a clear winner for housing investment, the law of supply and demand can always be twisted/tweaked by other means, PM still uttering 'supply' to catch up with demands. Overseas demand has been stopped, so FHB+investors now competing for the limited supply. This is 2020 factual.

The housing ownership is up into 65% of general population with the recent OCR down, stimulus, LVR removal, wages subsidy. So to get NZ close to 100% home ownership, OCR is in dire needs to go down further into negative area, the FLP must be balanced into housing via credit union & building society, lastly a further billions QE needed for climate change proactive measure, Mr. Orr/RBNZ team will be the first in the world to do so (NZ leading again, punch above the mostly uneven gonad line). Govt, should pro-actively in majority voice to remove the bright line test and make sure to extend/increase the amount of flexi-wage subsidy. While waiting for the next wave of overseas investment come in/people move in again, those measures above will ensure the steady upwards GDP trajectory, this is very crucial time to maintain the momentum.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.