By Shamubeel Eaqub*

A long-running crisis

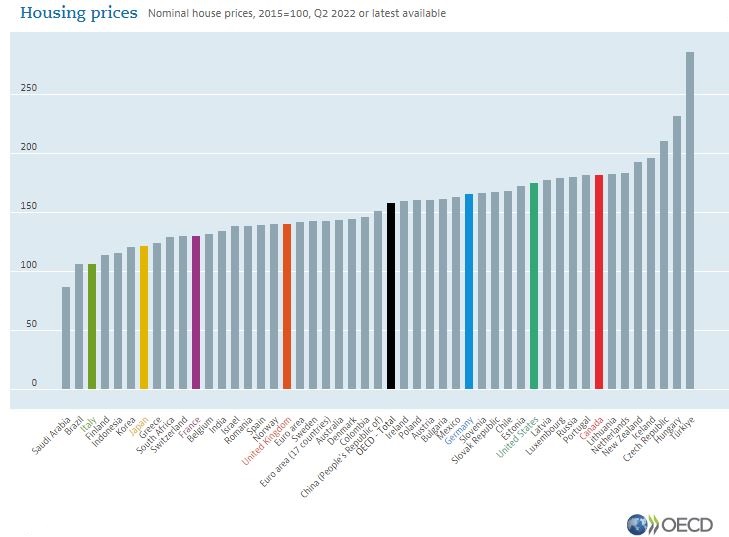

New Zealand has a long-running housing crisis; house prices have outstripped incomes since the early 2000s, increasing from four times the median household income then to over eight times now. Unaffordable housing used to be confined to a few urban centres at that time, but now most of New Zealand suffers from it.

The COVID-19 pandemic uncovered three additional housing policy priorities for New Zealand. First, that our banking policies need to be much improved to avoid further housing bubbles like we saw in the 2008 Great Financial Crisis.

Second, borrowers need longer mortgage terms for a long-term purchase.

Third, housing supply needs to be specifically targeted towards low-income and vulnerable people, instead of just waiting for it to filter down through the continuum. These are in addition to fundamental policy efforts to reduce barriers to housing supply; improve funding and financing for infrastructure; and implement broad-based taxes on land or capital gains. Without these measures, housing will continue to cause enormous hardship and potentially create political and social fault-lines. A local case study shows this well.

Rotorua - from promise to not fit for purpose

Rotorua is a district of a little under 80,000 people. It is famous for tourism, geothermal, recreational sport and Māori cultural attractions; it is now also infamous for its housing crisis, which worsened during the pandemic.

Rotorua’s population barely grew in the decade to 2014, increasing by an average of just 50 people per year. But between 2014 and 2020 it surged to over 1,200 per year, driven by strong inward migration attracted to local job opportunities in tourism and wood processing - and affordable housing.

But housing supply didn’t keep pace with the sudden surge in demand. Prices started to increase soon afterwards but really jumped through 2020 and 2021. At four times the annual income homes had been affordable, but as more people arrive they have now risen to nine times that. Rents also used to be manageable - around 25% of a renting household’s income - but as the housing pressures grew, they too rose sharply and now account for 40% of income.

Despite strong growth in population and rents, slow new housing supply meant the number of rental properties fell in the district, taken up by owner-occupiers. Rental stresses got so bad that the waitlist for social housing ballooned from 49 households in 2014 to 1,104 in 2022; many on the waitlist are being housed in motels. While this was a quick solution during the pandemic - with tourism accommodation vacant and the borders closed - it is now not fit for purpose and proving difficult to unwind with nowhere for these people to go.

Housing supply is needed across the continuum

New housing supply is ramping up but it will take years to clear the backlog: if it remained at the current historic highs it would not be sufficient to house the poor and vulnerable until 2030, even if population growth flatlined. There is also community backlash to new social housing supply, even though without it housing stress will worsen.

New Zealand has enacted a swathe of policies to increase housing supply: the unitary plan in Auckland; the National Policy Statement – Urban Development; and Medium Density Residential S (which essentially bans single family home zoning in large urban areas); reform of the act that oversees urban form; review of local government funding and financing; and clarified rules for the build-to-rent sector.

