By Alex Tarrant

Overall farm profits before tax are forecast to rise 53.7% to NZ$6.916 billion by 2014/15 as revenues rise faster than interest payments, according to the Ministry of Agriculture and Forestry (MAF).

Interest payments made by the agriculture sector are forecast to rise 27% between 2011 and 2015 as interest rates rise, MAF said in its annual Situation and Outlook for New Zealand Agriculture and Forestry (SONZAF) report for 2011, released today.

Total gross revenue for the sector is expected to rise 32.2% from 2010/11 to NZ$32.149 billion by the year to March 2015, while final income for the sector once costs and interest payments are taken away, is expected to rise 53.7%. However forecast revenue increases from March 2012 are largely relying on a depreciating New Zealand dollar from the middle of that year, MAF said, pointing to Treasury forecasts. The NZ dollar hit a post-float record high of 83 US cents in the past week.

Treasury is forecasting the Trade Weighted Index will drop to 56 by the March quarter of 2015 from 71 now.

The global financial crisis in 2008 and 2009 had seen growth in credit to the agriculture sector fall away, while farm sales and prices declined, MAF said in the report. Falling land values had increased the sector's leverage, which left farmers reluctant to take on more debt.

In its latest Monetary Policy Statement for the June quarter, the Reserve Bank of New Zealand said farmers were using current high prices mainly to pay down debt, although the RBNZ expected to see the sector begin investing and spending again when debt was back at managable levels over the next year.

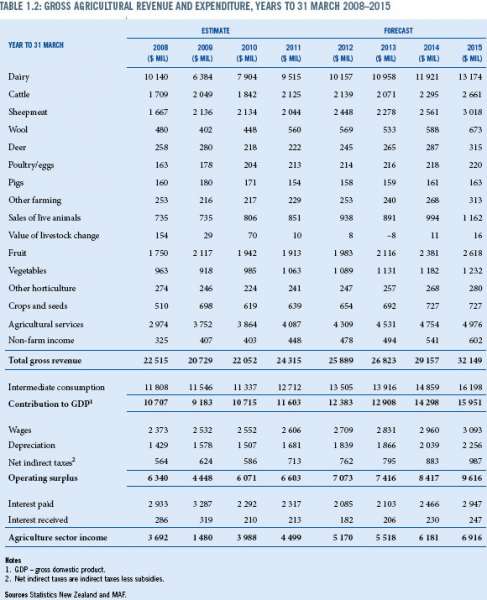

The numbers

Interest payments made by the agriculture sector are estimated to have fallen 30% from NZ$3.287 billion in the year to March 2009 to NZ$2.292 billion in 2010 before rising again slightly to NZ$2.317 billion in the year to March 2011. MAF forecasts interest payments to climb another 27.2% to NZ$2.947 billion by 2015.

Total gross revenue produced by the agriculture sector is expected to rise 32.2% between now and March 2015 from NZ$24.315 billion to NZ$32.149 billion.

The sector is expected to produce an operating surplus, before interest payments, of NZ$9.616 billion in the year to March 2015, an increase of 45.6% from 2011. Taking off interest payments, total agriculture sector income is expected to rise 53.7% from NZ$4.499 billion in the year to March 2011 to NZ$6.916 billion in the year to March 2015.

See the full table from the MAF report below.

The crisis hurt

"Over the decade, to 31 March 2010, aggregate credit extended to agriculture by both banks and non-bank lending institutions grew at an average growth rate of 14% a year," MAF said in the SONZAF report.

"With the global financial crisis in late 2008 and 2009, when international credit availability became more restricted and the outlook for agricultural commodities worsened, agricultural borrowing, farm prices, and farm sales all declined significantly. Aggregate credit extended to agriculture by both banks and non-bank lending institutions was constant in the year ended 31 March 2011," MAF said.

"The decline in farm sales has reduced the equity withdrawal from the agriculture sector. This occurs with farm sales as older farmers with relatively high levels of equity are more likely to be selling and younger farmers with lower levels of equity are more likely to be buying," it said.

