Even if the Reserve Bank did remove its restrictions on low deposit mortgages it would make little difference to first home buyers, BNZ chief economist Tony Alexander argues.

With Prime Minister Bill English and Labour Party Leader Jacinda Ardern both in election campaign mode, this week they said they'd like to see the Reserve Bank imposed restrictions on banks' high loan-to-value ratio (LVR) residential mortgage lending removed for first home buyers. Both politicians said the LVR restrictions had made it harder for would-be first home buyers to get into the housing market. English and Ardern's comments follow real estate agents, with sales volumes down 25% nationally and 31% in Auckland, lobbying for the LVR restrictions to be loosened.

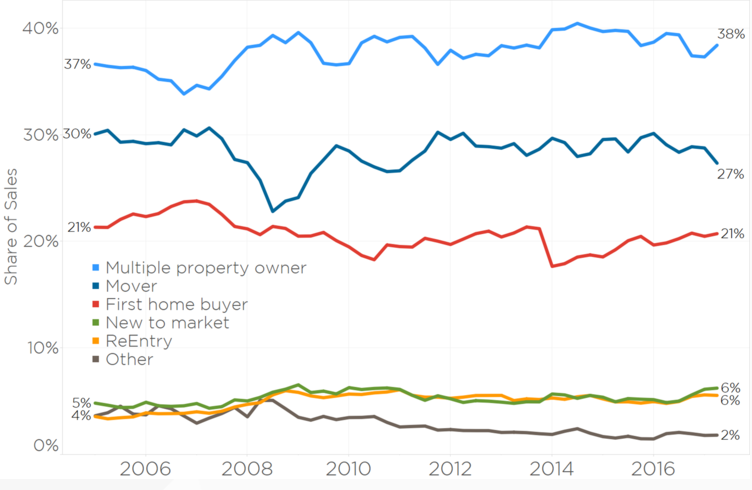

However, Alexander says based on Core Logic data first home buyers bought 21% of the dwellings sold during the June quarter. This, he points out (see chart below), is the same percentage as just before the LVR restrictions were introduced in October 2013.

"Compared to a year ago when annual dwelling sales were near 95,000, the proportion accounted for by first home buyers was around 20%. So there is no obvious disproportionate fall in sales to first home buyers," says Alexander.

"Note that during the year to April 2017, 15,400 people used the KiwiSaver HomeStart scheme which lets KiwiSaver members access their funds and receive a grant to purchase a first house. There were 85,000 dwelling sales by REINZ members in the year to April."

"HomeStart users therefore accounted for 18% of all sales. Feedback we get suggests that the reasons first home buyers are buying fewer dwellings now than one, two and three years ago is that the house prices are too high and the loans they would need to take out too frighteningly big. Meeting debt servicing requirements from lenders, which are being steadily tightened, also means some cannot qualify for a loan even if they have a 20% deposit," Alexander says.

The July Real Estate Institute of New Zealand figures show a national median sales price of $518,000, meaning a 20% deposit would be $103,600. The Auckland median price was $830,000 for which a 20% deposit would be $166,000.

Alexander points out that it's worth remembering that banks can do up to 10% of their lending with deposits of less than 20%, and suggests a quarter of first home buyers have a deposit of less than 20%. Additionally Alexander says first home buyers account for nearly half all loans with less than a 20% deposit, up from one-third a couple of years ago.

"Therefore, even without debating whether the housing market has slowed enough for the Reserve Bank to make special exemptions for first home buyers, we can reasonably say that LVR rules don’t necessarily seem to be what is holding all of them back."

Thus he says if the Reserve Bank did ease LVR restrictions for first home buyers, it would make little difference.

When the LVR restrictions were introduced in 2013 the Reserve Bank said they were a temporary measure. Governor Graeme Wheeler said; "How long LVR restrictions may remain in place depends on the effectiveness of the measures in restraining the growth in housing lending and house price inflation. LVR limits will be removed if there is evidence of a better balance in the housing market and we are confident that their removal would not lead to a resurgence of housing credit and demand."

