The country's banks are reporting that both demand and availability for credit over the next six months are set to be sharply down, according to a survey conducted by the Reserve Bank. Costs will likely go up for some customers seen as more risky and lending conditions will be tightened by the banks.

Normally the RBNZ carries out its Credit Conditions Survey every six months, with the last one done in March 2020. But it decided, as a one-off, to conduct an interim survey to understand how domestic credit conditions have changed post-lockdown. The next one will be conducted as scheduled in September and then it will be back to doing the survey every six months.

The June Survey was completed in the last two weeks of June 2020 by 12 New Zealand-registered banks, including the big five. The period covers credit conditions observed over the first six months of 2020 and asks how banks expect them to evolve over the second half of the year. *The survey methodology is explained in the note from the RBNZ at the bottom of this article.

Generally the survey suggests that both demand and availability for credit will be down substantially over the next six months. Banks are likely to look at increased interest rate margins and tighter lending criteria.

There's been a lot of speculation on the immediate future of commercial property with many businesses finding staff have adapted to working at home, while businesses such as hotels are obviously really struggling.

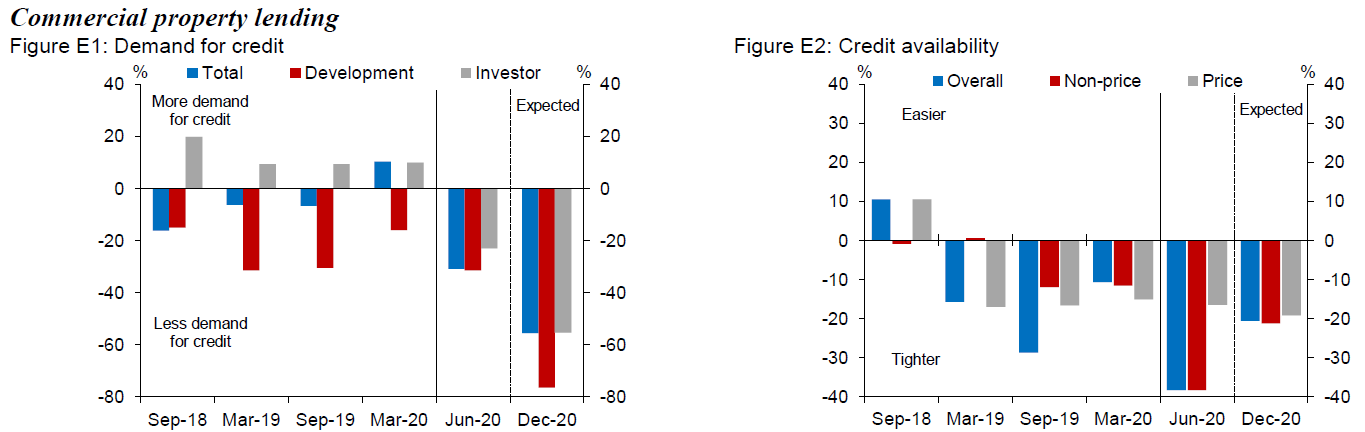

And based on the survey results, commercial property seems likely to come under a lot of scrutiny and pressure, with banks continuing the tightening on this sector that has been seen in the past three years or so.

In a release issued with the latest survey the RBNZ said several banks noted that they were downgrading their commercial property portfolios, "which has the effect of increasing capital utilisation and reducing their capacity for new lending".

And the survey shows a particularly big dive in the expectations both of loan demand and availability for commercial property in the next six months.

However, it should be stressed it is not all about commercial property at all. Credit conditions across the range of bank activities and lending are seen as being affected in the next six months.

