Some readers have been looking for data on the 'real' change in house prices over a long time frame.

Their thought is that this will show how different the current sharp run-up in nominal prices the recent data is from historical precedents.

But it doesn't look like that is the case.

Finding data over a long period is not easy. But Statsitics NZ has a Long Term Data Series where annual, national data can be sourced. It is available in their G.6.1 series from the AREMOS set. That runs from 1989 to 2004 but can be accuratelty extended by an earlier index of the same series, and a later reference to REINZ data that accurately mirrors the AREMOS data.

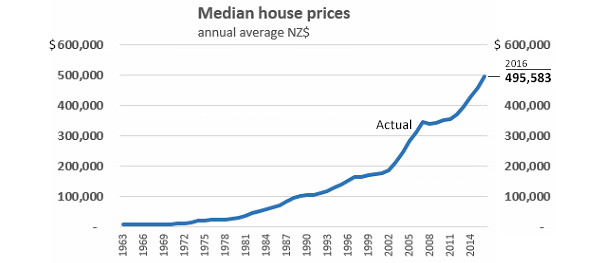

The full 1963 to 2016 series is listed below.

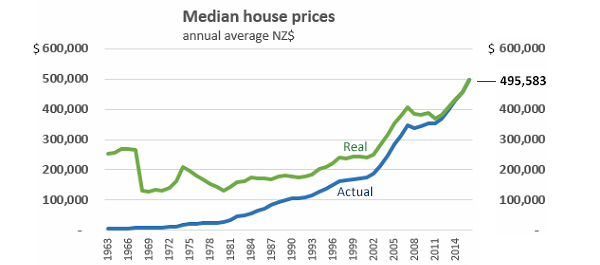

These median house prices can be adjusted using the RBNZ Inflation Calculator to derive 'real' 2016 prices.

The nominal run-up in house prices is familiar and quite spectacular.

Applying the inflation deflator and recalculating all prices to 2016 levels does smooth out some of the rise.

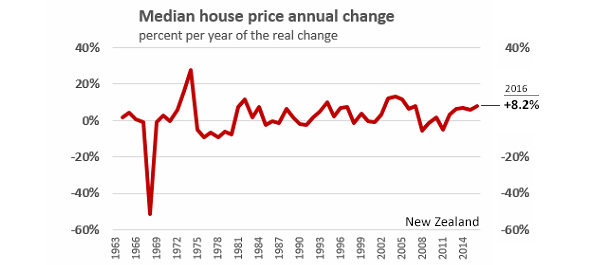

But when you look at the annual change in real house prices, you find that current increases in fact seem quite 'normal' in New Zealand's history.

Go figure.

Here is the data for these charts.

