By Gareth Vaughan

Stress testing of the country's major banks, kicked-off by the Reserve Bank in March as the COVID-19 pandemic took hold, shows New Zealand banks have a good level of resilience but aren't invincible, the Reserve Bank's Head of Financial System Policy and Analysis Toby Fiennes says.

The Reserve Bank modelled two hypothetical scenarios, both significantly worse than its current COVID-19 related fallout expectations.

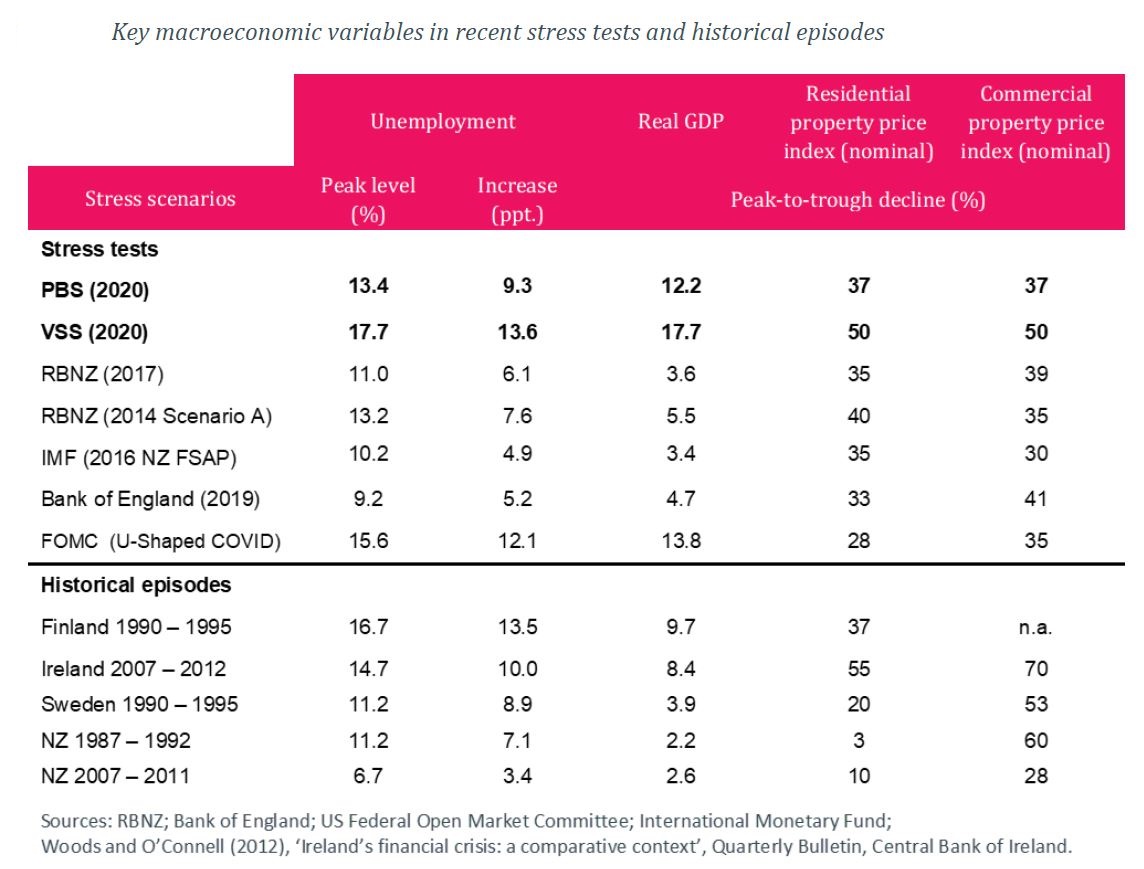

The first was described as a pessimistic baseline scenario. The Reserve Bank characterises this as a one-in-50 to one-in-75 year event with unemployment rising to 13.4% and a 37% fall in property prices. In this all banks maintained capital ratios above regulatory minimums.

The second scenario was a very severe scenario, categorised as a one-in-200-year event. In this scenario the unemployment rate reaches 17.7% and house prices fall 50%.The Reserve Bank's own actual current forecasts are for a 5.8% drop in Gross Domestic Product this year, an unemployment peak of 8.1%, and a 9% fall in property prices. The very severe scenario is akin to what Ireland experienced in the Global Financial Crisis, Reserve Bank Manager of Financial Systems Analysis Chris Bloor says. He describes the overall stress test results as "relatively reassuring."