Volumes sold - REINZ

Select chart tabs

119 Comments

Ah but it does make some difference at the margin. If FHBs were able to load up on mega mortgages with small deposits, that would act as a safety valve of sorts for the over leveraged speculators who desperately need to off load.

It's not every speculator that needs to sell...the industry just needs enough new entrants to mop up all of the mortgagee crap that will come to market.

If you can't afford a house in Auckland, you don't deserve a house in Auckland. Crybaby snowflakes want Mummy's help to buy a house. T_T

Crybaby snowflakes wants to avoid an investment as stupid as Auckland housing right now and leave it to the dumb money.

Go buy some more houses, trust me you deserve it. (^_^)

Tell that to the minimum wage workers who keep the lights on, teachers and (as it is now so bad), junior doctors. Maybe they should all leave Auckland and see how well it gets on.

Two teachers have household income no less than $120,000 yeah? And junior doctors can make over 80k.

You pointed me to an article from the RBNZ, dealing with DTI's, 39 pages ill note, and said it was 'a good place to start' in terms of LVR restrictions for some reason.

I have read it and found that the document is almost entirely dedicated to DTI's with some casual references to LVRs. The LVR section is an extremely poor resource for LVR impacts and is not at all the focus of the document. The whole document is completely in agreement with what ive been saying, which is that DTI's would not be implemented in falling market, and it fails to address my criticisms (other than when it tacitly agrees FHB should be partially exempted from DTI's, but notes that servicing isnt usually their problem, i.e. LVRs are) from its implementation of the LVR restriction, which are that it shut FHB out from lower prices, delayed them and they ended up buying later at higher prices, causing harm. As ive noted many times LVR restrictions are absolutely fine if FHB are exempted, as are DTI's if overseas buying is banned. I am specifically criticizing the failure to exempt FHB which shut them out of much lower prices.

Look at the data. LVR locked FHB out of cheap (relative term) houses and they ended up buying later, at higher prices. It was horrible and they should have been excluded.

Why should FHBs be a vehicle aid specuvestors went and got themselves over leveraged. I think the sentiment from a lot of them toward people unable to purchase in the market of the last few years deserves them every hiding they get.

They shouldn't!

Guess I didn't make that clear enough. I was trying to describe why I think the industry is lobbying for the change. TA is saying it makes no difference but I think it does (a negative difference allowing speculators to off load).

FHB should be sitting this out, whether LVRs are changed or not.

They're waiting for the big crash so they can buy quarter acre sections with new 200sqM houses on them close to the Auckland cbd for $500k.

I'd be scared if I was a FHB too. As Tony points out though the fundamentals of (lack of) supply have not changed.

Go for the low ball offers. Watch Ron Hoy Fong tutorials for sound advice on strategies to take.... But seriously any investors who bought recently and are not prepared for a 10% value drop in the short term are fools. The long game is sound.

It's a good time to clearly identify investors vs speculators.

I get the feeling many young have changed in their viewpoint. They're no longer obsessed with staying in Auckland, but are now looking around at what better equations exist both in NZ and elsewhere. They're looking at the idea of saving for years just to get into a 30 year mortgage, vs. living elsewhere where they need not be indebted for life.

They're looking at the cries of angst from Bill & Barfoot re LVRs and wondering "...but why should it be FHBs who bail you guys out?"

I got out of Auckland 10 years ago and it was the best thing I've ever done. My only regret of course was I wish I had bought a house before I left but never the less I couldn't afford to at that stage in Life. When I'm mortgage free at 40 I'm sure I'll get over it :)

Amazing no one cared less about FHB,ers over the last 4 years, included RE , now they rule the world to save the less expensive rental market, rich, shame to little to late

They're trying it on with the "appeal to pity" fallacy:

https://en.wikipedia.org/wiki/Appeal_to_pity

I cared and we warned extensively about the effect LVR rules would have on FHB. Locking them out of relatively cheap houses it forced them to wait and buy later at much higher prices. They should have been exempted from the start.