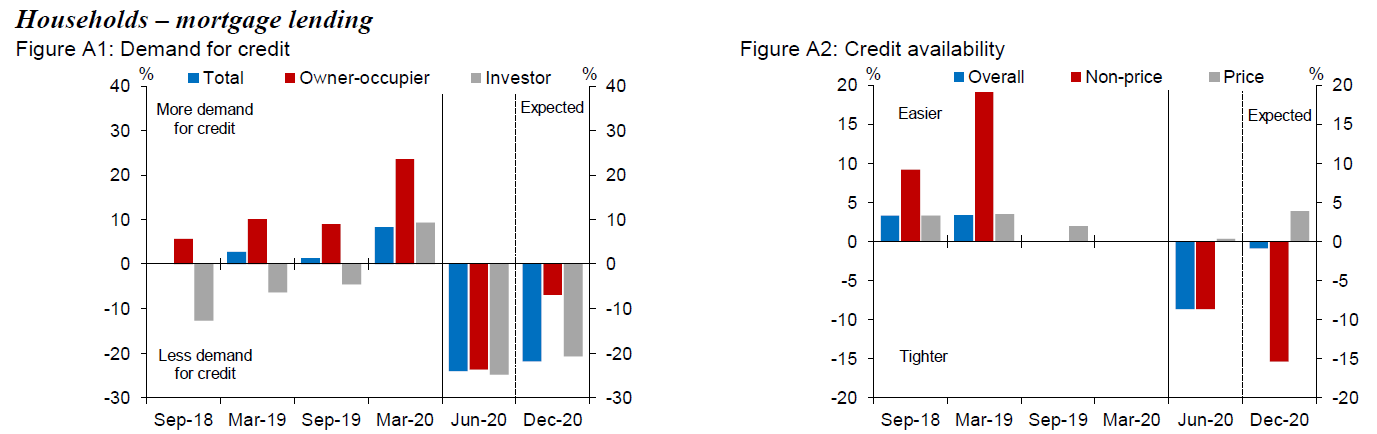

For example, both demand and availability for mortgages are expected to be down - although, interestingly, the banks indicate a likely greater availability of credit over the next six months for investors.

The RBNZ said bank submissions suggested that domestic credit developments post-lockdown have been predominantly demand-driven.

"Banks observed a decline in demand for credit over the first half of 2020," it said.

"Banks did experience an increase in demand for loans for working capital from SMEs and corporates to meet fixed expenses and sheep and beef farmers experiencing drought conditions.

"However, demand for credit for capital expenditure has fallen."

The RBNZ said that banks had noted low interest rates may support credit demand, however, uncertainty about the strength of future final demand is causing businesses to review their investment intentions.

"Banks reported that they have tightened several lending standards, particularly around serviceability requirements and interest rate margins across more risky sectors."

For some sectors (such as commercial property and dairy) this represented a continuation of trends that precede Covid-19.

"However, banks reported closely scrutinising new lending to sectors directly exposed to the Covid-19 shock, such as tourism, retail, accommodation and construction.

"Banks noted further tightening of lending standards is likely."

Mortgages

In the second half of 2020 banks anticipate a fall in demand for mortgage lending. Banks noted that lower interest rates may support demand. However, banks predict the economic impacts of Covid-19 will largely offset this.

"One bank noted they expect more distressed house sales as government financial assistance packages begin to roll off and the level of unemployment increases."

Banks also expect increased unemployment will dampen demand for consumer lending.

Banks reported that mortgage lending standards remain broadly unchanged.

"Whilst banks reported no material changes to their serviceability standards, they noted Covid-19 has resulted in greater income uncertainty given the likelihood of higher unemployment and fewer hours worked.

"Banks therefore expect to perform more thorough due diligence to assess income and job security, with higher haircuts applied to variable or ‘at risk’ income (for example, bonus, commission, boarder/flatmate rent, Airbnb income) included in servicing assessments.

"Banks expect this will impact credit available to applicants."

The RBNZ said most banks did not report a change in appetite for high-LVR lending despite the RBNZ's recent removal of restrictions for 12 months.

"One bank did note that high-LVR applicants would likely require very strong servicing positions and that property type and location would need to be less susceptible to price declines."

Commercial property

The RBNZ said banks were forecasting a significant slowdown over the latter half of the year for commercial property lending, particularly for development lending.

"Banks reported that uncertainty surrounding the depth and duration of the downturn has affected market confidence and slowed pre-sales in residential development projects, although demand is reportedly strong in the Auckland market.

"With regards to investment lending several banks reported that uncertainty around tenant covenants is slowing the market with a flight to quality evident in most sales transactions occurring."

Interest in retail, accommodation, and hospitality properties had softened.

Banks reported that the current economic environment means that they are generally more cautious and have reduced their appetite for both new development and investment lending.

"This represents a continuation of the trend towards tighter commercial property lending standards over the previous three years. Interest in new exposures to certain sectors (accommodation, tourism, retail) and regions (Queenstown) is very low."

