Treasury is conceding that much slower house price growth due to Government policy changes will have a dampening effect on the economic recovery.

And this will prolong the period of monetary policy support needed to raise inflation and employment to target.

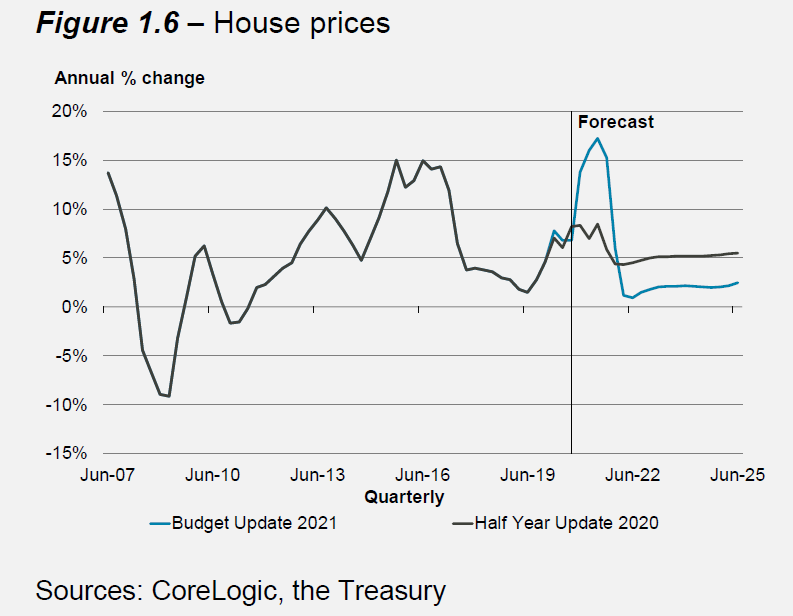

In its Budget Economic and Fiscal Update, Treasury says of the three housing-related policy changes announced on March 23 it is the removal of interest deductibility on existing residential properties that's expected to have the largest impact on the housing market "and wider economy" by significantly reducing house price growth over the forecast period.

It is forecasting annual house price growth to reach a peak of 17.3% in the June 2021 quarter before easing to 0.9% by June 2022. As borders reopen, higher population growth and continued low interest rates are expected to result in a gradual increase in house price inflation, reaching 2.5% in the June 2025 quarter. The slower pace of house price growth means house prices end up around 4% lower in June 2025 than forecast in the Half Year Update, and around 16% lower compared to an updated scenario without the policy change.

"House price movements have a broader impact on the economy. When the value of the housing stock increases, homeowners’ household balance sheets rise, causing them to feel wealthier and more inclined to spend, which raises private consumption. House price growth also encourages residential investment, with higher prices enabling more projects to be brought to the market as returns on investment rise to sufficiently high levels," Treasury says.

"Slower house price growth will likely dampen these effects, resulting in a slower economic recovery than otherwise and prolonging the period of monetary policy support needed to raise inflation and employment to target.

"However, the levels of private consumption and residential investment are still forecast to be substantially higher than in the Half Year Update. The impact of the tax change on house prices and the associated effects on the wider economy are uncertain and present significant risks to the economic forecasts."

Treasury says leveraged investors will be impacted the most by the removal of interest deductibility, which will increase their tax liability.

"Highly leveraged investors will be more impacted than those that are less leveraged, implying that highly leveraged investors will demand fewer homes going forward. Furthermore, existing property owners facing higher tax costs may seek to divest to bring overall costs down. This will increase selling pressure and reduce demand in the market for existing homes. Non-leveraged investors and owner-occupiers are expected to be largely unaffected by the policy change," Treasury says.

'Impact uncertain'

It says the overall impact of the housing Package on the housing market is uncertain and depends on various factors, including the final design of the policy and the extent to which other participants (including first home buyers) "step in to fill the gap in demand" left by leveraged investors. The Treasury forecasts assume that other buyer types will enter the market, moderating the downward pressure on prices, "but that their willingness to pay will be lower than the leveraged investors who exit the market".

"The overall result is that house price growth is forecast to continue, but at a significantly reduced rate compared to a scenario without the policy change."

Treasury notes that interest deductibility will remain in place for new builds for an undecided length of time, which is expected to result in a migration of leveraged investors from the market for existing property into the market for new residential developments. This is likely to reduce the impact on house prices, as demand from some leveraged investors is redirected towards new housing rather than being lost entirely.

