Housing affordability for first home buyers is slowly but steadily improving, driven by declining mortgage interest rates, steady prices at the bottom of the market and rising incomes.

Although expectations of cuts to the Reserve Bank's Official Cash Rate (OCR) keep getting pushed out, fixed mortgage rates have actually been slowly declining, driven by lower wholesale funding rates.

That has resulted in the average of the two year fixed rates offered by the major banks, the rate used in interest.co.nz's affordability calculations, steadily declining from a peak of 7.04% in November last year to 6.73% in April this year.

Although the decline isn't huge, it has taken the average two year fixed rate back to where it was in July last year.

Over the same period, house prices at the bottom of the market have remained relatively steady.

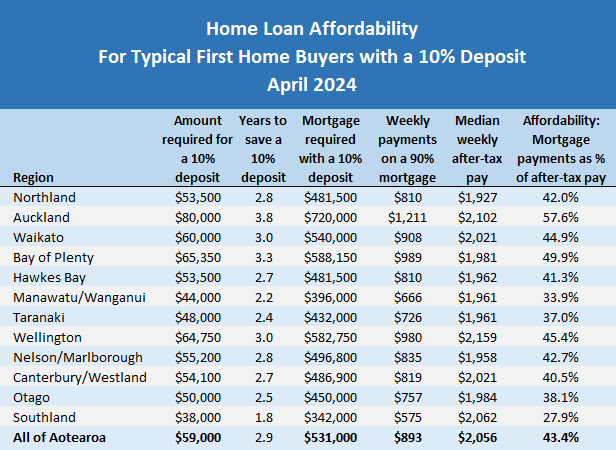

The Real Estate Institute of New Zealand's national lower quartile selling price was $590,000 in April, and has remained within a few thousand dollars of that since it dropped below $600,000 at the end of 2022.

That's still well below the record high of $670,000 reached in November 2021, with the subsequent declines taking the lower quartile price back to where it was in April 2021. It appears to be settling around the $590,000 mark for the time being, with small monthly movements up or down.

The other factor affecting affordability is one that gets far less attention than house prices or interest rates, but is just as important; incomes.

Interest.co.nz uses the median rates of pay for people aged 25-29 to calculate a representative after-tax pay rate for a couple in the first home buying age group, if both were working full time.

This was increasing by about $10 a month between April and December last year, but has slowed to around $2 to $3 a month so far this year.

The net result is that in April this year, the representative take home pay for a typical first home buying couple was $2056 a week, up $91 a week (4.6%) compared to April last year.

So when you take all of those factors into account, what does it mean for first home buyers?

Firstly, because house prices at the bottom of the market have been largely static for the last 12 months, the amounts needed for a deposit and a mortgage have hardly moved.

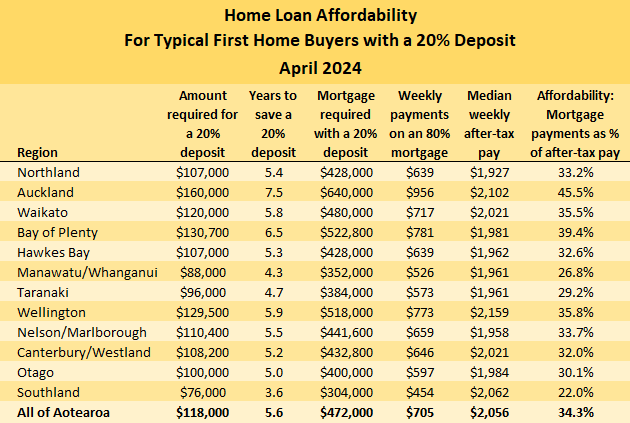

To buy a home at the April 2024 national lower quartile price of $590,000 would require $59,000 for a 10% deposit or $118,000 for a 20% deposit, and corresponding mortgages of $531,000 or $472,000.

Those figures are exactly the same as they were in June last year. So while there may have been small movements in those figures from month to month, essentially the goal posts are not moving for first home buyers in terms of how much they would need to save for a deposit and how much they would need to borrow to buy a lower quartile-priced home.

However, although mortgage interest rates have moved down very slightly this year, they remain high, and that means mortgage payments remain high.

The mortgage payments on a home purchased at the national lower quartile price with a 10% deposit would be around $893 a week. For the same home purchased with a 20% deposit it would be $705 a week.

The rise in incomes referred to above would have helped first home buyers make those payments, although in a high inflation environment there would be an increase in other claims on household budgets as well.

But taking the income and mortgage payment figures for April this year, the mortgage payments on a home purchased at the national lower quartile price in April would eat up 43% of median take home pay for typical first home buyers.

For buyers with a 20% deposit the mortgage payments would consume 34% of take home pay.

Both of those affordability measures have been in an almost continuous decline since they peaked at 46% for buyers with a 10% deposit and 36% for buyers with a 20% deposit in November last year.