"The overall conclusion from the Reserve Bank’s modelling is that banks could draw on their existing capital buffers and continue lending to support lending in the economy during a downturn of the severity of the pessimistic baseline scenario. However, in the more severe scenario, banks' capital fell below the regulatory minimums and would require significant mitigating actions including capital injections to continue lending. This reinforces the need for strong capital buffers to provide resilience against severe but unlikely events," the Reserve Bank says.

"If a banking crisis were to occur on top of an existing economic crisis, the economy's ability to recover would be seriously compromised, and outcomes would become significantly worse," the Reserve Bank says.

The Reserve Bank’s modelling didn't include strategic actions or capital injections banks may undertake to mitigate severe downturns. The test results are released on an industry-wide, rather than an individual bank, basis.

Fiennes says the stress test results will help inform Reserve Bank decisions on when to start implementing planned bank regulatory capital increases, currently set for implementation over seven years from next July, and any changes to current dividend restrictions. Decisions on these two issues are expected either before or when the Reserve Bank issues its next Financial Stability Report in late November. The Reserve Bank's proposed increases to bank capital requirements, finalised last year, are touted as preparing banks for a one-in-200-year scenario.

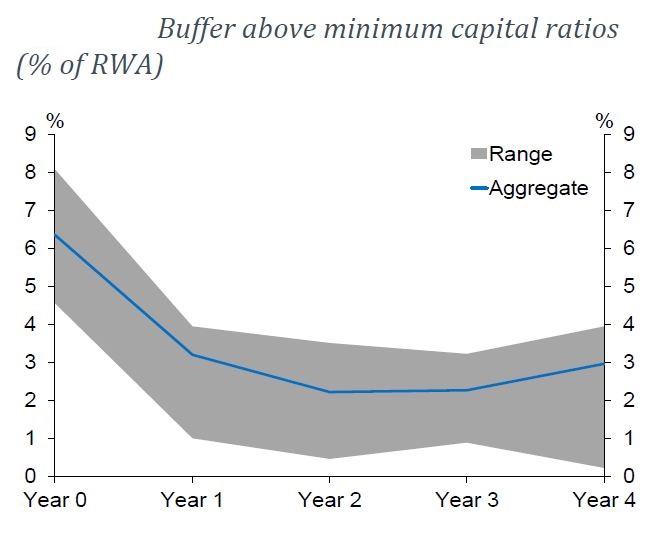

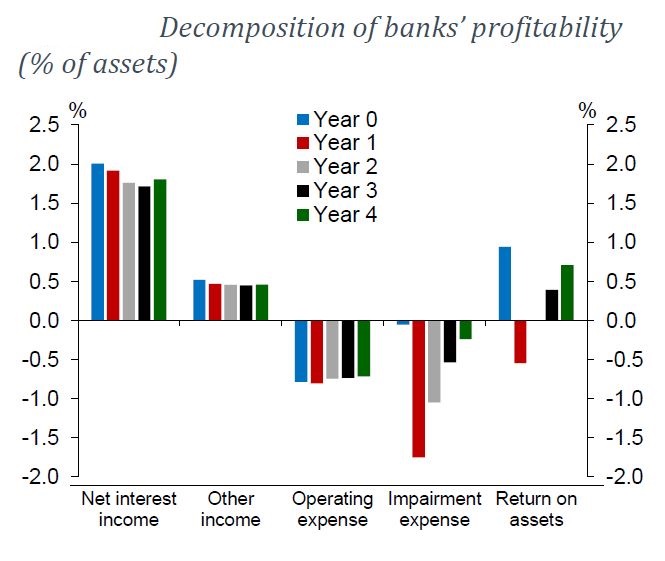

"The Reserve Bank’s modelling of the pessimistic baseline scenario resulted in a 57% reduction in the aggregate capital buffer by the end of year two. This translates to a reduction in aggregate Common Equity Tier 1 capital ratio from 11.4% of risk-weighted assets to a trough of 7.7%. The decline in capital is mainly due to high loan impairment expense, which is partially offset by strong underlying earnings," the Reserve Bank says.

Also under the pessimistic baseline scenario all banks remain above regulatory capital minimums despite some coming close to the minimum total capital ratio, while continuing to meet credit demand from customers.

