Content supplied by Rabobank

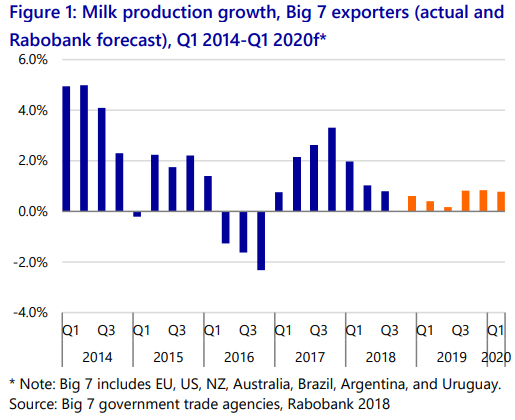

The specialist agribusiness bank says milk supply growth across the Big 7 (the EU, the US, New Zealand, Australia, Uruguay, Argentina & Brazil) sunk to 0.8 per cent year-onyear in quarter three and indicative quarter four numbers show a similar modest growth rate.

Report author, Rabobank dairy analyst Emma Higgins said the minimal growth rate was largely a result of lower production in Australia, the EU and the US.

“The lingering effects from mother nature have severely impacted Australian milk flows and stalled European growth with feed quality and quantity impacted across the second half of 2018. The US also looks set to see the lowest year-on-year milk production growth since 2013, due largely to tightening margins,” Ms Higgins said.

Yet while production growth in these regions was slowing, Ms Higgins said other corners of the dairy exporting globe were posting positive production growth.

“Brazil has moved into growth territory during quarter three 2018 as a result of more moderate feed costs and profitable milk prices, while Argentinian producers have overcome inflated milk production costs and continue to make a recovery from the low volumes delivered in recent years,” she said.

“But the star performer clearly remains New Zealand, setting a new record for peak milk flows in the month of October.”

Ms Higgins said the counter to strong New Zealand milk production has been sliding Oceania commodity prices, a theme evident across much of the season.

“With season-to-date milk production in New Zealand tracking six per cent higher than last year, the additional product has needed to find a home. There’s been 17 per cent more Whole Milk Powder offered on the GDT platform over the course of the season – and the average Whole Milk Powder price has tracked equally lower over this time,” she said.

“While December Global Dairy Trade (GDT) events have seen marginally better prices, the run of falls across earlier months, combined with the recent uptick in the New Zealand dollar, has fed into the bank’s downward revision to its full-year forecast from NZD 6.65/kgMS to NZD 6.25/kgMS for the 2018/19 dairy season.”

Challenging global production environment anticipated to lead to pricing upside

The report says a challenging environment for global milk production expansion lies ahead in 2019.

“Herd numbers continue to shrink in Australia, Europe and the US to either mitigate escalating costs and/or overcome disappointing farmgate milk prices,” Ms Higgins said.

“Australia faces a slow recovery with industry confidence severely knocked while consolidation of farms numbers in the US and Argentina is also set to continue and the EU is finding its footing post-quota removal and drought impact.”

Ms Higgins said New Zealand would also face barriers to milk production growth in 2019 as a result of stronger competition for other land uses and resource constraints.

“Rabobank’s full 2018/19 season milk production growth forecast for New Zealand has been lifted to 4.5 per cent, effectively underwritten by the favourable seasonal conditions to date. However, we expect to see a decline in milk flows across the first half of the upcoming 2019/20 season in comparison to the last six months of 2018, with the extraordinary seasonal conditions unlikely to be repeated.”

At a global level, Ms Higgins said slow and very modest global milk production growth was expected over the next 12 months.

“The net exportable surplus available from the “Big 7” will be limited across our forecast period to quarter one, 2020. Coupled with low stocks and steady demand, the risk is that the market moves rapidly upwards and catches buyers unaware, particularly in the first half of next year,” she said.

Uncertain demand outlook

The report says considerable uncertainty underpins the dairy demand outlook for 2019.

“There are several geopolitical irons in the fire that could have a major impact on dairy demand. The UK-EU divorce continues, while the fine print of a trade truce between the US and China still needs to be written,” Ms Higgins said.

“Oil prices have also recently taken a bearish slide and there are headwinds emerging at the US retail level for dairy demand.”

Ms Higgins said while Chinese dairy imports were anticipated to increase significantly in 2019, there were also uncertainties in the demand outlook in this market.

“As a result of a lower expectation of Chinese milk production growth in 2019, we’ve recently revised up 2019 growth in China’s import need to 11 per cent,” she said.

“However, China’s economic growth outlook and the unbalanced bargaining power between producers and processors continue to place a lot of uncertainties over the growth in dairy demand and milk production. And the recent developments in the political relationship between China and Oceania is certainly adding another layer of complexity.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.