While any improvement in affordability is good news for first home buyers, we need to remember the above numbers are based on national averages.

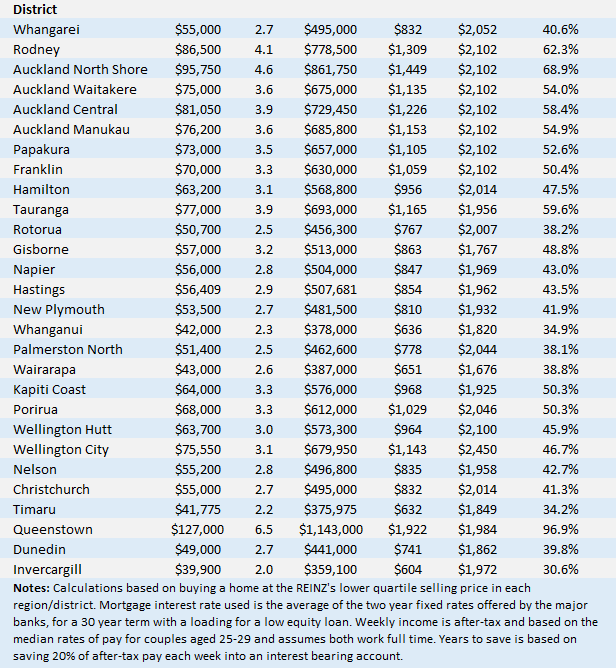

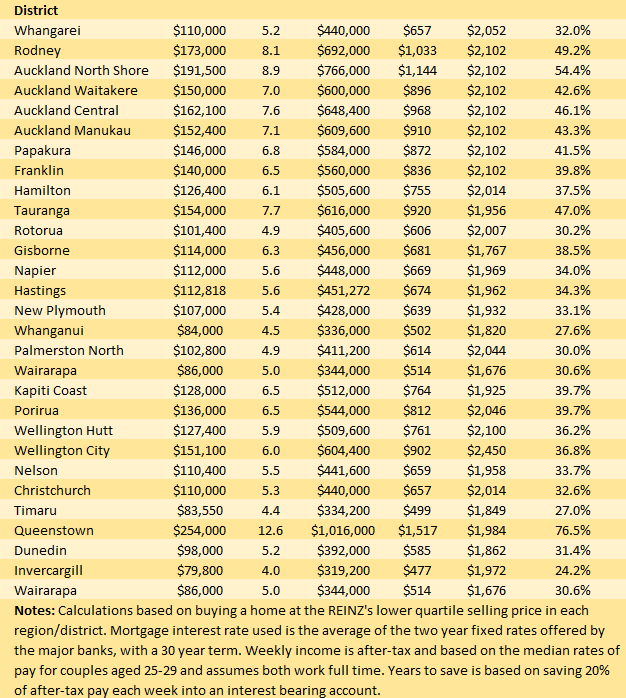

The tables below show the main affordability measures for the main urban districts throughout the country. These show the dream of home ownership remains hopelessly out of reach for first home buyers on average incomes in the Auckland region, even if they had a 20% deposit.

For that to change meaningfully, three things would need to happen: There would need to be a substantial drop in house prices, a substantial drop in mortgage interest rates and a substantial rise in incomes.

Don't hold your breath.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

106 Comments

Anyone else think the RBNZ jawboning on raising the likelihood of an OCR rate increase might be in response to the retail banks allowing mortgage rates drifting back? The people must be crushed!

Exactly. To be fair RBNZ has to be hawkish with everyone until the day they actually drop the OCR.

Banks are happy to help by lending tons of cash when times are good... not so keen to help RBNZ by slowing lending when times are bad tho. Funny that.

This is true and is why the Feb dovish review was so surprising to me. Currently I think their hawkishness isn't a bluff though, peoples mentality around prices is still that things will 'go back to the races' as soon as rates drop, so another raise may be needed to kill that mentality.

SKF

Certainly plenty around here who believe "that things will 'go back to the races' as soon as rates drop". Even by as little as 0.25%.

People are strange.

A 'real' estate agent at an open home was telling me in what can only be described as a horrible, patronising and threatening tone that I shouldn't think we have time on our side. "As soon as the interest rates drop, there will be piles of shoes in front of a house like this one again..", she bleated.

And yes, the property passed in at auction, then the downsizing vendors slapped on a ridiculously price tag that was good for nothing but a proper laugh. They've been cutting the price down ever since and it would be interesting to see the final sales price. I've been wondering how long the agent can last on the fat from the 2020-2021 binge. Might need to take her a food hamper before the fat lady sings (but no, I won't).

Indeed. But the market is snapshot in "today". Let them eat...less cake.

A 'real' estate agent at an open home was telling me in what can only be described as a horrible, patronising and threatening tone that I shouldn't think we have time on our side. "As soon as the interest rates drop, there will be piles of shoes in front of a house like this one again..", she bleated.

