By Brian Fallow

The Reserve Bank’s May Financial Stability Report (FSR) understandably focuses on risks to the asset side of banks’ balance sheets.

But there is also a risk sitting there on the liability side on the books in the form of a high degree of dependence on importing the savings of foreigners to fund their lending.

“Offshore credit markets are a key source of funding for New Zealand banks, representing close to a quarter of their total funding,” it says.

And indeed the statisticians tell us that at the start of this year the net foreign liabilities of deposit-taking institutions stood at $120 billion, equivalent to about a quarter their loan book at the time.

But the FSR is at pains to allay fears of any repeat of the episode during the Global Financial Crisis (GFC) when offshore funding markets froze and the Government had to hastily stand guarantor to the banks.

That fright led to the adoption of the Core Funding Ratio (CFR), which sets a minimum proportion of banks’ funding that has to come from “sticky” sources: retail deposits or long-term wholesale funding, where long-term is defined as a maturity at least a year out.

The banks’ aggregate CFR peaked at 89% last month, compared with 66% ahead of the GFC.

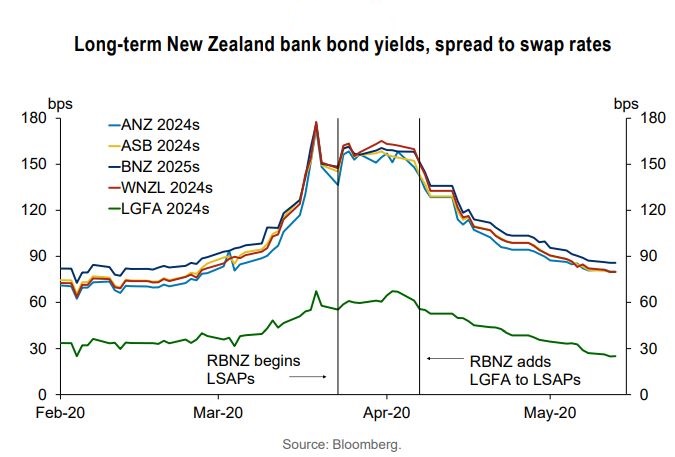

In March the markets delivered central banks another scare, evident in New Zealand’s case by a sharp rise in government bond yields, which prompted the Reserve Bank to immediately begin quantitative easing, something it had not had to do before.

Offshore funding spreads, which reflect the cost New Zealand banks would have to pay if they were to access term funding from international markets, also briefly spiked, though not to the heights seen during the GFC.

Not to worry, though, is the message from the FSR: “However, since February no New Zealand bank has needed to issue term funding in these markets, as the extension to the average term of their funding in recent years now allows banks to wait out the market turbulence and only return to these markets when they have normalised.”

But that sanguine and soothing language implies it is possible to tell how long the current global ordeal, and its attendant risk of further turbulence in offshore credit markets, will last. And no-one knows that.

What we do know is that the world went into this crisis carrying more debt, relative to the size of economies, than before the GFC.

New Zealand is an exception. Its total debt (government, corporate and household) stood at 204% of GDP at the start of the year compared with 208% in 2007, according to the Bank for International Settlements.

By contrast for the emerging market economies as a group (which includes China) the ratio has increased from 143% to 194% over the same period. It has also increased, though not as much, for advanced economies as a group.

These debt to GDP ratios will be worsening rapidly in the context of a gruesome global recession.

Some limited debt relief has already been extended to developing countries, which have to borrow in hard currencies and which are looking at evaporating export incomes even as the pandemic bears down on them. But the clamour for more debt relief is rising.

And at the other end of the spectrum the US Federal Reserve has announced it will extend its QE purchases to some corporate debt rated “high yield”, the polite term for junk. Glass half full, it is willing to do that; glass half empty, it considers it necessary.

So how exposed are New Zealand banks to further turbulence in offshore funding markets in this environment?

The FSR tells us that as of March just under half of banks’ $135 billion of wholesale funding had a maturity of between one and five years. How much of it is closer to one year than five is unclear, as is the key uncertainty in all this: How long will the Covid crisis last?