"Also, falling land values have, on aggregate, increased the leverage for the sector, which leaves farmers reluctant to take on new debt and increases the perceived riskiness of the sector to lenders. The fall in land values has been significant, with Quotable Value New Zealand’s total rural land price index at June 2010 18% below the peak achieved in June 2008."

Gross agricultural revenue was estimated to have increased by 10% in the year to 31 March 2011, driven by significant increases in dairy, cattle, and wool revenue.

"As a result of a later lamb slaughter in summer and autumn 2011, improving lamb schedule prices do not flow through to revenues until the year to 31 March 2012. Beyond 2012, increases in revenue are mainly driven by the assumption of a depreciating New Zealand dollar," MAF said.

"Aggregate interest paid by the agriculture sector has declined significantly since the year to 31 March 2009, primarily because of lower interest rates but also because the aggregate stock of agricultural debt has stopped growing. Interest payments are forecast to increase with assumed rises in interest rates and the relatively slow growth in the stock of debt," it said.

"Agriculture sector income, an aggregate measure equivalent to the overall agricultural sector’s farm-gate profitability, is estimated to have risen by 13% in the year to 31 March 2011. Further growth in income is expected as revenue rises faster than interest payments, in particular."

High NZ$ taketh away but also giveth

The SONZAF report said New Zealand agriculture exporters were receiving high prices for their wares as a rebounding global economy drove demand for commodities. However, it noted commodity prices had been driven upward partly due to suply disruptions in other parts of the world.

"Short-term supply disruptions such as droughts and floods in various parts of the world are a significant factor supporting recent agricultural price increases. At the same time, the strength of demand coming through from emerging markets, the recovery in many developed economies, and continuing demand for agricultural resources for biofuel production has led the Ministry of Agriculture and Forestry to revise upwards its view of medium-term international agricultural prices," MAF said in the report.

"The relative strength in the New Zealand dollar has seen only a portion of these foreign currency price gains passed through to New Zealand farmers and foresters. The strong New Zealand dollar has, however, also reduced the impact of price rises in imports, especially fuel and fertiliser," MAF said.

"Beyond 2012, steady production growth in dairy, forestry, wine and kiwifruit, together with an assumed depreciation in the New Zealand dollar, leads to strong forecast growth in export revenues."

Dairy outlook positive

Meanwhile, the outlook for New Zealand's dairy sector, which accounts for between a third and half of all agriculture revenue, was positive over the next four years, MAF said.

"MAF estimates that milk solid production will increase by 2.4% for the year ending 30 May 2011, 5.7% for the 2011/12 season and 2.9 and 1.2% for the following years," it said in the report.

"Dairy export revenue for the year ending 30 June 2011 is estimated to be NZ$13.0 billion. Increased milk solid production, along with high dairy prices, is forecast to increase export revenue for the year ending 30 June 2012 to NZ$14.6 billion, or 12%. Further out, export revenue is forecast to increase by another 6.9% for the year ending 30 June 2013, with more gradual increases thereafter," MAF said.

Dairy prices

International dairy prices had been increasing since the middle of 2009 but had not yet reached the highs of 2008, with butter being the exception. Since mid-2010, butter prices had increased faster than all other dairy product prices. Most other commodity prices had also increased rapidly in recent months, fuelled by strong demand.

"The outlook for dairy demand in 2011 is robust, based on both rising incomes and population growth in developing countries," MAF said in the report.

"Dairy products, especially milk powders, are in strong demand in developing countries like China, underpinning high international dairy prices. Increasing world oil prices should also support strong demand, and thus high international prices, for dairy products from oil-exporting countries, like Venezuela, United Arab Emirates and Saudi Arabia. These countries are already important dairy export markets for New Zealand," MAF said.

"An assumed return to average weather and high international prices is expected to encourage higher milk production in the major producing and exporting economies, such as the EU, US and Australia, lifting world dairy production beyond 2011. Producers in the US are already responding to high dairy prices by increasing exports and production, despite high corn prices," it said.