Yes they should have been exempt years ago when housing was more affordable but that would have only let even more people push the housing market up and in late 2015 and 2016 housing would still have become unaffordable to FHBers , ok a few may have got a house but it doesn't change where we are today, unaffordable, the housing market should have been rained in starting lowly in 2015, now Auckland and Tauranga are among the most unaffordable areas in the world to its locals that live here, I'm not sure what would have been the best thing to do say 3 years ago, not LVR,s maybe, not lifting interest rate ether , probably hard restrictions on overseas investors and DTI restrictions would have been the answer but to late now

Absolutely. It seems simple enough, LVR restrictions on investors, ban overseas buyers, enforce responsible lending on banks. Something like that, even broad DTI's are fine imo as long as overseas buyers are banned.

Welcome to the real world.....

If young people go they take potential future growth with them. Without young people Auckland will stagnate like crazy, whilst every other place they move to gains value.

I said the same thing in the late '80s when the catch cry was 'last one to Australia please turn out the lights'. The reality is that someone else will fill the void as they did close to 30 years ago.

Yeah, but the problem is the size of the void if you get my drift. Auckland builds slowly, with plans seemingly to keep on building slow for the next 23 years. Come back 25 years and Auckland is not going to be the big dominating city in NZ.

Tauranga will keep getting more inviting, it has the land and can build heaps cheaper and by growing now the planning for roads etc are so much better, it's hard to see how a bottle neck city like Auckland could anywhere near compete with Tauranga in years to come,

People can see that already: the PTE (Pretend Tertiary Education) visa-mill sector is filling the void, importing as many people as possible hand over fist.

Rick Strauss.

You could not be more right. I moved back to Auckland after Uni and my first year home I would have easily had 30 odd mates from Uni with me, most whom were out of towners. But 5 years on there's only a small group of us left as everyone has realized there's no future here long term, so they're all off traveling or settling in the regions. My partner and I, both Jaffa's born and bred will be gone within the year. It's currently a toss up between Tauranga ,Chirstchurch or Aus.

When you run the numbers Auckland just doesn't add up for anyone who doesn't already own a home or wants to buy one. So why stay? Aucklands stuffed, better to let the Specuvestors, Real Estate Agents and Politicians squabble amongst themselves and get on with living elsewhere.

I will miss the smashed avocardo though ;P

Avocado...the spawn of the devil and real force behind the housing crisis!

Avacado, much less expensive in Tauranga.

I think thats f...&% sad when Jaffas born and bred cant even live in their home city. People that NZ wants and need not Jaffas as such but young skilled NZers. Now we are looking at alternatives overseas.

What is wrong with this country when our first course of action is to bring people from overseas instead of plugging the gap with New Zealanders.

Eggs actly

So the only two possible outcomes are that houses close to the CBD remain $1.5m+ or drop to $500k?

Are there any other possible outcomes or does it have to be one of these?

Well they could hit $3m

Roundabout 2065 I reckon

$500k will never happen, but it's hard to hold a high price if 5 miles away is $300k cheaper, see my point

Never? What if interest rates hit 7-8% again?

Eventually they will, as people seek anything but a bank to put their money in

The PM of NZ doesn't get that... in order to grab votes, he is happy to pressure the RBNZ to make a move that could actually hurt FHB's..

He knows it's not likely to happen, he just needs to look good for a few weeks, put the idea out there, see it's working

Do these politicians actually want new FHB's to end up with negative equity?

BE already warned people not to borrow too much, and that people need to ask themsleves whether they can afford to service the debt, it rates go up.So not sure they consider that their responsibility.

What I find odd though is that the government think NZ are poor at saving, so they bring in kiwisaver, and by default people are signed up to . Eventually kiwisaver is likely to be compulsory. So basically they are saying they don't trust NZers to save for themselves. However on the other hand, we have the LVR in place to protect people from borrowing too much, which they want to see removed. They also don't want to bring in DTI ratios, which will protect buyers borrowing more than a house should be worth in a normal situation. So they don't seem to have the same protections in place to stop people getting into too much debt. So who are they trying to protect here?