Owner occupier buyers - real estate agents do not owe buyers a duty of care, real estate agents do not owe buyers a fiduciary duty.

Real estate agents need sales transactions to earn their commissions to pay their living costs and remain employed. No transaction means no commission.

CAVEAT EMPTOR

The answer is simple: Real estate agents offer personal and several no loss price guarantees.

I guess you can demand - given the agent (and their firm's) confidence in the future price - that they offer personally a severally - a guaranteed buy back at the purchase price should you desire it 365 days from your purchase date.

Any takers?

Good ol' Kiwi "herd" mentality ....and that other clanger - "Never look outside their own box"

I think it’s more of a case of wishful thinking, people believe what they need to believe to keep themselves happy (head in the sand)

@SKF The longer that rates are held up the bigger the surge later IMHO.

If genuine buyers are unable to finance a home there will be a growing wall of people on hold and waiting. This approach of acting like the angry lion is idiotic I think that the RBNZ would be better placed to test the waters by easing a little

If you agree with me give me a thumbs up... I want to apply for the rb governor role one day and earn a massive salary

The RBNZ is trying to manage inflation, not increase house prices!!

That doesn't stop FHB wanting to get out of the rent trap. They're being squeezed by higher rents and higher test interest costs

Councils have underinvested in drainage of stormwater/wastewater and are now playing catch up. For all those years councils thought they were doing ratepayers a favour by promising lower rates bills. Rates are there to raise revenue for local govt

But the RBNZ in its wisdom says NO no no, we will take that spare cash off you and councils will get the message. Not only do we pay tax on tax with GST added, the RBNZ uses higher rates bills to justify higher OCR costs

How weird is this place

Affordability is going to improve...at about the same speed as falling off a cliff.

-SMG.

Scooter .....this is a western world phenomenon, as the banksters are extracting as much money AS POSSIBLE, out of the small business and working people, whether it be through rents or mortgage repayments (P + I) !

The "elite" want us poor, as if we all "nickle and diming" it and trying to find money behind the couch, as they think they will have more control of the general population - ever notice how financial literacy was never taught in schools (it may be now and I truly hope it is) - there was always a reason for that.

Then you have the general "dumbing down" of society, with all this PC, "be kind" crap etc etc coming from people that are only using it for business interests ...I could go on for ever about that !

You've just gotta do what's best for you, no matter what your circumstances - as one thing for sure these "banksters" don't give a "toss" about you or I !

Still long way to go. Just a couple of inches down the escalator before we can safely get off without feeling the impact

Do you think Houses are Overpriced ?

Based on affordability models, and the size of the spec leverage bubble, yes.

I don't think the question was addressed to you... Did you not get that it was for Houses Overpriced?

Hold on, this is a public forum, if you want to be that sensitive, you should probably create your own site and control who answers whom

So you both miss that I was mocking your biased moniker! Boy the level of intelligence is getting lower and lower in the comments section.

Is it biased or is it a fact-based assertion?

Yvil wouldn't understand a fact based question

I think they were joking about your username, hence their comment to the other person. I think you can all relax ;)

They are cheap as chips, hence you have offered to buy a house for a homeless person for the rest of the year

The hot air is leaking from the bubble. Low interest rates are gone unless vendors want to offer finance themselves. I've asked, they don't, they just want their big greedy 2021 capital gain. Meet the market or be prepared to wait. No sale = no commission.

Funny watching RE still shunting 2021 greed.

Primo properties get top prices. There must be hidden potential in whatever it is you are looking for or dont bother

"Primo properties get top prices. "

No surprises there.

The well off in NZ almost certainly don't have mortgages (except for tax reasons). They really couldn't care less what the RBNZ does with the OCR. What the RBNZ seems unable to grasp is that these same people are most likely the "price setters" that the RBNZ wants to stop raising prices and/or start cutting prices. Good luck with that Mr Orr.

Quality is indeed quality but that can go up and down in cycles to. Reality here is if you can afford pay the stupid asking prices, its has to tick all the boxes.

The spec rubbish that everyone overpaid for in the last five years is taking a bath. Talking to a few agent friends, they have a "this is reality" conversation prior to listing so they don't waste their time. They also have listings prepped and stacked deep to drop on 1 July, its all about tax free gains remember. When will all the tax avoider's wake up to the fact that flipping between themselves is dead. Add in the people that want to live there can only afford what it used to be before speculative greed took over.

Crispy popcorn...

Refill the popcorn. The ones I've looked at have heaps of VALUE more than asking PRICE

Ok. How many have you purchased in the last six months?

Answer: not as many yourself

Flip 'em then. Tax, listing and agent fees, holding costs... still worth it?

In for the haul

But why would they bother waiting, surely no one has actually made a profit in the last few years anyway?

Patient's affordability blood loss has been stemmed, and they are now in an induced coma.