In the mean time the Reserve Bank has been doing a bunch of things to inject liquidity into the banking system.

Quantitative easing has that effect, for a start. The money the Reserve Bank creates in order to buy government bonds increases the level of settlement cash, the money banks have on deposit at the central bank.

It has also introduced a weekly corporate open market operation facility which allows banks to use corporate debt securities as collateral when borrowing cash from the Reserve Bank. “This gives banks confidence to buy these debt instruments, secure in the knowledge they can be exchanged at the Reserve Bank for cash.”

Then there is the Term Auction Facility offering collateralised loans for up to 12 months, and the Term Lending Facility offering loans for a term of three years.

All these initiatives are evidence that the Reserve Bank, as banker to the banks, is ready to ensure they can access all the money they need to do the lending we need them to do.

Given then banks’ high reliance, in normal times, on imported credit – the flip side of New Zealand households’ collective tendency to spend more than their income – that is just as well.

The chart below comes from the Reserve Bank's Financial Stability Report.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

35 Comments

We do not need to save or borrow from abroad in order to expand investment and growth

A basic argument by economists has been that we first need to accumulate scarce savings in order to fund investments and hence enjoy economic growth – or alternatively borrow those savings from abroad by taking a loan from the international banking community. But this argument is based on the erroneous belief that banks are merely financial intermediaries that require savings first in order to be able to lend money out. In reality, increased domestic investment requires neither savings nor borrowing from abroad. Domestic banks can fund domestic investment without prior savings becoming available. Link- section II. - 4

I get the basic principle of banks creating credit through loans, but does the maths actually scale to the volume required within the current regulatory capital ratios?

Capital ratios are applied on a percentage basis to the asset ledger and thereafter risk weighted, why can that not be scaled as long as banks' shareholders and regulators don't cap it.

Thanks.

So then, assuming no regulatory interference, the only upper limit is the limit of shareholders willingness to keep funding it. Given both the actual and implied government bank guarantees that limit must be very very high. I mean, if things go widely sour in the investment environment where else could you put your money in any flight to safety?

Ever lower interest rates will show us just how "sticky" those retail deposits really are. Even the RBNZ are saying depositers will need to put their money elsewhere to get a return.

A bank run? - there isn't enough cash - and asset diversification results in the vendor swapping it for bank deposits.

The issue is the type and risk profile / term.

Just because it’s a bank deposit doesn’t mean it’s eligible to pair a bank asset. E.g on call vs sticky.

A bank run can occur if foreign deposits leave, and takes the form of USD pressure, reduced reserves or increases in USD swaps etc.

Can you detail what you mean by foreign deposits, if you reference something different from this declaration?

Foreign claims on NZ banks by BIS shows some holdings, but is largely by parent co holdings in AUD. I’d guess your link would reference that same table, would need to check.

I’m picking the non-resident liability refers to onshore banks only?

At a high level I view any NZD instrument as a deposit, they work the same, just the term is different. So bonds, deposits, transaction balances, savings balances etc, I wrap them all up as one.

Net foreign liabilities shows the true extent, which overall represents foreign deposits in my eyes (as a foreigner has a claim to it)

A bank run can occur if foreign deposits leave,,,

If they are NZD instruments which foreigners claim, how do they leave a bank's ledger balance as you say? Surely the foreign claimant sells/swaps them to another NZ registered deposit taking party to purchase another currency or security, leaving these NZD deposits on the ledger of an institution in the realm of NZ's banking jurisdiction.

Yes and I completely agree, but everyone knows that.

Which is why I said it results in USD pressure, in swaps and spot rates. March is a perfect example, foreign deposits left (they had been for a while now but not that heavily)

The forward curve blew out and was illiquid, netting the CC basis you see large swings, domestic bonds vs 90d or OIS.

The way the ledgers are cleared fyi, is via the trade balance flows over time. Export incomes reduce foreign holdings of NZD deposits (or results in large pressure upward on kiwi if they stay and the trade balance is in surplus)

The newly generated USD earnings replace foreign deposits here.

