Property information and analytics provider CoreLogic says the New Zealand property market is currently showing "a prolonged period of soft conditions" as stricter mortgage serviceability criteria continues to limit the ability of potential buyers to borrow the money required to buy and transact in the market.

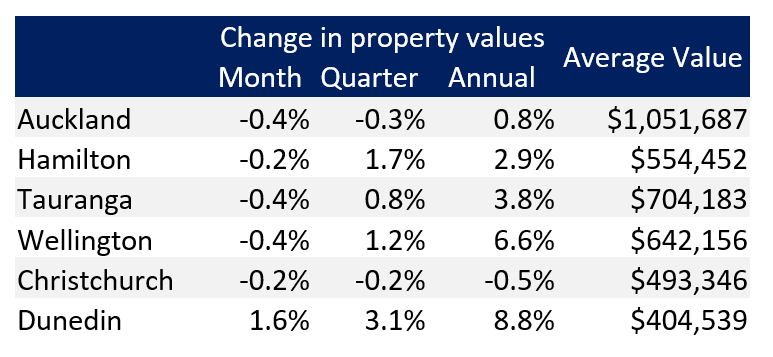

CoreLogic's head of research Nick Goodall says the latest QV House Price Index, which utilises data from CoreLogic shows that property value growth remains constrained with five of the six main centres seeing a minor loss in average value through the month of April 2018.

"This is the first time since September 2010 that at least five of the six main centres saw value falls in the same month."

He says the highest capital gains can currently be found across the regional markets, but warns there are signs of weakness ahead.

"We’re starting to see population growth slow in these regional centres, and with extended value growth not matched by wage growth, property is becoming less affordable, especially given a tightening of lending credit policies."

Goodall says a "heavily scrutinised" property investment sector is weighing on the minds of some investors.

"With the extension of the bright line test to five years, as well as the Healthy Homes Guarantees Act changes coming into force later this year and the ring-fencing of losses applicable for negative gearing, some investors will be questioning the profitability of extending their property portfolio."

So far CoreLogic had not seen a noticeable lift in investors listing their properties for sale.

"But we are keeping a close eye on activity taking place in this sector, given the more challenging investment conditions and potentially weaker prospects for capital gains."

Goodall says that the role of lenders and credit policy in the market can't be underestimated.

"While mortgage interest rates have been dropping again recently, lenders remain risk averse, limiting interest only loans and testing serviceability at over 7%, meaning that despite the minor relaxation of the LVR limits from 1 January 2018, there hasn’t been a wave of newly-eligible buyers hit the market."

And despite news last week that the first KiwiBuild homes are now under construction, Goodall says there is a long way to go before housing supply meets demand, especially considering the high rate of net migration.

"A high rate of population growth will help to support housing demand and ensure the slow-down remains a relatively placid one."

Goodall is expecting that property transactions will remain constrained "for at least the rest of the year" as finance remains harder to acquire.

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

51 Comments

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

On the laws of probability (which is not our area of expertise); on the basis of our forecasting model; and on all other things remaining equal.

If you have a strong understanding of comms / media strategy and psychology, there's always the possiblity of a job for you at Corelogic crafting media releases.

Another great "I want to sound more intelligent than the expert" comment.

If you mean to say "sound more intelligent than the 'experts' by acknowledging what isn't and cannot be known", then you're right. Corelogic are indeed "experts"....within their known parameters. I can guarantee you that their back office is not a hive of magical activity that knows the price and volume of house sales into the future.

I repeat: CoreLogic will always be open to talking to skilled communicators.

I can guarantee you that their back office is not a hive of magical activity that knows the price and volume of house sales into the future.

I agree. It's not magic. Nor is it necessarily extremely point accurate (which isn't always the purpose).

What they do have though are some very well qualified data and personnel.

Having met a couple of their quant people, I can assure you that their understanding of "The laws of probability" is of a resoundingly higher caliber than yours.

Oh, and for the record - they're Frequentists.

Having met a couple of their quant people, I can assure you that their understanding of "The laws of probability" is of a resoundingly higher caliber than yours

If they were as good as you think they were, they would be the first to admit their limitations. If they couldn't admit, they'd be nothing more than charlatans.

But you're not going to read that in a CoreLogic media release.

Since when did you JC admit to your own “Limitations” ?

Since when did you JC admit to your own “Limitations” ?

Very well aware of my own limitations. The world has too many people who profess to know more than they actually do. Because of that phenomenon, we have frequently occurring asset bubbles.