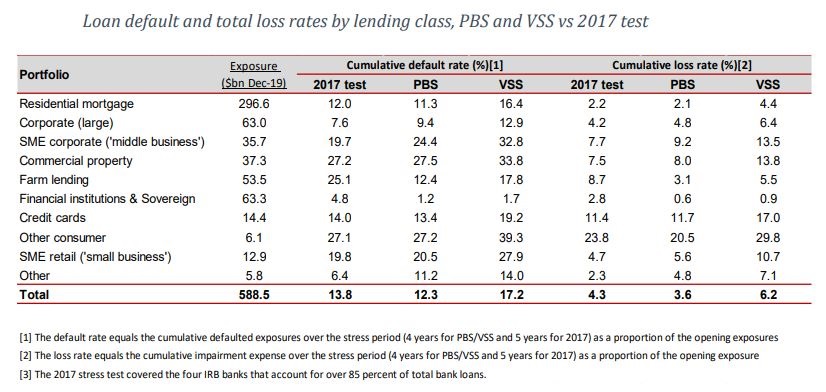

"The Reserve Bank’s modelling of the very severe scenario resulted in aggregate capital falling below regulatory minimums. The deficit in total capital reached $7 billion in year three. The very severe scenario illustrates that there are limits to the shocks banks would be able to withstand at their current capital positions. Provision of credit would come under considerable strain in this scenario, and capital injections would be necessary to ensure banks’ survival."

Under the very severe scenario both aggregate tier one and total capital fall below the regulatory minimum requirements.

Banks' current minimum regulatory capital requirements are a Common Equity Tier 1 capital ratio of at least 4.5% of risk weighted exposures, a Tier 1 capital ratio of at least 6%, Total Capital ratio of at least 8%, and a buffer ratio of at least 2.5%. You can see more on bank capital, including the Reserve Bank's proposed increases, here.

Nine banks stress tested

Nine banks holding 92% of total New Zealand bank loans - ANZ, ASB, BNZ, Westpac, Kiwibank TSB, SBS Bank, Heartland Bark and The Co-operative Bank - featured in the stress tests. The five biggest - ANZ, ASB, BNZ, Westpac and Kiwibank - submitted results based on their own modelling and provided mitigating actions.

"Overall the capital outcomes of the bank modelled submissions were similar to the desktop exercise in the pessimistic baseline scenario, but less severe in the very severe scenario. The submissions provided a challenge to the Reserve Bank’s desktop model and some of our assumptions were revised as a result," the Reserve Bank says.

The Reserve Bank launched the stress tests in March to determine the resilience of banks and the financial system to the risks posed by COVID-19. Stress testing is a tool used by bank regulators to give them a forward looking view of risks to the financial system. It involves modelling the impact of hypothetical severe shocks on financial institutions in a sort of health check of a bank's balance sheet to see if they hold enough capital to support lending during stressed times.

"Banks have increased their capital buffers significantly since the Global Financial Crisis. The stress test period began at December 2019, with the nine banks in the desktop stress test having an aggregate capital buffer of $19 billion above regulatory minimums, to absorb losses during times of stress. This stress test is one gauge of whether the current buffer is sufficient," the Reserve Bark says.

Being prepared for the unexpected

The two scenarios tested by the Reserve Bank drew on elements of scenarios developed by Treasury in April combined with different degrees of global economic stress.

“The onset of the COVID-19 pandemic provides a stark reminder to us all of the importance of being prepared for the unexpected, especially when you are a systemically important bank at the core of New Zealand’s financial system. The more capital a bank holds, the better it can weather economic storms and meet customer needs during tough times like now," Reserve Bank Deputy Governor Geoff Bascand says.

“Our stress test assesses the impact of significant, hypothetical, economic downturns on the profitability and capital of the largest banks in New Zealand. The results show us that banks can, and should, draw on their capital buffers to continue meeting customers’ needs during very challenging economic times."

“Even though these scenarios are severe, they are not unprecedented internationally, and the economic costs of such bank failures are significant. There is a limit to the comfort these stress tests provide, given that they are only simulated. In particular, the user knows how the stress ends and can act rationally. This is not the case in real time. The more bank capital there is, the less the banks and the New Zealand economy are exposed to the risks of decision making under uncertainty,” Bascand says.

Considering more severe ‘black swan’ events in stress test scenarios

The Reserve Bank says the onset of the COVID-19 pandemic has emphasised to both banks and regulators the importance of considering more severe ‘black swan’ events in stress test scenarios. Speaking to interest.co.nz in May Bascand said in previous bank stress testing, dating back to 2009, the Reserve Bank hadn't modelled a pandemic-type scenario.

"They tended to be more epidemic or foot in mouth type scenarios really rather than full blown pandemic. But we've had SARS in the past and we've had thoughts about these things. But this is a real live one," Bascand said in May.