Bank runs are highly associated with cross border flows and exchange rate depreciations (which is why the RB has refused to talk about the exchange rate for the last 18 month essentially)

Edit: or the RB reduces its reserves, or engages in fx swaps with the Fed (which is why the fed has done swaps recently, it’s a form of USD intervention for them)

The issue is that the foreign deposits vastly exceed fx reserves here

The other issue is that NZD deposits can be sent from a local bank, to outside the domestic regulation, I.e the offshore Kiwi market. I don’t think a lot of foreigners actually invest directly with Domestic NZ banks, would likely be offshore banks that then lend to NZ institutions, they don’t need to be directly lending to banks either (think Visa, or PayPal or whoever), then those funds eventually end up in local banks etc

Thank you for your outline of NZ current account deficit financing. And much has been made of Fed USD swap lines, but I don't believe our banks have issues borrowing dollars to engage in xccy basis swaps with foreign NZD Kauri bond issuers - we pay the basis to borrow Kiwi in this swap so the counterparty gets sub Libor USD financing. Offshore lenders of USD via xccy basis swap are in receipt of the basis because these swaps trade in negative territory in times of stress against Euro, Yen, STG dollar borrowers.

The other issue is that NZD deposits can be sent from a local bank, to outside the domestic regulation, I.e the offshore Kiwi market.

That is not my understanding-

Bank money stays within the respective banking system of the currency of denomination. (This is also true for foreign

currency accounts or mortgages offered by banks: in these cases, respective balances are recorded in accounts with overseas correspondent

banks.) Link

Eurodollar market for example is not under fed jurisdiction, no offshore markets have regulation by the domestic authorities. I’m not sure if they access ESAS etc (id say they definitely do)

And back to the original point, a bank run can occur just as at any time in the past. Your definition of money staying in the system somewhere doesn’t change the fact that the term structure of a banks liability can and will change, and that NZD deposits moving around between different banks (or even at the RB directly for example, or into a government bond, is exactly the same as if it were withdrawn in cash) is what causes bank runs

Money can and does “run” and the mechanics of it haven’t changed in electronic banking

Your argument that a bank run can not occur due to mechanics of transactions is a little ridiculous (sorry)

Edit: to answer your question on Fed swaps, the RB hasn’t engaged in fed swap program, and the issues of the xxcy basis were to measure pressures on nzd deposits, I wasn’t suggesting they were having trouble in that market that I’m aware of.

Eurodollar market for example is not under fed jurisdiction, no offshore markets have regulation by the domestic authorities

I agree, but it is not a coincidence that the active eurodollar banks are US registered primary dealers.

into a government bond, is exactly the same as if it were withdrawn in cash) is what causes bank runs

Bank depositors exchanging savings for government bonds allows the government to spend those swapped deposits into the system - deficit spending.

Yes, no shit, but the cash is still removed from the system on a new issue. The RB knows this and influences the level of settlement cash for upcoming issues or redemptions to smooth flows.

Your statements that bank runs can’t occur is ridiculous

Yes, no shit, but the cash is still removed from the system on a new issue

And placed where for the government to dispense into the system?

Are you saying that bank runs can’t occur?

“Everything comes from somewhere and everything goes somewhere.”

Is that a yes or a no? Or are you just going to quote someone else, because you don't have your own answer to things?

I asked you a question just above at 1.10pm - you have yet to answer.

That is so obvious I didn't even bother to answer. The distribution of the funds don't go back into term liabilities either.

You've yet to answer, you keep implying that there can be no bank run because money appears in another account.

I have started "unglueing" mine a couple of months ago. Everything that matures I am now moving somewhere else, mostly overseas, into the countries where there is a deposit guarantee. Mine is not an asset diversification, mostly a Country diversification. My only regret is that it is going to take me until end of the year to complete this process.

A "bank run"(in the sense of significant flight of funds from a bank) does not need any withdrawal of physical cash, at the end of the day it's just electronic balances on computers.

