Reserve Bank Governor Graeme Wheeler's decision to hold off lifting the Official Cash Rate until at least March 13 is likely to dilute the impact of increases, at least a bit, when they do come.

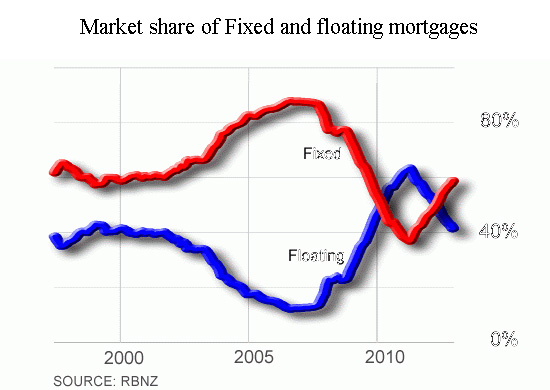

The latest Reserve Bank figures show another decent rise in the value of mortgages shifting from floating rates to fixed-term rates. As of December a total of 58.6% of home loans by value were fixed with 41.3% floating. The balance was unallocated.

Month-on-month the value of fixed home loans was up from 57.4% in November, with floating loans down from 42.5%. The month-on-month increase in fixed loans was $2.6 billion, or 2.4%, to $111.424 billion, with floating loans down $2.1 billion, or 2.6%, to $78.502 billion.

The year-on-year change is even more stark. The value of fixed-term home loans increased by $28.7 billion, or 35%, in the 12 months to December 2013. At the same time the value of floating rate loans dropped $18.2 billion, or 18.8%.

When Wheeler does ultimately lift the OCR the increase is expected to feed promptly through to floating home loan rates. So with no hike at last week's OCR review, and the next review not until March 13, the six week delay is likely to see the trend of borrowers switching to fixed-term mortgages from floating, or variable, rate ones continuing, which means fewer people will be immediately impacted if the OCR does go up.

However Wheeler and his Reserve Bank underlings will be encouraged by the fact a major chunk of fixed mortgages are fixed for less than a year. A total of $61.5 billion, or 55.2%, of fixed mortgages by value are fixed for less than one year. That means if the OCR has been increased before those borrowers' loans come up for renewal, they're likely to face increased interest rates.

This article was first published in our email for paying subscribers. See here for more details and to subscribe.

4 Comments

I wouldn't fix for too long. There will be cuts again once more negative world events occur again.

Dont panic to the banks tune of hike hike hikes.... heard it before ...

Floating is cheaper over the long term if you can keep your nerve.

I'm not so sure. What's certainty worth?

Not much. Would rather take the savings now. There will always be uncertainty, & more uncertainty later as well. And larger Global upheavals in the next 18 months....

A 6.3% 2 year rate compared to 5.6% floating now (carded) .. take the savings now. Are we going to see floating at 7 - 8% in today's world? Unlikely - unless the the Fed & IMF get us mixed up with India or Turkey!!

2.69% Fixed 2 years in the UK ..... we are most definitely over-priced in NZ. Still, we are well behaved Guinea Pigs here ...

Do the Americans & Brits pay break fees on their 15+ year fixed rate loans? If so, they must be horrendous charges if they use the same formula as NZ banks.

The risk in fixing mortgages in NZ for 3+ years is paying stiff 'break fees' [so called] if you need to move.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.