Bring them back to full consciousness slowly with rising incomes to restore a better median multiple and if that doesn't work fast enough keep freeing up land use policies as there is another 20% of speculative and bureaucratic waste that could be removed from the patients' arteries.

.

There can’t be rising wages without rising productivity (or inflation, which leads to circular reference of rising interest rates…), and there’s no sign of that as would require investment- and we don’t do that.

The "Big 4" banksters win under any circumstances, at all times.

They trap the FHB's when interest rates are low, saying "get out there, fill ya boots son", while they are competing with the "astute" property investoor ...then when the prices get a bit too much for all, they lift interest rates to increase income from their existing mortgage book....and so it goes...

Time to bring in REAL competition - Open Banking would be a start.

Also how about "non recourse loans" where the BANK TAKES THE RISK ON WHICH PROPERTIES THEY LEND OUT MORTGAGES TO ? ...THAT WOULD REALLY GET THEM "THINKING" ABOUT THEIR RISK ASSESSMENT as THEY would be left with the security of that damp, crappy 3 bdm house facing south in the beautiful Mt Roskill ....instead of hounding and bankrupting the owner !

New Zealand - run by banksters, a supermarket duopoly and a building materials CARTEL.

This is the result folks - to live in Auckland (where most of the work is) and to be starting out, enjoy what's left of you net pay, after the banksters have taken their cut !

Good one, 'astute' is my favourite real estate word of the week, perhaps leading to the apocryphal corruption desti-astute.

Yeah stefanblaise ...as if they were that "astute" , they should of realised that "nothing goes up forever" !

A bit of personal and exciting news on my side is that we bought a house in April! I found a great brick and tile that ticked most boxes (and then some) for a price we could, surprisingly, afford. We paid almost 10% under the 2017 CV adjusted for CPI inflation. (Yes, a pretty rough indication of value, but still the best I can put here).

The vendor already bought another place and was very motivated.

Although prices are likely to continue tumbling after the recent RBNZ's announcement, I believe this was a great find.

Finally, the kids can have pets and live in a decent, quality home with bedrooms painted whatever colours they want, I can hang beautiful paintings where I want and we can upgrade and renovate as we see fit. Not to mention, with a bit of luck, I never have to talk to a real estate agent (seriously, what is the real doing in there..!) again in my life.

I've previously thanked Interest.co.nz and all the generous contributors on here and can't but gush with praise for you all again. I tried to convince my partner to donate to Interest.co.nz (long overdue!) and we plan to do so soon as we've got the mortgage payments in place.

Thanks again, you guys and gals, for the all advice, the recons, the entertainment, and the invaluable information I've read here during our house-hunting journey that spanned more than 3 years.

Congrats.

Thank you, Averageman.

by Averageman Hide All | 24th May 24, 12:23pm

Congrats.

Congrats ??? How hypocritical is that comment? You repeatedly post that you expect house prices to collapse in the near future, but you congratulate someone for buying now.... Have a bit of honesty and consistency.

Yvil, I won't be surprised if house prices collapse in the near future, or at least crash further. Yet I just bought. Dishonest and inconsistent much?

Like Averageman, I keep on cheering the current downward momentum of the NZ property ponzi. NZ's younger generations deserve better, so bring on that kaaaaark! moment for all I care!

You've hit the mark with that

Well done

Well done and congrats. You can now focus on other, more enjoyable things and pay a fair bit less attention to the property market, and more on what else is important to you and the family :-) When is the housewarming??? XD

The housewarming will probably be low-key since many/most of my best friends might never be able to afford their own places. I should have just invited all of you on here! That would be interesting. :-D

I have some survival guilt, to be honest. It feels awkward even telling most of my friends that we bought.

To be fair, my partner and I both have demanding full-time jobs (and I realise that we're lucky to have great jobs, but it didn't happen without serious effort on our parts) and I also have a part-time job that takes up most of Saturday (pretty enjoyable though, teaching kids at a local music school for very modest pay). We're obviously great at prioritising, saving and planning long-term, not to mention working like there's no free lunch ever.

I'll continue to hope that the housing market will continue improving (meaning falling!) as NZ's younger generations sure as heck deserves better.

Goodonya Tuis best !....you can now tell the land lord to stick his rent increases, where the sun don't shine ! .....Enjoy your new place, you both deserve it :)

Ps love your story above about that real estate agent - never known an industry that was so full of ABSOLUTE BS !!!

Thanks so much, Crazy Horse. You're so right about the real estate industry.

To be fair, I have one very cool real estate agent story too: The agent at the open home was awesome, chatting away with my kids and looking like a nice, decent bloke who couldn't possibly be a REA. When I approached him (by then my youngest kid had already invited the REA to his upcoming birthday party), he instantly asked whether we were first-home buyers. He then said something along the lines of: "In that case, you really need to stay away from a leaky, overpriced rotter like this one! I'll only sell this place to someone familiar with leaky houses and NZ property ownership, someone who would understand what they're in for and has the money to fix it." This level of honesty was probably a violation of the BS in the REA Code of Conduct.