One bank noted that higher LVR standards are being applied to retail, secondary office and hotel properties.

Banks noted that the greatest uncertainty concerned the impact of Covid-19 on commercial property values.

One bank reported that commercial property valuations are difficult to obtain as valuers are preferring to wait until market evidence exists post Covid-19.

"Several banks noted that more current valuations will be required and that valuation cycles would be increased.

"There has been a focus on increasing interest margins over last six months and banks expect this to continue for the next six months."

*RBNZ Note: The Credit Conditions Survey asks banks a range of qualitative questions about changes in conditions in the bank lending market. Banks provide separate responses for household, small and medium-sized enterprise (SME), corporate, commercial property and agricultural lending. The questions focus on observed changes in loan demand and credit availability over the previous six months and expected changes over the next six months. It also asks banks how their own lending standards have changed over the past six months. The Reserve Bank produces aggregate indicators from the survey. These indicators are loosely referred to as ‘net percentage changes’. Aggregate indicators are constructed by assigning each response a score between -100 and 100. A positive score indicates a bank observed (or expects) an increase in credit demand or availability, or a tightening of their own lending standards, and vice versa. Aggregate indicators are then constructed by weighting bank responses by their market share for the relevant sector.

56 Comments

This trend of reduced lending was emerging a few weeks ago , but everyone was pretending otherwise.

No one in their right mind should be making decisions involving credit commitments beyond 1 month, in my view .

We are in a recession with evidence of deflationary forces on the horizon ........... and overlaid with a pandemic wreaking havoc with economies , just for good measure .

Add to that we have China and America behaving like drunk youths outside a nightclub spoiling for a fight .

Never before in my 60-something years have I seen or heard of anything like it, and I get the sneaky feeling its not going to end well for many

My pick is that there is a perfect storm on its way , and its going to be brutal

You make me feel relatively optimistic in comparison to you Boatman! But, alas, I'm not that positive at all.

There, Boatman, we are in complete agreement.

Boatman,

I seldom agree with you, but I do this time. I found the view of Westpac economists that we would have a V shaped recovery quite bizarre.

"and it's going to be brutal". Sadly, I think that's probably right.

I was watching a documentary last night about Japanese prisoner of war camps and the brutal cruelty inflicted on Allied soldiers. I couldn't help but feel that the CCP is just as cruel and the same could happen to all of us in NZ and Australia if they invaded..... which they easily could.

Is that because they are both Asian countries?

Please don't take offence. I forgot that snowflakes look for something to be offended with in every aspect of life.

Ask yourself..... Had I said that I watched a program about the internment camps in Germany during the second world war and that they treated the Allied soldiers in a horrendous way, and that I feel the Russian FSB could be just as cruel if they invaded would you have said 'Is that because both are European'? I can tell you that you wouldn't, so get over yourself

Well then where did you get the "feeling" from? The only similarity I picked out of your comment was they're both Asian, hence the similarity.

Also, I see your bias towards allied forces. Atrocities are committed by all sides - all is fair in love and war.

Research the CCP and then you will find out where my "feeling" comes from.

Sounds like you post something racist, you get called out, so you call someone a snowflake when in reality you’re the one acting like a snowflake. Seems like a lot of racist views here are hidden under the aegis of China evil yet y’all trade with the USA, Saudi Arabia, the UK. Stop pretending your views are based on rational thought. I’m not buying it.

Yawn.

Foreign buyer: yes, I think I saw the same documentary, it was about the battle for Burma in WW2. But let's not get holier-than-thou........if you read a recent history of the battle of the Somme, called "Into the Breach", by British historian Hugh Sebag-Montifiore, you will find around page 460 from memory, that the NZders were the most brutal allied troops when they reached the German trenches: absolutely no quarter given....they shot surrendering Germans wholesale. (There was only a sole Canadian company that matched the NZders' general brutality.)

My grandfather, a particularly humane man, who was in that battle as a mortar bombardier, made mention in his diary of all the instances of any brutality committed by soldiers in his unit, originally the Auckland Mounted Rifles which was disbanded after Gallipoli. The day after he died my grandmother burn't the diary not wanting its contents to be made known to locals from the Auckland and South Auckland areas.