So, you're moving your money to the USA then?

That's where a Depositor Guarantee makes sense - where there are probably 10,000 banks that can't all be monitored 24/7.

But if you're moving your money to a country that has 4 TBTF banks, what's the point of any Guarantee?

If any of them ever had to pay out, what do you reckon you'd get and what would it buy - they sure wouldn't just hand over notes? (Besides, they would probably be the parent of 'our' banks anyway!)

Not the USA, also because I found it very difficult to do it there. Not such an open country as they claim to be. To Germany (definitely not the DB for sure, LOL), and Luxembourg, mostly, but not exclusively (Netherlands and even UK are in the portfolio too). Not to any TBTF banks, anyway. In any case, they are not parents of our banks, I can guarantee you 100%. The world is not just NZ, AU and USA.

And if things go wrong, I would definitely get more than what I would get in NZ with its OBR for sure.

Are you bearish on the NZD? Why does it have to be a bank deposit? Govt or kiwibonds will be more liquid and you wont be at the mercy of an overseas bank and government in a different timezone that you can't visit that wont receive any blow-back if it finds an opportunity to throw you under the bus.

The currency issue is a very good point indeed. Yes, I am quite bearish on the NZD, not necessarily in the very short term, but definitely in the medium term. Just my personal call, and I know perfectly well how extremely difficult it is to forecast currency movements.

Good point about Kiwibonds too: but I am already invested a bit in Kiwibonds, which I am not dropping for sure. I am also not bearish about the NZ stockmarket (excluding the financial and real estate sectors), which I actually think is less inflated than the Dow (again, a very personal call).

In my portfolio, I would like to keep something like 25% in accounts/term deposits.

I am not worried at all about the "overseas" or timezone factor. But of course, before investing in any such bank you have got to make your careful homework about the treatment of non-resident investments in the specific country - Cyprus as a bad example.

If you obtained a TIN the US should be fairly straight forward. They wont open an account without one.

Yes you are exactly right that is what stopped me in my tracks: the bloody ITIN (Individual Taxpayer Identification Number). I don't have one. Have you got any experience/ideas about how do that without one, even if it seems a pre-req ? Or more relaistically about how to get one ?

All the banks are secure, don't worry folks. Don't scare the horses....

Brian Fallow seems to believe in the loanable funds theory of money, where there is only an existing pool of money that everybody from governments to banks must go to find it.

He fails to understand that both governments and banks are creators of money.

My strategy at the moment is to not work. On purpose. To slowly use up my money so that when I am 65 I will have only a modest amount in the bank and kiwibonds. I see no need to keep earning when it is not necessary. Assets are liabilities in certain circumstances. But there is a need to have some amount sitting there for health emergencies. (Or health insurance if you prefer).

I don't need to go on any more cruises. NZ holidays (which include camping and sleeping in the car when my missus is not with me) are perfectly adequate...

I think you might well be the wisest of all of us. Seriously,

Uninterested,

Interesting approach. What age are you now? I retired fully at 57-now 75- and am now better off than I was then, though my income is lower It would never have occurred to me to use capital to fund my needs. I live comfortably on my income and if that falls, say as result of reduced dividends, then I will alter my consumption pattern accordingly.

What makes an asset a liability?

Assets can be liabilities, but liabilities can be assets as well. The latter, especially if your older and the banks wont lend to you. Maybe Im naive but I cant see how our dollar deposits will receive haircuts in the future. Successive governments have devalued the $NZ so much anyway, which is one of the main reasons why properties on average double in nominal value over 10 yrs and which is why you should leverage your assets to buy more.

Use public debt to reduce private debt, use taxation to reduce public debt and increase interest rates. Keeping taxes low is generally good because it makes them more effective when raised. They shouldn't attempt to keep interest rates low, they need to create more capital to leverage. Offset this with temporary 2 year reduction in GST. The new benefit tier should become permanent for 3 months every 2 years at the higher rate prevent wage deflation. Cut taxes at the end of the decade once there is a stable growing surplus.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.