Great reply but you mightve been best to educate JC for I feel he might miss the jist of your ending “Frequentists” https://www.explainxkcd.com/wiki/index.php/1132:_Frequentists_vs._Bayes…

The laughs never stop here ha

Most people's understanding of probability is based on something similar to "gut feeling" or a narrative that they believe makes sense to them. Hence the importance of "skilled communicators" who are integral to central banking and property data businesses.

Nymad

Great reply but you mightve been best to educate JC for I feel he might miss the jist of your ending “Frequentists” https://www.explainxkcd.com/wiki/index.php/1132:_Frequentists_vs._Bayes…

The laughs never stop here ha

LOL, so the message to all DGMs is clear ... open your ears and eyes and listen to reality coming from the Horse's Mouth ( well one of the horses anyway). No Crash yet, and there isn't one on the horizon.

Values will continue creeping up in the main centres - that is S&D, hopes, and wishes do not translate into cheaper prices in the market.

When inflations kicks in next year ( and another 68000 new immigrants) we shall see another significant appreciation in prices.

So Auckland average price is still over $1.050M and Wellington is over $640K ..get used to these numbers.

FHBs have a window of opportunity to get in this winter when the find what they like and can afford and lock in low interest rate for few years.

And of course from the same Corelogic analyst that said that after the election prices would rise again.

LOL, did you miss this part

"This is the first time since September 2010 that at least five of the six main centres saw value falls in the same month."

Time will tell what the future has install for us, but the tide is slowly turning.....

“When inflation kicks in next year”…..

Oh dear – what will interest rates do in response??

“and another 68000 new immigrants”….

I really don’t know, and maybe it’s simply wishful thinking – but I wouldn’t be surprised if the number is somewhat less than that in a years time.

Told you so.. my trusty RE agent said " the time to buy is NOW"

All I need is that 1 million bucks in loose change! Wonder if I can find it tucking away in my Louis Vuitton inspired crocodile skin couch.

hahaha "a window of opportunity to get in this winter" with this incredulous comment there is no dispute now Eco Bird has confirmed he/she really is one of those highly respected professionals...a RE agent.

lol, that RE agent broken record has long passed its used by date ... it just prove how disconnected you are from this market and forum.

Time and again, month after month, everyone related to this Market, be it corelogic, REINZ, the big realities and economists are saying the same thing - but hopefuls (and the Broke) are still clinging on to a miracle and a mirage!

Sure, it makes you feel good for every bit of negative sentence in any report but you still miss the big picture and the end result.

Hence the message was to the WISE FHBs ... who BTW are increasing in numbers as they are buying as they can according to lending numbers published yesterday...

Sleep well

Agree with you Eco Bird.

The DGM (Doom and Gloom Merchants) have taken a sustained hammering over an extended time period.

I do have some empathy, however, for them. Like pretty well everyone else here, they want a house of their own.......

What they don't seem to understand is that to own a home, you first have to purchase one. That may sound simple/trite - but it's true.

The DGM need to know that sitting on the sidelines ranting and raving will get you no where. It certainly won't get you the keys to your own home.

TTP

#sanctimonioustripe

"I do have some empathy, however, for them. Like pretty well everyone else here, they want a house of their own.......

What they don't seem to understand is that to own a home, you first have to purchase one. That may sound simple/trite - but it's true."

I think you will find that most have their own home on here, or have sizeable deposits. Most people are looking at the fundamentals and that houses compared to the past, and compared to other places in the world are over valued relative to incomes. That is they are unaffordable for most in NZ. These fundamentals don't stack up. So if there is some type of change like interest rate rises, no foreign buyers, China not allowing outflow of money, extension of bright line, tax on capital gains, no ring fencing losses, reduction in immigration, a global recession, tightening of credit lending etc etc, then the house of cards may come tumbling down. It may not but its like a game of Jenga, and it seems like its quite wobbly at the top.

Are you willing to put all your money at the top of the Jenga pile. Borrow up TTP, get your family, investors, you will make millions.

@ Tui12

Your comment well said.

"a window of opportunity to get in this winter"

Calling any Suckers out there?To add to the statistics of the Greater Fool Theory

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

Wonder what they consider a "significant drop" as, -5%, -10%, -20%....

I wouldnt consider a 10% drop significant considering in real terms most properties (in Auckland anyhow) are about 30% over valued IMO.

New book out by Nomi Prins her last book All The Presidents Bankers ) suggest everyone read it

http://www.nomiprins.com/

Global debt now 225% of global GDP Which is way higher than just before the GFC.

