By Gareth Vaughan

Reserve Bank deputy governor Geoff Bascand suggests at least some bank depositors might want to put their money to use elsewhere.

Speaking to interest.co.nz after the Reserve Bank issued its latest Financial Stability Report on Wednesday Bascand, who is also general manager of financial stability, told interest.co.nz it's possible deposit rates could drop to zero. This is against the backdrop of the COVID-19 crisis and the Official Cash Rate (OCR) at just 0.25%.

"We don't really anticipate negative deposit rates," Bascand said.

He said negative wholesale or interbank deposit rates are possible, but for retail depositors the Reserve Bank is "expecting them to be floored by zero." ANZ, the country's biggest bank, now has all its advertised deposit rates - except for its five-year rate - below 2%. The five-year rate is 2%. (All banks' advertised term deposit rates from one to nine months are here, and here for one to five year terms).

"Deposit rates have been declining and that's part of what we have to do in a monetary policy sense to reduce the cost of funds to banks so that they can reduce the cost to borrowers. And I guess it also encourages savers to look at other areas to divert those funds," said Bascand.

"It reduces the cost of equity if they shift their funds from a deposit into an equity instrument, it pushes up those prices and reduces that cost in a different way to the equity funders. They could put it into other assets... so hopefully seeing that saving used closer to supporting the economy."

Asked whether he was encouraging savers to put deposit money to use elsewhere, Bascand said this was a choice savers have to consider.

"What we've said for quite some time is we expect interest rates to be very low for quite a period of time. There's not just a short dip and we suddenly see interest rates go up. We think in the circumstances it'll be quite a while for real growth to pick up, let alone inflation to pick up. There'll be quite a lot of surplus capacity in the economy, unemployment, other resources not fully utilised, capital that could be sitting a bit idle."

"It takes a while for any likelihood really of interest rates to rise. So if you're a saver you've got to say 'well, do I just accept that?' You've always got to mix up the safety element, how much I want certainty of my savings being there, which is why you might keep it in a term deposit or a bank, versus how much I need income from it or a higher return. And I might get a higher return somewhere else. They're going to have to make those portfolio choices," Bascand said.

In its latest Monetary Policy Statement on May 13 the Reserve Bank nearly doubled its quantitative easing programme to $60 billion, and kept the door open to the possibility of a negative OCR.

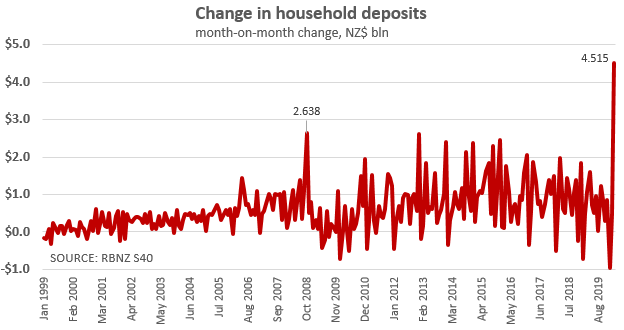

March saw the highest month-on-month gain ever in household deposit growth of more than $4.5 billion, according to Reserve Bank data, as COVID-19 fears gripped the world and the Government launched its wage subsidy scheme. The previous record high was $2.6 billion in October 2008 as Global Financial Crisis fears held sway. (See chart at the foot of this article).

No rush to implement deposit insurance

Whilst the Government is proposing the introduction of a deposit insurance scheme through the review of the Reserve Bank of New Zealand Act, full implementation isn't scheduled until 2023. Asked whether this could be brought forward, Bascand noted because it would require legislation it's ultimately a decision for the Government. Speaking to interest.co.nz in April Finance Minister Grant Robertson indicated no urgency in deploying a deposit insurance scheme.

"What we've indicated is we are working on being able to be ready to introduce legislation if the Government wish to do so," Bascand said. "...what we're doing is preparing advice on getting the Minister and Cabinet prepared if they wish to move at an earlier date."

Asked whether the Reserve Bank had advised the Government it should introduce deposit insurance before 2023, Bascand said there had been discussion of optionality and consultation with the banking industry.

"There are practical things like how would you pay the money out. The whole idea of the scheme is to support depositors if their institution failed. You want to get them the money so they can actually pay their bills. You've got to get ready to think what are the mechanisms for that? We don't have an institution that would run the scheme as yet. You've got to make sure you know what's covered by it, what form of savings are covered, etc. It's really just getting those options well developed for discussion with Cabinet," said Bascand.

A consultation paper issued in March by the Treasury and Reserve Bank team overseeing the Reserve Bank Act review proposed which products should be covered by the scheme.

In the video Bascand also talks about mortgage rates, banks' appetite to lend, cyber-attacks, loan deferrals and climate change.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

125 Comments

Good suggestion, since New Zealand has lots of residents who are originally from other countries, if deposit rate drops to zero, won't they just transfer their money to another country? What does this benefit our economy?

I totally agree......goodbye New Zealand.

I completely agree. This is exactly what I have been doing. You should have seen the type of negative spin and of spurious and ill-supported arguments that some have directed towards my choice. But this has only further confirmed that I am doing the best thing.