But long-term improvement in housing supply alone will not alleviate the existing acute stresses the sector faces. Rotorua’s experience shows that there must be concerted policy efforts to increase housing supply across the continuum, including rentals and social housing. Currently, government intervention is mainly focused on subsidies for housing assistance - roughly 70% of non-homeowners receive them - but they are not co-ordinated with other policies to actively promote supply of rental and social housing. Stresses in these parts of the continuum have increased even though housing subsidies now make up NZ$4 billion, or 4% of government expenditure.

Subsidies cannot work on their own. We also need other policies, such as inclusionary zoning, to direct a share of all new supply towards affordable homes, and a long-term, apolitical programme for social housing.

House prices have been egged on by too much lending

The Reserve Bank of New Zealand gave itself a clean bill of health in its pandemic response. But it did not address the role of easier lending criteria, which helped increase house prices by 40% in the first two years of the pandemic.

Loosening of criteria for buying second-hand homes was wrong. New Zealand’s central bank should have made its cheap and plentiful money conditionally available for consumer and business credit, which were the most affected by the pandemic. No houses died from COVID - but business failures and job losses were the greatest economic casualties.

The central bank is still stuck in a 1980s time warp, unwilling to countenance directing how credit should be allocated and instead trusting private banks to assess risk and opportunity. The experience of the last three decades, when more and more of bank lending has gone to residential mortgages at the expense of lending to businesses, proves this to be a fallacy. Oversight of the central bank - as well as its regulation of the private banking sector - need to improve.

Recent mortgage borrowers have been exposed to more risk

The recent surge in inflation, and the sharp increase of interest rates to deal with it, has exposed the extent of the risk faced by homeowners. During the pandemic, many people were offered one- or two-year fixed-interest rates of less than 3% for a 30-year mortgage; now they will need to refinance at rates over 3%. If someone is borrowing for this amount of time, interest rates with terms lasting a maximum of only five years are not fit for purpose.

Even through New Zealand’s banks are some of the most profitable in the world, they have not innovated to meet this need from consumers. Policy makers need to work with the sector to change the mortgage market norms; rather than only borrowing for up to 10 years, the government itself will also need to borrow longer term to create a local market for such bonds.

Longer-term fixes

New Zealand is currently amid the biggest housing policy reform programme since the 1950s, looking at a broad suite of policies to increase land and housing supply and dampen demand. The policies are not yet cohesive nor co-ordinated, but the government - and its opposition - are increasingly of the same mind: pull many levers. Many aspects of the programme started under the previous regime, and there is every chance that many (though not all) of these policy reforms will be enduring. While this progress is positive, the pandemic years have highlighted that urgent additional policies are needed to avoid another generation of renters in New Zealand.

*Shamubeel Eaqub is an economist at Sense Partners. This article first ran here on the OECD Forum Network and is used with permission.

**Eaqub recently spoke in interest.co.nz's Of Interest podcast on why he's optimistic about the housing market.

37 Comments

+1 to a sea change needed in residential lending, be it longer periods of loan fixes or even a cap on the length mortgages can be offered for. The shift from 25 to 30 year mortgages happened so quietly you might have missed it if you weren't paying attention, but it helped smooth that affordability speed bump out just a little longer. It could be that there also needs to be some discussion about the limits of break fees or minimum voluntary repayments to help make it easier for those currently facing a life-time of work to pay down a starter house mortgage have a way out of purgatory.

Shamubeel has been saying this stuff for years - he argued houses were overvalued and strongly advocated to rent instead of buy back in 2012.

In 2012 one of my properties was valued at $325000. Now it is $1300000. Who was right? Sham to say it was overvalued then, or me to think with any sort of inflation, it's dollar value could only go up. Let's see, $975000 gain in equity. Looks like a clear loser here.

The clear losers are those that you rent to. And people wonder why we have a crime problem. If you have no stake in society there is nothing to lose if you commit a crime. With our personal selfishness we have created a society of have and have nots. How about Luxon send landlords to a boot camp to learn the error of their ways. They may not be breaking any law, but their moral compass sure is way off. Won't be long till we have razor wire fences to keep the poor from robbing us. Sheesh.

Landlords just need to realize that more of them doesn't mean better outcomes. Maybe we should change the title, the whole "Land" "Lord" thing is attracting too many undesirables.

True. Folk born at the right time may have done well financially, but society did poorly. So now they must fear the social outcomes we've created.

Sell at a low price to someone in need, yeah nah greed. No one needs more than 2 houses.

