Any wannabe home owner, particularly a first home buyer (FHB), will tell you at length what a struggle it is to get a deposit together to buy a house.

But even they might be a bit gobsmacked by the rate at which it has become even more difficult to get a deposit together.

In material prepared for its latest Financial Stability Report (FSR), the Reserve Bank has produced some eye-watering figures that show just how quickly the deposit requirements shot up in the closing months of last year.

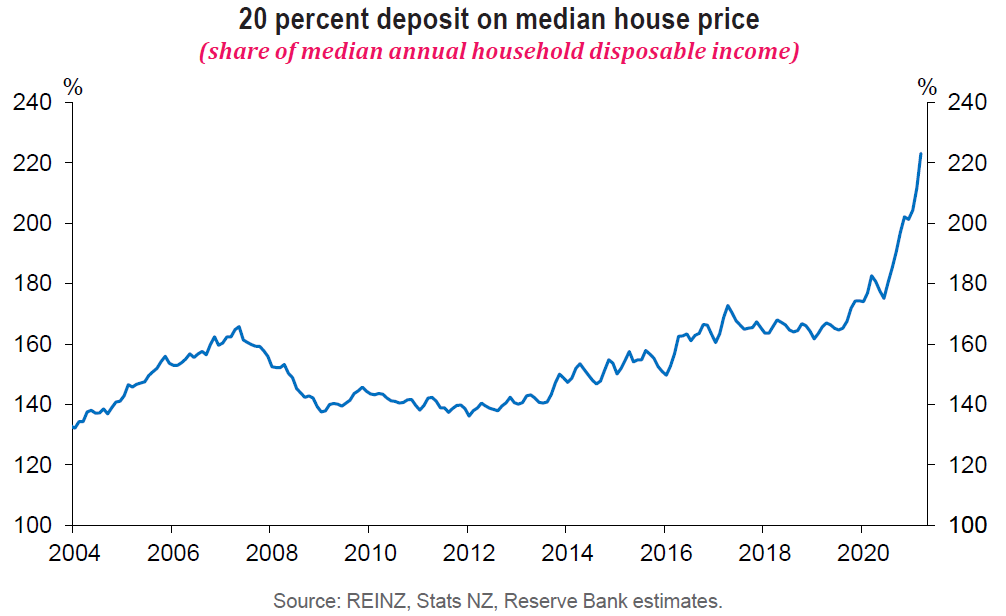

According to the figures, as of the end of June last year it would have taken 175.2% of median disposable household income to get together a 20% deposit on a median priced house.

By the end of November that percentage had shot up to over 200%.

And by the end of March the figure stood at 223.2%.

Needless to say the 223.2% ratio is very much a record high in figures that go back as far as 2004.

And the figure represents a real break-out from where we've been before, with the ratio of disposable income to deposits having previously hovered in a range between 130% to 170%.

In the FSR document the RBNZ said New Zealand house prices "appear stretched by several metrics, such as house price-to-income ratios and the affordability of entering the market" - by which they refer to the disposable income to deposits ratio.

"The question of house price sustainability has two parts.

"Firstly, are prices deviating from levels implied by their drivers, including both cyclical supply and demand factors and longer-term fundamentals (such as land-use restrictions, tax policy, and global neutral interest rates)? If so, this could signal that houses may be mispriced.

"Secondly, are underlying house price drivers themselves on sustainable paths, and how might they be expected to change?"

Still, it might be said that every cloud has a silver lining - particularly if you have managed to drum up the deposit and are already now in a house.

