We kiwis always like to compare ourselves to our bigger neighbour to the west. And if you do so in the area of monetary policy at the moment you'll see a stark difference.

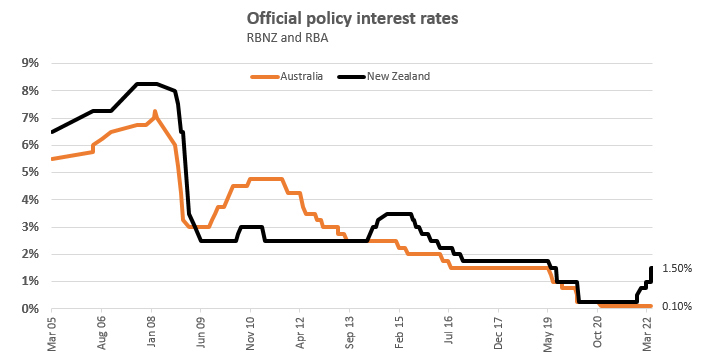

With the Reserve Bank of New Zealand (RBNZ) having last week increased its Official Cash Rate (OCR) by 50 basis points to 1.50%, a huge gap has opened up with the Reserve Bank of Australia (RBA). Whilst the RBNZ has now increased the OCR at four consecutive reviews, the RBA's Cash Rate Target remains at just 0.10%, which is where it has been since 2020.

So why has this chasm emerged between the two neighbouring central banks? After all both countries now face similar inflationary challenges.

Kiwibank Chief Economist Jarrod Kerr describes the differing cash rates as interesting.

"The RBA painted themselves into a corner by continually saying they're not going to do anything until 2024. And that was on the back of them manipulating the yield curve," Kerr says. "So while they were doing that ... they couldn't change tack so quickly."

"That's a long way of me saying they're late. And we'll see them tightening from June, which is a big about face, a big turnaround," says Kerr.

"And then on the New Zealand side, with the benefit of hindsight the RBNZ was ahead of the curve, ahead of most central banks around the world. And now they're in a situation where they're still worried about inflation, still worried about meeting their mandate and the threats to their credibility. So I think you've got a central bank which is much more aggressive."

Kerr also points out that NZ has higher inflation than Australia.

"We had higher inflation here prior to the pandemic. So we went in with a higher inflation trajectory than Australia did. But at the end of the day I think the RBA's late and the RBNZ is accelerating," says Kerr.

In December NZ's annual Consumers Price Index came in at 5.9% versus 3.5% in Australia. Economists expect the NZ March quarter figure, out on Thursday, to be above 7% with inflation also expected to rise in Australia.

Meanwhile NZ's official unemployment was 3.2% in the December quarter versus 4.2% in Australia. Australian unemployment dropped to 4% in the March quarter, with the NZ March quarter data due out on May 4.

RBA goes lower

Whilst both central banks cut their key overnight interest rate to 0.25% in March 2020, the RBA went lower still, going to 0.1% in November 2020 where it remains. And Kerr's comment about the RBA's yield curve manipulation highlights another difference in the Covid responses. One of the steps the RBA took was a target for the yield on the three-year Australian Government bond of around 0.25%, which subsequently reduced to around 0.1%.

Whilst the RBNZ went down the quantitative easing path from March 2020 through its Large-Scale Asset Purchase (LSAP) programme, through which it spent billions on government and local government bonds, the RBA didn't adopt this tool until November 2020.

ANZ Chief Economist Richard Yetsenga notes the rate gap between the two central banks is large, but expects it to close. He also argues that central banks went too far in their responses to Covid-19.

"Yes the rate gap is large, but it substantially reflects the speed of monetary policy action this cycle. Policy, in general in advanced economies, responded too aggressively to the pandemic. Some central banks, like the [US] Fed and RBA, have also adjusted their policy approach such that they would tighten later than might have been usual previously. The net result of this is that modest timing differences are resulting in large rate gaps," Yetsenga says.

"Over time the differential between Australia and NZ will start to narrow once the RBA more clearly recognises how much monetary tightening will be required to return inflation to the target band and ensure it remains there on an ongoing basis," adds Yetsenga.

The RBA must seek to keep consumer price inflation between 2% and 3%, on average, over the medium-term. The RBNZ's target is for annual inflation between 1% and 3% over the medium-term, with a focus on keeping future inflation near the 2% midpoint.