| Real house price inflation | ||||

| Stats NZ | RBNZ | |||

| Year | LTDS | CPI adjustment | 'Real' | 'Real' |

| G.6.1 | assume Q2 | 2016 | price | |

| based on AREMOS | price | change | ||

| NZ$ nominal | Index | NZ$ | % pa | |

| 1963 | 6,171 | 40.98 | 252,888 | ... |

| 1964 | 6,454 | 39.78 | 256,744 | 1.5% |

| 1965 | 6,964 | 38.41 | 267,473 | 4.2% |

| 1966 | 7,247 | 37.18 | 269,432 | 0.7% |

| 1967 | 7,643 | 34.93 | 266,970 | -0.9% |

| 1968 | 7,700 | 16.86 | 129,816 | -51.4% |

| 1969 | 8,039 | 16.03 | 128,870 | -0.7% |

| 1970 | 8,719 | 15.23 | 132,786 | 3.0% |

| 1971 | 9,625 | 13.72 | 132,049 | -0.6% |

| 1972 | 10,927 | 12.77 | 139,534 | 5.7% |

| 1973 | 13,701 | 11.87 | 162,629 | 16.6% |

| 1974 | 19,249 | 10.80 | 207,890 | 27.8% |

| 1975 | 21,061 | 9.39 | 197,760 | -4.9% |

| 1976 | 22,533 | 7.98 | 179,811 | -9.1% |

| 1977 | 24,005 | 7.00 | 168,033 | -6.6% |

| 1978 | 24,514 | 6.23 | 152,724 | -9.1% |

| 1979 | 25,816 | 5.55 | 143,281 | -6.2% |

| 1980 | 28,138 | 4.70 | 132,247 | -7.7% |

| 1981 | 34,762 | 4.09 | 142,175 | 7.5% |

| 1982 | 45,575 | 3.49 | 159,057 | 11.9% |

| 1983 | 50,161 | 3.23 | 162,019 | 1.9% |

| 1984 | 56,615 | 3.08 | 174,374 | 7.6% |

| 1985 | 64,598 | 2.64 | 170,538 | -2.2% |

| 1986 | 71,222 | 2.39 | 170,219 | -0.2% |

| 1987 | 83,337 | 2.01 | 167,508 | -1.6% |

| 1988 | 94,320 | 1.89 | 178,266 | 6.4% |

| 1989 | 100,208 | 1.81 | 181,377 | 1.7% |

| 1990 | 105,875 | 1.68 | 177,870 | -1.9% |

| 1991 | 106,000 | 1.64 | 173,840 | -2.3% |

| 1992 | 109,229 | 1.62 | 176,951 | 1.8% |

| 1993 | 115,813 | 1.60 | 185,300 | 4.7% |

| 1994 | 129,083 | 1.58 | 203,952 | 10.1% |

| 1995 | 138,125 | 1.51 | 208,569 | 2.3% |

| 1996 | 150,729 | 1.48 | 223,079 | 7.0% |

| 1997 | 163,333 | 1.47 | 240,100 | 7.6% |

| 1998 | 164,167 | 1.44 | 236,400 | -1.5% |

| 1999 | 168,990 | 1.45 | 245,035 | 3.7% |

| 2000 | 171,813 | 1.42 | 243,974 | -0.4% |

| 2001 | 174,958 | 1.38 | 241,443 | -1.0% |

| 2002 | 186,500 | 1.34 | 249,910 | 3.5% |

| 2003 | 211,971 | 1.32 | 279,802 | 12.0% |

| 2004 | 245,896 | 1.29 | 317,206 | 13.4% |

| 2005 | 283,167 | 1.25 | 353,958 | 11.6% |

| 2006 | 311,375 | 1.21 | 376,764 | 6.4% |

| 2007 | 345,458 | 1.18 | 407,641 | 8.2% |

| 2008 | 338,125 | 1.14 | 385,463 | -5.4% |

| 2009 | 342,854 | 1.11 | 380,568 | -1.3% |

| 2010 | 352,500 | 1.10 | 387,750 | 1.9% |

| 2011 | 354,708 | 1.04 | 368,897 | -4.9% |

| 2012 | 370,021 | 1.03 | 381,121 | 3.3% |

| 2013 | 396,919 | 1.02 | 404,857 | 6.2% |

| 2014 | 428,188 | 1.01 | 432,469 | 6.8% |

| 2015 | 457,929 | 1.00 | 457,929 | 5.9% |

| 2016 | 495,583 | 1.00 | 495,583 | 8.2% |

As someone who was around in the 1960s and has memory of the period, the early prices above resonate as realistic to me.

Another thought: House prices are actually just a proxy for affordability. But they are not a good one because they are incomplete. Incomes, tax rates, and interest rates all have as much to say about 'affordability'' often more. And recently, we can add regulatory limits, like LVR standards.

106 Comments

That is rather special... if you happened to have bought a home in 1967, you would have finally returned to the same "real" value in 2003.

It would be fun to see this same analysis as applied to regions such as Auckland, and compared to other regions such as Hawkes Bay. The country on average may have had not too outsized property gains in the past decade, although the majority of the capital gains have been concentrated in a few markets. For example, Hawkes Bay property has been losing real value over the last decade (along with many other regions). At some point there will a reversion to the mean.

Sadly, there is no long term data available by region that we can find. If anyone knows where to source it, we would be interested, especially for the main centres.

Oh Dear DC, just read this article for the first time now and within 5 seconds picked the major error.

Maybe some other readers picked it too??

What happened on 10 July 1967??.

We didn't have a 50% fall, we had.....decimalisation!!!!!!!!!!

2 dollars equalled one pound.

For the other issues with the analysis I will reply shortly.

Obviously NZ as a whole hasn't seen the bubble Auckland has over the past 5 years. In fact the 5 yrs to 2016 is only up 34% while the 5 years to 2007 was up 63%. Compare Auckland only data for those same periods!!

The graph of annual growth changes is nonsense, it has too much "noise" to be intelligible. The better comparison is rolling 5 year average price growth.

The other issue is that there are historical reasons for repricing. Interest rate declines being the main one. Whether current pricing in Auckland is justified is based on so many factors, one being that if current prices are based on the anticipation of future "real" price rises, and the previous "real" price rises are based on an upward revaluation due primarily on falling interest rates and rising expectations of future capital gains, then Houston, we have a problem...

I think the risk we have Chris is that kiwis are applying the 2002-2016 real home price trend line as the 'norm' and applying that to the future - and completely ignoring the 1960's - early 2000's real home price trend line and applying that as the norm. If you apply the 40 year trend from the 60's to early 00's - it would appear we could have a bubble on a bubble - and prices overdone by 40-50%.

If you look at the USA real home price chart that Shiller put together, their house prices returned to the historical post-WW2 trend line for a few years after their bubble - but prices are away again now, hence why he's been suspicious that they might be heading towards another bubble there.

Agreed. Just need someone to stick a stake in the blood sucking vampire called ZIRP.

ZIRP the medicine not the cause. Kill it by presumably raising interest rates and we'll have a second Great Depression on our hands, no thanks.

What's the cause?

Root cause, limits to growth, specifically peak oil. However there are then multipliers, specifically a huge parasitic ponzi scheme namely financial markets. With energy no longer cheap from about 2004 there are huge amounts of parasitic money looking for a place to make money / hide, hence huge asset inflation.

What century is this 'Peak oil' going to occurr?

So you are a fan of hugely inflating the money supply, thereby blowing bubbles in asset values all around the world?

At some point, the non-performing debt has to clear the system. Kicking the can down the road via ZIRP just makes for a bigger and nastier problem in the future. I'd rather take the smaller pain sooner rather than the larger pain later.

But after 30 years a buyer's mortgage would be gone. When someone bought a house in 1963 for 250k or so, they could get it with a deposit of 12.5k (5%). Even if in real terms ,adjusted for inflation, the house didn't go up in price the buyer still makes/saves a couple of hundred thousand $ by 2003 because now they have about 250k worth of equity instead of only 12.5k adjusted for inflation. So even if house prices didn't go up in real terms between 1963 and 2003, having bought a house in 1963 would have been a smart financial decision still when reviewed after 40 years.

Really?