"Additionally, some owner occupiers and less-leveraged investors will be displaced from the new build market into the existing home market. To the extent that new and existing houses are substitutable, it is expected that prices across both markets will converge, but the incentives to build new properties are ambiguous and could vary by location. Nevertheless, the new equilibrium price for housing will likely be lower than without the tax changes, but higher than without the exemption for new builds."

Treasury said key policy decisions relating to the housing package were yet to be decided at the time of forecast finalisation, making it difficult to estimate the fiscal impact with a reasonable level of certainty.

"These policy decisions include the duration for which interest deductibility will remain in place for new builds, definitions of ‘residential land’ and ‘developer’, and whether interest deductions would be allowed on the sale of property, among others."

'Bold assumptions'

Meanwhile advocacy group Property Council New Zealand said it was "sceptical about the bold assumptions made regarding house price inflation" in the Budget.

"There is no clear evidence that interest deductibility and bright-line changes will lead to such a dramatic reduction in house price inflation – especially since many of the details around these policy changes are yet to be finalised or announced," chief executive Leonie Freeman said.

She said there was no doubt the Government "has invested heavily" in the Budget.

"However, for many of the core issues around housing supply, climate resilience and delivering infrastructure at pace, the Budget doesn’t offer any new, alternative options.

"It’s encouraging to see the Government engaging with the community and investing $733 million in Māori housing, and our members are supportive of any initiative that increases and improves New Zealand’s housing stock. However, it would have been good to see further investment in alternative housing initiatives to help fuel our housing supply.

“There is no mention of initiatives like Build-to-Rent in the Budget. At a time where all options should be on the table, Build-to-Rent offers the Government a unique opportunity to support longer term options for New Zealanders."

She said much of the detail around the Housing Accelerator Fund was still left out, so it was hard to know how much of a difference this will make to supply.

72 Comments

"Treasury concedes that the Government's changes to housing policy will result in slower economic recovery and 'prolong the period of monetary support needed'"

Did treasury mean that house price after rising 50% in less than a year should jump another 50% or 30% or......in a year.....ponzi should continue...

Also government feels that have tamed the housing market - A house with CV of 990 going for appox 1.7 million ...is that taiming and it happened yesterday, much after housing announcement and reintroduction of LVR.

Number of success rate has declined as it normally does over winter but houses that are been sold are going at high premium.

https://www.landlords.co.nz/article/976518654/govt-reckons-its-tamed-ho…

Just because do not wants to act have chosen 26th May for RBNZ announcement to pursue the policy of Wait And Watch - give enough time to narrate the already drafted scripit.

Fibbing and manipulation with the sole intention to........does Mr Orr needs reasoning or convincing to not act..........

Main conclusion from treasury :

"The overall result is that house price growth is forecast to continue, but at a significantly reduced rate compared to a scenario without the policy change."

Firstly they mention that they are not sure but last year when these people were not sure, opted for least regret policy and now when not sure if housing policy will be effective or not are going with wait and watch- Why.

Secondly are not sure if the rise in price will be 50% like last year Or less, may be 30% or say 20% or even if it is another 10% from here on, how does it help FHB.

Speculative demand has to be controlled and for that.......

The more time NZ stays under control of the Labour/Green, the quicker NZ will become a country that rewards mediocracy, cares only the minority at the costs of majority, kills innovations and productivity.

You aren't entirely wrong.

But it could be worse, imagine being communist China.

China just successfully landed a rover (Zhu Rong) to Mars.

Considering what the new China was like in 1949 when it was first founded after 100 years of war, and what China has achieved to date, no one can deny CCP's capability or more like everyone should applaud for China's achievement under CCP's leadership.

They need to get rid of that autocratic tyrannical Winnie the Pook look-alike President Xi. The guy is a real Joseph Stalin wannabe.

Well, president Xi has had more 30 years of experiences of successfully managing a village, to a county, to a city, to two provinces with population more than 100 million.

I'd thought he is more qualified than anyone sitting in NZ's parliament when it comes to manage a country.

You admire ruthless dictators?

there is no dictator in China.

Lol...

Not in the Republic of China maybe.

If it walks like a duck, looks like a duck & quacks like a duck - odds on, its a duck. And Mr Xi looks like a dictator

Let's not let his minions into Aotearoa eh.

How do you govern a population of 1.4 BILLION people?

There are MANY factions in the CCP, to make out Xi is some kind of Supreme Dictator pulling ALL the stings is ignorant.

Not really, most of the rival Chief Toad Jiang Zemin faction have been purged/executed for "corruption". This leaves Xi with almost complete control. We can see this by his ability to change the constitution and make himself Supreme Dictator for life, with no dissenting votes.