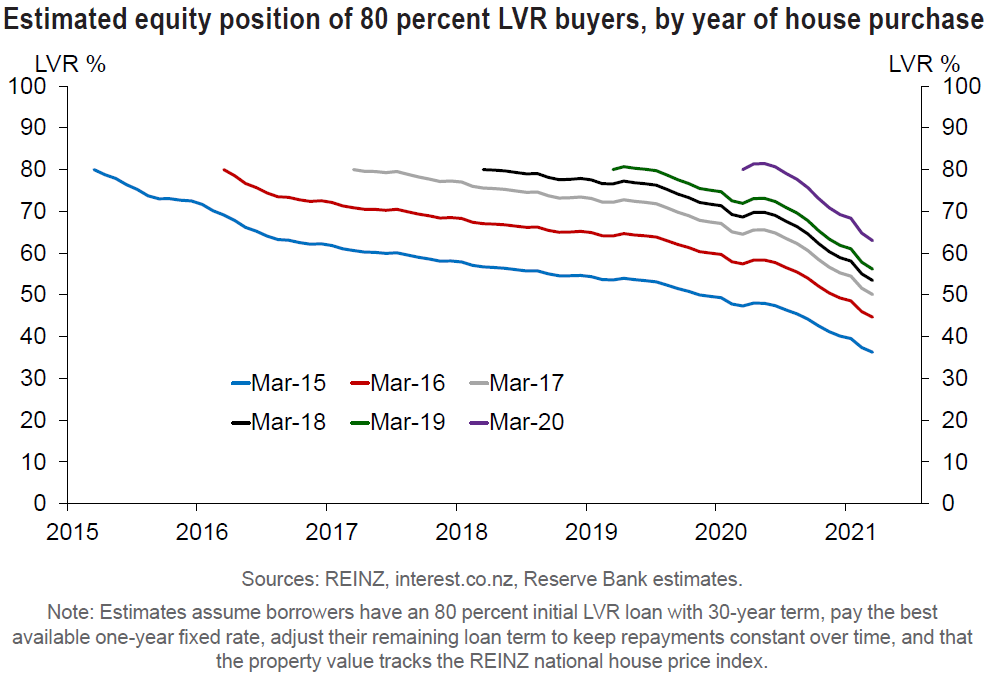

Separate figures produced by the RBNZ for the latest FSR show that someone getting into their own home in March 2020 with a deposit of 20% - so 20% equity in the property - would have grown that equity massively to 37% by March 2021 and therefore be comfortably above water in the event of any downturn.

Going back a little bit further, to March 2015, somebody putting a 20% deposit down then would now, according to the RBNZ figures, have just under 64% equity in their home.

So, rising prices are pretty good once you are 'on the ladder'.

Getting on the ladder at the moment, however, seems to be a different story...

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

63 Comments

..... and they’ve only just realised?!

Sounds like a nice way of saying - it now takes mum and dad to fund your 20% deposit for 99% of punters not on the ladder.

Or another way of saying it might be - here, eat this shit sandwich we've created for you.

Labour: driving inequality since 2017 (with help from Mr Orr).

#FourYearsOfNeglect

Well Jacinda did say that she wanted to see house prices keep rising ad infinitum. Finally our fast talking, disingenuous, hypocritical leader has found an undertaking that she can fulfill.

One could certainly picture Treasury and Reserve Bank shouting "YOU SAID THE QUIET PART LOUD!!!" when she repeated that sentiment. This model of transferring wealth to asset inflation has been the norm for the last decades and we've only had tinkering and pretense of addressing it from anyone. John Key campaigned on it and abandoned ship; Jacinda Ardern seemed to do similar (if with some conciliatory efforts with the recent tax move).

It seems we need Treasury and Reserve Bank to also admit that the "wealth effect" philosophy is bunk, and the model of transferring wealth to assets is not one that helps make NZ society a better place.

Everyday news / data suggest the need to target Speculative demand to contain the ponzi...still Mr Orr is playing around and supporting speculators by not banning Interest Only loan to investors with filmsy excuses and reasons.

Interest Only Loan if not the only contributor is a Major contributor, along with low interest rate. Interest rate cannot be raised but interest only to speculators can be stopped.

Mr Orr should go for a long leave to help NZ.

You can almost pinpoint to the month where the fools at the RBNZ screwed the pooch with their idiotic policies.

They broke it, now they should own it and resign.

Except for Bascand. His performance yesterday for the FSR oozed competence.

Agree heads have to roll.

" it seems to have become accepted that a median multiple of 3.0 times or less is a very good marker for housing affordability."

https://www.interest.co.nz/property/house-price-income-multiples

And yet now that is more like the measure of a deposit (x2.2) - let alone paying for the actual mortgage!