What about the 30 years of mortgage payments, and kindly note that for some of the time in that period, the interest rate was in the teens, sometimes the high teens. On average, the home value increased by something close to the mortgage interest rate. There is usually a delta though, something on the order or 3%, where the mortgage rate is higher than the CPI by this amount. So, one is pouring in money into the mortgage at a higher rate than the home is increasing, at least in the early days. Where is this in your simplistic analysis?

What about the property taxes and rates paid during that time period?

What of the maintenance and upkeep costs incurred?

It would be best to do a full accounting of the total costs in order to make an assessment as to the merits of the financial decision.

In terms of an accurate comparison for purchasing the home back in 1963, it would be appropriate to assess at least one alternative. Assuming that one needs to have a home to live in, it would be appropriate to assess the cost of renting for the entire time while saving and investing the funds saved as compared to the costs incurred in owning the same home.

Or for the investing side of the argument, take the total cash flow put into the home throughout the time period, and invest that cash flow. If one is adept, then use the rule of 70 during the lifetime (invest in equities by 70 minus your age, the rest in bonds or term deposits). See how that compares in terms of price appreciation.

Yea, but don't don't forget and ignore the 10 years of RENT FREE living between 1993 and 2003 after the 30 year mortgage has been paid off. Besides, during the 30 years Rent vs Mortgage payments would not have been vastly different anyway. That's just the cost of living, you pick- whether you pay rent or whether you pay a mortgage, but you have to pay one or the other anyway.. The difference is with one after 30 years you are still paying rent and that rent costs you more and more each year. With the other your payments cost you less and less(well, in theory), and after 30 years you don't pay anything except for the maintenance and rates, and have 100% equity in your asset. Any extra savings after rental or mortgage payments can be invested in both cases, whether you rent or pay a mortgage. And if a person would have chosen to invest into the share market in 1963 instead of buying a home, well there are no guarantees that they would have made more then 260k profit 30 years later. Real estate is generally safer then the share market, especially if the real estate in question is your home.

Yes, but because of leverage, there can be very good times to buy, and very bad times to buy. The last couple of years, and perhaps the next few years are in the very bad times to buy in my opinion..

I say that because you can't dollar cost average when buying your house like you can with shares and reduce a lot of the risk of bad timing - I'll buy 10% now, 10% in 2 years, 10% in 4 years - to smooth out any fluctuations in houses prices. Buying a house is essentially a game of poker - at the point of sale I'm all in with 100% of my money, and the bank the rest (with whatever lending they give you). Timing becomes incredibly important when you do that - but if you could dollar cost average that would negate a lot of the risk of being all in at the top of a cycle (or bubble...). The individual returns between investors will be dramatically different between people purely on luck of timing....unless of course they are a Darklord and they buy more and more houses over different periods of time - but again if you start out at the wrong time and end up with no equity, games over..My personal opinion is housing investors starting out now will really struggle over the next 5-10 years. Those who started 10 years ago are okay because they had the benefit of lucky timing...

"That is rather special... if you happened to have bought a home in 1967, you would have finally returned to the same "real" value in 2003. "

Explain a bit?

Interesting I played around with smoothing out this data to try and understand the trend. Here it is here

http://imgur.com/a/plhfC

the rate of growth is growing!

try going back to say 1900 and run it forward.

example,

http://observationsandnotes.blogspot.co.nz/2011/06/us-housing-prices-si…

... here's the Gummster's take on this excellent series of numbers ... our nominal house price ( $NZ ) in 2015 was 74 times what it was in 1963 ...

But our nation's GDP ( $US ) has only grown 26 times in that time period ( $US 6.639 B in 1963 : $US 173.8 B in 2015 ) ...

... so in relation to our GDP , the growth of our economy , houses are nearly 3 times the price in 2015 than what they were in 1963 ... And yet houses are an unproductive asset ... the time is ripe for a repeat of 1968 .... or something greater than a 51 % downward correction .... Hmmmmmm ?

You are definitely smarter than the average bear, Gummy.

It's currency that's collapsed in value. Look up how many kg of gold and silver the average the average 1963 salary purchased. You'd have to really be an optimist to think that paper is going to regain it's lost purchasing power sometime in the future.

Given the house prices are per house, not total national housing value, is it not more appropriate to compare with per capita gdp?

1963 Us $ 2622

2015 37807

Increase of 14 times.

So house prices have increased 5 times faster than GDP per capita.

Except that this compares nominal housing to inflation adjusted GDP.

Indeed...60~75%, maybe if you listen to Nicole Foss 90%, so where to hide.....

I think this analysis mostly shows the pointlessness of national averages/medians etc. A nation's housing market is made up of many disparate markets with their own characteristics. A house I lived in in Herne Bay in 1980 was worth $50,000; now it would be worth $2m easily, or 40 times as much; yet my salary only doubled in that time.

You either had a very high salary in 1980 or have a very low one now. My salary is 31 times what it was in 1980.

I'm usually not in agreement with ZS... in this case, I'd be questioning the validity of your career path. My salary ratio is similar to ZS, maybe slightly higher. This is comparing a bit of apples to oranges though in that in 1980 I was an entry level unskilled worker, whereas now I am a skilled and experienced consultant. From 1980 to 1986 my wages increased by 5x due to upskilling and training. From 1986 to present, the ratio is more like 10x.

A side note, this is a good example of working hard (and getting lucky at the right time, one should always credit luck as well as skill/dedication). The social system is hopefully in place to assist the people that are not so lucky. Unfortunately, the system also assists some that may not be as hard working as well as the less fortunate. Not sure whether it is appropriate to attempt to separate the two cohorts though... that can get rather messy.