The two charts below relate to the Reserve Bank's pessimistic baseline scenario.

Here's the Reserve Bank's conclusion for its pessimistic baseline scenario (PBS):

The Reserve Bank’s overall assessment of the PBS is that the New Zealand banking system can absorb such a downturn and continue lending to support the economy. All banks maintain their capital ratios above regulatory minimums. Banks will have much lower capital levels at the end of the scenario and will require time to rebuild buffers. Banks may consider applying timely mitigating actions, not modelled in the desktop, to lessen this task.

And here's its conclusion for the very severe scenario (VSS):

The Reserve Bank’s overall assessment in the VSS is that the banking system would come under pressure to stay above regulatory minimum capital requirements. Significant mitigating actions, including raising new capital, would be necessary for banks to avoid breaching regulatory minimums under this scenario.

A RBNZ Bulletin article on the stress testing is here, a summary here, and data here.

28 Comments

"The very severe scenario is akin to what Ireland experienced in the Global Financial Crisis."

So not 200 years ago then? Not even 20. How does 'a once in 200 years scenario' take into account; a Global Great Depression; 2 World Wars and the removal of the Gold Standard and its replacement with the fiat regime we have today? Where's the possible 90% fall in property prices scenario? You know, like the one 130 years ago ( in Dunedin here? Certainly Melbourne in Australia); Tokyo 30 years ago, or isn't that possible today?

But still, nothing to worry about.....

(What do we think the Bank of Ireland's Stress Test would have revealed in 2005? Something similar, or else they would have shored their banks up more than they did. Modelling is no more than a "What if?" calculation and "if" can be many things - most of them totally unexpected.)

What do we think the Bank of Ireland's Stress Test would have revealed in 2005?

Nothing threatening at all. In fact, it would have been glowing because the bank assets (mortgage debt) was as solid as a rock. I take the RBNZ's analysis with a grain of salt. All it tells me is that the stress tests show the extent to which the banks meet their capital req'ments. That's not to say that it's not BAU, but to suggest that banks can carry on as in the past (continutation of the status quo) seems 'subjectively' unbelievable to me.

Yes it doesn't make sense because in the article below they more or less say that without their extraordinary intervention, banks would have failed. So why even bother beating around the bush with capital ratios and more importantly why even bother with a private banking sector any longer when its clear that central banks just step in and clean up the mess when it happens. They may as well just be the lenders themselves and we can just live in a communist state - which is the rule book they're applying to what is labelled a 'free market'.

https://www.stuff.co.nz/business/122796046/house-prices-could-halve-in-…

Perfectly said, Independent Observer. I wholeheartedly agree.

Especially with the latest RBNZ's intention to start funding retail banks directly at OCR, we might as well now remove the bullshit, stop pretending that we still are in a normal market environment and just honestly go the full way and nationalise the entire banking system, so we can finally savour the "joys" of living in a particular type of a pseudo-Communist economy (with the minor difference though that, rather than having the burden of a minority of privileged, parasitic apparatchiks, we would have the burden of a privileged, unproductive minority of landlords).

House prices could halve if we have unemployment at levels witnessed in the US - will unemployment rise if/when covid subsidies end?

https://www.stuff.co.nz/business/122796046/house-prices-could-halve-in-…

Fortunate that tax payers are keeping the housing ponzi and our banks solvent (for now) - but how long do we use socialism (or could you even say that central banks are a communist regime now?) to keep our housing bubble inflated - or should we just let the free market be free?

And why did property price fall 90% 130 years ago? Because the free money - gold dug out of the ground everywhere in those days - came to an end.

What do we think is going to happen when today's free money also comes to an end - which it will. It's just a matter of when and how bad things will be when it does.

It's a nice thought. However, think central banks have proven over this period that free markets are not/will never be free

Too many of a certain age and influence have debt that they cannot pay under their own steam, therefore prices must be socially supported via wealth distribution.

Any idea what the rent level projections were on scenario 2 ? This will drive defaults in the investment class, not price reductions per se.

Doesnt this all suggest banks have enough capital already?

OK, they need to replenish the capital position after a 1 in 200 year event... but they do survive it.

Seems like the RBNZ are in a flap about the banks needing more capital, but the results here would suggest otherwise.

Clearly not because without extraordinary intervention (fiscal and monetary), it looks as though they would have failed:

https://www.stuff.co.nz/business/122796046/house-prices-could-halve-in-…

I'm struggling to understand why we even have a private banking sector any longer when the cental bank will take on any risk when necessary.