Investing money overseas will be achieving, for just slightly lower rates, the following:

- get my funds guaranteed by a decent deposit guarantee

- diversify away from NZ banks

- diversify away from the NZ$

I suggest that depositors seriously consider such options: in some cases, they are much easier to implement than many may think.

Note also that there are several such options; not just direct investments for the lucky who already have a foreign account (or can open one) in their country of choice, but also, for example, foreign cash ETF's (there is one widely available UK Cash Fund, for example), or investments in International Bond Trusts, if you are a conservative investor).

One thing is for sure: I am not going to subsidize the NZ housing Ponzi scheme (which is going to end pretty badly anyway) through my depositor money for a pittance return and no security.

Everybody's circumstances are different, of course, but this is definitely my personal course of action.

What he really wanted to say was ‘could everyone please swap any savings you have to a deposit on a house and FFS please start borrowing shit loads again because thIs house of cards is looking very wobbly’

Very true indeed.

What is the solution to excessive debt ? More debt.

What is the solution to a housing bubble ? Inflate the bubble more.

What is the solution to low productivity and lack of investment in the real economy ? Kill domestic savings in NZ and divert what is left to asset bubbles.

Perfectly idiotic. Like giving more alcohol to an alcoholic who is feeling depressed.

Its one of those situations where its fine until its not.

"We need to mortgage our children and grandchildren's future so we can keep partying right now!"

There's one downside to foreign bank deposits: Bank accounts or loans in foreign currency are subject to the financial arrangement rules. This means any foreign exchange gains are taxable. Many people don't realise they have an obligation to report these gains to Inland Revenue.

Conversely forex losses should be claimable. I think its on unrealised gains as well

The UK is in a mess , my accounts there pay next to nothing .

Indeed. I've done precisely that. May as well have it somewhere with deposit guarantee. My international friends over here have done the same.

Have you seen interest on deposits in other countries. This is not an NZ only problem. Every country is punishing or about to the savers and trying to drive down borrowing costs and encourage spending. The whole world is in s deflation due to Covid. We are in a much better situation than others. Believe me rates for savers going down all over the world.

I have funds in other countries and a big regret as very difficult to get back and complex tax issues.

RBNZ Suggestions......

To reignite housing market

Buy and build houses to stimulate the economy.

Westpac said that they expect further loss of construction jobs next year due to fewer houses being built. It dose sound like a good time to build and flick as there will less on the market. Small builds 2 bed, FHB'ers and down sizing boomers the market to hit. Exactally what I've been waiting for.

Who are you flicking too ? Zero immigration and people losing jobs, sounds like a mugs game to me.

What I usually do is subdivide a section with a existing house. Renovate the first and rent out / sell and build another house on the newly created section.

2 bedrooms for older people down sizing are hard to get due to a lot more people in that market. They have the money from the sale of their larger house.

There will always be demand, it is just where you aim your build. An expected 30% decline in new builds also adds to demand.

I thought he was hinting more at bitcoin.

Yep exactally what he said. Throw a hundred thousand on a loan and buy Bitcoin and hope that there are no cyber attacks.

I think it was more to TD holders i.e. "If you think TD rates are too low there is always bitcoin...". Basically, if you are sitting on a big wad of cash stop whinging and put your money somewhere else if you don't like what the banks are offering. I agree the focus should be on those people who are struggling to survive and pay bills rather on investment opportunities for the rich.

The good old trickle down. Lol

It's direct relief in the form of lower debt servicing costs.

Hold on TTP has just been on another article telling people that house prices are going up further because we can go a long way into negative interest rates. This says we don't even expect deposits to go negative!

Some Property Brokers will stop at nothing!

A lot of articles I've been reading are indicating stagflation in the coming years - everyone but the central banks....

Agreed

It does seem like the most likely outcome.

Naill Fergusson, the economic historian, points out that China hardy improved the average peasant wage for almost 500 years. So stagnation can last for very very long periods of time.

For most of human history there was very little "growth". Whatever there was, it was marginal, took ages and was regularly wiped out and reset by war, collapse or natural disasters (sometimes all three). The more I study the history of economies, they more I wonder if it is not the last few hundred years of "growth" that is the anomaly.

:) off course the past few hundred years are the absolute exception ninja. The only other comparable points are 1) sedentary farming replacing hunter gathering 2) urbanization and rise of cities. But even these two revolutionary turning points in modern human history pale compared to the scientific and technological revolution of the past 300-400 years.

The world discusses GDP and "growth" like its a natural phenomenon though. They uncouple it from population growth, which is undoubtedly a huge factor in the fast pace of economic growth since the Industrial Revolution. The population growth has slowed, it will cease entirely within the next few decades. Those of us who are at least that far away from retirement, need to stop assuming that the future of investment can be based on the yield assumptions of the past. I mean, sure, there are still developing countries that we can descend upon like a plague of yield hungry investors to try and see is through a bit longer, but ultimately, growth is probably going to be MIA as population plateaus over the next few decades. I'm just reading "Capital in the 21st century", Thomas Piketty which is a historical deep dive into growth and capital yield in prior centuries and he suggests that there was usually no inflation at all for most of history. Unless there was a supply/demand issue everyone expected that a standard loaf of bread would cost the same in 1400 and is did in 1700 (barring the war/famine related supply demand issues).