5x in 6 years is really good! Me and my mates who graduated circa 2011 have only seen our income increase by 3 - 4 times since then (mostly due to upskilling / specializing). I suppose that when you were born does really make a difference.

2001 (graduated) - 2017 my increase is approx 6x.

Now due to location, and lack of available work, that figure is likely to come down.

A graduate in 2001 earned about $40k in Auckland, so you are now on $250ish(?) in the same field but now at a senior level?? But a graduate today would be only on $60k. Need to compare apples with apples.

The appropriate item of interest here is not the wage after upskilling/training but instead the wage prior to upskilling. The minimum wage when I was a teenager was quite low. The ratio of the minimum wage to the wage for a white collar technical profession has decreased over time, largely due to the increase in the minimum wage rather than the decrease in the technical profession wage. In other words, wage inequity was higher in the past than now. I just looked up engineering starting salary history in current year dollars. Turns out that the value is rather constant over the past 30 years. Minimum wage in current year dollars has not been constant, but increasing with time. Just to be pedantic, the phrase current year dollars means that one uses CPI to adjust the value from the amount in the past to the current year.

If your wage after graduation has increased by 3-4x in 6 years, you are on a high wage increase track than I was after graduation. When I graduated, inflation was considerably higher than it is now, and my wage increase over 6 years after graduation was more like 2x.

I agree, when you were born does make a difference. The standard of living for young people is higher now than it was when I was young. The housing issue is only a small aspect of what goes into evaluating the standard of living.

If my salary went up from 33000 in 1990 by 31 times I would be a happy camper and retiring but that just not happening. As for 10 times I would also be happy, but my salary alas is way less. In 1990 I could buy a crate for 18 bucks now a bottle of beer on the viaduct costs 15 bucks and they say that's progress.

Doing a paper round in 1980 doesn't count ZS!!

Using Stats NZ data: median wage data back to 1998 and CPI data prior to that, a wage would have increased about 5.5 times over the period.

Depends on your industry, I went from $9K in 1987 but rose very quickly to $32K in 1990 after an apprenticeship to salaries in the $70K + Comm plus a car so potentially 10x, or only double depending on how you view it, however I agree that has I stayed in certain service industries they are still only paying $35-45K PA. What has been noticeable is that things basically have not moved in the last 10 years so you essentially hit a low glass ceiling in many sectors.

I think you are right about the glass ceiling.

It seems very hard to move up in an organisation. I have had various "Senior" positions created as a means of retaining/paying me more. But breaking through and hitting the next level seems almost impossible. Those above seem permanently fixed to their chairs these days, as do those above them.

It also seems to be harder to move across and up in a new company as they want you to have some "in house" experience first.

As a tradesman in Auckland mid 80's I was able to earn $24 an hour. Now I would be able to earn maybe $50 an hour. That is about double. The cost of a house during that period has gone up x5 at the very rough suburb least. Police, Nurses, school teachers and laborers would be in the same wage growth area as myself.

The people that a city needs to function are going to struggle to stay on in Auckland. The young replacement generation will mostly go elsewhere.

Haha yeah that is funny. My hourly rate in 2016 was $18/h. Now in 2020 it is $36/h for my anecdotal 2cents after upskilling etc blah blah blah...

Hi David - appreciate you putting this data together. Out of interest, would it be possible to have the inflation adjusted values indexed (based) 100 from the 1963 point to show relative change from that time. Similar to the below:

http://www.gmregroup.com/agent_files/graph.jpg

{kind=link}

I see your real and inflation adjusted median sales are only equal in 2016 which I'm not certain, but don't think paints the real picture here (its plotted back to front in my opinion). I think if we base 100 from 1963 from there I think we'd see the real picture. I might need to do some more reading to see how Shiller adjusted/indexed his data from 1890 onwards.

David - Shiller has provided his data-set for the US Real Home Price Index here:

http://irrationalexuberance.com/main.html?src=%2F#1,0

1890 is base 100. I'll see if I can make sense of his methodology, but if you bet me to the punch, it would be great to compare like with like (US vs NZ) - especially knowing the outcome of their 'bubble'.

Even then with upskilling that house price growth still has outrun your salary growth.

Worse now is market is saturated with skilled or rather qualifications that they are now devalued and many are underemployed while we keep the migrant tap on full bore.

Maybe in some locations, and for some people. The first home I bought, back in 1986, was worth approximately 6x my annual salary at the time of purchase. It is currently worth approximately 2x my current salary. Amusingly, my current home is worth just about exactly the same as my first home. In other words, I do not subscribe to the property ladder method of increasing wealth. A home should be purchased to be a place to live in, not an investment. People that treat a home purchase to be an investment tend to be disappointed over time if they compare overall returns with other investments of similar risk. The challenge is that most people do not make this comparison in a fair manner if they bother to make any comparison at all.

I am always utterly shocked how often people ignore women's participation in the labour market as a factor in house price inflation. For me, this explains much of the increase above inflation since the 80's.

In New Zealand, women's participation in the labour market has increased by 50% since 1986. However, this has been even more pronounced during the last 2 decades and as the wage gap between men and women has narrowed.

There are so many factors that have influenced house prices obviously, but the fact that the average household went from one income to two incomes will clearly have had a huge factor on house prices, yes this almost never gets mentioned.

http://women.govt.nz/work-skills/paid-and-unpaid-work/labour-force-part…

Gingerninja I think you should give me some credit for pointing this fact out many times! I believe dual incomes has made negative gearing, where a rental property's income in the early years doesn't quite cover costs, practically unnoticeable. The fact is many households have too much disposable income.