High corn prices were expected to moderate production growth in countries that mainly used feed-based systems but the additional product available should ease some of the pressure on international prices over the medium term.

"The milk price for the 2010/11 season is estimated at NZ$7.50 per kilogram of milk solids, 9 cents short of the historic high of three seasons ago. International dairy prices improved as the season progressed, lifting the milk solid price," MAF said.

"MAF forecasts the milk price for the year ending 31 May 2012 at NZ$6.87 per kilogram of milk solids. This price reflects the assumption of softening international dairy prices as world supply starts to respond to increasing world demand," it said.

"Beyond 2012, the assumption of a depreciating New Zealand dollar drives most of the lift in the milk price, which is projected to be NZ$8.64 per kilogram of milk solids by the year ending 31 May 2015."

(Updates with link to full report)

26 Comments

"Beyond 2012, steady production growth in dairy, forestry, wine and kiwifruit, together with an assumed depreciation in the New Zealand dollar, leads to strong forecast growth in export revenues."

I thought the reason for the high NZ$ was due to the demand for our commodities. If this demand remains along with high commodity prices, where is the reasoning for the depreciating NZ$? Assuming the NZ$ does depreciate then the cost of inputs increases as well - a lot of reliance then on production volumes increasing.

How much faith being placed on Treasury forecasts?

What happens if commodity prices don't remain high?

Where are the actuals to compare with estimates for 2008, 2009 and 2010?

This link will give you previous forecasts:

http://www.maf.govt.nz/news-resources/publications?title=Situation%20an…

MAF places total faith in TSY forecasts. From their 2009 forecast we should now have TWI at 52 and USD at 0.52 - based on those TSY numbers. But it is not all TSY's fault - MAF's 14% forecast increase in milk production for this season came in at I think 2.4%.

MAF has at least returned to providing figures on agricultural revenue and expenditure, something they took out last year. Maybe a change in Director General helped. I don't think the last one liked me doing comparisons of their past projections with their current estimates.

If you want a very positive view of NZ agriculture's medium term future I would recommend MAF's Situation and Outlook. I think it is probably compulsory material for all government economic forecasting e.g. TSY.

Maybe Roger J Kerr advises them on currency moves...

Have you still got those comparisons Colin?

Have just updated with a link to the full report on MAF website.

Cheers

Alex

The link I provided earlier gives MAF SONZAF's from 2000 to 2011. MAF's website didn't when I was looking for them a couple of years ago have any before 2007.

There is some fascinating stuff about dairying and MAF's expectations of DIRA especially in those up to 2005.

so are they assuming a strengthening US economy and therefore a stronger US dollar versus the kiwi?

I wouldn't be so confident of that - I see a period of Japanese style stagnation hitting the US

You are right Matt...it's just rubbish talk.....and the USA is on course for depression time...riots...killings and emigration....

I'll keep that in mind here in California. Thing is, if the US takes that dive then so too will half the planet. In the meantime I will go back to enjoying some sun.

later

I don't think the US will take a dive - I think it will be similar to Japan.

It will recover, but never fully

It will plow along at sub-optimal growth levels

China will fall back a bit in the next year or two, and then resume a sligthly lower level of high growth

And that goes for the EU , too ... they'll plod along for a few years , gradually deleveraging their debts ....... quietly being overtaken by the prudent economies of Asia , plus India & Brazil . ....

...A gradual shift in economic power from West to the East . And we are the lucky ones to be witnessing this momentous change !

[ ... one needs to read between the lines with " Wolly-speak " : when he says riots and blood in the streets , he actually means that a guy delivering fresh chicken meat will trip over another guy , holding a " Vegans Rule " sign... . ]

hehehe...always enjoy the riots...hey we had them on Auckland didn't we...all hushed up...

Funny thing is Gummy.....time will see the Chinese bitching about jobs being lost to low income Americans and dives in Europe...

I've heard tell that the Chinese coast-guard is on high alert to intercept American boat-people , refugees from " Obamanomics . "

... apparently Vietnam is the place to set up your sweat-shop ........ oooops , ah , I mean to set up your factory .

well I got a laugh out of it.......! it's that iron ronnie...running hot.