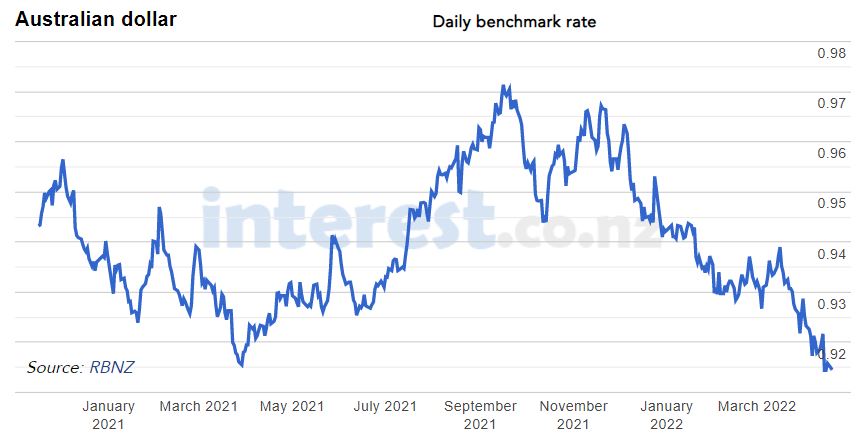

Economists do expect the RBA to start lifting its Cash Rate Target from June. And this, Kerr says, is why the Kiwi dollar has fallen against the Aussie dollar when you might've thought it'd have followed the higher OCR up. At the time of writing the NZ dollar was at A91.44 cents.

"The Kiwi has depreciated against the Aussie because markets are now focused on what the RBA has to do. So we've actually enjoyed a depreciation in our currency relative to Aussie," says Kerr.

"I think it'll be interesting to see how that plays out now that we've got the RBA coming into play in June and the RBNZ ramping up their rate hikes with another 50, I think, a done deal for May to get the cash rate back to neutral."

Kerr believes the RBNZ wants to get the OCR to what it deems a neutral level, where it's viewed as neither stimulating nor constraining economic activity, as soon as possible. He sees this as 2%, from where the OCR climbs several times by 25 basis points up to about 3.25% in this tightening cycle.

As for the RBA; "I wouldn't be surprised if they are forced to do a few 50 basis points licks themselves. They'll go through 2% for sure," Kerr says.

As the chart below shows decent sized gaps have opened up between the key RBNZ and RBA overnight interest rates before, albeit not for about six years.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

37 Comments

And yet the NZ dollar is weak against the Aus. Which suggests the impact of the OCR on the exchange rate might be exaggerated?

I would say it potentially suggests a recession may be coming in NZ.

No its because we have a higher inflation

yes with the current OCRs the exchange rate right now should be overt .95

I would be interested in the views of people who consistently say the OCR needs to be hiked to strengthen the NZ dollar.

I certainly think the OCR is a factor in exchange rates, just not as strong a factor as some people suggest.

I think it is the primary factor. Hiking the OCR increases the the value of money which increases the NZD relative to its peers.

So then, why has the OCR been hiked here and not in Aus, and there’s a big gap, yet the NZD is so weak against the Aussie dollar?

clearly there is a relationship, but it’s certainly not a simplistic causal one.

Australia's currency is backed by commodities, a "commodity currency". There currency will always perform well during a period of commodity price inflation. Even if they are not as aggressive with the hiking of the OCR.

New Zealand economy has a lot of bubbles, which Australia doesn't. The inflation data is different too.

I would have thought that is obvious : Scomo got on the phone to the RBA Guv' and told him to hold off rates rises until he's voted back in

I think it's the RBNZ's OCR outlook might've not met market's expectations to curb inflation, hence 10 year bond yield dropped after 50bps OCR hike. Another reason could be market starting to lose confidence in New Zealand economy. Again, hiking OCR doesn't necessary mean we can successfully strengthen the NZ dollar. But not hiking OCR will definitely weaken NZ dollar. We are choosing the second worse option here, there is no good option from now on. It's between bad and worst.

Good comment, but I don’t think it’s that black and white. Hiking the OCR will whack the economy. Also at some point a strong NZ dollar will hurt exporters.

I still favour moderate hikes to circa 2%. Stopping at 2% could avoid destroying the economy, while taking a reasonable amount of inflationary pressure out of it.

I still maintain that hiking the OCR will have only limited impact on inflation, it’s far more of a supply side problem than a demand side one. The demand side has largely been dealt to by the hikes to date, plus CCCFA, not to mention the demand quelling impact of high inflation (high costs as a cure for high costs).

I think these comments are spot on.

Why is there going to be demand for the New Zealand dollar. The hoarding toilet paper craze has passed now.

Thanks HouseMouse.

But I think our economy had already been whacked many years ago. Hiking OCR will just bring it to neutral as it is not supposed to be that low. For many years, we have been stimulating our economy to create gdp growth illusions. This made our economy very vulnerable to any "black swan" event. Covid caused supply side problem is just a trigger to show the real issue in our economy, which is excessive money supply unmatching with our productivity. If it's not covid or supply side issue, there will be something else. To me, this is an economy correction, of course it's gonna be painful, but it's a necessary process for our economy to move forward.