This begs the question of why the savings rate in NZ is so poor. If there is so much disposable income, then why does the typical NZ household have such a terrible track record in terms of saving?

Sorry Zach, i'm not as regular on here as you are, so I may have missed you making that point. Women joining the work force, at the high levels that they have since the mid 80's and then earning increasing wage parity is bound to have made a major contribution to house price inflation across the western world (where house buying is desirable).

Yankiwi, this is my point though. Double incomes have not ultimately led to more disposable income as such. It just led to people pushing up house prices and therefore that extra money becoming subsumed by the mortgage payment.

I would think it has had more of an impact on single income families and those on benefits. These people would have little disposable income after living costs whereas above average dual income folk are quite comfortable even with high value mortgages.

This makes you wonder about the notion of equality. How can you have equality with different lifestyles? Those with strong parental support with in-house childcare services would have an advantage also. We are never going to get away from inequalities in the system.

You could even take this a step further and ponder the economic advantages of threesomes and so on.

Zachary,

I'm not referring to inequality but why house price inflation since the mid-80's has risen above the previous historical long term trend.

I think if you look at house price inflation adjusted for inflation since the mid 80's, it's valid to suggest that dual income is a major factor in pushing up house prices beyond the previous long term trend.

Two incomes, bank offers you a higher mortgage, so you can afford to bid, tender or negotiate higher on the house you want. Once upon a time, the majority of families could afford to buy a house on one income. My parents are boomers and all my friends parents are boomers. All our mum's were either stay at home parents or very part time and then joined the work force full time mid-to-late 80's but all our first family homes were typically purchased and afforded on one income. That would never happen now. Those two incomes just became subsumed by the house price increases.

In terms of inequality though, how about this anecdotal story....My husbands Dad, head teacher, wife stay at home parent to three sons, built a 4 bed house, 2 large reception rooms in West Harbour, with swimming pool on a teacher salary.

My parents-in-law now rent that house out to two couples (all four of them are teachers). Rents are supposedly affordable in Auckland (comparable to house prices) but even then, the irony cannot be lost. 4 GenX/Y teachers (without kids) renting the same house that one baby boomer teacher could afford to buy the generation previously. Generational inequality is a much bigger factor than "class/income" inequality at this particular time. My husband's parents also managed to afford several long holidays in Europe with their three sons on those teacher salaries, including Disneyland. They also paid their mortgage off 15 years early. Not a chance in hell any teacher now would have that kind of disposable income, even with the dual incomes.

You are right Zachary. IRD just refunded me over $10k for my tax-return due to losses made on my investment properties and I am not sure what to do with the money. I am tempting to buy a spa pool and build a pergola in my courtyard just for the sake of it.

I would think that the 10k should be churned back into the property company account. Your 'problem' is that you have too much money from other income sources. Maybe it is time to invest in theses mysterious equities/shares or become a philanthropist?

Jeepers - what kind of actual loss did you have to make to get that refund! Spend the money on RE commission and get out of some of the loss making assets would be my recommendation. Otherwise you won't only have these huge operational losses, but you'll also end up with massive capital losses as well.

In theory, could Darklords all drop rents and claim additional losses? Wouldn't this achieve the same outcome as National simply increasing subsidies while Darklords increase rents? If they could, then Darklords could truly call themselves the hero's of society - the ball would then be back in the governments court in terms of finding a real solution to the current housing issue. I guess the government would have to increase taxes to pay for the Darklords additional losses...and so we go around in circles..

Never thought about that - the fact that taxpayers are funding subsidies on loss making assets - what a stupid idea that is.

Perhaps only private businesses that are returning a profit should be able to house those needing accommodation supplements.

and did we not cut subsidies to farmers for the same reason, many farmers would be looking at the accommodation supplement through bewildered eyes as to how the state could go backwards to subsidizing unprofitable businesses again

You will get 1/2 a spa and no pergola for 10k. Inflation.

The increased household income from double incomes should only lead to an increase if the supply is controlled by a profit maximising monopoly.

Otherwise would you expect the cost of avocadoss and refrigerators to also skyrocket?

Have you not noticed - housing in NZ is a profit maximising monopoly? Government backed...

Costs become greater than Darklord profit - government allows negative gearing.

Supply doesn't meet demand - government provide accommodation supplements that flow to Darklords pockets.

Such belief, because it has been growing for a long time in the past, so it will continue to do so in the future, is the very fundamental error caused the Black Monday, GFC, and more.

While the risk of a correction in the market is getting greater, such belief stops people from realising the actual risk but to under-estimate the unthinkable to happen.

What a real estate agent would do is, however, viewing over a full 50+ year timeframe and tell his/her client the market always goes up so not to worry.

like the view from the top of a seneca cliff

https://1.bp.blogspot.com/-9kjKr_S0S14/WSbafG1kYZI/AAAAAAAAVIA/5PcXLgfr…

{kind=link}

Double GZ: 10k tax return equals at least 30k in losses! I think I'd put that 10k somewhere safe if I was you, you might need it!

The problem with this type of analysis is that you can pick your start year to suit your needs. Choosing 1968 as a start year would tell a completely different story to 1963

The *money* chart that supports the conjecture made in this article is the last chart, showing the % annual change. Removing the first 5 years just gets rid of the huge downward spike on one year on this chart. The remainder of this chart remains unchanged.