You really think that China can sustain current trends of growth? You must be kidding. Its maintained by the Chinese Communist party's willingness to backstop malinvestment by local authorities and their pet developers, but it can't continue much longer. The collapse will be bloodier and deeper than bubble bursting in Europe and the United States thats for sure. Watch this space.

http://www.sbs.com.au/dateline/story/about/id/601007/n/China-s-Ghost-Cities

Hey Justice...I appreciate your busy.....but if you can spare an envelope..post back a few rays o that California sunshine....I'm working on a winter tan thingy...my therapist says if i feel like shit...I'll need to colour up some to get in sync.

You haven't been reading this have you Wolly?

http://www.marketoracle.co.uk/Article28574.html

Of course, if QE3 does go ahead is that a positive or negative for our primary sector?

Nah...missed that...jeez oh dear....QE2 is not to stop....therefore no QE3!....I suspect all eyes are turning to Greece and China....look to a collapse in Europe first...but that's just a guess.

I also see rising credit costs as a result...not due to inflation...but to the haircuts...the impact from the rises will be critical.

Explains why Treasury etc have been borrowing all they can get at low rates...they have been shorting the bond mart! haha.

..' but that's just a guess' Hell, Wolly I thought you were been factual

Nah..crap like that is for the "experts" Muzza...I prefer to ask Blue what he thinks will happen and go on how loud the bugger barks at me.

Hey Muzza..check out channel 73 at 730....I'm sure I had one of them coins...dang thing was here somewheres.

From my accountant

He has just been to a presentation by Khoon Goh an ANZ economist. He said that we are heading to a golden age selling stuff to the right people now, China is our 2nd biggest trading partner and with Asia growing strongly, we are selling the right things and demand will continue to increase. He thinks we are heading back to the 70's when we had the 2nd highest standard of liveing in th OECD.

Mind you, in 1972 my father tells me the beef schedule dropped from $1.50 a lb to .43c a lb in a few weeks.

Happy days are back again, from the same bank that won't lend any money to farmers, to buy more land. However I see a Russian has been busy buying Mt Potts as a private play ground and a few others.

He has just been to a presentation by Khoon Goh an ANZ economist.

I suspect ANZ is trying to reduce its exposure to NZ agriculture, and Goh is spinning a line to encourage everyone else to come to the party. Goh's job is therefore more likely to be marketing spin than providing independent economic analysis. An ANZ economist? Doing presentations to accountants?

Field days will tell us something

Please let me know what it is.

Thanks.

yeah funny isn't it how these bank economists are so bullish yet their banks are so unwilling to lend. They are certainly not walking the talk!

I know bugger all about agriculture, but in terms of housing if these banks are so bullish about housing why aren't they stepping in more and lending to developers??? If demand is outstripping supply and prices are "edging higher" then surely there is little risk to the banks??????

Optimistic dreaming.

Before optimists are dreaming of growing world economies into another boom, climate change, shortage of resources and as a consequence, the destraction of our planet/ environment and political unrest will dominate - all causing costs in the trillions – “Broom Economies”

Where is the money ?

E.g. China uses about two barrels a year of oil per person. In the United States we use 23 barrels of oil per person per year. If China’s usage grew to the U.S. equivalent, it would be 85 million barrels a day, which is about the total consumption of oil for the world.

http://oilprice.com/Energy/Energy-General/A-Look-at-Chinas-energy-Futur…

Walter : Why would you extrapolate from US usage of oil , and assume that China will consume as much , per capita ? ...... Not just a long-bow that you're pulling there , my friend , a positively stratospheric one .

....... unlike the US ( whose presidents , such as Jimmy Carter , were acutely aware of the energy problem ) , China's leadership is actually doing something aboot it . They're pumping billions into alternative energy R & D . And currently , Chinese companies lead the world in solar panel research & manufacture .

As much as China currently gobbles up fossil fuels , they know that cannot continue indefinitely .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.