Moderate hikes to 2% is really off based on the current data in my opinion. Major banks are already predicting another 50bps hike for the next OCR decision release. That will bring OCR to 2%. After that, I don't think it will stop there until it reaches high 2, or it could be even higher than RBNZ's OCR outlook Of course, we will need to see how the inflation data and inflation expectation data look in future.

2% is probably a good prediction when inflation is at 4-5% but not for 7% in my opinion.

“The Kiwi has depreciated against the Aussie because markets are now focused on what the RBA has to do. So we've actually enjoyed a depreciation in our currency relative to Aussie," says Kerr.

Yes, our central bank is much more aggressive and this could lead to a recession. Housing prices were already falling in our overindebted and housing-dependent economy when interest rates were raised aggressively last week. This has the potential to throw us into economic peril.

After years of cheap money supply, inflation cannot be successfully fought at this point, in my opinion. The money that has been created ex nihilo during Quantitative Easing cannot be extracted from our house of cards-economy without risking collapse.

The current inflation is also largely driven by supply shortages overseas. There is no way this could be addressed via our interest rates, it is illusionary to think we can fight inflation at this point.

Instead of acting with decisive force and some element of surprise (only to possibly lead to destruction), it would be prudent for our Reserve Bank to take a less aggressive and more considered approach.

The money ex nihilo-party is now over. The hang-over (stagflation or recession) seems inevitable.

The choice is between a) stagflation (best case) and b) recession/depression or even total collapse.

Option a, with high inflation rates (whilst avoiding hyperinflation) over a few years would devalue the debt bubble and open the way for a true recovery in a few years. This could be similar to the Paul Volcker-moment in 1981/82 (raising interest rates to 20% p.a.) with Reagan/Thatcher/Kohl taking over politically, opening up a new era of opportunity after a few years of inflation.

It is crucial that the vast pile of debt is allowed to be devalued first via inflation, before aggressive rate hikes can occur. It must be understood that after years of feasting on cheap money there is now a hangover period coming which cannot be avoided.

The approach currently chosen is aggressive, which very much risks a path down option b) - recession/depression.

Now would be the time for the Reserve Bank to apply prudence, not aggression. Interest rates should be retained at current levels and the economic outcome of the rate rises that have already occurred should be carefully monitored, especially their effects on our real estate sector, which (like it or not) determines the fate of our economic wellbeing. A property crash would spell disaster that would spill over in all kinds of sectors and could lead to massive unemployment and hardship. A crash should be avoided.

Now is the time for prudence and carefully selected interest rates, not for acting aggressively in our economy like an elephant in a porcelain shop. I was surprised and quite shocked by last week's 50% interest rate increase from 1.0% to 1.5%. I consider a 50% hike far too aggressive in a fragile economy with a housing price correction that was already going on before the rate hikes, which could now turn into to a housing crash.

The move surprised me, as the Reserve Bank had been saying they would choose the path of least regret. The path of least regret, in my opinion, is clearly inflation as opposed to deflation. This could be seen as being within the mandate of the Reserve Bank, as that mandates includes employment rates as well as consumer price inflation rates.

Oh boo hoo, are you overleveraged and cant get out?

The labour market is pretty strong/tight im sure RBNZ has a brain to monitor that after every hike.

You should deleverage. Seriously.

He’s totally right.

Hiking the OCR is only likely to have limited impact on CPI inflation, yet it will cause significant economic damage.

This view has nothing to do with how leveraged you are.

and btw, it’s a view that is not rare amongst leading international economists (although none here in NZ seem to subscribe to it).

It's quite the wealth transfer from savings and wages to assets though, isn't it. That's a truckload of pensioners receiving significant economic damage to avoid asset values being reduced...

The labour market is strong now, but the economic / employment impacts of hiking the OCR lag quite a lot. Aggressive hiking in the next few months is likely to lead to a lot of economic pain and rising unemployment in 6-9 months.

Don't worry Markus NZ property prices are driven by supply issues not interest rates. The expert in economics and monetary policy Mr Orr said so himself. Please see below

"Reserve Bank governor Adrian Orr has issued a fresh warning that high house prices are unsustainable, but says its own low interest rates have only played “a bit part” in the problem."

"The “long-term fix” to ensure a well-functioning housing market – one that responded to changes in demand – was to ensure new homes could be built when needed, he said."

So you have nothing to worry about. The housing market is primarily impacted by housing supply issues not interest rates. The RBNZ needs to filful its mandate to maintain CPI in the 1-3% range. Let them do this in peace. Just sit back and kick your legs up. Nothing is going to happen to your nest egg as no political party has the capacity to fix these housing supply issues. Hell I would even consider buying. Let the DGM's panic foolishly over monetary policy and interest rates. You just trust the experts and buy buy buy!!!

