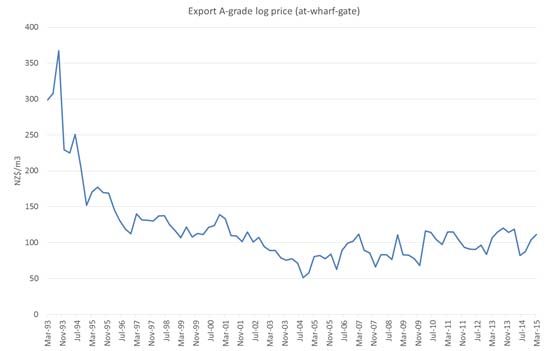

During the 1990s forestry investment was at an all-time high in New Zealand.

This was stimulated by a price spike in 1993 which saw log prices reach an historic record high in the third quarter of 1993.

Export A-grade peaked at $370/m3 delivered to wharf gate (NZ port).

Source: MPI

From 1992 to 1999 there was an average of 65,000 hectares per year of new commercial forest planting. In 1994 new planting levels peaked at 98,000 hectares. Radiata pine forestry was the new “green gold” with the associated talk of riches and a “paradigm” shift in the markets.

What has transpired in the market since is radically different from most of the expectations of those that participated in the planting boom and financial returns from well-managed forests have gravitated to be more in line with other comparable land uses.

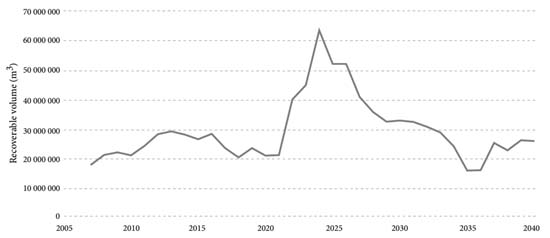

Twenty three years on from the start of the planting boom, these forests are nearing maturity. The chart below shows one scenario of the potential wood availability. A key characteristic of the massive increase in wood availability is that it is entirely from the smaller (less than 1,000 hectare) forest owners.

Source: MPI

The actual increase in harvested volumes won’t look like this chart. This is partly because the chart is based on harvesting at age 30, whereas the average harvesting age is actually several years younger than that, especially when the log market is strong.

The increase will also be constrained by logging, transport and port capacity. PF Olsen conservatively estimates that 300 additional harvesting crews and 900 additional logging trucks will be required to tackle the projected volumes. Most of the volume will have to be exported unless there are significant expansions in domestic processing. This is expected to double the current volumes going through New Zealand’s log export ports. With these constraints, it is unlikely that harvest volumes will be able to increase any more than 20% year-on-year.

The profile of these large areas of maturing forests are:

- Smaller blocks. An estimated 80-90% of the owners have forests less than 100 hectares.

- Greater distance to domestic processors and ports – higher log transport costs.

- Steeper (more hilly) terrain and higher logging costs.

- More rigorous environmental and safety compliance based on revised legislation relating to principal’s duties and higher societal expectations.

- As a result of the above, relatively lower stumpages (net return to the forest owner). Lower stumpages are much more sensitive to log price swings. For example, a $10 log price increase means a 50% increase in a $20 stumpage, but only a 20% increase in a $50 stumpage.

- Higher volatility in harvesting volumes based on more market-sensitive stumpages (above) and shorter harvesting time-frames. Smaller blocks are exposed to the market for shorter periods. Smaller forest owners are, therefore, more likely to suspend harvesting during market downturns.

There will be increased tension between forest owners wanting to avoid selling logs in a down market and harvesting contractors needing steady work to maintain financial viability and skilled workers. While this tension exists today, it will be much more significant in the future as harvesting shifts from predominantly larger forests to predominantly much smaller blocks.

Large areas planted in Radiata pine forests in the 1990s are approaching maturity with significant implications for the sector.

The other big question is whether the markets can take the volume.

Announcements of large increases in capacity at Red Stag and Lumbercube will make a material difference in log demand in the Rotorua area, but have little impact elsewhere. Other areas will likely have to rely almost entirely on increased log exports. Our current log markets have the potential to easily absorb the increased volume, so long as the key purchasing countries’ economies continue their current strong growth.

Competition of supply from other sources is not expected to be too big an issue especially if the current momentum to reduce illegal harvesting around the world continues. However, when the above are unfavourable, New Zealand’s increased harvesting volumes do have the potential to weigh heavily on a soft market.

Implications for the sector

The above context is expected to result in the following trends:

- Rationalisation – aggregation of the larger forest blocks into single ownership entities (usually specialist timber investors).

- Attempts to form harvesting cooperatives/clubs to provide more efficient working programmes, more work stability and better log marketing. Such arrangements, however, have had low uptake in the past mainly due to individual forest owners all believing that they can time their harvesting for the peak of the market (despite the physical impossibility).

- Increased challenges for harvesting-related contractors, mainly in the form of attracting and retaining safe and skilled workers and high debt levels with volatile work programmes.

- Congestion at those log export ports that have made insufficient investment in infrastructure to handle the increased volumes.

- Greater benefits from getting Harvest-Ready early. This includes mapping, developing an inventory of the timber in the block and harvest planning.

- Widespread disappointment amongst forest owners who take an opportunistic approach to harvesting and try to time the market, but get left with no harvesting capacity or the high risk of using unsafe and low-quality contractors.

- A higher level of sales of near mature/mature forests (and land) as owners opt for an easier sales option and earlier cashflow. This options can also take away the residual land issue after harvesting.

---------------------------------------------------------------

This article is reproduced from PF Olsen's Wood Matters, with permission.

7 Comments

Sawmiller - ie expert processor and marketer, tells me Radiata is poor quality below thirty years and gets better for every year after that.

What drives the short term managment and setup that leads to so much been felled shortly after twenty.

I was surprised as well at that level of early felling. Perhaps these are large plantations on reasonably easy slopes - and the owners profit objectives are largely driven by re-conversion to pasture?

I remember a forestry worker in Marlborough saying 25 years to first harvest for pine, then 35 years to second harvest. Which gives an idea of how hard pine is on thin NZ soils.

What does stumpage related to in standard accounting terms? Revence or GP?

Harvesting co-operatives; or co-operatives in modern NZ have been shown to be very untrustworthy.

Hire outsiders you get a Fonterra taking over the operation killing the small holders - handle it in house you end up with a Red Meats collective where none of them agree on anything and end up split over their original interests and everyone loses.

Many of us have good reason not to like the English style Unionists - but the old ones were actually working for their industry not their own interests. They no long seem to exist in modern NZ.

too many...what did the guy say here on Interest.co.nz comments... "Winners" he called those with the money and privileges. Too many guys like that wanting to be "winners" and damn all the "losers" because it's their fault.

Are there figures available to what macro-economic volume of _mature_ logs will come through?

Are those figures publicly available as that would allow the industry ... 20 years? ... to prepare for volumes.

Personally when I'm doing building work with houses/fencing I constantly shake (haha) my head at the low quality of modern pine timber.

but 23 yrs vs 30 yrs, what NZ business can afford to take a 25% drop in turnover (with no price increase, and 33% higher ongoing expenses per unit) just to put out a good quality product

Interesting that there is no comment at all on the influence of the carbon market on owner decision-making. I'd have thought a great deal of the forests are registered under the ETS. Perhaps not many sold their credits and therefore won't need to purchase on harvest? Or maybe there is a thought that these cheap offshore credits of dubious 'quality' will continue to be available? Or maybe there is an expectation that the whole obligation will just be scrapped?

What might oil prices do to the log market?

or the wool market

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.