Fonterra has today released its FY26 Q3 business update. Year to date their total group operating profit of was $1.8 bln, up +$103 mln on this time last year. That will deliver a profit after tax of $1.1 bln, equivalent to 65 cents per share. (Adjusting for Mainland’s result to reflect the Co-operative's underlying business, the Co-op delivered $946 million profit after tax, equivalent to earnings per share of 57 cents, up from 53 cents this time last year.)

They lifted and narrowed its full year forecast earnings range to 60-70 cents per share, due to confidence in the Co-op’s contracted sales position for FY26 and their ability to navigate ongoing supply chain disruption.

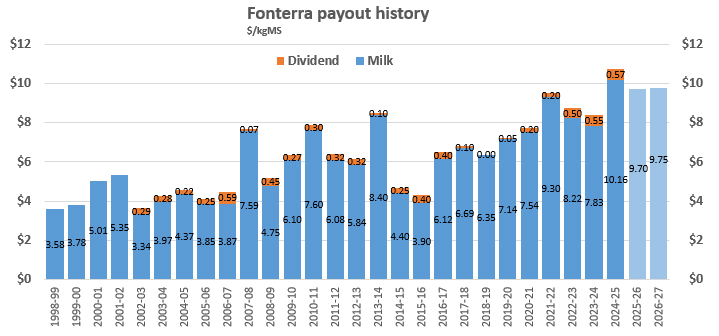

The forecast Farmgate Milk Price midpoint for the current season is unchanged at $9.70 per kgMS, with the range narrowing to $9.60-$9.80 per kgMS.

They have also announced an opening forecast Farmgate Milk Price for the 2026/27 season of $9.75 with a range of $8.00-$11.00 per kgMS "to reflect potential impacts across the season from ongoing geopolitical risks and inflationary pressures".

Business performance

They said the Ingredients business benefited from ongoing protein demand in the US and Europe, while Foodservice continued to achieve both volume and margin growth.

Outlook

“Our full year earnings guidance reflects the strong shipment volumes expected in the final quarter of the year," CEO Richard Allen said.

“However, we acknowledge the uncertainty caused by the ongoing conflict in the Middle East. Like our farmers, and others around the world, we are experiencing cost inflation and shipping disruptions.

“We are confident that our deep relationships with customers and logistics partners will continue to help us navigate these challenges.”

Fonterra's full payout history, along with other dairy company payouts, and analysts forecasts, is here.

3 Comments

One of the few area's of the economy still smiling.

That's pretty damn good from Fonterra and huge kudos to Miles Hurrell. Be real interest in the earnings per share with the brands gone going forward, my thinking has always been it will get better.

Agree, economically 2026 should be good for dairy farming (and Fonterra). But don't overlook the much improved tourism sector. Or the positive sheep & beef sector. Or the strong Kiwifruit sector. Or the quickly-recovering education sector. There are increasing numbers of areas that are on the improve. There will be others.

The negative conversation tends to be focused on residential and commercial property, which are getting re-set after years of unsustainable activity. We are lucky there are other, outward-facing sectors that are doing well and moving forward, while this necessary and overdue correction takes place. Housing is 'shelter', and should never have been allowed to become an 'investment'. Tax settings are to blame (no CGT). I hope we are seeing a generational shift in thinking about housing's place in our economy. It is just a shame many KiwiSaver funds are so average, undermining the strength proper investing should play. But at least you have a choice of KiwiSaver funds and can find good ones. It's a crude benchmark I know, but surely KiwiSaver funds can do as well as NZ Super?

Perhaps my dislike of GDP all these years was incorrect. The industries you mentioned aren't exactly large in GDP figures despite being the absolute vast majority of export earners. With most people involved elsewhere the positive side of the equation may not be enough to sift the whole economy proving the measure correct.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.