Of course, removing this data point minimizes one interesting aspect. The aspect of risk to equity in property investment.

Interesting data. The thing I take out of it, is the lack of any real crash (Outside of the adjusted1968). Rather the "crash"es for want of a better word, appear to be instant stabilisations, that then last for a few years.

Even if we experience that sort of crash again, it still wont benefit FHB, or those struggling to find a roof of their own.

An actual crash (i.e. actual house prices drop >15% would appear to be unlikely, but if it were too happen... wow, that would be some disaster. I somehow think house prices will be a minor concern compared to everything else that would be going on.

Why is a property value drop of 30% some sort of disaster? That just rolls back the property values a few years. I really do not understand why this would be any issue of significance or hardship for most people. Unless you were one of the latest greater fools, all a 30% reduction in value means is that some of your paper wealth gains wasn't eventuated. That is, unless you are one of the fools that used this paper wealth to finance a lifestyle that is beyond their income.

But I think that is exactly the point Yankiwi.

Lots of people have been withdrawing equity from their houses. The huge increase in household debt is indicative of this. They have also been using the equity to buy additional properties. So if there was a 30% loss that would be across numerous properties for a lot of people.

And house prices had their most rapid increase over the last few years, so a lot of people would left in negative equity in that kind of scenario.

Personally though, I am not forecasting a massive correction. The party might be over for awhile, but some other factors would have to come into play for a massive correction, otherwise everyone will just sit tight and prices will slow or stagnate for ages. Although, global volatility is very high, so there is a good chance other factors will come in to play. I'm not placing any bets!

Oh, the fun and entertainment of leverage. The usage of leverage has risk involved. I have zero sympathy for the losses caused by foolish behavior. A few years rollback of value should not be anything resembling disaster to a prudent investor, and shouldn't even be noticed by a prudent homeowner.

On the other hand, greedy and irrational property speculators may have issues. It is a rather pointed hint that banks are now requiring significant down payments as they do not want to be the bagholder when (not if) the market reverses. Of course, it is anyones guess as to the amount of retrenchment or the timing. I've my opinion, as do many other people.

It's not the house price drop itself that is the problem. It all the related factors that would lead to it.

I am guessing mass unemployment, shares tanking, banks in mortal trouble.

Now imagine the bank you have a mortgage with, wants the money back now - and your house is worth 30% less. That is cash out of your pocket - with interest.

Can anyone explain why, between 1967 and 1968, there was a small increase in nominal house prices, yet a massive 51% drop in real house prices. Implies a one-off massive CPI inflation that year, which seems implausible.

Currency float decimalisation

I think the data has been put together back to front which skews the presentation. Shiller used a base 100 index (for 1890) when he worked out the real house price growth in the US in his book Irrational Exuberance - and the bubble they had there sticks out like a sore thumb.

Real House Price Growth for the USA:

http://www.gmregroup.com/agent_files/graph.jpg

All kinds of things hidden in those averages. Anyone remember that period in the late 80s/early 90s when they were giving houses in Bluff away for $1 in a desperate attempt to get people to move there, and there was a suspected serial arsonist in Invercargill which turned out to be people desperate to get out of there who couldn't sell their houses?

I suspect many think of Auckland when talking about the last four years. Unfortunately there is no Auckland specific CPI.

But the National CPI has barely moved over the past four years, while Auckland average house prices are up 65% since May 2013. I guess that is about 13% growth per annum (hard to compound in my head, but whatevs), sustained over four years. That seems unprecedented.

Nice! If only...

I'm a bit staggered by the innumeracy to be honest. The article seems to invite a direct comparison between the third graph and the previous two. But the third graph is showing the rate of change, rather than the total prices so it's completely different. It's a bit like trying to talk your way out of a speeding ticket by claiming that the needle on your speedo may have been at 130, but it was barely increasing at the time the speed camera snapped you.

Graph three merely shows us that, "increases from a low base look proportionately higher than increases from a high base." Take 1974 for instance, prices went up 27.8% more than three times faster than 2016's 8.2%! But that represents an increase of $45k in inflation adjusted dollars, which is only a little more than the with the 2016 increase of $38k. Remember these are inflation adjusted figures so should be directly comparable. And I suspect the 70s numbers are weirdly affected by the 1968 outlier, where the decimalization inflation adjustment halved the base to make later changes look even more dramatic.

For me the green line in the second graph is where the action is, and the really interesting thing that should have been the third graph would have been to plot this as a multiple of the inflation-adjusted household income.

Innumeracy indeed.

I agree, it would be nice to see the home price to household income (not sure as to whether one cares about adjusting for inflation as it affects the numerator and denominator in exactly the same ratio).

The rate of change of the green curve in the second chart is the important aspect (numerates call this the derivative). I'd suggest that a gain of $45k on a base value of $208k is in fact a much more significant gain than a gain of $38k when the base value is $496. Hence the usage of percentage values in chart 3.

Using velocity as an analogy is not an apt analogy IMO. That analogy assumes an invariant absolute "safe" boundary. In reality, the safe boundary is a function of income and interest rate.

Conrad and Yankiwi,

Totally agree, really good points. It would be fantastic to see the second chart with additional data ohouse affordability over the time period. I wouldn't want to say income multiples because mortgage rates are such a huge factor in housing affordability, so it would need to be based on the percentage of income being spent on the mortgage.

It would also be nice to see incomes adjusted for inflation over the same time period.

Plus, women's participation in the work force, compared to house affordability.