And yet once he had a child, he figured out why some people don't just base their purchasing decisions on what returns the most money - there is a pragmatic aspect: especially then, it was all to easy for a renter to find out they were homeless in 6 weeks. Which can be a bit scary when you have kids.

Like a local Fannie Mae / Freddy Mac setup......

Thats going to hurt bank profits.

Bring in 25 year fixes limited to DTI of 4... oh yeah this could have wheels, Maybe thats a way to get it in, sure you can borrow DTI 8 but only fix with banks for 5 years max, or borrow 25 years fixed but only at DTI 4 ish....mmmmm I actually like this, but it reeks of Labour policy not National.

imo the Govt needs to buy up large tracts of land,recreate the MOW and get building and keep building.If they really have the interests of nz citizens at heart then this should happen.

Its a long term investment in the people that will pay off in spades for future generations.

Don't worry, they're building 100'000 affordable homes, that promise got them elected!

They should have taken land from land bankers under the public works act and got on with it like a proper socialist government.

It starts with Councils and their 100 year plan, where are the next bedroom communities going to be?

Approximately every decade a new suburb needs to be opened up along with roading and three waters infrastructure.

This is what councils are supposed to do.

Councils' job is to look after their ratepayers' assets, not be social workers. I don't pay my rates to be wasted on stuff central government should be looking after.

I'm alright Jack.

Nothing social about Councils expanding their boundaries - generates development revenues from new sections and increases the asset base with roading and infrastructure (3 waters, power etc) assets.

There's a whole lot of existing land already developed they could simply stop preventing people from building more on, too. Without as much expense of maintenance, thus rates rises.

Time to extend mortgages to 40 years

That encourages the unaffordable to look more affordable while increasing interest debt. The property party needs to stop.

How about no recourse mortgages as applied in the USA ? Force the banks to have skin in the game & the risk will moderate excess lending & behavior.

Combine that with the USAs hands off building regulations outside cities & towns. Encourage off grid, tiny home etc. Not everyones a fan of neighbours.

The average home price in the US was less than USD400k (last time I looked).

Yes, it's like people can't do simple housing maths.

All savings in a system are captured by the most restrictive parts of that system. So any saving a longer mortgage term might initially give a purchaser will automatically go to increase the land(if it is restricted as it is.) price within one build cycle. And since property can be leveraged, then that saving acts as a multiplier. EG saving 10% per annum, cost of house purchase will increase by a $ multiple of that saving.

To say, 'the USA' is too general in that you have States like California that are just as much a housing basket case as NZ is, and then you have Texas which is more what you are referring to.

Really good article - the criticism of RBNZ and oversight the key point for me. In the old days of US Regional Federal Banking, the regional Fed banks were charged with making sure that credit was allocated to productive endeavours - things that benefited the community, created jobs, etc. Let's get back to that.

'New Zealand has enacted a swathe of policies to increase housing supply: the unitary plan in Auckland; the National Policy Statement – Urban Development; and Medium Density Residential S (which essentially bans single family home zoning in large urban areas);'

NO THEY HAVEN"T. yes they have enacted policy, but they don't increase supply in excess of demand in real-time.

The simple logical theory of what they are trying to do shows that this is not correct, and more importantly, the results in practice show they haven't. Prices have continually increased due to internal policy decisions until external policy decisions overran them.

Simply, all that policies like the UP did was highlight to the speculator and land banker market which land was next up for development, and it allowed them to buy and hold monopoly control over a smaller parcel of land within the greater RUB. IE it actually created more restrictions.

These restrictions create an artificial 'next best economic use' above what the land could have been purchased for in a less restrictive market. In fact, this artificial use makes it more profitable just to sit on the land instead of even farming it, or building on it.

To suggest that subsidies are thrown at it and inclusionary zoning is used only feeds the beast and prevents what really needs to happen next.

Just as spending billions on the pandemic has only exacerbated the present problems, so will trying to prop up this bubble.

There is no jurisdiction in the world that has successfully via policy unwound a housing boom, without the pain we are going to go through.

The only choice they have is to jump or be pushed. It's time to pay the piper.

All the talk NOW should be what we do when we hit rock bottom, in that, we then should be enacting policy that keeps houses at the new more affordable level and prevents another boom and bust cycle.

There is no jurisdiction in the world that has successfully via policy unwound a housing boom, without the pain we are going to go through.

Correct. But the sheeple has been led to believe we're diff'runt (similar to Australia).