"President for life" not dictator. There is a difference... One name starts with P the other D.

Yes perhaps, but we don’t want him here in NZ

All China did is happily accept American factories fleeing environmental controls and seeking cheap labour, then syphoned off technological knowledge. It was just a transfer of knowledge, pollution, and income, not an act of creation. But China is away now and is really helping with tech advances, so I think there is some upside to come.

Modern China is actually a very impressive these days. I’ve been a few times and it’s a marvel.

Also as any small business owner would know the speed efficiency and execution of working with Chinese B2B is a joy.

Also Chinese neighbours are excellent. Quite, respectful, hardworking and excellent gardeners. Especially compared to the mongrels every suburb in Auckland now seems to have with HNZ draining public funds and incentivising for them to keep popping out kid after kid.

Good on you for respecting the Chinese. Shame on you for your racist dogwhistles directed at Maori and Pacific peoples

The rebuttals in reply make valid points. No need reiterate. I'll just say piss off @xingmowang. Stay out of New Zealand's domestic politics.

'Property Council New Zealand said it was "sceptical about the bold assumptions made regarding house price inflation" in the Budget.

"There is no clear evidence that interest deductibility and bright-line changes will lead to such a dramatic reduction in house price inflation – especially since many of the details around these policy changes are yet to be finalised or announced," chief executive Leonie Freeman said.'

Corelogics report on youtube indicates it is making little difference. But what the video does how is how far fewer houses are on the market in 2021. Far less than 2020, and then far less again than 2019. At some stage these houses will need to be sold won't they, and there will be a glut?

It is interesting that it appears instead of selling when moving, people are just buying and retaining the existing house to rent out or keep for the time being.

The government is saying here our main driver for growth is housing and we would like it to keep going up or we are in big trouble.

How sad we need to encourage other options for growth or maybe look at endless growth as endless costs.

NZ is really on a downward spiral economically if these eggheads really believe their own horse manure

“And this will prolong the period of monetary policy support needed to raise inflation and employment to target.”

What!?!

Hello Treasury – real world speaking here – please be advised that by various measures we’re already there.

And a quick suggestion - feel free to get your head out of the sand before releasing any further updates/forecasts.

"House price movements have a broader impact on the economy. When the value of the housing stock increases, homeowners’ household balance sheets rise, causing them to feel wealthier and more inclined to spend, which raises private consumption" Treasury says. "We drink the 'wealth effect' Kool-Aid along with the central banks, asset bubbles forever!" Treasury went on to say.

But surely that isn't sustainable long term. History shows that house prices drop. Slowing down house price rises is suddenly seen as a bad thing, but that isn't even a price drop.

More like they hope it will raise intention to spend. The boomers are ageing and no longer need to spend like they did. This money printing nonsense is an idiotic attempt to keep alive the wave of spending that came with the boomers and goes with the boomers. Its all about demographics.

"House prices not rising as much will slow economy." Really? I understand their imagined explanations for that, but don't see anything that shows it's so.

What about the enormus drain of vast mortgages. Money that does not get spent in 'the economy'

I came here to make this point. When your whole income is drained on mortgage payments you don't spend as much. My mortgage is only $220k, we're on one (decent) income, and expenditure is tightly controlled. No holidays, eating out twice a year max, and discretionary spending = buying some M&Ms without the agreement of my spouse. I can't imagine having a $750k mortgage and 2 incomes. It must be frightful.

That sounds miserable. Forfeiting holidays when your mortgage is only $220k. Why?

I'm guessing it's to pay off debt as fast as possible. What's wrong with that specifically?

We still visit family and camp on their lawns and plan some DOC site camping holidays. It's a good life. Short answer: priorities. We're on track to pay our 30 yr mortgage off in 27 years. We could do it much faster but we're depreciating our assets like cars, phones, major appliances etc so we can actually afford to replace them, and putting money into our kids' kiwisavers so they get a head start. Also home schooling so we actually get to see our kids grow up. Couldn't do that with a massive mortgage.

Our mortgage taken out in 2017 is about a third less than yours, I too cannot imagine someone needing a deposit the size of our entire mortgage to buy a house.

Yep my deposit was over $290k!

Could have bought our house outright in 2017 and had a good whack of change.

Frankly that’s a pretty miserable way to live your life.

My mortgage is much higher than yours and we don’t really scrimp on much.

The most important thing in life is time and what you do with it.