They're just trying to get home owners votes, and anyway once KiwiSaver is older, 40 to 50 years , a big chunk of people won't bother with rentals, why would you bother, pump the hell out of your KiwiSaver for 50 years, maybe one rental haha, pay your home off, party party, maybe then for the first time this country will forget this boom bust, rich broke crap

Thankfully someone has stated the bloody obvious . It does not matter what the LTVR is , houses are simply too expensive, and everyone knows it .

I know someone who can afford to buy a house outright at the moment. But they consider the prices too high, so have put their money into other things. They don't want to be competing on price with all these people who are getting loans with cheap credit, beucase that has only helped to push the prices up. A pity you can't get a decent discount by paying cash these days,

I'm the same I'm looking to buy one house, one commercial and a appartments in the Gold Coast but I'm not falling for these prices, the commercial I could buy now it's come up next to one I have and they work together well

Like Machiavelli says it's a long game - a little short term negative equity shouldn't break the bank/s

Yes. And many, many people have a lot of equity today as a result of the past few years.

As for investors.. if they are investors the value of the property shouldn't change the cashflow fundamentals one bit. Rents aren't declining. If properties are bought for the income streams, which all investors are necessarily claiming, short term increases and decreases in values should not matter.

You would have to have a serious change of circumstances to have to sell right now if rental income was really your primary objective. It's time to sit on our hands.

It doesn't matter if some decide to keep there properly , people keep property all the time , People sell, but prices WILL fall , by how much ,who knows , Aucklands cheaper housing mighted be that bad , maybe 30% drop, because of FHBers , renters going to homeowners, like for like, but in parts of Auckland theres areas gone up 2 to 5 times over 10 to 13 years , madness, and just as worrying outside Auckland, Tauranga has hit 9.7 times income, this money came from Auckland and has stopped on a dime , normally locals in these towns could never keep pace with these prices, add to that plenty of towns outside Auckland have had building booms because they start building so fast, now the supply is threw the roof and the money gone, thank national and the RBNZ for this stupidity, Jacinda has a nice smile , there might be some pain coming but as a country we better come to our senses, low home prices are a lot better way, better for our kids, makes no difference when people buy on the same market, and for a long term investor it great, plus mortgages are less so people have more money in there pockets for buying what People make and happy to live, did I mention Jacinda,s smile

With just a 10% deposit your Auckland FHB will be able to procure a median priced home (including rates and insurance, of course) for just $1300 a WEEK... (made a correction from $1700 I had earlier, but even cheaper at the price) . Household income will need to be 200K a year... easy peasy! Go for it guys, buy two! What could possibly go wrong...

"Housing has never been more affordable! Whippersnappers just need to cancel their sky tele and stop eating smashed avocado!"

I thought we were to drugged up to work?

Haha

As per Tony Alexander's recommendation to buy a meth contaminated house they are drugged up enough to work. All that meth has boosted productivity.

You just lick the walls every morning before setting off to work

Time to harden up and stop eating and sleeping all 'yous' young ones...tothepoint/eco bird said it was because they bought "...beer and pizza on a Friday night." Some people /person have been working as qualified engineers and doing do-ups every hour they are off, including those 7 hours when ever one should sleep, since they were 12, just ask Zac/Double GZ....

They were smashing them AND eating them, what is this world coming to?

@blue meanie Your numbers are a bit wiffy sir. Payments would be about $1,000 p.w. plus about $70 p.w. in insurance costs. A nurse and a police man both working full time make about $140,000 per year combined. Those incomes will clear servicing and see a loan issued. The loan is costing them $55,000 per year, which is 50% of their after tax income. Thats the reality of a median priced home in Auckland today. Im not thrilled by that but its an accurate set of numbers at least.

The rent for that home would be about $650 p.w. while the interest cost in the first year is $793 p.w. So compared to renting its probably still pretty attractive long term.

The family would have $1,000 net each week to live on.

ah good observation Laminar, thanks for pointing that out... I'll correct the figures... it's $1350 a week for a 900k @ 5.5% over 25 years (won't get lower because of being at a higher risk of defaulting - apparently) house with rates and insurance... and salaries still will have to be $200k... call a bank or broker and ask..