Anyway, I always kept an eye on his listings as I would have loved buying from him. (Unfortunately, this was not to be.)

tuisbest ....an honest and straight up RE Agent are worth their weight in gold ! .....I had one here and in the US ...the sad part is, they are as rare as hen's teeth !

It's a real shame you couldn't of dealt with your one - but I would say in that industry, being straight up and honest doesn't get the commissions !

Indeed all RE agents will lie to a degree. Honest ones are in that mythical & rare as hens teeth category... if they existed in NZ they are unicorns. The trick is to pick the one that appears to lie the best & is the most networked to help convince buyers. Ethically all should disclose any serious issues, (which is what a seller should take them through on a property walkabout), but if there is any doubt unless you are donating land to charity (as we are) then you will want a sale price that is fair to the current market value.

I pretty much had to laugh at the draft RE agent "valuations" as some were so ludicrous to get the job signed up on their books they were obviously pulled from where the sun doesn't shine and would significantly differ to sales. But the trick is with RE agents is the sales pitch you are grading them on. Not the truth and not the fake valuation they think they can sell for (a real market valuation you would get from other analyst research, building condition & land geotechnical condition). Also grading the RE agent based on their appeal to the market most likely to buy the property which you can probably work out with your own judgement.

In this day and age they need to be aware of tech, online marketing & SM, correct pitch for the properties, physical tasks in preparation, adequate legal representation and local market knowledge etc. Some can still fail on all these counts so if you have the above then you might as well self represent.

In many ways the survivors guilt is normal but your friends will appreciate the reasons you had to buy. So you don't need to feel that you have overcome their position. Many of them would buy too for the security in housing, wellbeing benefits and a better base for a family so I think they will understand it and perhaps see you more as a yard stick of possibility. There will be many who cannot reach it no matter how hard they try but no true friend would hold that against you. They will want to celebrate with you your success.

Only when people start talking shamefully about the poor tenants in their third property and raising the rent to meet the market expectations that friends start judging them as property investors ;) Or the typical survivorship bias that somehow you deserved it more or tried harder then the others, and that they must just all be much lazier or do not deserve the same opportunities or did not try hard enough.

Sadly so much of the distain for the poor or less fortunate can be explained by a lack in self reflection into our own survivorship bias. Going right back into the education & upbringing we had, first jobs, first relationships, first homes, etc. Having survivors guilt is much more honest to the truth and actually shows a good degree of self reflection on our own position. In many ways it is to be celebrated and to be worked through to retain a feeling of joy and happiness for the luck.

Looking back on my position I know full well of those in my demographic I was the lucky 1-2%. I am now out surviving many of them and family and friends... but knowing my luck I can look at how to provide more opportunities to others less fortunate. Reaching the ladder/rope down so more don't fall into the pit or off the cliff too early.

Well said Pacifica:) I will reflect more on my own very meagre beginnings and those still dealing with life's meagre pickings.

Thanks very much for your nice message, Pacifica. We have great friends who are very happy for us indeed, even if they have very different circumstances, so we'll be sure to celebrate with them.

Good on you for realising you are among the lucky ones and for looking out for others. NZ already has enough 'savvy', rich property investors who got there by being so smart and awesome (even though they're not 'math people' who don't understand 'complicated' stuff like how to calculate ROI and have done little honest work in their lives).

Anyhow, I doubt it's love that makes the world go round, unfortunately - it's probably money. But, it is definitely love that makes the trip worthwhile. So here's to filling our new house with lots of happiness, laughing kids, play dates, BBQs with friends, silly pets and great memories.

Thanks so much to you all for being happy with us.

Well done Tui!

Awesome, congratulations! The intrinsic benefit of owning your own home will outweigh any short term falls in the spot price.

From past experience I completely agree

Very nice!

Congrats. Hope you get many happy years there

congrats, what region did you go with in the end?

Welldone Tuisbest!

Its not easy to get a toehold on your own place and its a good thing to have your own home.

Glad you now free of the evils of the REA Industry Industrial complex :)

Where have you settled?

We're in East Auckland, NZ Gecko. Lovely suburb we never thought we'd be able to afford buying in.

Yay, that house we really wanted to buy is now being offered inside our budget.

Boo, pity we both lost our jobs.

There are always openings in healthcare sector & tech. If you have good STEM knowledge Australia is calling.

I posted here a few months ago about the Kumeu/Waimauku/Riverhead area booming and got thoroughly rubbished.

A new subdivision was listed in Riverhead one month ago, and over 50% of the sections have already sold. So much for the great kiwi property crash.

Great spot for trout fishing I hear.

Good luck getting in/out there on a normal day....perfect for stay home family's I guess or out of work surfers?

I'm retired, living the life after several very good property investments.