"What about the enormus drain of vast mortgages. Money that does not get spent in 'the economy'"

Sorry, that doesn't fit their narratives. Negative house price growth is their uncharted territory. They don't know how to manage the economy if that happens. So they choose to ignore and keep telling lies, hope more people get on this train and have couple of more years peaceful time. Cause after couple of years, it will be someone else's problem, not theirs.

I wonder why a link is never drawn between affordable houses and 'wealth effect' ie the lower the house price, the less spent on a mortgage, the more disposable income available to spend - from actual income earned through a job producing or selling products or providing services! As opposed to spending down personal equity in the form of ponzi bubble money. The people who promote this state of affairs need to be rounded up and sacked

Yes, there is. In jurisdictions with more affordable housing, they have more disposable income. Go figure.

Of course, you can't control where they spend it, from extra booze to holidays, to health, education, investment, savings etc.

I'm talking about adults who work for their money and decide where to spend it. Why would you want to control it unless youre a commie in training. Its already being taxed to hell to spend on free lunches that get binned

yes, that's the point, Labour like to control, National less so. But it's all control.

It's like the answer to the old sales question: What is the difference between hard sell, or soft sell? The Answer: 'Getting caught doing it.'

Even National deliberately limited how quickly payouts from EQC happened after the Earthquakes because they didn't want people to get their own money and spend as they pleased.

Govts. main role is to implement laws to control certain behaviour. The further right you go, they feel this is achieved by fewer laws, and the further left you to go, the more laws. What they fail to understand is the right law is more important than the number of laws.

Adam Smith's invisible hand' of the market is really that fine balance where we go about our business without even being aware that we are surrounded by laws that dictate our behavior, the behaviour of which we just put down to 'that is how we want to live anyway,' or it has become so innate, we don't even realize that we are doing it. Putting your seat belt on is a classic example. That law was a hard enforced law, but people have gotten so used to the behavior of putting their seat belt on, that if they forget for a second, they feel so uncomfortable, they are innately reminded to do so. The law that you must wear one regardless hardly plays a thought on making you put on your seat belt.

The housing crisis is people reacting to what the Govt. laws allow, and even encourage them to do. If we want a different result, we need a different Govt. policy. Labour has failed with their more control, and National with their less control. None of them want to implement the right control.

.

.

the level of incompetence of our government in relation to housing crisis is beyond any scale! How is it possible that they houses are increasing $500.000 ....$1.000.000 in 12 months and people are getting away without paying a penny! At the same time hard working people getting tax increases....

I will not even mention housing affordability as this is simply gone. And it looks like it is gone forever and government did absolutely noting to stop it, even opposite!

I'm glad they acknowledged the facts, revaluation of property is our economies leading 'industry'. People perpetually predict a crash in property but RBNZ and Government will never allow that to happen. They are as beholden to the status quo as any government before them.

How is 30% increase in one year the status quo?

For more than a decade New Zealand has failed to sustain an inflationary environment without asset prices growing at a much higher rate than wage or CPI inflation. The larger the debt burden the faster we need asset prices to inflate so we can sustain CPI inflation. If you think 30% is a big jump wait until the next recession.

Because it's UP. As long as house prices go UP, it's fine. They can never ever go DOWN.

House can never be economy, if it can, the economists wouldn't give any warning couple of days ago. It's also a silly statement that treasury made about slowing house growth means slow economic recovery. As matter of fact, the high housing price could be one of the reason that we were heading into recession two years ago. Households just don't have as much disposable household income to spend. If we continue this path, stagflation will be our destination.

https://www.interest.co.nz/property/110262/according-reserve-bank-it-no…

Hahaha let it go baby, money for jam. This government is pathetic, but hey, they making me richer and the poor they say they care for so much worse off then they have been for years,. They hand out $50 bucks but screw them on the other side. Sadly most of these people think they getting a good deal

I wonder how much damp housing has slowed economic recovery...

You mean people not able to open windows anymore? I'm not sure it does at all. In fact the mould removal, sickness, curtain replacement, painting all adds to GDP.

So from from an economic perspective it's a positive mate!

We found it difficult to open the windows during the day when we were renting, as we'd leave for work 6 am and get home 6 pm. Wiping down the windows every morning didn't remove the need to clean mould off the ceilings and the curtains every couple of months.

The landlord could have added to GDP by installing window stays, but refused to do so.

Maybe instead of free lunches the govt should be giving every tenant a free dehumidifier

Unfortunately, while a dehumidifier might help the windows, it can reduce the indoor humidity to less than 40% which then becomes bad for people.