Yes indeed, the new measure of affordability will be exactly as you state, deposit amount should be under 3x median salary. All loans to be interest only. That will "fix" it as we can all then be perpetual debt slaves.

Then the Ministry of Truth will tell us that is the way it has always been.

Time for evaluation, processing, waiting is over.

Robertson should put a full stop to all the nonesence and just go for DTI and more than DTI should stop interest only loan immediately for new application and existing loan can be phased out just like he did with Tax Change.

Not to forget that they did introduced FBB despite Bill English denial and lie.

Where their is a will their is a way.

If Mr Orr has to go, so be it. He has done his time and time for fresh outlook

100% agree.

FBB is laughable, carve outs for Aussies, Singapore, no restrictions on non-resident Kiwis and the recent pump has happened in spite of it. You're up in arms about Bill English who hasn't been PM for three years but have nothing to say about the current government who have seen prices rise faster than at any stage under National during their reign. Talk about choosing your battles.

'Only Labour has a comprehensive plan to solve the housing crisis' - Labour, 2017.

by Audaxes | 1st Feb 21, 4:10pm

ANZ has cut its Serious Saver account -5 bps so that the top potential rate is now just 0.20%A $5,000,000 deposit to save $10,000 annually - a signature example of how to part the masses from the capacity to gather capital to meet expenses and save for assets.

I moved some funds out of a "bonus" savings account yesterday through Internet Banking. A screen saying "Are you sure? You'll miss out on the bonus interest rate for this month" popped up. For the life of me I couldn't find the "HAAAAHAHAHAHAHAHAHAAAAA!...Bite me" button.

They are taking the proverbial mate.

Once upon a time house prices were 3 x Income, with TD rates at 15%.

$60k salary, work on $6k per year savings capacity, $200k (3x salary rounded) vs $800k house today:

1) 20% deposit on a house @ $200k with 15% TD = 5 years to save, $30k of own money & $10k interest.

2) 20% deposit on a house @ $800k with 0.5% TD = 13 years to save, $78k of own money. $2k of interest.

All the talk about "houses are so much more affordable today" is not wrong, but no FHB is complaining about the cost to service the mortgage.

Agree in principal but that $60k salary worker wouldn’t be earning $60k when house prices were averaging $800k

What would they be earning?

I've plucked a modest salary for today, applied some house price to single income ratios and relevant term deposit rates at it.

If you are comparing how long it would take a single person to raise a 20% deposit on $60k today compared to when houses averaged $200k (probably back in the early 90’s) then you have to also use the average salary for that time period which would be much less than today’s $60k

If you are comparing how long it would take a single person to raise a 20% deposit on $60k today compared to when houses averaged $200k (probably back in the early 90’s) then you have to also use the average salary for that time period which would be much less than today’s $60k

You're right of course, but when you do that the numbers are pretty close to NZDan's back of the envelope calculations.

1998: Median house price 165000, Median full time wage and salary earnings: 26,936. Years to save 20% deposit: just over 6.

2021: 800,000 (or thereabouts), 55,120. Years to save 20% depost: 14.5

Of course, this doesn't take into account interest, and house price inflation. Interest clearly falls in favour of the 1998'er. House price inflation? We'll have to wait and see.

Don't worry, there's always an excuse why actual, measured statistics aren't right or don't apply. Usually it's iPhones or cafe breakfasts or some other garbage - everyone these days is just lazy.

It's the overseas travel, alcohol, SKY, and eating out accumulated over 10 years. Real life example; Male friend earning $100k incl commission, plus company car (turned 50 this year), renting same 3 bedroom house in Avondale for 15? years. Every year the family goes overseas, Fiji, Rarotonga and even an LA Disneyland trip. I estimate he spends $6k/yr on travel, another $1k on SKY, and most weeks there is a dinner out for the family ($120/week, $6k/yr). This is >$130k in todays equivalent dollars over 10 years. He could have had his kids bunk in the same room when they were young and saved some cash by renting a 2 bedroom place (vs 3 bedroom). No longer practical as they are now teenagers and M and F. A bit of belt tightening and cashing in his Kiwisaver and he'd be in his own house. Now he is screwed, like a lifelong smoker complaining about lung cancer. Irony is he and his wife still use a personal trainer and wear nice clothes. Guess its just a different set of priorities.