No, a teacher and a policeman will NOT be able to afford a million $ house... unless one is an inspector and the other a principal...

Is that 200k after tax and with two people working? Considering the median household income in NZ is something like 60k, a couple would have to be doing really well to be earning that sort of coin, and would likely be in the minority.

Chief Wankers of the year awards. In a week that the Chief economist, the Chief real estate agent and the self anointed Chief squirrel, all find media coverage lamenting first home buyers and LVR's, the in fighting starts. As the pie suddenly shrinks, we have the hair dyed Alexander, the corpulent Thompson and the effeminate leather clad Bolton . With the icing being removed from the cake, all these bottom feeders want it back ,layers of it, they deserve it apparently. Auckland has been built on decades of house lust, granite and wood chip and these cosy groups have enjoyed the gains. Now with prices and volumes fading fast, the story is so much harder to sell, the plebs fewer, and the hard data increasingly difficult to hide. The current portrayal of these three groups is so consistent with other global real estate crashes, when vested interests start to pick each other apart. There was a time two decades ago that the majority of Kiwi's could purchase an Auckland home, now the majority of Aucklander's cannot afford an Auckland home. The first to go, will be the mortgage brokers ,squirrels will be found in the parks,so it will be unfair to give them an award. A collection of cowpats will comprise the award.

Can the awards be presented at speed through the medium of air?

I may require some P2P lending to facilitate transport, an interest only loan to cover heavily fertilised pasture and a Barfoot's advertising hoarding ,( with happy agent face,) to load material and facilitate use as frisbee.

How correct. Irrespective of the deposit if the house is a million plus and do manage to get $200000 deposit- How does one service a mortgage of $800000 as the weekly installment will be $1000 or Plus depending and what happen whenever the interest rate goes up in next year or two.

Either the speculators and Investors, money launderers have to enter again and play or the house price has to fall, which is happening, now

You have two full time workers on 70K plus. That leaves them with about $1,000 per week to live.

Should solve the population problem. DINKE. double income no kids EVER.

God bless Bill English and the banks.

Less student loans $12000/year, rates $3000, insurance $1600, transport to work $4000 already its $640/week. Childcare is another $200/week/child. Food $200/week, electric $50/week, internet $20/week, water $20/week. If you have two children, you are now at -$50/week excluding clothes, house repairs, haircuts, any sort of entertainment or activities.

Where do I sign up?

Well student loans are pretty clearly identifiable as the problem in your example and it is indeed a problem. Food would be more like $300 p.w. i would think.

FHBers would eat $300 a week in McDonald's for starters, something else every FHBers different, as house prices go down they don't need to try and enter at where ever the bottom might be, for some if they see a house for a reasonable price , do the math with stopping paying rent, travel cost might be cheaper, there might be the opportunity for a boarder but don't take stupid risks, interest rates could go up one day, some I here would say if you don't take risk you'll never get a house, nz shouldn't be like that, Theres some on here didn't take any risk but make out that they have , just share luck

Stupidly risky when you might as well do the wait and see thing, there's a real possibility a FHB ,er could save well over a $100k in only the first year of this correction, look how much is it so far and wait to after the election,

How many families have family income of $140000 plus.

I understand most national supporters and friends do have that type of salary as a result think differently and justifies national policies.

Well most families dont even have two full time workers but he asked how do you service that loan and the answer is with two full time workers on 70k plus.

2 full-time workers on $70k+ with no student loans and no kids

If you have a polyamorous relationship with 2 full time workers on $70k+ then the third person could look after the kids. Although student loans wouldn't work.

So really Bill English's preferred FHB are same sex couples or numerous people in polyamorous relationships without any tertiary qualifications. That sounds very progressive although I wonder if the Pope would approve.

Back up plan was importing a demographic of one husband with multiple wives. Unfortunately, plan didn't work because the husband doesn't permit his wives to work.

Your 70k is wrong... Laminar, as I have said, ask a bank what you need to earn to pay off a 900k house... I make 110000 and with a 20% deposit they will loan 400K... at the moment...