Remove restrictive zoning, remove yield and price welfare subsidies, and rebalance LVT and income tax and we'd see some pretty useful movement.

With the high proportion of vacancies in my area, it doesn't feel like lack of housing supply... it's more like lack of willingness to make that supply available the buying or rental market

Hey Sham. Did you ever buy your own house, or are you still renting?

Great article…

The headline would read..."Crown to seize and carve 9000 odd acres out of the Waitakere reserve" and import/build/transport 70,000 2 bed transportable designs on 1/8th acre sections... Those interested apply for funding privately and settle with Crown... further details to follow... Limited number (10,000) of bare sections available 90k (900M) *Conditions apply....'Well that has fixed that problem'...said Les Jus'doit the Department of Problem Fixing chief executive spokesperson....In other news today protestors have gathered outside the Department of Problem Fixing dressed as trees and shrubs...Les Jus'doit spokesperson was heard trying to explain to those gathered that the proposed designs were solar powered and very eco friendly with contained sewage and water tanks , the crowd was seen to be pelting him with battery hen eggs...lol

Over and again Shlemiel and others like him come up with the worn out old argument that banks should concentrate on businesses rather than on houses.

It may come as a huge shock to him to know that banks are very risk averse and far rather lend on houses than on businesses. Houses and land are for ever while business can go bust over night. An empty house is still a house plus the land, while an empty business is just papers and junk.

Also Shambil forgets that most banks want property as security for a business loan with only the most successful long term businesses obtaining loans outside real estate.

It may come as a huge shock to him to know that banks are very risk averse and far rather lend on houses than on businesses. Houses and land are for ever while business can go bust over night. An empty house is still a house plus the land, while an empty business is just papers and junk.

Which is like saying that property bubbles are preferable to economies based around producing goods and services. Would be interesting to know proportion of bank allocation to productive enterprise from the 50s-80s (before the banks became primarily purchasers of debt securities based around housing and consumption).

Put another way, houses are way less risky than businesses. What do you expect banks to do?

Banks run on OPM and cannot afford to take chances.

A banks assets are its customers debts so there is far less room to move in any downturn!

It’s amazing that many people, including Shlemeil, think that banks are siting on piles of cash that belongs to them to do whatever they wish to choose.

Well I dunno, a DTI against residential property investment does make it a bit more risky. $30k rental income at a DTI of 5 = $150k mortgage.

You're correct, the banks are not sitting on piles of cash they've already shoveled those offshore and divvied those out. We should see ANZ's payments 15 December?

The problem is LLCs and bankruptcy law make debt on business non-recourse, in too many cases.

So make mortgage debt non-recourse too, and that'll fundamentally transform property speculation vs. productive business in NZ.

Absolutely spot on article, well stated. Need government (of all shades, not only the current one), central bank and retail banks to really take all this onboard. The upcoming crunch is actually the perfect opportunity to get hard stuff sorted out

Bang on. What we need is - to start:

1. All parties to accept affordable housing is vital for kiwi quality of life (govt should have a target for a house to be a max multiple of the median income for location)

2. a full on CGT (without bright line dates etc) on property.

3. A focus on promoting alternate investment options for people - like the UK ISA's. Mandatory Kiwisaver contributions.

4. A revised immigration policy - focussed on getting high quality talent that contributes enough $ to pay for infrastrature and public services

5. Maybe a restrictions on number of properties that can be owned by an individual or company.

6. A focus on social house building as a % of population. This is one thing that should be entrenched so governments cant sell housing stock and need to keep it updated.

7. A minimum number of house builds per council per year - tied into immigration settings. if immigration grows house building must grow or people arent allowed in.

Sounds socialist - but really is no different to restricting foreign ownership of NZ assets and properties - as its in the national interest to have some government controls.

PS - i run my own business and am a committed capitalist. HOWEVER for one of governments key task is to provide adequate public services, infrastructure and look after the poor and disadvantaged. current policy in the housing, tax and immigration areas are distorting wealth distribution and meaning key services are underfunded and underresourced.

This sort of focus would echo earlier decades, where folk built stable families and lives on average incomes.

Would probably also go a long way to helping resolve shortages of nurses, teachers, emergency workers etc. Because they could do the aforementioned.

"Oversight of the central bank - as well as its regulation of the private banking sector - need to improve."

Understatement of the year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.