Have I told everyone about my 2002 Honda Jazz? Fits right in when I have meetings in Parnell :-)

Its totally about priorities when your on that sort of income. Some people simply cannot pull their heads in, see it all the time its just a personality trait. Yes still driving a 1990 car and a 2004 car here but on the flipside the house looks like it just hit the $1mil this month.

Do you honestly think though, that despite the stats above, that the main reason that rates of home ownership have dropped, especially amongst younger people, is that younger people in general are a lot more frivolous with their spending than they were in the Nineties (and before)? Or are you just trying to make the point that for some particular individuals, it's not house prices that are the problem, it's overspending? If so, I don't think that's a new phenomenon.

And if we're bragging about our frugal transport habits, I reckon 'my feet and my bus card' trump your 2002 Honda Jazz.

Remember back in the good old days when a house was around 3 x the average wage and interest rates were double digits?

People back then couldn't even save the equivalent of 2 - 3 years wages to pay cash for the house when term deposit rates were 15%, instead they rushed out and borrowed money at 22%. Fast forward to today, it's not uncommon for a deposit alone to be 2 - 3 years salary and term deposit rates are 0.5%.

Not really that must be before my time because when I started looking I couldn't even afford an apartment so its never been 3x it was more like 5x. By the time I did purchase it was like 7x with interest rates at 8%. Sure its only got worse but so has all the crap thats out there to buy now and people think nothing of jumping on a plane for overseas holidays and that just didn't exist back in the day. Expectations these days are through the roof. I think its impossible for the current generation to imagine a black & white tv, no cellphone and no computers with takeaways only on Birthdays and one car in the family.

I suspect most older folk must be rationally aware that the argument is bollocks, but perhaps are emotionally wedded to the idea that their wealth is only of their own doing. Even lottery winners begin to believe their wealth came through their own merits.

The numbers don't lie.

The great NZ wealth effect

This a 'wealth effect' that the taxpayer pays for and where the national debt grows at an exponential rate daily.

Meanwhile the likely decision to convert the Marsden Point refinery into an import terminal is going to cost 3.5k jobs to Northland.

Inexplicably high power prices threaten to kill off the few remaining productive enterprises in NZ.

The government could potentially redeploy all those factory workers to produce ink for RBNZ's printers.

https://www.stuff.co.nz/business/121939523/ending-refining-at-marsden-p…

"Let's do this! Let's wreck New Zealand!"

Labour just let F&P Appliances leave the country all those years ago and thousands of jobs were lost including mine so what's really changed ?

The graph in the article above makes it look like the ratio of deposit required to purchase a house peaked under Clarke before falling away under John Key and has spiked up again under Jacinda Arden!

.

I'm neither a Key or Ardern fan, but to be fair it appears to be rising under Key. And the GFC in 2008 played a part.

Key and Ardern are cut from the same cloth. The only difference is that they use different tactics to push emotional triggers.

At worst you can say it only fell slightly over the course of John Key’s term, then rose slightly under Bill English before shooting for the moon under Arden.

The only reason it stopped rising under Clark was the GFC - unless Labour is going to somehow claim credit for the worst financial crisis this country has faced since the Depression, unless you count the current one they've foisted upon us.

That's a lot of avocado toast and lattes...

That won't cut it.

At this stage, if the Government wishes to do something, they could get NZ Blood Service to start compensating for blood donations. That could help more under 30s get closer to the fleecing dream of saving up a deposit for a house in NZ.

"...closer to the fleecing dream..." - typo or Freudian slip?

Two-bed townhouse in Stonefields sells for more than $1.2m https://www.oneroof.co.nz/news/39385

'The 87sqm townhouse last changed hands in 2015, for $735,000, handing the vendor a profit, on paper at least, of nearly half a million dollars. The sale price is thought to be one of the highest for a two-bedroom townhouse in the suburb.'