Maybe 10 Juggalos earning $20k per year could afford a house in Auckland in that case. I'm sure Tony Alexander would approve.

One average income, wife stays at home with our two pre school children and we can borrow $180k from the bank.

For all those who think that long-term Auckland prices will continue upwards, what multiple of income do you consider the ceiling?

@kiwimm ...........Forget mulitples of income as a measure of affordability, attendance at Auctions is still largely an Asian affair, and according to my sources , they are still buying either for cash or with very low borrowings.

Kiwis are now locked out due to :-

Being displaced by massive immigration numbers

Being poorer than most Asian migrants.

Interest rates that are higher than one can borrow in Hong Kong

LTVR requirements which are a massive hurdle for Kiwis and actually help migrants with money to get ahead of them .

@Boatman... interesting you say that because these Asians would be risking prosecution and jail time as per the many many many links that CJ099 has provided on clamping of Chinese capital flight.

But let's say your sources are correct and there are still the rogue one or two money launderers around. Well then they sure as heck ain't making a dent on the market as 43% clearance rates, according to this website, is the new normal.

So to correct your statement, Kiwis WERE locked out due to the reasons you listed, but now we are not.

Therefore kiwimm has asked the right question here as MOST buyers left now are FHBs and local, working Kiwis. If history serves us correct, I bet we'll see prices go back down to affordable levels at around 5-7 times income, not the current 10-11 we have now.

@ RichMuhlach would like to know how we will ever get it back to 5 x annual income .

A decent flat 500m2 section alone costs $500k to $800k , thats a huge multiple of the median wage in Auckland .

Just a water connection to a new section from Watercare costs and eye-watering $15,000

there are a number of ways ... LVTs could be introduced to break up land banking, forcing specuvestors to sell

or it could be that costs of NEW houses will remain expensive, but all the old houses can be had for much less, therefore bringing the overall prices down

another report from realestate.co.nz mentioned apartment listings for June 2017 are double on May 2017, and with the low clearance rates it can only suggest that we will have an oversupply of apartments soon, thus pushing the prices of housing even further

I think you're on the right track, you correctly highlight that land costs and building costs are extremely high - but the whole market is not dictated by new housing only. What we'll see is a return to more affordable levels, and realistically it's just house prices going back to what they were, say, 5 years ago before this astronomical rise in house prices happened.

So no more Ranui mansions at $800k, I suspect those would go back down to $400k or $500k real quick

But houses in the more central areas of Auckland will still be valued at $1M+++

@ Boatman, RichMuhlach is quite correct in what he's saying and those land and even construction costs will just gradually deflate along with property prices. I saw the same thing happen in the UK during the GFC.

You could also take a look at Canada, since they've been effected by the same market forces that has affected our over inflated market.

Look at Toronto, their construction costs are deflating at a rapid rate without the huge overseas investment money to keep them afloat. Apparently the cost of a new construction in Toronto has dropped by -20% already.

article: Toronto New Construction Prices See The Worst July Since 1993

https://betterdwelling.com/city/toronto/toronto-new-construction-prices…

Give me an interest rate and ill give you a ceiling.

5%

Let's all rise up and make the $2M DGZ villas $500K for the FHB's.

Sharpen ye pitchforks

Hi DGZ,

And a relaxing weekend to you.

The problem with your proposal (above) is that some people who come here are deluded enough to think it's already happened.

But I see house prices in GZ are holding up very well.

Hi tothepoint,

You write: "some people who come here are deluded enough to think it's already happened."

Can you please provide a quote / evidence from AT LEAST ONE PERSON who has said double grammar zone houses that were worth $2M are now only worth $500k as you have asserted.

Otherwise please feel free to retract your incorrect statement.

Hi RichMuhlach,

There's a whole bunch of left-wing losers who visit here and fantasise about Auckland house prices plunging to unrealistically low values - as you must surely know.

I think my comment articulates the point well enough.