Plus savings rates and household spending (adjusted for inflation) over the same time period (in response to Zachary's notion that higher income + double income families have more disposable income now than a higher income single earner in previous generations).

I have seen a article, and I can't remember where, that suggested that all the verbiage about Millennials and their flat whites and smashed avocados being the cause of their dropping home ownership rates was unfounded, because Boomers spent more, had more consumer debt and less savings than Millennials, so it couldn't be true that Millennials were just entitled and frivolous to be the cause of their current home ownership woes. I'll have to see if I can find it and go back to what that article based its data on.

I think we had a comment thread on this note by MIchael Vink that shows that Millennials are saving at higher rate than any previous generation at the same stage of their lives.

http://www.treasury.govt.nz/publications/research-policy/staff-insights…

Is this the one you were looking for?

https://www.greaterauckland.org.nz/2017/03/07/no-boomers-its-not-like-i…

Wildcard, yup, that's the one, I was remembering. Thanks

Tracking these prices without also tracking incomes in the same way seems completely pointless to me?

Without incomes being factored in how is relative affordability at any given time period measured?

The green line on the second graph shows that the real value of the median NZ house has increased from about $400,000 in 2007 to about $500,000 in 2017. That's a 25 per cent increase in the real value in a decade. Not too many classes of asset/commodity have shown an increase of that magnitude. (But, of course, the graph says nothing about regional differences.)

Many commodities - for example, new cars - have shown a significant decrease in real price over the last decade (and even more so over the last two decades).

So, I'm not to sure what the moral of David Chaston's story is?? Could there be a suggestion that further gains in house prices at this juncture wouldn't be extraordinary......

Anyway, based on the track record, houses would seem to be a pretty good long-term investment - albeit there will always be large differences according to locality.

Thanks David, for your worthy contribution. Interesting to think about. And a goodly lot of comments above!

Good work DC. My take on tbis is that last century - since 63 - real price bumbled along, up n down, at much the same level - which is as it should be. But this century they have shot up. A social disaster.

Applying a 40 year trend line to real house values from 1963-2003 (if that holds any value) might show that housing in 2016-2017 is around 40% overvalued based on that 40 year trend. But then again one might consider that history should hold no value in determining current/future housing prices. If that argument is true, I get confused because that would conflict directly with the opinion of the property bulls who claim that historical trends should be applied directly to the future when predicting house prices (housing has always gone up in the past, so it shall continue to go up...). But I look at the past real values, 1963 - 2003 and historically they haven't gone anywhere - so I apply the bulls argument and say they won't go anywhere in the future. I end up asking myself, does history hold no value at all when predicting the future, in which case the only thing I can decide upon is that the bulls argument of applying the past to the future is a fallacy...and therefore everything that is happening in the current market is speculation because past trends can't be relied upon for predicting future values.

Hmm.....

The 40% increase could be pretty easily explained in one way. Back in 63, most households would have had a single income earner. But in 2017, most households are likely to have two income earners, so people can afford to spend double on theoir house when there is a supply shortage. This mixed with low interest rates for borrowing, whereas in 63, people didn't borrow anywhere near as much. So the question is, is NZ better off as a country by having both parents working?

But if we're earning so much more - why do we have so much debt...? Shouldn't debt be disappearing at the same/similar rate that it's generated if you use the argument that greater income is pushing prices higher?

Or are we speculating that a man will have two wives at some point soon in the future that he can 'send out to work' as Zach Smith puts it. and pay off the extra debt?

Good point as always follow the money.

Clearly houses are less affordable so incomes have not increased at the same rate as house prices in the last few years (if not longer)

Some incomes are much higher, having risen faster than inflation and house prices, but i think most have not.

The fact that you need two incomes and 48% of the combined income to buy a basic house in Auckland is all the proof you need, 25 years ago it was one income and less than 40% of a single income

I have also been making this exact point.

And no, I do not think we as a society are necessarily better off. Families no longer often have the choice to afford a stay at home parent, even for those families when it would be better for the kids and would vastly reduce various psychological and emotional burdens on the parents. Some mothers and fathers would like the opportunity to spend crucial years at home with their children and they simply can't afford it.

My take on all this is that Graphs 1 and 2 show the early stages of an exponential function (https://1.bp.blogspot.com/-u03Lmy4qOf0/Ucg-wXuyKEI/AAAAAAAAADo/wyGQcs-c…).

{kind=link}

In other words, x in the exponential function here is the mean long-term annual growth value shown in Graph 3, which I calculated as being 1.91% over the entire dataset since 1963, by putting it into an Excel table.

Trouble is, exponential functions in closed systems simply cannot carry on forever. So what's the outcome? A crash into some kind of limit.

Thank you very much for this data David.

As I've claimed many times before it shows that houses in NZ roughly double every 12 years (of course with some steeper increases and some stagnant periods) which equates to an average compound increase of 5% and that there has NOT been a significant crash for as long as the data exists.

Sure, the market is overcooked now and it may decline a little or stay stagnant for a while and just as surely, houses will be much more expensive in another 12 years time. "it's different this time" won't happen.

I'm not saying it's fair or it's right, I agree it's hard for FHB that house values outstrip wage growth but nevertheless it's fact that, over the long term, NZ houses increase at about 5% pa

History is interesting, but i am more interested in the future. Maybe this is what the future holds http://www.radionz.co.nz/audio/player?audio_id=201845436

Steve Keen is always worth listening to. I'm not going to bet against his prediction of a crash in the NZ housing market within 1 to 2 years. .

