The December AWG prices for export grade logs increased by NZ$7-8 per JASm3 from November prices. Log prices increased in China as the market reacted to the ban on Australian logs.

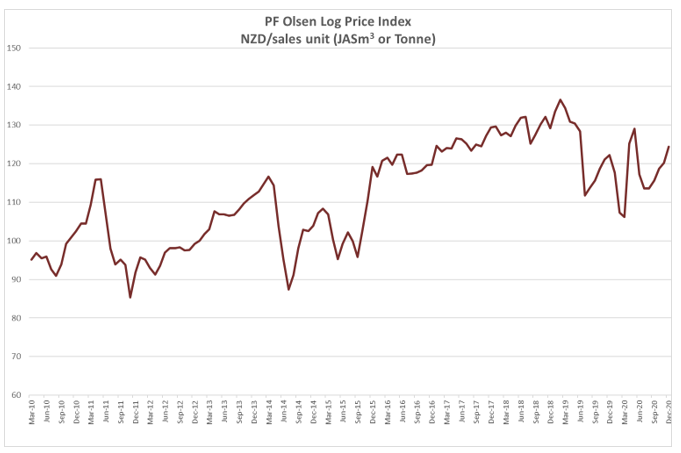

Due to the increase in export log prices the PF Olsen Log Price Index increased by $4 in December to $124. The index is currently $3 above the two-year average, $1 above the three-year average, and $1 above the five-year average.

Domestic Log Market

Log Supply and Pricing

Prices for domestic logs have been stable as we head towards the end of the year. Many mills are closing later than normal for the Christmas holidays as they look to fill orders. Some mills even have shifts working through the holidays. There is plenty of log supply as harvest levels are high.

Sawn Timber Markets

The domestic market for sawn timber across all product ranges continues to be very strong. In many Asian grades such as the cut of log (COL) prices are at 5-year highs.

Export Log Market

China

The CFR prices for New Zealand pine logs in China has continued to increase. The range for A grade logs is 130 for early December shipments to mid-130’s for later December shipments.

Softwood log inventory in China has dropped by approximately 14% over the last month to 3.0-3.2m m3. Inventory levels have dropped about 30% over the last two months., which is a good sign heading towards the Chinese New Year in February 2021.

Daily log use in China is now back to the 100k to 105k m3 range after peaking at over 120k m3 at the end of October.

China’s ban on export logs and sawn timer has widened to include all of Australia. There is no sign of this changing in the short term. In Quarter 3 of this year Australia supplied approximately 11% of the softwood logs imported by China.

The supply chain costs for spruce from Europe continued to increase due to a shortage of containers.

The longer-term supply situation may be beneficial for New Zealand logs with forecasts that 2021 will be the peak of spruce availability from Europe and a proposed Russian ban on export logs starting in January 2022.

India

Sentiment from log buyers in Kandla is turning negative, with reports of four vessels to load from Uruguay, one from Argentina, two from New Zealand and one from Australia. This is a total of eight ships during December for arrival in Kandla in January. Some of the vessels may yet be diverted to China.

Uruguay logs were sold around 128 USD and New Zealand logs around 136 USD CFR Kandla for A grade longs.

Australian logs are quoted at 115 USD levels, with more micro pulp logs at discounted prices, for which Kandla has little appetite.

Lumber prices are dropping rapidly at Gandhidham market. The price of sawn timber from Uruguay logs has dropped INR 20 in the last month to INR 451 per CFT and might drop further due to the negative sentiments of over-supply. The New Delhi national capital Territory (NCT) market is cut off due to the farmers agitation in Delhi borders and poor demand.

As Uruguay is likely to load more ships to China in January, arrivals may reduce in February and sentiments might firm up in March. However, how many logs will arrive from Australia is unknown.

Exchange rates

The NZD was relatively stable during October but has increased against the USD in the first half of November. The CNY has continued to strengthen against the USD increasing the buying power of the Chinese log buyers.

Ocean Freight

The average ocean freight rate has remained relatively unchanged with some minor increases over the last month.