Brutality is not the exclusive possession of any one race; it is part of the human condition in situations of war. In fact, I watched a very good documentary by David Attenborough on chimpanzees the other night; the power struggles for dominance were brutal. But it must be remembered that chimpanzees are our cousins.

So true

Everything you said is true, however I personally am not scared of the NZ army invading NZ, but I do fear the CCP.

As I read it, the decreased availability is all about decreased appetite for lending by the banks. Currently, there is no lack of liquidity in the system preventing banks from lending if they had the appetite.

Consequently, the effective levers available to Government to influence the situation are limited.

Keith W

Think we might be entering the theoretical liquidity trap.

Yes, the banks looking after themselves before the country. But this may well bite, and hard, because if they're too tight they could cause property prices to fall sharply rather than flutter down, which means they will have shot themselves in the foot. In the meantime they will be looking for ways to protect their profits so look at savers charges going up, and if the RBNZ goes negative in the OCR then god help us all!

Actually I think the banks believe(d) their own b*%lshit. I think they really bought into the idea that the 'lending-into-existence-on-mortgages' paradigm had found its most fertile and and perfect environment in NZ and Australia. And perhaps the paradigm was the elixir.....until the devil (COVID-19) reared its ugly head and exposed just how fragile the model really is.

I love the expression 'anti-fragile' as coined by Taleb and have adopted into my own life and business as much as I can. Unfortunately, I beleive the economic model of NZ is not anti-fragile and scant regard has been paid to the idea. Quote: Anti-fragility goes beyond robustness; it means that something does not merely withstand a shock but actually improves because of it. And while not all debt is necessarily bad, Taleb identifies 'not getting into debt' as a key element in becoming anti-fragile.

Its a good concept eh? I was quite taken by that and watched a few interviews in which he talks about it.

The problem with anything like banks is that you have to buy into the culture and people work with herd mentality. He/she who has superior herd mentality gets promoted then has further influence on pushing that mentality onto others. And having witnessed banks involvement in previous credit bubbles, you realise that we're not likely going to learn from past mistakes as 'this time its different' as it always is.

The problem with anything like banks is that you have to buy into the culture and people work with herd mentality. He/she who has superior herd mentality gets promoted then has further influence on pushing that mentality onto others.

Taleb addresses this in 'The Black Swan' and 'Fooled by Randomness.' Quite prevalent in the trading world where people confuse luck for skill.

I agree with Taleb. I have always considered debt to be a last resort both privately and professionally, but the banks would have you believe otherwise. Look what they've done to farmers.

@Keith , Bankers are notoriously gun-shy when it gets a bit cloudy , taking the umbrella back when it starts to rain .

Its understandable , their entire training and credit -approval systems are about risk aversion .

Defaults are likely happening already

Can you imagine the losses or non-payment the Banks are carrying on commercial properties in places like Takapuna , which is basically a village of restaurants .

You can be sure that many of those tenants are taking massive strain right now , and simply cannot pay rents .

Some may optimistically try to trade through this mess , or use personal funds ( or home equity) to fund the business to stay afloat .

The harsh reality about a recession is that it generally lasts longer than you money does.

Its understandable , their entire training and credit -approval systems are about risk aversion

I disagree. On the surface, it's about 'risk minimization.' And by that I mean how they're perceived. The banks past behavior and actions have put them in the situation they're in now. Illustration of this: A bank customer might have high income streams and reliably paid the bank what they owe. But in reality, that same customer is living month to month with all income streams exhausted for outgoings. Now to what extent does the bank understand this and how is it built into their risk management models? I don't know but what I do know is that it's not a highly prioritized factor in the banks own assessment and assessment of their cutomers' ability to pay.

That's all coming home to roost now.

The world sharemarkets are totally disconnected to the real world

I see this morning that American banks have warned about huge loss provisions ahead and the situation will get worse

The virus is raging and the sharemarkets rise again

Talking to a friend the other day who said they are making really good money with their investments

I asked where their money was invested and the reply was Sharesis

Can’t go wrong they said

This seems to be a worldwide trend at the moment

Reminds me so much of just before the 87 crash,everybody was buying shares because thats how you made money

Overnight it all came crashing down,no more long lunches with a bottle of Boly, it was clients coming in crying because they had lost all their money

Many are going on a spending spree at the moment thinking we are fine in nz ,the economy will be back to normal soon

I don’t believe we have started seeing the worst ,it is yet to come and it won’t be nice

Yes many shares are now at least 20% over real valuation, but the worlds fund managers dont know where to put other peoples money.