As a thought experiment, why do we need growth? If there is negligible inflation?

There was a huge population growth in Europe in the 16th or 17th century, something crazy like %50 in 50 or 100 years, while since I read about it. Lots of depressions too.

Lucky they then found the USA as an export destination and the UK had the commonwealth. My money is on Musk and Mars

Andrewj, very much so and that was despite the plagues that came every 20 years or so! Apparently the boom happened after the Tudor explorations brought back new crops from far flung places (potatoes yum!) so there were diversified food yields which could sustain higher populations.

No small irony in that point. So the introduction of the common spud spurred unprecedented population growth. Ireland for instance. Then the blight. Then the famine. Then great human destitution and wastage. Could we argue that the spurring of the creation of a monumental global debt mountain, has the same characteristics, parallels and likely fate. As a contributor pointed out here not so long ago, society can no longer afford itself. Just thinking. South Seas Bubble comes to mind too.

If I have a comfortable material life and my neighbour has half of what I have (materially) then we could;

(a) Take a quarter of my 'stuff' and gift it to my neighbour, or

(b) Create more stuff and give it my neighbour. Assuming he wants more material crap of course.

Now if I create more material wealth of any kind the economist will set a dollar value on my creation, add it to everybody else's creations and it might pop up on some bureaucrats monitor as 'an increase in GDP'. Ultimately neither my neighbour or myself cares much about bureaucrats or their statistics. Some frenchman somewhere might even write a book about it.

In the 1920's this evil process (GDP) installed electricity in people's homes and created new distribution systems that made goods cheaper for everyone.

In the 1930's homes started to get refrigerators until by the 1970's even families below the 'poverty' line had one. By the end of the 1990's almost every household had a microwave oven.

We could talk about cars, computers, heat pumps and Gore-Tex etc. But in the end I just want to let people earn and spend what ever they can from free and voluntary transactions with other people and not be very concerned about what bureaucrats have to say about it.

Ralph, interesting comment. Although human ingenuity isn't evil and it isn't GDP either. We may as well be called Homo Technologicus, because adapting to our environment with technology is our most notable feature as a species.

If we strip it down even further all we really need is material comfort and health. Technology and human ingenuity helps massively with that. GDP stats and economists? not so much.

There seems a lot of trash talking of GDP these days, but to me it seems like a meaningless red herring and the wrong conversation to have.

I'm not trash talking GDP (although it's an imperfect measure surely?) i'm asking if building economies on expectations of perpetual growth is flawed? Especially if growth over the last few centuries has been majorly fuelled by demographics.

What is the right conversation to have if GDP is the red herring?

It was a general observation and not an accusation, apologies if it read that way.

I agree GDP is an imperfect measure, but I suspect no one really expected it to be perfect and it was never meant to carry the weight of an idealogical debate about growth and finite resources. I feel like it is just an unlucky economic statistic caught in the cross fire.

If remove GDP as a red herring what is left (for me) is people. Which shaped the reply I made earlier.

The right conversation is how do we continue to provide opportunity for people to lift themselves out of poverty. Justified by the observations that;

1. Poverty has many poor empirical outcomes, and

2. The solution to poverty is wealth creation.

In that view, the needs of people are placed higher than any theoretical debates about the nature of resources management.

Couldn't you also say Ralph that "the solution to poverty is resource allocation"?

Growth has hugely reduced poverty, but we're running into problems:

1) Growth seems to be harder and harder to maintain without unstable levels of debt (largely because we've picked most of the low hanging fruit, esp in the industrialised world)

2) Growth may actually be leading to a net reduction in true wealth. Hence the critiques of GDP. We're measuring wealth with an accounting technique which largely ignores natural capital and services - i.e. the planet. If I'm catching fish at an unsustainable rate, then in theory I'm creating wealth year after year. And then I starve.

The needs of the people ARE resources: food, water, shelter, air. The bottom of Maslow's hierarchy. Hence resource management and, to some degree or another, wealth redistribution.

I think the word growth is now so associated with this kind of Malthusian apocalyptic ideology that it is a problem to use.

I don't agree with the Malthusian view, he was wrong when he published (meaning his predictions did not in fact take place) and similar such predictions have been proven wrong on every occasion it has been used since. I see nothing to think 'this time is different' will be any more different to all the other times 'this time was different'. I would have thought the scale of empirical failures (every time someone has used his theory to predict disaster it has not in fact taken place) that it would give people pause to wonder why that was the state of affairs. But anyway, some points to consider on that front:

1. We live in the greatest age of material plenty the world has ever seen. Food is so plentiful in the world it is very hard now to make living from farming. Think about that in simple supply and demand terms. There is very little hard evidence for resource exhaustion. Peak oil graphs seemed to fit, until they didn't.

2. The earth is part of a universe and is absolutely not a closed system. Various forms of energy and even material stuff enters and leaves the planet every single day and yet Malthusians continue to talk about closed systems as if the earth is the functional equivalent of a 'petrie dish'.

3. One large reason these predictions fail so consistently is; such arguments are theoretical in nature and are made with an assumption. Sometimes that assumption is stated but often it is not. The assumption is, 'all other things being equal'. A Malthusian logic statement might look something like this:

(a) If we keep using horses at the current rate, and

(b) if horses keep eating grass at the observed rate, and

(c) horse poo keeps coming out at the observed rate, therefore

England will run out of arable land in the year XYZ and London will be buried in between 1 to 1.5 metres of horse poo by the year XYZ.