You got me S R. I wasted 32 minutes listening to your radio link... highly theoretical and much about semantics. If anyone wants to listen to the radio link, there is a brief mention of the NZ housing market at about 18 minutes in

One factor that you have to build in is that house sizes have been growing and houses are also becoming more complex to construct. Regardless of inflationary impacts, a new house constructed today is likely to be twice the size of one built in the 1950's, plus have more complex kitchen and bathrooms. This is on top of the double glazing and insulation. what we have seen is a trend for two income families and with that a growing preference for larger more complex houses. However, I think the burst of price increases in the past ten years is beyond the change in size. However, the ability to build to meet demand has been constrained by the added complexity of building regulations which has also added to prices.

Indeed people want, safe, warm housing. Ignore the regulations though, speculative demand, the price of land and its development costs looks like the biggest drivers in prices.

As an example of the spectacular speculative impact a parasitic financial sector can have we can look at oil in July 2008, driven up be an increasing shortage starting in 2004 peaking in 2008 at almost $150USD a barrel. Then it popped as demand collapsed and prices dropped a long way.

So if we ever take out immigration and stop allowing foreign ownership in land I think we'll see significant price drops.

Try finding a section where you can build something like a Universal Home from the 70s or place a relocatable.

Problem with the data set is the fact that the reported CPI figure was altered substantially in 1999 when RBNZ removed the land price growth rate from the CPI so the post 1999 CPI data doesn't reflect the same calculation of CPI that was used in the cycles prior to 1999. However that doesn't alter the fact that this boom (since 2013) has been much milder than the previous one (2002-2007). Whilst the data is NZ wide it clearly reveals that this cycle has so far delivered relatively low growth cyclically compared to the last property cycles. This boom is not over yet even though it may look that way at present, the high net migration and lack of adequate building consents to satisfy demand will continue to fuel the tail end of this boom. Whilst 2017 will likely show a significant drop in capital growth rates its likely we will see double digit growth in 2018 and maybe even 2019 before the real slump arrives in earnest.

Its not a problem taking out land, it allows a better gauge of the overall health of our economy.

Not sure about the boom not being over, I think there are a lot of people doing wishful thinking and gambling it isnt. So after watching this for over a decade my personal conclusion is I cant see any sound way to measure how the market is going to do. However the recent tax cuts proposed by National in the budget are a tested and true way to pork the system. Giving tax cuts or FHB cash bonuses seems to work every time to recover a flagging housing market, so if National wins in September (and I think they will) I think your projection is very reasonable. If however Labour wins it would be run for the hills time.

I tend to agree with u KJ..

CPI is not a good deflator to use to determine "real house prices".

The simple fact that building cost inflation is generally much higher than the CPI is reason enuf.

Also... my own view is that Land prices (locational value of the land component of Housing ) are somewhat related to Money supply growth.

ie. Land prices might be a better proxy for measuring the effects of monetary inflation than is the CPI. ( especially so, in a Global world )...??

I tend to agree that boom is not over yet.. After this slight downturn/rest period , we will get the tail end of the boom (going into what some call the "winners curse' part of the cycle )... as you say.

at the moment our economy looks ok..

AND.... I am thinking that we we finally do peak ( I'm thinking 2025ish) ...we will get some sort of crash, some real hardship...?? ( ie.. A Real Estate crash will cause a severe recession, , and Bank stress )

just my view... which changes often..

cheers

Yeah except for the not so minor weekly dividend called rent, and although the yield has been falling, it is a non trivial, albeit missing part of the equation.

Exactly Kjfreeman. Why did they take the cost of land and houses out of the CPI ???

It beggars belief - who cares what the cost of a pint of milk is when housing just tripled in value.

The game is rigged my friends...

If we were to do something as stupid as having land and houses in CPI what do you think the impact would be?

Its simple really you dont seem to understand why the CPI is monitored let alone all the exceptions to the "crazy" price increases you would have to monitor to get what you are really after. ie CPI is monitored to gauge the health of the economy and determine the OCR overall and not for some specific sectors and areas in that where people are being silly.

Example, I have owned my property over 20 years, its inflationary effect has no impact on my spending ability, ergo CPI for me and indeed many other people (if not most) is not impacted, ergo its pointless it being in CPI.

Now if you want to monitor this and make your own financial decisions based on it, fill your boots.

My understanding is that the CPI is primarily a Monetary tool used by Central Banks to monitor the effects of Monetary inflation ( money supply growth ),.

One of their mandates is to maintain "Price stability "... ie.. maintain the purchasing power value of money.

(The CPI is only an index of consumer prices.. and does not represent all of the ares where Monetary inflation can manifest..)

ALL... of the great professional investors I follow , share this view of the purpose of the CPI..

This allows them to see the dangers of a myopic view of the CPI = inflation , and they are all "watchers" of the credit and monetary aggregates..

One of my favorites ( for understanding the current climate) is Ray Dalio.... also Gary Shilling..

If u want to check out how the changes in how CPI is measured , look today, check out this graph.. ( it is for USA )

Can I confirm whether the impact of GST (or other Tax changes) have been backed out of the CPI figures.

IMO these should be removed.

Did you allow for the fact that official CPI removed house and land prices in the late 1990s?

Hi David. Are you sure about the data for the 51.4% drop in 1968? This doesn't seem to match the data that Brian Easton is using here https://www.interest.co.nz/opinion/88343/brian-easton-analyses-house-pr…. I suspect this might be an issue with the shift to decimalization that someone has previously raised.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.