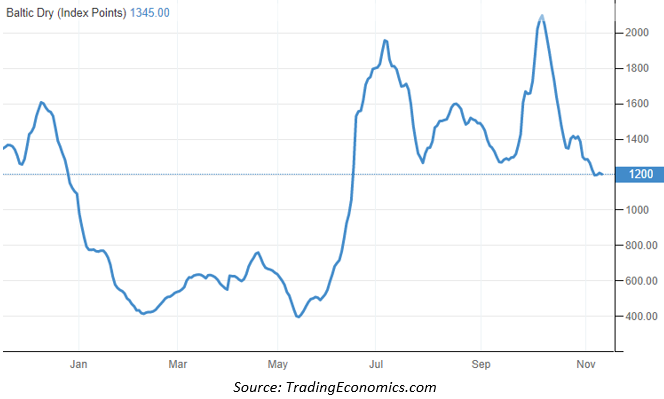

The Baltic Dry Index (BDI) is a composite of three sub-indices, each covering a different carrier size: Capesize (40%), Panamax (30%), and Supramax (30%). It displays an index of the daily USD hire rates across 20 ocean shipping routes. Whilst most of the NZ log trade is shipped in handy size vessels, this segment is strongly influenced by the BDI.

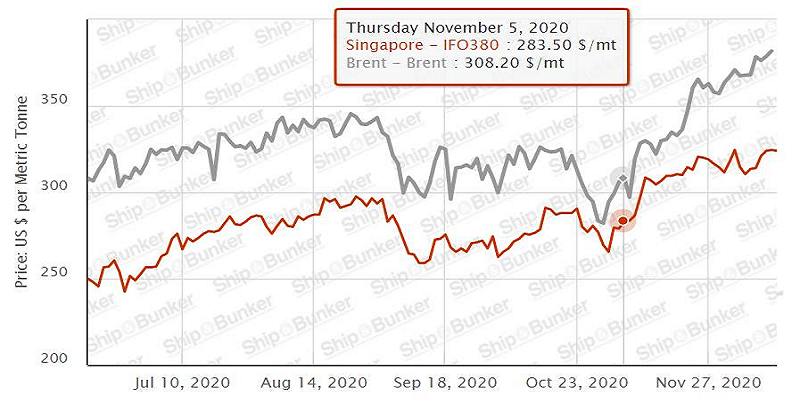

Singapore Bunker Price

(IFO380) (red line) versus Brent Oil Price (grey line)

Source: Ship & Bunker

PF Olsen Log Price Index – December 2020

Due to the increase in export log prices the PF Olsen Log Price Index increased by $4 in December to $124. The index is currently $3 above the two-year average, $1 above the three-year average, and $1 above the five-year average.

Basis of Index: This Index is based on prices in the table below weighted in proportions that represent a broad average of log grades produced from a typical pruned forest with an approximate mix of 40% domestic and 60% export supply.

Indicative Average Current Log Prices – December 2020

| Log Grade | $/tonne at mill | $/JAS m3 at wharf | ||||||||||

| Dec-20 | Nov-20 | Oct-20 | Sep-20 | Aug-20 | Jul-20 | Dec-20 | Nov-20 | Oct-20 | Sep-20 | Aug-20 | Jul-20 | |

| Pruned (P40) | 170-195 | 170-195 | 170-195 | 170-200 | 170-200 | 170-200 | 170-185 | 170-185 | 165-175 | 155-165 | 162 | 162 |

| Structural (S30) | 115-130 | 115-130 | 115-130 | 110-120 | 110-120 | 110-120 | ||||||

| Structural (S20) | 105 | 105 | 105 | 105 | 105 | 105 | ||||||

| Export A | 138 | 130 | 128 | 123 | 119 | 119 | ||||||

| Export K | 131 | 122 | 120 | 115 | 111 | 110 | ||||||

| Export KI | 120 | 113 | 112 | 106 | 102 | 104 | ||||||

| Export KIS | 115 | 105 | 104 | 97 | 95 | 99 | ||||||

| Pulp | 46 | 46 | 46 | 46 | 46 | 46 | ||||||

Note: Actual prices will vary according to regional supply/demand balances, varying cost structures and grade variation. These prices should be used as a guide only.

A longer series of these prices is available here.

Log Prices

Select chart tabs

This article is reproduced from PF Olsen's Wood Matters, with permission.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.