To be fair, it's a tough spot. Everything appears overvalued and cash returns are nil -- indeed this is the point of the various policies: encourage you to spend by making the saving options unappealing.

keithwoodford,

I'd love to get your view on Regenerative farming. I have just read a piece on it in the NZ Geographic.I was surprised to read that NZ is the 4th highest user of mineral fertilisers in the world at 1777 kgs per hectare of arable land per annum. This compares with 68 kgs in Australia. Why the enormous discrepancy?

I have no farming background, but the regenerative approach looks very appealing from almost any perspective. What might the drawbacks be?

Im trialing it, i'll get back to you in twenty years and let you know how it went.

I found the article you referenced, linklater, and also found this added at the end:

"June 30, 2020: An FAO figure was found to be misleading and thus removed from the story. The FAO reports that New Zealand consumes 1777 kilograms of fertiliser per hectare of arable land per year, but this number seems not to take into account the fact that most fertiliser used in New Zealand is applied to permanent pasture, not arable land."

The article also rightly points out the high levels of carbon already present in most NZ farm soils, that most NZ pasture is already rotationally grazed by ruminants, and that the research showing regen. ag. dramatically increasing soil carbon levels took place using heavily degraded arable land.

Linklater01

It is a big topic. But as a starting point, and at a national level, if we were to stop using artificial fertilisers then we would need to recycle all human poos and wees from the cities back to the farms. The biggest requirement in NZ is for phosphorus.

KeithW

" both demand and availability for credit will be down substantially over the next six months." - What a surprise! But just 6 months?

" more distressed house sales as government financial assistance packages begin to roll off and the level of unemployment increases." - Another surprise!

Anyone with any sense loaded up with unapplied; fully drawn (and offset and no holding cost) credit some time back. Now is the time to patiently wait and look to apply it in due course. But not to asset speculation. That will become the pariah of investment, but to production. (That will also include the production of housing for accommodation, not speculation. Those who want to speculate from now on will be free to continue to do so, but they will have to do it with their own liquid capital - not debt)

and Gov't wanting to increase taxes with a shrinking economy is not possible without hurting the economy even more.

We'll keep that one under the hat untill after the election. At least Crusher will be able to point that out to the public and ask how they are going to address it.

Follow this......Maybe we will do the same...GST here on everything.....money can buy......But UK cheaper and drops Vat equiva-lent like a stone.

https://www.godsavethepoints.com/uk-vat-tax-drop-hospitality-2020/

"We know that markets can be complacent until a certain point and then they turn on a time. We are at this point in a benign phase supported by an enormous amount of central bank liquidity emanating from the primary reserve currencies, the euro area, the US Fed and to some extent the Bank of Japan and the Bank of England."

"But we must also recognize is that there are no free lunches. If there’s one statement you want to keep to pound into the head of every policy maker, it’s that there are no free lunches. If you borrow today, there is a presumption that it will be repaired at some point, so you are in a sense taking away resources from somebody else in the future."

"Now it may be a generation or two down the line will be on the hook for this...whether they can pass it on to their children is an open question...but you’re definitely taking away their ability to borrow by borrowing today."

https://www.zerohedge.com/markets/there-are-no-free-lunches-former-rese…

Sorry DGM but mass defaults or mortgagee sales etc will not be happening until Xmas at the earliest. Most people will still have a few months on their 6 month COVID deferrals and even then there is whisper on that being extended to a total of 10 months. Throw on top of that banks inability to just immediately sell a persons property when they default (probably need 90-120 days) we are looking at another 6 months glide time (see Falling with Style from Toy Story) before reality (see concrete) hits us.

And so it begins......

"One bank noted they expect more distressed house sales as government financial assistance packages begin to roll off and the level of unemployment increases."

At least some real news is starting to come out but I willing to bet they are calling for good times in another articial.