I'm struggling to understand why we even have a private banking sector any longer when the cental bank will take on any risk when necessary.

Duh, without private banks how would billions of dollars of our earnings be expatriated to Australia every year?!!

Yes my bad....

Exactly. If a one-in-a-200-year event is not enough to even bother the banks, why does the RBNZ need to influence their behavior? It's almost like the central bankers are communicating that all is fine under their guidance and overview. That's a bit ripe. Even Alan Greenspan admitted he was wrong and not infallible.

Steve Keen said stress tests are bogus. It sounds like when an engineer does a stress test on a bridge then it's safe to say the bridge is safe.

But banking stress tests do not take into account different shocks and crisis unrelated.

Hmmmm....engineers take stress testing seriously and are working with physics, not something as ephemeral as banking and human behavior.

That's the point keen was making..

My view and I could be wrong. I think that 30-40 years ago we lost jobs and incomes started to fall, Margaret Thatcher's time and we replaced the wages with debt, I never had a credit card till the 80's all this debt is new.

What the system cannot take is risk or recession, so we get all this jargon which we all know isn't true but we just go on anyway, like before because what can we do? it's Adam Curtis and his Hypernormalisation.

Adam Curtis interviewed by Russell Brand who is being a bit of a dick but still worth a listen on your way home.

Adam Curtis interviewed by Russell Brand. No thanks. I'd rather listen to Adam Curtis' work. There's plenty of it.

ANZ have net tangible equity of $10b, a housing book of $77b and $45b of other loans (business, personal etc). they would have to be insolvent in a severe scenario house price fall scenario, which is why houses are going up.

Aren’t they insolvent right now? That is, take away the fiscal and monetary intervention, I’d argue that our banking sector is an oligopoly of zombie companies - but that is just a reflection of many households I.e. their customers.

No, of course the're not insolvent. Directors face jail time for trading insolvent and I'm pretty sure JK wouldnt risk that.

Operating in a ‘free market’ I doubt they’re solvent. But that just sums up the insanity of our modern economic model. JK would be one of the last people I’d personally trust - would only do so with a stab proof vest (mostly to protect ones back!)

"They tended to be more epidemic or foot in mouth type scenarios really rather than full blown pandemic. But we've had SARS in the past and we've had thoughts about these things. But this is a real live one," Bascand said in May."

Seriously, did he actually say foot in mouth. Does fit the theme rather well.

Without having read a dot of the article.... can someone tell me if in their stress testing they factored in the high likelihood that the Bank will not only be ‘stressed’ by lil-old NZ but the same event/s that caused the stress would affect Australia and others (see GFC, COVID-19)

Would the RBNZ ever come out and say "Gosh the banks are looking like they're about to tip over"?

No, never. They ALWAYS say the banks are strong etc. Here and in Aussie. Which they did in 2008. And they lied. Turned out later on that 2 of our big 5 banks had borrowed money from the US Fed to stay afloat.

The media were asked by the RBA and Australian government to keep schtum about the real situation - i.e that the banks were struggling. And they complied.

Sounds like BS I know, but look at this: https://www.smh.com.au/business/nab-westpac-tapped-into-us-feds-emergen…

Aren't the Banks TBTF ? Why do this all these numbes, graphs, tests etc matter ?

The Reserve Bank tested 2 scenarios, the PBS (Pessimistic Base Scenario) & the VSS ( Very Severe Scenario). Both scenarios assumed that the global pandemic will be mitigated by the end of Year 2.

The PBS resulted in peak unemployment of 13.4%, house prices falling 37% & banks surviving.

The VSS resulted in peak unemployment of 17.7%, house price declining 50% & banks needing a bailout.

I am surprised that the worst scenario is assumed to be only over a 2 year period.

In my opinion it is likely that Covid-19 is endemic & in the worst case scenario it could easily last several years.

Further significant outbreaks of Covid-19 & other disasters occurring at the same time should also be considered.

This latter scenario is far more likely to be a more realistic worst case scenario if you are considering a 200 year timeframe.

It the worst case scenario it should also be assumed that a vaccine cannot be successfully developed.

It also amazes me how officials from Treasury have assumed that there will be no resurgence of Covid-19 in NZ. In its latest forecast Treasury has assumed that Alert Level 1 restrictions are assumed to apply from 1 Oct 2020 until 31 Dec 2021 & then all borders are open by 1 Jan 2022.

The world is in a global pandemic that has not peaked yet, so NZ is likely to get several more outbreaks of Covid-19 over the next few years.

Why do many of our economists underestimate the long lasting nature of Covid-19?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.