The problem being, of course, that things did not remain equal, things changed. We did not, in fact, keep using horses at the current rates, all things did not remain equal and the theory failed once again.

One way of wealth creation is the willingness of people to work at anything. Too many people on benefits can not make the country more prosperous.

Tacit admission from RBNZ that its QE program is not being spent on stimulating economic activity.

Pushing on a string.

Ask yourself, Geoff, "Why would deposit interest rates go to zero?"

My answer would be, "Because Central banks have removed the risk component from capital markets, and the probability of loss of 'investing elsewhere' is hugely increased, because you and your fellow 'experts', have stopped The Market from doing its job and qualifying risk"

So rather than 'investing elsewhere' depositors are going to refrain from investing ANYWHERE, as the probability of capital loss is unquantifiable.

Drop interest rates at your risk, Geoff!

It's going to flatten the NZ economy and do unimaginable harm to this and future generations of your fellow citizens.

yep, it might be a zero interest rate policy but if the cpi is -5% im a happy saver. Interest rates should be set by the market.

For many years the 5 yr term deposit rates were about 9% and very slowly dropping. At that time inflation was steady at around 2% so the returns from term deposits were huge. Those days are long gone. NZ is falling into line with all the major countries. Money printing etc. We are no different.

Your desired cpi of -5% is a bit optimistic in my view.

I thought I was being conservative, looking at you Japan

Completely agree bw. Geoff is a smart guy and this is his wheelhouse, so he must know this also. Question becomes, why are they doing this when the consequences are obvious to them?

We already know. TINA (Or so 'they' believe).

We should not be in this situation, but we are. So the only question that needs an answer isn't "What do we do when deposit % rates are 0%?" but what happens after that, and what do we do to be prepared for the disaster-in-waiting.

We've all got a different answer to that, and given a large number of options from (1) Buy another renter! to (2) Take the cash out of the bank and bury it in the back garden, to (3) Put your finger in your ears and hope it all goes away to (4) ...any one of many more choices.

There is only going to be ONE correct option, and we all have to figure out what that is for each of us.

(PS: I have no issue with 0% deposit rates as such, but they should come with an economy that also has 0% foreseeable risk; an economy at 100% productive capacity that needs to encourage the further uses of idle capital. And that is the very opposite to what we have about us today. Interest rates should be set by the commercial and retail market, not the Central banks, but the last 40 odd years have given them the false impression that they can control any and all economies if they use a big enough stick. That may work on the way up ( to suppress runaway asset prices etc) but it is not guaranteed to work on the way down - no matter how big the stick. In fact, the bigger the stick is, the bigger the chance of killing whatever it is that is being struck)

Bond markets generally set interest rates - central banks follow.

Central bankers today aren’t trying to peg interest rates to a low level, the bond market is doing that for them and they are actually trying to make the case that the resulting low interest rates are somehow good. And because it really isn’t, they keep doing the same things over and over and over. No radical rethinking of the process deep down to the fundamental intellectual level. Link

Do you think this is happening with NZ govt bonds? It looks to me we are reliant on QE to keep them <1%. We are getting QE (announcements) right after high (above retail rate) bond tenders.

you need to ask 'why would interest rates be 0%' why can people not afford the interest bill? I think it's because they are being forced to follow the economy down. It's a disaster for NZ.

It's like the woman who sat in a bath full of glue

I wonder if gold will make some kind of come back?

Or is bitcoin the new gold?

Why not both?

There won't be enough PM's to go arround if it goes nuts, so yeah Bitcoin could go with it.

Kezza check this out FWIW:

Jim Rickards: His Gold Price Prediction Explained.

https://youtu.be/HpqJ-sFScxA

Yeah I follow him.

The riots have started, the population of the US is on a knife's edge, it won't take much to set them off.

It is hard to get physical gold and silver at present and you pay a good amount on top of spot.

If the big money boys jump into PM's you won't be able get it at all.

“the probability of capital loss is unquantifiable” well now, cannot recall a better summation of a quandary for many a long time. It reminds me somewhat of the good Doctor Cullen bemoaning ordinary NZr’s passion for investing in property rather than stocks/equities, and then a few days later his protege Cunliffe announced with unbridled glee, the take down of Telecom. Thus the collapse of a blue chip cornerstone investment that cost ordinary NZrs millions. And so can we dare ask in today’s scenario, is property still not the preferred investment and for very good reason?

Depends what our employment rate is going to be and wage reductions.

They could put it into other assets... so hopefully seeing that saving used closer to supporting the economy

I'm sure he's not referring to Bitcoin. Buying a house would support the economy, but it might not be in your own self interest.

Move to USA.....and become a Trump Supporter... Buy a House out right. Why work.. They chuck money around the entire World.

https://www.calculatedriskblog.com/2020/05/new-home-prices.html?utm_sou…)

"Put their money to use elsewhere"... RBNZ recommends housing.

"The Reserve Bank of New Zealand released its bi-annual Financial Stability Report (FSR), which stated that the nation faces its sharpest economic contraction in 160 years."