When it floods.

https://www.tiktok.com/@twentyfour_13/video/7233166816703565057

Fortunes are being made out West. What do they say? You can lead a horse to water, but you can't make it drink.

And there, dear readers, is why some people are rich, and others aren't.

I would say having the capital & equity for multiple deposits & investment types is why some people are rich. Most of those start with the capital prior to their first job so saying it was of much value to them, or as much risk as it would be to others would be disingenuous.

After all you cannot choose your birth or take those early opportunities before you learn to breathe. If you think people are responsible for the conditions, early financial benefits & education of their childhood then you obviously are not and never have been in the very rich category. Perspective is key. Step outside your own experience to see what opportunities people truly have. It is vastly different for everyone.

Even in NZ not everyone is guaranteed the minimum wage in their work or indeed any chance of work at all. If you think you are not extremely lucky for your position then start reading, I would recommend even the cases on the Royal Commission for Abuse in Care would provide a key education in how we all had very different opportunities. Not all with education or benefits that you and I were very lucky to receive.

In my case you are very late to the party out west. What is the phrase for looking for the next one to sell to.

I would say most rich people I've met didn't inherit or start 'rich'...they earned it. By being smart, getting a decent education or trade, and making good decisions.

Many make appalling decisions and then blame others for their predicament. Did you know that most of the richest people in America aren't lottery winners or CEO"s...they're tradesmen who started from scratch and built very successful businesses.

I'm not late to the party out West, it hasn't even started yet - I listed about 10 reasons a few months back why the party's just getting going. Maybe you should take a look at the Unitary Plan. A property conglomerate involving Fletchers want to build 1,800 houses in Riverhead, and they've already acquired the land. Road widening in Riverhead,, new intersections, school extension, SH16 widening, 422 apartment retirement village in Riverhead, between 2 major highways etc. etc., I can't be bothered listing them all.

It's massive.

I see that you are still versed in the old ways of the 40years of decreasing DDDebt price, stoking massive DDDebt and Asset Bubbles to the moon ??

Good luck on selling your current bag holder/Bubble, to someone more even more gullible.

The higher and higher price of DDDebt will not allow for it and has you frozen in the old days.

The city is about to spread past Westgate, and waiting there just beyond is Kumeu and Riverhead. The amount of work planned for that area is monumental, and it's already commenced with the widening of SH16.

I made an absolute killing in West Harbour when it first opened up. Not many believed anything would happen there, but I did, in fact when I was building my first house there a guy wondered up and said, "nothing will ever happen out here". I bought 2 sections on the waterfront and then 2 more. And built 2 houses.

I've already outlined here a few weeks back why the cost of new builds won't be coming down. You're obviously risk-averse....I'm not, esp. where it's a foregone conclusion.

Monetary theory might be interesting, but practical results are always more reliable. Ever met a rich university professor? Drive to Westgate Shopping Centre and environs and observe the colossal amount of work underway there.

Hi Winger,

I know those areas exceptionally well.

The glaring problem is the just atrocious traffic in and out of the new developments around Kumeu and the Riverhead areas.

My own Hoby motorway, (was always freeflow) is now starting to strain under the increased traffic from Hoby Pt, etc.

8 to 5 Working people hate traffic. Stuff all useful transportation options exist past Westgate, THIS PRACTICAL reality stops me moving there.

I see no significant positives on the transportation side NW of the mighty Westgate......then you have the legacy flooding of those NW greenfield housing zones. I don't see land engineering solutions to mitigate low lying swampy land zones, especially when 50 to 200mm of water lands in a number of hours/day.

Real life examples of practicality, win everytime!

I have riskier investments in my diversified portfolio, property is a significant part, but it's risky to have it all in that space.

Auck down -40% from peak in REAL terms.

Then we have both the massively contractional fiscal and monetary times, that won't ease for 24 to 36 months. Many will go bust in the property dev/weak owner occupied space, from here.

Too many don't understand history or recognise an economic paradygm shift.

Maybe Winger has plenty of fat to ride the lows, many, many will not.

Good luck with it neighbour.

Firstly, there is no more flooding there than anywhere else, I've checked, it's a fantasy. The flooding invention is BS. The Council and everyone else is so paranoid about it no one is going to build anywhere near flood zones. The land I own is well above the local stream and if my property floods, all of Auckland will be under water.

I couldn't care less about the traffic and the motorway, I don't work and many now work from home and have flexible hours.

It's really about making money, and next opportunity in Riverhead and I'm going to check exactly how many properties have sold off the plans of a new subdivision there, but when I drove by the other day, on the sign it looked to be more then half....in one month. Everything is selling in Riverhead, so who's got it right, you - or the ones with the cash?

Auckland is not down 40% - my neighbour here recently sold for $2m, just outside of Auckland. More than what I thought he'd get.

You can talk about paradigm shifts until the cows come home, but with interest rates up, now's a great time to do a deal and drive a hard bargain.