CGT review in UK to help pay back the massive debt caused by COVID-19. Jacinda must now do the same.

https://www.dailymail.co.uk/news/article-8523663/Rishi-Sunak-orders-cap…

CGT will not provide any tax income if asset prices fall. (also Jacinda has explicitly said "no CGT under her watch")

There's a new borrower in town with pristine assets seeking a buyer - why wouldn't banks seek to reduce risky exposure in favour of government liabilities, whether it be bonds or RBNZ reserves.?

Heard Jim Bolger on the radio today saying the world and New Zealand has to have a public debate about what to do about the massive amount of money that has been printed or created out of thin air

Do we follow traditional economics and raise taxes to repay the debt or do we just write it off

Interesting comment from ex prime minister but he is right how do we repay this huge debt

Do we we follow modern monetary policy and all just write our debt off

Writing it off is an urban myth.

Debt must either be paid off or written off. Many lenders have been playing " extend and pretend " but sooner rather than later they are going to have to face up to the reality that they will not be repaid. When this is acknowledged both the debtors and the creditors will be bankrupt. Until the world's economies are purged of this zombie debt we will not be able to move forward

In the case where recourse lending is in force lenders will come after the borrower's assets and future income. But not much hope for unsecured bank depositors. They risk everything for nothing and yet underwrite about ~90% of the banking system.

Correct me if im wrong, but In this case is the debt is lent between two government bodies, treasury and RBNZ, so the assets and liabilities cancel each other out and effectively dont need to be repaid? Can someone with better QE knowledge please explain

Millennial Woman,

In a narrow sense that is correct. But at that point the RBNZ has lost the chance to subsequently undertake any quantitative tightening and the State (Treasury and RBNZ) has financed its operations with created money which can not be recalled - except through fiscal policies of raising taxes . The likely outcome (after a lag) is inflation. Maybe even stagflation (i.e. inflation in a non growing economy). Right now, very few economists would argue against some level of QE as a way to reduce the forthcoming recession. And that QE has been happening big time with the RBNZ buying up the Treasury bonds. But it is somewhat like morphine - good for pain relief in a crisis, but definitely not a desirable long-term medicine. At some time you have to get off it! In the long term there is no free lunch.

KeithW

Thank you Keith

Which is why many are calling stagflation is inbound - which i you have a lot of debt may not be a great place to be (misery index level = high).

High unemployment, rising inflation.

The RBNZ's QE operations buy issued government liabilities from banks and credit those banks with central bank reserves. In effect banks have swapped a fixed rate government security for a floating rate government security. Reserves have to be held until the RBNZ sells purchased bonds back to the market or they are redeemed at maturity by government. At maturity the RBNZ is in receipt of the redemption proceeds and passes them to the banks which cancels the previous reserve liability the RBNZ extended to the banks in exchange for the bond purchases. The only cancelled liabilities are the coupon payments from government to the RBNZ held bonds. Nonetheless, the latter has to pay out OCR to fund banks' reserve claims.

Audaxes,

Surely the banks can withdraw those reserves whenever they wish as long as they stay above the minimum total prudential reserves as set by regulations?

KeithW

Hi Audaxes, I'm just trying to decipher what you wrote.

How are central bank reserves considered a floating rate security from the banks point of view? What incentives commercial banks swap assets in the first place, ie govt bonds for reserves? At the end of the process why are the commercial banks obligated to give the reserves back to the RBNZ, and what do they get in return for those assets? (Re assets/ liabilities perhaps it's easier to refer to everything from the commercial bank's point of view)

Keep hearing an ad on the radio for enable me run by hannah mcqueen. Says you can gain financial independence using the power of "leverage"..

About now we will begin to see whether Mr Robertson & Mr Orr have the banks on their side or not. It's going to be a very interesting final half to the year.

Banks are buying fixed coupon government debt and swapping it for RBNZ floating rate (OCR) debt. That's a big bank favour for the government while OCR remains at 25 bps or below.

Sounds like commercial property is going to be split up into the do's & the don't's. Some city retail will be tough going while the burb's might be onto a winner. Tourism & accommodation will probably be half the price in March 2021 than it was in March 2020. Great. We can all afford to discover Aotearoa again. In fact, life in the big cities may not quite be the same again for a while as working from home gathers pace aided by the great digital transformation's fifth generation, now upon us. It's already happening in the big towns like London, New York, Chicago & LA, albeit with the street riots not helping things much. I'm thinking this is probably a step change folks, whether we like it or not. Remember to breathe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.