We seem to have trouble in NZ differentiating between demand for a taxpayer-subsidised, tax-privileged, and risk-protected investment...and demand for accommodation.

There is no way to maintain the CPI below 3% after years of money creation ex nihilo. This newly created money has driven up house prices and is now driving up consumer prices, that tsunami cannot be stopped.

The mandate of the Reserve Bank within this range appears illusionary at this point in history. It seems now important to take a pragmatic approach, not a robotic one.

I consider the current situation critical, if not dramatic. It is a turning point in history. Care and prudence should prevail. The situation appears very fragile to me.

Whilst unemployment is currently at record lows, property prices have recently been at record highs. Both are effects of years of "money-printing", so to speak. There is a bit of delusion, an element of artificiality in both.

I am convinced we have to be careful now not to fall off a cliff. This is why I have started writing here, I am convinced this moment in history is crucial.

The Reserve Bank should try to let the air out of the debt bubble carefully, ideally via devaluing debt through inflation. Any super-hero style approach may spell disaster.

There needs to be a waking-up to reality - there is no way to retain the illusion of monetary stability in a fiat money-system. The approach by our Reserve Bank should be less robotic and more pragmatic. The inflation band below 3% cannot be maintained, it is completely delusionary.

What can be maintained is high employment and a certain level of economic stability (as opposed to an economic meltdown). This should be the focus of the Reserve Bank.

Both the Australian and the NZ Reserve Bank are acting quite extreme, interestingly in different directions. Whilst I think the truth may be somewhere in the middle, I consider the Australian far preferable over our Reserve Bank's approach.

I see your point. But I disagree. The RBNZ will not be able to "air out the debt bubble carefully"

If we need to eat a serious recession to maintain the integrity of our financial system then we should eat a recession. We do not want to go down the road of having an inflationary currency. This is more damaging in the long term. As inflation is essentially a regressive tax which disproportionately affects the poor.

Markus, you are copying and pasting this comment around a lot...

A property crash is inevitable at this point.

Better to just accept that and get your affairs in order. Deleverage, sell what you can.

No point in being an "old man yelling at clouds". Better to just move with the changes.

Yup. Further there still seams to be a few dreamers out there paying too much. This could be the final call.

The dreamers have gone and anyone dealing with any RE can be expected to receive plenty of phone calls if your currently a cashed up buyer. The time to buy is coming to a street near you very soon.

Its funny you say that. I went though a couple of properties and showed some very vague interest. I am getting absolutely hounded by both of them. They also both want to come and appraise my current house. Go away......!!!!

Thank you, I appreciate your comment.

"And then on the New Zealand side, with the benefit of hindsight the RBNZ was ahead of the curve, ahead of most central banks around the world."

While I can agree the RBNZ are ahead of most other central banks, they are definitley NOT ahead of the curve! 7% inflation and a 1.5% cash rate is as far behind the curve as you ever want to be.

yes they are going to get to OCR 2.5 as fast as possible by the looks. Covid and the emergency stimulus is over.

They are throwing us around, too extreme. One way down, radically, likely overdone. Now another way, radical again. The economy is not a boxing ring. It is more like a porcelain shop.

At some point you have to look at the actual facts in front of you and question whether pushing the OCR lever up (or signalling that you will do) connects through to prices in the economy (or exchange rates) in the way that the models suggest. This is especially the case with macroeconomic models, which are notoriously useless.

I know I could trigger a pile on here - but it is not possible that increasing interest rates in a supply-side driven inflation environment just pushes prices *UP*? Would that not be a hypothesis worth exploring given that the countries hiking rates (or signalling that they will) seem to be the ones with relatively high inflation? When Chris Luxon was comparing high inflation in NZ to low inflation in Australia, Japan, and Singapore on the news this morning, did anyone spot that all of those countries have very low interest rates?

When I looked into why inflation was comparatively so low in Australia it looks like non-tradable inflation was far lower than New Zealand. Rents seemed to be falling across most cities offsetting tradable inflation. New Zealands Reserve Bank just did far more quantitative easing as well which has been helpful to controlling inflation in Australia.

As long as strong commodity prices persist, and it does appear we are heading into a supercycle, Australia will likely out-perform New Zealand on a per capita basis. We've seen this effect before where when New Zealands economy stagnates relative to Australia talent goes over the ditch and unfortunately I think we might start to see that play out again.

It's true the RBA got itself in a corner but it has also been pretty consistent saying it was looking for wages to grow before tightening, and to date they haven't been growing very strongly. Also the exchange rate impact of increased rates on exporters in a tight commodity price cycle with an already higher AUD will be on its mind. And Australia has a more diverse, competitive economy compared to NZ, which might tend to mitigate inflation pressures.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.