Sorry Winger, if you do not know (or acknowledge) that the Auckland region has recorded -19% ACTUAL/NOMINAL falls in house prices and we have had +20% accumulated inflation since 2021 ?? - I cannot help or discuss further, as I look foolish, being in a discussion with a Head in the Sander.

Auckland has had REAL - 39% falls (yes rounding would see 40%) since 2021. For those unfamiliar in the term of "REAL" - it means CPI (yes inflation) and nominal (actual $ move) adjusted pricing.

For you to pick a perfectly ripe cherry ("This" sold at a good price) out of a bowl of otherwise rotten ones (valuation collapsed) ......does not fool anyone that the rotten have reversed age....

Don't just believe me, just research it more deeply yourself, after the sand has been shaken loose....

Let me help in this education, NZ stats only are below, but a smart person can do the same calculations regionally and by any city.....if we care to learn.

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed (stlouisfed.org)

The 1970's info is a real doosey NZ wide!!!

You are wasting your time debating with an old boomer in his 70’s. According to him he had it harder when he started off. All beneficiaries are lazy bludgers. All millennials waste too much money at cafes and on travelling. Everyone can be rich if they work hard. What he will never admit though is that the boomers had a great early life in general, were able to get a qualification for virtually free, when they climbed on the ladder their first home was cheap and loans were 3 times or better, inflation was kind to them and when they sought to grow their wealth those assets were cheap compared to today.

Yeah you are probably right. It's good for us to debunk the false information, old narratives, when we see it.

But we have to give up on some.

Anyways its truly great to see this pricing reset taking shape and continuing for another couple of years, to again have housing at the 3x, 4x, 5x DTI again, as when I started out.

Firstly my qualification wasn't free, I paid for it.

I didn't have a great life at all, I did some very tedious, long hours at various slave-driving outfits to make money, so I could learn my skill. But it paid off, and in my spare time I learned about property, and that's why, according to the internet, I'm in the wealthiest 1% in NZ.

Not bad, wouldn't you say? And my next foray in Riverhead is going to be a real winner, one of the best ones yet.

There's nothing like a bit of excitement in the real estate industry, I don't know what you guys do for fun. Go to the pub?

3 huge companies have bought hundreds of acres in Riverhead. Ever heard of the expression "follow the money"? Probably not.

Yeah right. So you ended up with a student loan in the tens of thousands. I paid a little for my four year degree. Like $300 a year. It was cheap and I got a bursary. Life was good to us. We were lucky. We had a lower cost of living, assets were cheap to buy and inflation drove up their values. A lot of boomers were greasy and accumulated more than they need. I hope you are not one of them. I hope you also help those less fortunate than you. If you can get past the thinking that they are useless lazy buggers.

I never had a student loan, there was no such thing. I paid for everything as I went.

I took huge risks, something people like you couldn't even imagine how risky it was. My father was horrified, but it all worked out. I made good decisions, and didn't do things like get married and pump out kids while I was young.

And now life's a breeze, I do whatever I want, when I want.

Did you ever marry and have kids?

Yes. I have a very supportive wife who takes me to task if I ever suggest buying something I don't actually need. I've been very lucky in that respect.

If you in fact have so much money why don’t you enjoy it and have the odd toy. You strike me as someone around 75-80 years old. We don’t live forever. My wife and I are busy getting rid of our capital by giving it to our kids before we kick the proverbial. In saying that we live well in terms of food and general living.

I do enjoy it. My wife and I have just spent 5 weeks touring about 7 countries in Europe with a few days in Qatar, which, by the way, was absolutely amazing.

I encouraged my late mother to indulge in a bit of property speculation. The result was that my children and a few other very lucky relatives have just inherited $250k each.

Do the sections each have their own jetties ?

They've got their own personal bank managers for all the cash that's being made. I'm up $500k on my bet, so far. And this subdivision isn't developed yet, it's still farmland. The question is.............what will they sell for when the roads are in?

Sure it was a good time to buy over 10years ago. Now it is a laugh tipped with caution as the network is not setup for the population, (ok if you are not living there though). But hey anyone buying are helping those move from the market with a significant profit. We were around there then and a few friends have made a mint. Get in while the road access still is available. Sadly the train is out... (AT canned it) and will be out for some time (AT decided no one needed PT to work) & there is actually negative amounts of PT and road access in the area (with AT less focused on how real people live esp at the fringes).

The doctors and beaches are alright out there. I hope they still have the decent bakery (with the really nice meals, salads, pies, cakes) and the Ausi butcher. Oh and don't start trying to tour the wineries promising yourself you will try them all in a day... there are a few and you will need a sober driver. Best days are those with live music & festival like events. Try the slightly closer in market next to a winery restaurant... mmnn tasty memories.