Maintaining the flow of credit to sound borrowers will contribute to the long-term stability of the banking system by reducing borrower defaults and preventing large falls in property prices and other asset values. Maintaining credit will also play a strong role in supporting the upcoming economic recovery.

https://www.rbnz.govt.nz/financial-stability/financial-stability-report…

Awesome. We just need those "sound borrowers" then eh? Who decides who they are?

In the real world, low interest rates brought with it talk of of a weak, faltering economy. Not anymore.

The rbnz knows all the answers, and decides to lower interest rates, then turns around and says,"wow, interest rates are low, fancy that."

"Well, we don't know what people will do with their deposits, if they're not happy with no interest, maybe they'll put them into something else?"

Deposit insurance? "Well, you know figuring out how to completely rig the economy, so it looks healthy, ( while it's practically dead on its feet), that's been tiring, and a deposit insurance, well, that's really very complex, far beyond our capabilities, probably need to spend big bucks on consultants to figure that one"

The rbnz needs mental health assistance, on one hand they believe they are in complete control, on the other "well, maybe people will spend they're hard earnt savings on helping us prop up this synthetic economy we're working on".

What a load of bull.

Perhaps people will have the sense to take their deposits out of the system altogether, that would be a vote for a decentralised banking, and a return of individual sovereignty.

It's pretty obvious that the boys on the terrace get their instructions from the boys in the hood, oops, fed.

Pretty sure he means KiwiSaver, or other managed/self managed equity and bond portfolios. Diversify the risk away, exposure to international markets. For the average person, rental property is a veil of tears, commercial property a minefield. Bitcoin? Ho ho, ****ing ho. Gold? If the worst comes to the worst, you always make bullets and fishing sinkers out of it.

Well said Pietro. Rental houses only pay if you have capital gain and a commercial building without a tenant and eating it's head off with rates and insurance is a significant liability.

"Deposit rates have been declining and that's part of what we have to do in a monetary policy sense to reduce the cost of funds to banks so that they can reduce the cost to borrowers. And I guess it also encourages savers to look at other areas to divert those funds," said Bascand.

Not at all, every bank created asset (loan) is in need of a corresponding liability (deposit) until said asset is extinguished by borrower liquidation. Furthermore:

Low retail interest rates aren't shifting balances out of this type of saving.

Mainly because those swapping savings for another investment vehicle find their way back via the vendor of said investment.

That's why the RBNZ considers retail deposits "sticky" in terms of CFR:

The CFR addresses their longer-term funding position by forcing them to hold a certain amount of more ‘sticky’ core funding, e.g., long-term wholesale debt with maturities of more than one year, or retail deposits.

I expect mortgage rates to drop too which could fire housing and commercial property prices.

If I had funds languishing like teenagers with their feet up I would quickly move them out into the field and put them to work.

These unelected crooks really are loathsome aren't they.

They push everyone into risky assets and suddenly its return of capital you have to worry about.

Funds, like people have to work for the master to make the master happy and comfortable.

"The whole idea of the scheme is to support depositors if their institution failed"

I thought the idea of the scheme was to stop a run on the banks that led to institutions failing in the first place. He then goes on to encourage people to take their savings elsewhere

"They could put it into other assets... so hopefully seeing that saving used closer to supporting the economy."

This is lying. Inflating assets do nothing to support the economy. Can the good deputy governor please walk that back? If savings and indeed credit creation are put into something PRODUCTIVE eg actualizing new technologies then we will support the economy, but just trying to find better returns through asset speculation is EXACTLY what is wrong with the situation and why we are here. It feels like there is a religion called central banking and they have only beliefs.

This unholy alliance of the RBNZ its disciples the merchant banks will be the ruin of us all.

Well put Rosenstein.

Furthermore, beyond swapping existing savings for assets, newly created credit needs to be directed to the productive sector by a change to the RWA capital allocation scheme to favour business, not residential property.

That would be amazing.

So well put, Rosenstein. It appears that the RBNZ has no f...ing idea of what the real economy is about.

The RBNZ are in crisis mode. The goal is to save the banks because if they go nothing else matters (at least as far as the RBNZ's mandate, the OCR certainly won't matter). If people stop stop borrowing to buy these assets and instead sell them and deposit the proceeds this will of course decrease the price the asset. If all these asset bubbles return to fundamentals at once the banks will fail, the internal models are not designed to cope with this. I can't see how in these economic conditions we could transition to anything without the banks failing when existing assets are revalued. Once they have failed we change what ever we like.

In NZ at least, soaring prices and asset speculation must have resulted in meaningful increase in supply of new houses, which would have been a productive economic activity, albeit short-term and unsustainable. Yet it failed to even do that as new houses were so expensive (or in undesired locations) that people were willing to pay more to buy (or rent) very old houses at staggering prices. Wooden houses after all are depreciating assets. This to me indicates that there are serious economic problems in NZ that will seriously handicap you if you want to produce anything, even things that crook bankers are willing to lend you to built.

After all lack of opportunity (or mad loss aversion) drives so many savers to simply leave their money in the bank as opposed to investing it in anything productive (as the return on those activities must be so abysmal and the risk of losing your money so high, that you have to leave it in a bank).

I mostly get your point except many people choose old wooden houses for reasons unrelated to the price of new houses. Also, many new homes are also made of wood.