NZ (regardless of what forex traders say otherwise ) weathered the last GFC pretty well without significant

downturn in Auckland property prices albeit apartments took a big hit

GFC2 May deliver a different scenario due to massive Chinese speculation in Auckland property that just might

unwind itself from Auckland property However I wouldn’t bet on it NZ is a safe haven no matter what any QueenSt forex trader says otherwise

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

Also what are the strong fundamentals they talk of??? there doesnt seem to be any listed in this article. maybe TTP aka MTP could enlighten us?????

Hold on to your seats folks

how can anyone possibly enlighten a dark minded pessimistic person?

quite obvious from your use of percentages willy nilly that you have no idea at all !

If you haven't seen or known the fundamentals of the housing market thus far, why the hell are you commenting on here?

Or, you are just trolling to pass time ? :)

In this case, pessimism is a matter of perspective. Hoping for house prices in Auckland to return to a more affordable level seems rather optimistic to me. Further house price rises from here would make the city worse from my perspective and I don't think I'm alone.

Really? here is a small dose to help your "Optimism " and add to your fundamentals' knowledge:

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Are you still hoping for prices to come down soon ?

For the record - changes to development contributions is unlikely to increase house prices - but it will reduce the value of undeveloped land. Many land bankers would be hit by these changes.

Says who?, which land bankers? the Todd family or the Neile Groupe ? or others who own suburb size lands for development?

are you suggesting that the small guy owning a section here or there will chicken out and sell asap? and do these have any weight on development at all?

For the record, this is not the first, and wont be the last , and it Will increase prices in the short term ... watch the space !

The council is exploiting developers because they can and now they feel more powerful being backed up by this left inclined CoLs !!

"House prices aren't rising much at the moment, so developers will factor the increased contributions into their cost structures when they buy land for building on. Land prices will go down, rather than house prices going up, Duncan says."

Jaysus, where do auckland council find these morons.. either house prices will go up, or developers will hang up their workboots and go lie on a beach somewhere till there is margin to be made again. Neither option is good for NZ.

Just swallow a cold turd and put rates up 15% across the board, then close ATEED and all those other waste of space departments down and get back to providing the core services without the luxuries.

In the good ol' days ie pre 1990, the cost of development (and contributions to development) did come of the land cost (what you negotiated to pay the land owner after taking development costs into account).

But that all changed when council restrictive growth policies kicked in and when they starting collecting DC for 'well being' projects as well ie what and who they charge for DC's is completely divorced from what the money gets spent on and who the beneficiaries are.

So in theory what council are saying (but in name only) is a return to that policy.

But in practice, it won't work for two reasons, 1) There still is no link between money collected and who pays the money, to were it is spent and who benefits, and 2) The present developer owners have already paid the inflated restrictive land price to the former owners so there is no going back and getting a discount against this new increased charge.

The present owners options are: 1) take a loss, 2) sit tight and hopefully on top of them causing less supply and councils continuing restrictions, capital increases will claw back this future cost to them, and/or 3) They get a zoning change to increase the value.

Yes. Why would that change my mind? As ex socialist points out, this could equally act to reduce the land component of build costs. Note that is doesn't actually cost much more to build a house in Auckland than it does in other parts of NZ (I have a ballpark figure of 10% higher in my head but feel free to correct me) - the higher house prices are almost entirely due to higher land costs.

edit: you may has misunderstood my original post. My point was that house prices falling would be a good thing on balance. I didn't predict that house prices will fall.

Cool, let's leave building cost out of Auckland aside because I disagree with you on that. It's not just land cost ... examples are available on trademe and builders' sites.

There are two facts in the Auckland property market:

1- land will not become cheaper as long as ACC refuses to release land !! and PT needs to grow big balls to make that call.!

2- Any additional costs to development raises the value of ALL Auckland houses ( this tide will raise all the boats - without any doubts, just like it did so many times before). this is not the first rise ... Total property development cost will now exceed 100K in many places ... whether that is fair or not, remains very debatable .

The ACC will not only get extra contribution from developers, but it is rubbing its hands with glee come the next property valuation and rate increase in 2020 as all property values go up due to this increase .

Was anybody surprised when the new 2017 values came to underpin current elevated market prices - as I always been saying?

This Big ACC machine will do anything to keep its rusty wheels well oiled and running - and they are very creative in milking money out of everyone, you have to give them that !!