Leftwing yes, loser potentially, depends on who you speak to, the bank would lend me & mine over $1m without difficulty. Question I ask myself is if I had that much money in a suitcase would I hand it over for some of the houses on offer? Am I then prepared to pay almost double that back to the bank? Answer - definitely not, houses are over-priced, simple.

Left wing losers.

Nice way to articulate yourself TTP with people who disagree with your philosophy of unlimited house price increases.

Any view not yours makes people Left wing losers. Personally Im a sports and beer enthusiast, that looks forward to houses that are affordable for most NZers, and house price increases that move along with average NZ wages. If this is left wing, then tar me with that brush. I do support Counties so we do lose the odd game here and there. But win or lose I love watching Counties play.

Left or Right, not everything is about house prices. Give it a break.

I don't think anyone has said they want that Zac...

Err wouldn't that be $4-5m that should be $2-2.5.....?

Viva la revolution !

God they call anything a villa these days, I sore a house the other day a RE agent was calling a villa, what a joke, it was a 1950s weather board house with a tin roof that was as boring as hell, I have a 1930s house with push up windows and next to each and everyone one of those windows is a up and down window that open out, that's not even a villa, I'm not even sure we should be calling any of our early 1900s houses villas , really most are 100 year old colonial with balconies which is perfectly fine, villa was I think Spanish square two story but have changed a lot over time, Ozzie had the Queenslander and federation houses, in nzs now terms I would call a villa a house around 1900 to about 1930s with balconies at front and rolled balcony roof, maybe some colonial bits around posts and rails and push up and normally pull down windows, large as weather boards, big chimneys sometimes 2 or 3 , maybe leadlite , some in nz can be very small and dark , there are some of the finest ones in Auckland and personal worth every cent of even today's money , but you need to compare apples with apples, some are tinny cold little rooms tinny chopped up sections ,

July sales figures just emailed to me. Kohimarama sales/CV 141%, 141%, 136%, 141%, 143%, 143%, 142%. June was the second highest turnover month of the year to date with 15 sales totalling $28.5 million.

People with a lot of money still have plenty of money?

They appear to. Apart from noting the neighbourhood is older and often empty nesters I have no idea where the buyers have come from or how they can afford these prices. Based on volumes we're only talking about 130 buyers per year in Kohi. The wider Bays area is close to 630 sales per year.

Hahahahaha, whatevs, Tony.

1. Price out FHBs, tell them to go eff themselves

2. Realise that you need new entrants at bottom of pyramid or the whole thing collapses, oh crap,

3. Import replacement base of buyers for speculative frenzy

4. Imported buyers disappear

5. Need new crowd of suckers to come to the rescue with buckets of money and boxes of stupid

6. FHBs are all LOL no, not my problem, laters Tony, now go away and let me eat my avocado toast in peace

7. Banks and speculators panic and freak out

8. Government stand slackjawed with fingers up their noses, so no change there.

I wish we would stop going to bank economists as experts. They have a vested interest in more people buying.

Not long ago a certain RE agency (rhymes with La whore), advertised investor seminars on radio. Last night I heard the same agency saying one-on-one investor advice can be arranged. Can't fill the rooms anymore?

Hi G_m,

Typically, such property investment seminars attempt to flog off apartments. And, of course, apartment sales have bourgeoned over recent times - despite many being poor investments.........

Stand-alone houses are a far superior investment to apartments. Buying LAND has an intrinsic advantage.

Anyone who buys this side of the election is either really desperate or stupid or both. After election its to make a king or not waiti g, then its xmas more waiting, and then its new policy and tax changes announcements by March.

Fhb have waited so long. Wait some more, more to gain than loose.

agree Averageman. Right now LVR's essentially protecting first home buyers. This would seem like a crazy time to take on these crazy levels of debt. It's a Life sentence.

I guess one of the many reasons people who havn't voted in previous elections will stand up and vote this time round.

Great to see labour not only holding it's ground but making inroads on National in the latest Poll. Bill declaring national as the government for New Zealand property owners seemed pretty blatant. Desperate times for National.