Building water storage so that dry land can be used more productively to grow kiwifruit etc would be a Productive use of savings.

Just me or does anyone else think we might be coming to the end of the philosphy of central banks?

The whole system doesn't make any sense any more.

What do you think the clear alternative would be?

Whittle them down to regulatory body for the finance industry, retain the focus of financial system stability and drop the focus on inflation. Open up their decision making process, not just the reports we get afterwards. Provide some means for the public to remove governors from office. Interest rates to be set by the market, banks compete for deposits (foreign and domestic).

Remove the Reserve Bank Act> https://www.rbnz.govt.nz/about-us/our-legislation

The alternative is a decentralised banking system, otherwise known as "free banking". Scotland and Canada were 2 countries that had such a system into the early 1900's. All such things need research and consideration, and a more broadly informed number of the public doing likewise. Unfortunately, it's not an overnight phenomenon, simply becoming aware that alternatives have existed is a great start. They can exist again, blockchain goes a long way to making decentralised systems, (not just finance) a reality.

I just wonder if at some point enough of given populations will go, you know what, I'm sick of the central banks manipulating this funny money, I no longer want to operate using this fiat currency, $#@@ you government, we're doing our own thing. See ya. Try to make our new currency illegal (be it bitcoin or like) but there are too many of us now to control.

Just watching what is unfolding in the US riot wise and you think, gee whiz, it really wouldn't take much to tip over the whole system if people lose faith in it - I'm a law abiding citizen who has held the highest government security clearances in the past and even I'm left thinking, why do we do this if it isn't working for everyone and only some parts of society? How long will people put up with it?

Not for profit community banking a la Germany

I'd like to support a local credit union like Baywide but figure that my money is more at risk than in one of the big banks.

One can hope, but I don't see any mainstream criticism of their actions. Or indeed any criticism, aside from the comment section on this website.

dont think I will be following his advice,increasing risk from TDs to shares,increasing the bubble.I have already joined the hoarders and got a new freezer,they are selling fast.

The Soviets had a controlled economy where the quantity and prices of goods were dictated by a central authority. Today we laugh at them, because without price signals their markets failed to respond to gluts and shortages, resources were badly misallocated, the whole thing was a complete shocker. Doomed from the start. Yet today, we have a central authority who tells us how much money the economy needs, and what the interest rates for that money needs to be, and everyone thinks that's completely normal. The cognitive dissonance is astounding. Maybe in a hundred years they'll laugh at us for being so backward.

100% correct. This is the most cogent analysis I have read in a very long time. I could not have used better words.

From a centralized control perspective, for one thing we are even worse than the good old USSR: at least they did not try to keep a housing Ponzi scheme afloat at all costs, regardless of the immense cost to the economy and to society.

But we are like the USSR, insofar as mis-pricing is concerned. Especially regarding mis-pricing of risk, which has become utterly pathological and meaningless in current NZ financial markets.

Given the market intervention we've witnessed the last two downturns (GFC and now) we may as well just live under a communist construct. It just that we've decided to fix the prices of assets and that price is insane (unless you were born before 1975 then its fantastic right?)

Anyone else getting a bad feeling about all this?.

Investors hate uncertainty and I can not remember a more uncertain time than now. Every day brings more shocking revelations about the economic outlook and more importantly the responses to it. I am going to stay on the sidelines until I can see where its all going to end up.

You are doing what people will increasingly do. Which is what the RB doesn't want you to do, but you will do it anyway.

This is why the RB is useless. But they aren't any more useless than any other RB has been in history. It's just that they follow failed economic models which they try to fit reality into.

Anyone know if there is any economic theory which is actually useful for a depression/deflationary environment/stagflation/whatever we are going to get?

Yes - let it play out so the bad debt leaves the system.

We're trying to carry bad debt and its suffocating the life out of our economy (not just us but many countries).

The longer we do it, the more it will be a burden on us and its going to be very painful and for a longer time than it needs to be.

I think it all comes down to the delusional thinking that you can cheat the system and ideally avoid the economic cycle altogether by artificially creating debt, sustaining bad debt and pretending it does not exist, inflating asset prices, and/or by directly controlling the market levers in a manner reminiscent of the failed Communist experiment.

While it makes sense to try and flatten the curve a bit with counter-cyclical measures, the current extreme approach is complete madness and it can only, at best, kick the can a little longer, at the expense of making the problem ever more difficult to solve in the future. Let the housing Ponzi scheme implode, hopefully in a controlled manner, and it will be all the better for the economy in the longer term. Now, for the sake of keeping it afloat, the RBNZ is literally compromising the very structure of the economy.

Yes think we see this in a very similar light.

RBNZ mandate is supposed to create stability, but in reality they're promoting instability in the longer term to avoid it in the short term. And its creating all sorts of ugly distortions in our 'free markets'.

I think its going to get ugly this year. There will be a game of hot potato with the bad debt and politically, how long are we going to be willing to pay everyone's wages for? When those payment stops, it will be like a game of musical chairs and everyone (workers, tenants, landlords and banks) will be rushing to find seats and many wont.

I'd love to know where a safe higher return exists. He should have told the rest of us the secret.