*The ACC will not only get extra contribution from developers, but it is rubbing its hands with glee come the next property valuation and rate increase in 2020 as all property values go up due to this increase .*

Oh god, not this again. I suggest you learn how rates are determined.. your rating value going up 20% along with everybody elses' doesn't mean everybody pays 20% more rates. If your rating value goes up and nobody elses does, then you get hit with a rates increase.

The fundamentals are when a house sells for 1,000 times its weekly rental - Wellington is close; Auckland is a long way away.

Hit a nerve did I?

Funny how you too are are unable to list these strong fundamentals that are underpinning the market, you know why? because they dont exist

Your 2 examples of inflation and immigration dont hold any weight at all.

Unless wages inflate alongside inflation, it as the opposite effect of tightening the belt of those stretched with high mortgage payments.

As for immigration, it is starting to fall, and even though we have come off a record year, Auckland inventories and days to sell have pretty much doubled in the last 18 months along with low sales volumes so the demand for buying houses has actually substantially reduced.

Am I a pessimist? No, but I am extremely Bearish on the Akld property market as all of the fundamentals lead to a much needed correction.

High inventories

Low sales

ban on overseas buyers

ring-fencing losses

extension of the bright line test

Tightening on lending

International interest rates rising

falling immigration

Record high DTI

Sorry but its true!

If you are bullish in the face of these facts then you are a fool

I hope you’re Guess comes true

I would love a Muriwai beach house as a collectable

I am neither bullish nor bearish - I have and own enough ! and just stating what some of you guys are refusing to see and guiding FHBs with dissected logic and views.

you posted what would affect the demand side ( and none of these has lowered prices so far) - without any factors affecting the supply side and the shortage therein ... so one sided argument to suit your narrative which is contrary to all expert opinion.

Again, read this to add to your list of goodies, and draw your own conclusions:

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Another clever move from ACC - they are experts in placing spanners in the wheels !

Bearish. Agree with all bearish points. Even RE cheerleader NZHerald has articles about possibility of significant lending tightening in Aussie banks ok. circa 30%. Wont flow over here will it....

The strong fundamentals they talk of can be summarised in one word....'HOPE'

The "strong fundamentals" referred to, are population growth, high employment. I thought most commenters would have known that.

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

Not exactly.

In Auckland prices are more underpinned by a stupidly tight land supply constraint used by a lunatic council to stifle the building of new housing. Prior to the last election Phil Twyford said a Labour government would remove this restriction if elected.

If Phil Twyford keeps his promise Auckland will be in line for a 20-30% correction and a building boom. If Phil Twyford breaks his promise Auckland will stagnate and decline.

There's really nothing new about this news. CoreLogic just provided the actual figures to emphasize softer housing market which we already know.

Net migration starts to slow down too which is great. term deposit outperformed property investment in Auckland that is one thing for sure.

I miss the vastly accurate T. Alexander

Where is he

At BNZ

As a FHB, I am not convinced that now is the right time to buy. I have started to give false contact details when visiting open homes. I'm tired of getting spammed, and called every 5 seconds.

I'm very wary of the Aussie property market just now. Tightening availability of credit just when the foreign buyers have disappeared and a big supply of flats in Melbourne and Sydney coming on line.

There are 250,000 young Aucklanders looking at the flats in Brisbane, Melbourne, Sydney and they be thinking.

Those places are all bigger, provide more opportunities and will pay better. And soon the smaller, less vibrant Auckland will be more costly.

House prices in Auckland have reached a permanently high plateau. Now is the time to be aggressive! You don't need to have any financial discipline either. A sound recipe involves borrowing 150K from you parents, then going to Harmoney to borrow another 70K @ 14% interest. Now that you've "saved" that deposit any bank will give you an interest only loan of 800K (with a healthy safety margin under the 20% LVR). Now you really ought to pay back the high interest rate Harmoney loan quickly before the interest only loan becomes interest + principal. (tongue in cheek)

"However, with strong fundamentals underpinning the market, we’re unlikely to see a significant drop in either volumes or values across our main centres."

Good grief - the number of times in my life I’ve seen this type of “carte blanche” statement thrown around just before the whole thing fell over.

Then again, perhaps the get out of jail card is the word “significant” – somewhat subjective.

The reality is no one knows or can predict a market. The analysis in this article is based on past records. Past does not equate to future in an open market. Markets react to changing conditions both local and international.

Such statistics & articles make good money for publishers, researchers & media but should not be considered investment advice!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.