If it's any consolation, once renowned school districts in Texas are now closing schools as enrollments are too low. Locals are acknowledging that “families with school aged kids cannot afford 500k starter homes at 7% rates.”

https://www.fox4news.com/news/plano-isd-is-considering-closing-these-4-…

More from the US. WaPo editorial proposed a solution to unaffordable housing: Get everyone into mobile homes by stripping them down and calling them something else.

If Congress removed the permanent chassis requirement, manufactured homes would be safer, and they would be much more acceptable in traditional neighborhoods. Today, they come in sizes ranging from 600 square feet to more than 3,000 square feet, and in a variety of designs and finishes.

Amending the law would also facilitate the financing of manufactured homes. Private mortgages are largely unavailable for manufactured homes because, in principle, they can be moved. This leads them to be typically financed as personal property, like cars, with higher interest rates than mortgages. In 2021, 77 percent of manufactured homes were titled as personal property rather than real estate.

https://www.washingtonpost.com/opinions/2024/05/21/affordable-mobile-ho…

Looking at the mortgage rates discussion facebook group, it appears that special rates being offered are increasing again since the OCR announcement.

Seems like banks have tried to steal headlines with trimming carded rates but the discount for special rates is reduced. Early days yet, but are real mortgage rates increasing again?

Yes. Banks have a pricing team, they have been instructed to increase the minimum rates they can offer. Not by much but still an increase.

Owner occupier buyers:

In real estate agent speak "more choice", potentially coming. Even more of a buyer's market as highly leveraged property investors are under cashflow pressure.

https://www.oneroof.co.nz/news/countdown-to-bright-line-stressed-landlo…

affordable comparable to 2016 property prices when we had a severe housing crisis? Yeah thought not.

Geez given those numbers no wonder our land tripled in value in a few years. Crazy, that 2 full time wages still takes way too long to reach a decent deposit and the mortgage is a mountain in comparison to what they were. It is no wonder most people would still not be able to afford this market if they were starting out and decide to ditch to Aus before they are too old to have kids safely. Seriously NZ is crazy priced compared to the housing quality & severe housing issues with large future risks (like rotten structural elements, severe black mould, lacking adequate ventilation & management, toxic materials that are hazardous/deadly to children and adults long term). Finding a good home is like winning lotto and is about as life changing (especially for children and for when the owners become more elderly). Being stuck in bad rentals is like a crippling car accident that can affect health & opportunities long term.

Then we wonder why children become disconnected to their communities when they are living near itinerant lifestyles forced to move every year or couple of years, to more ill designed houses not suited to wet weather conditions common in NZ.

Now's a great time to buy, interest rates are up and there'll be more than a few homeowners under pressure.

Not as high as they were in the '80's though, mortgage interest rates got to 25%. Try that out.

1980’s. I had my first and second home. Both loans $49,000.00. Three times income. My highest rate was 21per cent or so. Only there for months and rates came down quickly. Totally different from today. Rates up there for ages, loans as high as ten times, incredible inflation in terms of food, rates , insurances etc etc. Don’t listen to old boomers who have no idea how lucky they are. They are totally ignorant and small minded.

Not true. Interest rates in NZ went above 10% in 1981 and declined below 10% in 1992. 11 years, very tough for a lot of people.

I had to sell a house to ensure I stayed afloat.

What "incredible inflation"? Inflation in NZ is 4%. Back to the drawing board old chap.

You conveniently forget to mention how cheap houses were back in the 80’s and that borrowing was generally at 3 times income at the worst. Interest rate comparisons are irrelevant when you look at say 10 times income in Auckland today along with the current incredibly high cost of living. Please be honest and factual. I appreciate that’s hard for you to do.

You conveniently forgot to retract your absurd statement that interest rates "were up for a few months and came down quickly". You've got a short memory buddy. They were up for 10 years.

The cost of housing is relative pretty much worldwide. I travel a lot and it's the same everywhere, NZ is no different...and stop making up absurd stories that inflation's out-of-control.

It isn't.

I was referring to interest rates being in the 20’s for a short period of time actually and they were. When you borrow 3 times income at worst you can handle interest rates well above 7 per cent. Very few people today could borrow say $800k at 15 per cent. At 3 per cent it was easy for some. Everything was much cheaper in the 80’s. Food , power, rates and insurance and building costs and land. I had it much easier than my kids. My wife never worked like many in those days. Now both partners work in many situations just to survive. Why is that? Be honest!

People work more because the government hands out less, and so they should. The days of endless gubbermint handouts are over.

They have to pay for their tertiary education like most other countries, whereas in the good ol' kiwi socialist past the govt coughed up. I had to pay for my education following high school in the 60's, whereas most got it handed to them on a plate. When I left NZ in 1969 to get a job overseas my father gave me $50 when I got on the aircraft I was so broke.

Piggy Muldoon's marginal tax rate of 66 cents in the dollar going to the government, the reason I got into the property business. The light at the end of the tunnel.

NZ was living in a fool's paradise, and Roger Douglas knew it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.