I don't think there is. Bond markets are dead, for example, killed by Central Banks interventions.

Sharemarkets.... there are some good opportunities there, but not for the faint-hearted: in the current settings, they are not so different to gambling at the casino.

But there are options for safer albeit a bit lower returns. Just not in NZ though.

The RBNZ wants you to fall into the NZ housing Ponzi scheme: their unspoken mandate is to keep it afloat at all costs. This is their real message. They want you to believe that this is the safe, higher return option.

This is exactly how Ponzi schemes work - you constantly need new participants in order to avoid having the whole castle of cards tumbling down. And in order to achieve that, you need to make the offer more and more appealing (read: ever lower interest rates).

Now they want all with deposit to come out of their comfort and invest in high risk stocks and also housing, which too is high risk specially now. Many with deposits whom they want to bail out the economy are retired or about to retire people. Is it the right advice. It also indicates that RBNZ and government are running out of ideas as well as money.

People when young did not took risk and went for safe deposit and now when are or about to retire RBNZ wants them to come out and take risk....for what To support housing ponzi knowing that this time they will not be able to manipulate/support the ponzi.

This is the worst advice that any governor or anyone in authority can give to people who have played safe and have saved till now and now they are asking them to invest in high risk asset and most probably go negative. Worst advise. Better to seat on zero percent return at the moment instead of trying to venture out and take risk.

This shows how bad the situation is and will be as RBNZ is advising its senior citizen to move away their money from bank....may be they know what we do not know that in future chances of bank going burst is high so want many to move away their money from bank. As earlier his boss - Governor Orr was also talking about the possibility in worst scenario of bank defaulting.

Something is wrong some where.

I totally agree. Like in any Ponzi scheme deserving its name, the NZ housing bubble needs ever new participants. It is now the turn of the few savers who can't easily move their money overseas. You have to keep feeding the scheme, otherwise for its very nature it will implode. In order to attract new participants in the scheme, you have to make the offer ever more promising (ever lower interest rates). They are not counting on you for investing in real businesses or in the sharemarket, this is clear. They know that the real problem with business is accessing credit, flexibility with input costs (such as rent) and cashflow, not the 1% difference in interest rates. In reality they are counting on you to join whoever has already fallen into this housing scheme, in order to prevent its implosion, which they now know is a distinct possibility.

I agree fortunr - but what gives it ponzi characteristics in my view was people using equity in previous homes (that had appreciated in value) as deposits on additional homes. And you read some of the property investor sites on FB - some people on there have used that model to buy 5, 10, 15, 20 properties! That is great until something like our current economic conditions come along and people can't pay rents and prices start falling.

You are completely right, Independent Observer. This is very true. It is a Ponzi scheme in more than one dimension indeed.

By the way, this phenomenon also creates societal and economic distortions and problems that go well beyond the purely economic aspects. But some speculators will tell you (as they have told me) that they are almost like philanthropists, providing an indispensable service to society.

I don't blame them at all though, as they are simply making the best of the existing opportunities and environment.

I think it has almost become an 'ego' thing for many of them though. Most I talk to can't justify their personal requirement for the 3rd, 4th, 5th rental etc. They've got enough, but its almost like they are trying to cover some inadequacy they may have - some type of insecurity and they like to have the power and control over tenants or something. Sure I met some nice landlords, but I've meet a lot of real strange cats as well.

There was a property investor FB comment section the other night with some women with a couple of young children (she must have only been 30 or 40) and she was like 'So how many rental properties does everyone here want? I want twenty. I just like the number. That is my life goal is to turn my five rental properties into twenty because that sounds like a good number. How many does everyone else want?'

No shit, then about 30 people jumped on this and they all listed the number of rental properties they wanted to own. 5, 30, 50, 1000! Some of these people already own 5, 6, 7. Its completely bonkers.

As I say, I lived through the mortgage crisis in the US - we're cruising for a massive bruising and it could get very nasty indeed.

wow, your examples are really sobering.

I was taken aback by one commentator, in one thread, who demonstrated a total lack of interest in the issues created to the structure of the NZ economy and its financial health, and who made it clear that his only interest was in the next available property for sale with a supposedly good return. You are right, it has become almost dystopian.

You are not sitting on a zero return though. Thanks to their financial repression and theft via inflation targets they are picking away at your savings.

Exactly right. If you keep your deposits in a NZ bank account for zero gross interest, you lose say 2% pa of your investment value every 12 months.

- On top of this, you are taking a totally unpaid risk as an unsecured creditor with the bank, and with no deposit guarantee.

- On top of this, if the NZ dollar depreciated substantially, the value of your savings in international terms (ultimately translated into future domestic NZ inflation) depreciate further.

- On top of this, you are indirectly subsidizing the housing Ponzi scheme, further damaging the longer term prospects of the NZ economy .

The lower the rates, the more likely is the prospect that the traditional stickiness of NZ term deposits will come unglued. In a normal market, rates should have gone up, not down, in order to properly reflect increased risk. How many noticed, in April, that Fitch decreased by one notch the rating of all major NZ banks? (also putting all of them on negative outlook?).

Why would anybody, with these terms, keep significant investments in NZ TD's ??

100% correct.