Dehumidifiers have humidistats. Like a thermostat, they switch the unit off when it reaches the set point

My point is, to reduce the dew at the window interface, you have to lower the room humidity and/or increase room temp, into a range that is bad for human health.

Best window detail will allow an indoor temp between 20 to 24C and 40 to 60% RH, without any condensation on the window.

It's sad to see New Zealand's economy is fully relying on housing market now. Even Treasury thinks a slowing house price growth will result in a slower economic recovery. I think the government and most of parties have lost the focus to make New Zealand a prosperous country.

If a slowing house market leads to a slower economic recovery then they are measuring the economy wrong. If anything, increasing house prices are a risk - a gamble that interest rates will not rise substantially in the next 10-20 years. If they do then the economy will be stuffed. But how can this be if house prices increasing = 'good' for 'economic growth'!? There must be some very short term thinking going on.

A simple example - if an unmodified house sells for double what it sold for last year, has anything of value been created? Of course not, it is inflation. There is no 'economic growth', just more money borrowed into existence and more unmeasured inflation.

Yes, but it is not just inflation. It is also an utterly unjustified and highly counter-productive on-going transfer of wealth from the productive sectors of the real economy to a parasitic self-serving minority of speculating landlords.

What % of our GDP is residential construction? in Ireland before their crash it was 7%, I wonder if we are beating them.

Not sure but it seems NZ govt is working overtime to cause an oversupply. Just wait till conditions arise than unleash a ghost house sell-off, combined with completed new builds. More houses than people will know what to do with

Can't wait! I just hope they have the unemployment insurance scheme set up in time to catch all my builder mates that will become unemployed.

Most of the builders I know are self-employed so Government unemployment insurance is unlikely to help them. They should consider private income protection insurance instead.

Found it! GDP from 'Rental hiring and real estate services' is nearly 2x as much as Agriculture!!! This is scandalous. It is true that real estate IS our economy (data at 2019).

https://www.stats.govt.nz/tools/which-industries-contributed-to-new-zea…

It looks like 3 of the top 4 GDP industries in 2019 were related to real estate - a massive shift if you take the slider back to the 1970's or 1980's.

Sorry, pressed the wrong button and reported.

Just wanted to say great charts. Thank you for posting.

Treasury has predicted house price inflation will be under 1% but they didn’t consider the tax impacts of interest deductibility.

Your article assumes Treasury’s forecast for house prices does include the impact of interest deductibility.

See B.3 | 23 of the Budget Economic & Fiscal Update 2021 which states;

“The forecasts incorporate Government decisions and other circumstances known to the Government and advised to the Treasury (up to 30 April 2021). The main exceptions to this are the tax impacts of interest deductibility of the recent housing announcements & impacts of recent health reforms. Neither of these matters are reflected in the fiscal forecasts as not enough information was available to reliably estimate the fiscal impact from these policy changes.”

The government deliberately delayed the announcement so Treasury couldn’t model the impacts. The forecasts of course are not worth the paper they are written on.

What’s more is B.3 | 55 states there is unchanged risk to “increases to market rent”.

It is obvious that the changes that the interest deductibility rules will result in significant increased pressure on rents and emergency accommodation.

It is laughable that on p 16 | B3 that under downside, upside & main scenarios for Covid-19 outcomes that unemployment in all 3 scenarios in June 24 & June 25 converge at about 4%.

Wealth effect is one of the biggest neoliberal falacies. People are meant to spend what they don't have, is that supposed to be the best we can do for our economy? Most likely not.

Maybe the New Zealand Herald should 'Trumpet" louder so that the Government and its Financial mishmash can hear and learn to read our Newspapers.

https://www.nzherald.co.nz/business/warning-mortgages-could-see-56-per-…

This is not what I hope will happen, but I am afraid the Banks may have 'Bought" it on themselves. Plus of course the borrow till you drop Brigade lead by ORR will wake up to the real World.......it ain't all Free......it has to be repaid.....even when there is not a drop in the ocean of dire House speculation....yet. 56% is repayment needed......not the "bleedin Profit'. .......Read for yourselves....Not the Builders, Orr, Real Estate Agents, nor Jacinda/Grant wasting my hard earned money on Motels and Speculationists.

https://www.msn.com/en-nz/news/national/accommodation-supplement-ends-u…

Shock ..Horror......Can One Take Supplements to fix all ills.....in a sick market. Orr will...."Leverage" for ever and a Day be continued...in the"""""""""""""""" Housing Market""""""""".Watch this space.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.