Deposits are easy when you make a profit of almost double the house value in 6 years.

Insane. And ultimately if it all falls over those gains are in the bag while the NZ taxpayer will be left holding the bag.

I can't believe young people are taking this stomping by Govt and RB lying down and instead are out protesting climate, rascism etc. You will have a problem with the climate, alright! - when the rain is pouring in and blows your shanty town shack corrugated iron roof off because you were too busy virtue signalling to oppose real estate increases

It's a weird condition of the human mind alright.

We have some of the highest house prices, poorest quality of housing, highest asthma rates, leaky home syndrome, mould etc. and barely a whimper from those affected, and nothing from the Govt of the day to solve it.

Yet, climate change, zero-carbon etc. then let's shut down our coal mines and import it instead, and heap extra taxes/costs on people.

And it does not even occur to them, that if they enacted policies that enabled affordable, quality, energy-efficient, healthy homes to be built, then they would already be halfway there to mitigating climate change.

Speaking of importing coal, I still chuckle on the brilliant plan from Ardern/Robertson of replacing high-wage jobs in gas extraction, reticulation and power generation with a $100k green hydrogen business case and cycle tracks in Taranaki.

The concept of conservation has been slowly replaced with abstract ideas of wellbeing and sustainability. An almost quasi-religious belief that army of eggheads is going to save the world when once its all magically 'unveiled'

Well some are stacking BTC,ETH,DOGE as realize the game is so rigged might as while swap the fast depreciating FIAT for something harder. So when the inevitable crunch comes (on the horizon now) they will be in a much happier place.

Young people marched for climate in a massive protest, the biggest in decades.

Government did nothing. Claimed they cared, did nothing.

Government claim they care about the housing crisis, but do nothing.

Most young people I know have now checked out of pretty much all civic society and now don't care about the government. Many don't vote for this reason. Easier to play games in shacks and gamble on bitcoin. And why not when the government cares not for your future, yet claims they do?

This is true. Peaceful protest doesn't achieve jack sh*t.

Unless you are causing major disruption to the country or flinging molotov cocktails the powers that be won't give a rats.

Everybody should have a portion of their savings in crypto.

I'm surprised there hasn't even been low level disruption yet.

For example, we see defacing of political billboards all the time, but there are plenty more real estate signs out there that are never touched. Peaceful protests could easily disrupt auction days and venues. No marches, no protests, no minor stuff...

Perhaps they don't actually realise how much their wealth is being transferred to the older generations who have castigated them for eating avocados.

I can't believe old people are expecting the young to shoulder the weight and not doing anything about it themselves.

Maybe the young believe the issues of environmental degradation, racism, classicism etc are more important than the conditioned belief in the bullshit story of material wealth. Maybe they have a better understanding of value and respect - towards the planet, towards people, towards life.

Are you buying overpriced property and expecting to sell it for more? Are you marching down the street demanding that security of a home should be a right and not a privilege? Are you putting energy into being the change or are you expecting others to solve the problems? Are you questioning your own conditioning?

Too many are too busy shrieking at even paying a little tax on the wealth transferred to them via property, or too busy pretending they never bought for capital gains so don't have to pay tax.

Book I am reading states uk wages rose 30 fold in the 50 years to 1962

House prices? 90 times

The power of monetary inflation and how property ownership is the bastion against it.

I hope they patch your NPC script with some new material.

Good luck defending it

Is labor doing it intentionally or it is full of retards?

Who spend there major part of life as financial experts & still doing these debacles.

Still whatever, the common sense says if you have done the mistake, accept it & try to correct it. Oh sorry common sense is for common people not for these idiots.

nevermind, interest rates will go up at some point - seems to be starting already if I look at the US 10yr rate, not to mention inflation, it's already here - from school fees, restaurants, cars, groceries - its everywhere. There will be winners and losers sure, but hopefully we get back to capitalism and not the state sponsors mess we have have now. Governments shouldn't pic winners and losers.

Yes, hopefully, but we are nowhere near Peak State. This has years to run.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.