I watched the RBNZ video stream yesterday as well as J Powells 60min video the other day - it looked apparent to me that central banks around the world are shitting their pants. In my view they are realising the economic/financial models they've been taught like the gospel and that have worked for them for decades now may not be true and could actually cause more destruction than good.

They're dropping rates but nobody wants to take on more debt. They fire up QE and asset prices go higher - then in the case of housing it means more debt that may not be serviced if we have high unemployment and low growth (stagflation).

Central banks (in my view) are stuck between a rock and a hard place.

Yeah they want me to take what's left of my savings and put it into a market that is distorted to all hell by their manipulation already.

Tough cookies when it all goes tits up.

These bankers are crooks and theives.

I'm almost looking at central banks as the enemy now...is this ok? Or should somebody lock me up immediately?

Glad to see some other people starting to get it. They are the enemy. Unelected, unaccountable crooks that steal wealth from the productive and hand it over to speculators, rentiers and asset holders.

The government already did lock you up.

The central banking system is designed to give more wealth to the wealthy. The missing piece of the jigsaw is that the fed is a private bank. The ponzi scheme, especially in housing and stocks, has been going on for a long time. It's simply reaching it's end game, and the deception is being seen by more and more. We have expectations that the system at the very least, is "our" system, and that at some level, we think they are trying to work it out

Yet, they were never working things out to be fair and balanced for all of us.

The interview Bascard gives is testimony that the rbnz has no intention of being responsible, of at least looking after people and their financial interests.

In my mind Bascard is trying to do one of two things, make himself look stupid, or the rest nz look stupid.

He is supposed to be at the centre of an organisation that takes money, and it's value to the individuals that use it, very seriously. Instead he merely seems to be laughing as he says "well, I guess with low interest, and no deposit insurance, individuals will have to put money to work somewhere else".

What a complete joke.

He knows that a majority of Nz'ers are up their eyeballs in debt, and he's speaking with complete hubris because he feels certain that he can get away with it.

He's not a economic critic, he's the deputy head of the rbnz.

If it were up to me, I would sack him tomorrow for dereliction of duty.

We don't need central banks, and we certainly don't need their permission to have a decentralised system.

I agree, the RBNZ has recently demonstrated to be utterly incompetent and in complete dereliction of their duties. They are not elected officials, and this is the result of their lack of accountability. Be sure that if the NZ financial system goes down the gurgle, none of them will be held accountable.

Wonder How come No experts or journalists are questioning the wisidom of the bosses in RBNZ.

In this uncertain time who advices the people who have saved to go out and speculate/invest.

Seriously..... Deputy Governor gets away with such advice.

Yes, the elderly relying on TD are not going to be getting the income they expected.

However, sadly potential FHB are also being continued to be screwed.

"They could put it (TD) into other assets... " From experience, property may likely be their go to option.

I have previously posted that speaking to a couple of investors; they are currently sitting, cashed up, watching and waiting. Although a 5% a yield is poor by historical standards, it is still a lot better than cash. With mortgage rates less than 3%, it is going to mean that their equity will be leveraged so taking a mortgage is an attraction.

Personally, along with other property data, I will be watching RBNZ monthly mortgage figures (C31) closely as to number of mortgages made to investors as an indication that those with a bit of knowledge and experience are starting to buy seeing the market bottoming out and providing the best opportunity.

Unfortunately, although falling mortgage rates, those FHB with less than 20% equity are going to be hit that extra 1% banks are applying and also considering job and income security more so in this high risk and uncertain environment.

The reality is that unfortunately, the home ownership rate for 25 to 35 olds - which has dropped from 65% in 1985 to 35% currently - is not going to get better but rather worse.

I keep hearing bleating (seemingly mainly renters) about how renters are going to be laid off and not able to afford rent. Renters; don't get too smug. Many on this site may not get the accommodation supplement and aren't considering its impact. Had an investor friend in HB lose a tenant (bought a house as expected) in the last few weeks; he had over 60 applicants, the vast majority on accommodation supplements and competition such that they were offering to pay above the asking rent knowing that the additional rent they were offering would be picked up by WINZ.

Yes, RBNZ is saying to those with cash - you need to think differently, conditions have changed and you need to adapt. No use bleating.

Likewise, young potential FHB are facing difficult conditions but are not getting better and you need to adapt.

Both groups need to do a Richie McCaw - conditions and circumstances are not great but how do we adapt.

Indeed, adapt, the path of least resistance is get the accommodation supplement and live on the benefit. We only have so much time on this earth, and trading it in for rigged tokens is stupid and pointless.

Why bother being a productive worker or fiscally responsible? They will take the value of your earnings and transfer them to asset holders. They will tax you to death and hand it out as accommodation supplement and super for your landlord.

They tell you that you must now gamble your money in their totally manipulated system. The only way to win is to not play their game.

Put what you have into Gold or Crypto, do the bare minimum, collect the benefit and keep your time.

True, we've recently been subsidising 300,000 rental properties. Quite bizarre welfare for property investors. People rant against beneficiaries while they are so themselves.

We (young people) do need to bleat.

These scumbags are leveraging our future to bail-out property investors.

It makes me ropeable.

What a scum bag.

Shamelessly drive elderly etc up the efficient frontier and not GAF about the fall-out (i.e. more speculation, moral hazard and further indebtedness for the young).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.