It seems the mood here has swung and apparently the property party is unofficially back on. Surely our government must take some responsibility and moral obligation to protect young people and FHB from taking on these crazy levels of debt. It kinda feels like everyone agrees that the current houseprice to income ratio is unsustainable which makes it sad that so many here are wishing house prices to infinity.

The cost to society is real and dire. Surely you dont really wish this upon the future generations of NZ'rs.

Kind of makes you think the generational war is real, eh. Why wish this on young FHBs? Why ask them to prop up the party and wear the risk?

I've been saying don't buy or put in extremely low offers since the start of the year. At this point I'm just saying don't buy. Wait until the end of the year and see what's happened before looking at the property market.

Alternatively people could look at equities with low P/E or indexes. The returns this year have been good compared with property which has been going backwards.

Any suggestions on share options at the moment dictator?

Just buy and hold on this:

https://investnow.co.nz/award-winning-managed-funds/fund-search/?_sft_f…

Thanks kiwimm - pretty well allocated already in terms of offshore ETFs.

Hi dictator,

The problem is that house prices could start climbing again by the end of the year....... When the tide turns it can happen rapidly - and without people noticing for a while.

As this blog shows us, quite a few people missed out on the last upswing - and just look at how they're moaning now.......

hmmmm if your including me in the moaners that missed out. I should correct you. I own my own home + some land all freehold. I'm 39 but had to work overseas to be able to afford this. For me my home is the place i live and hopefully the place i will always live.

To be honest the value of my property is insignificant to me.

treating property as an investment is a fools game that is causing all these sad distortions in our society.

The fabric of our scoiety is being destroyed and all the old things i loved about NZ are quickly dissapearing. Just hoping for a more fair and just NZ

Hi Wally,

I enjoyed your post above. Like your positivity.

Well done!

"The fabric of our scoiety is being destroyed and all the old things i loved about NZ are quickly dissapearing. Just hoping for a more fair and just NZ"

Exactly.

In a similar situation and have similar wishes - but for the life of me do not see how Lab policies would help bring that about.

With Auckland house prises down 8% since Feb FHBs are saving about $3k per week by not buying a house.

So forget about LVRs and wait another year, you could be saving another $150K which would require $30K less deposit

Easy...

Wheeler is a twit if he doesn't make some sort of allowance for FHb. He runs the risk of putting nz inc into recession, as so much domestic activity is linked to housing, and construction.

Targeting the first bracket, dropping lvrs here for new builds, and FHb will keep the cogs turning, give young folk some hope, so that they remain in nz, help drive down construction costs, and enable people to trade up.

Sure if we stay with the status quo prices will slowly come off the boil, which is I believe his focus. However this will be at the expense of the wider economy. Whether wheeler likes it or not we are part of a global economy, and young folk will walk.

Melbourne and the like look appealing given the current climate.

I would not be surprised if immigration started to slow, with kiwis starting to head back across the Tasman.

My fear is that this may very well become a stampede if labour gets in, and they start taxing everyone, and anything as they are bound to do.

Forget house prices. It looks like the Big 4 Banks are becoming a bit stressed. Interview mentions Johnathan Tepper who is trying to short our banks and comments from CBA and Westpac are ringing alarm bells. Westpac quoted "If the housing market crashes, people will loose their wealth but the size of their debt will remain long." Either way, it looks like both Australia and New Zealand are heading into possibly quite a large recession. Well it was fun while it lasted.

I hate to think how many home owners won't be in the market for years, but I guess there'll be others who didn't play these games over the last 10 years, some would have sold and made good money but if rebrought even they are in for large losses

There aint going to be a big crash, just a small correction over the next 3 yrs, maybe 10-12% in my opinion (from past data). All the scaremongering just makes people panic and do stupid things like sell their houses, the prices of which in the medium -long term will go up (after 2020). Look at what Bernard did, sold his house and lost out on big equity increase. Shamubeel Eaqub is another idiot who was telling people not to buy 3yrs ago but now has bought a house at double the price he could have bought way back when he started throwing his opinion around. He says that he is an "experinced economist" ! Bollocks!

"Experienced" sorry

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.