The Reserve Bank (RBNZ) is nearly doubling its quantitative easing programme, committing to buying up to another $27 billion of bonds over 12 months.

It will continue to buy New Zealand Government Bonds and Local Government Funding Agency Bonds, but is now adding NZ Government Inflation-Indexed Bonds to the mix.

This brings the value of the RBNZ’s Large Scale Asset Purchase (LSAP) programme up to $60 billion - in line with market expectations.

BNZ interest rate strategist, Nick Smyth, last week pointed out that if the RBNZ keeps buying New Zealand Government Bonds at the rate it’s going, it will have accumulated around $70 billion of these bonds by March 2021.

OCR to remain at 0.25% until 'early 2021'

The RBNZ’s Monetary Policy Committee (MPC) also opened the door slightly to the possibility of an Official Cash Rate (OCR) cut before March 2021. It on March 16 said it would keep the OCR at 0.25% for "at least 12 months".

However on Wednesday it “reaffirmed its forward guidance” that the OCR will remain at 0.25% until “early 2021”.

The MPC said it would "stand ready to deploy further tools as needed, should the need for stimulus continue to increase".

"Tools available include further reductions in the OCR; a term lending facility; and adding other asset classes, such as foreign assets, to the LSAP programme.

"The Committee noted that a negative OCR will become an option in future, although at present financial institutions are not yet operationally ready.

"The current goal of monetary policy tools is to reduce borrowing rates for New Zealanders, and further OCR reductions at this stage would not be effective in achieving that. Consequently, the Committee reaffirmed its forward guidance that the OCR will remain at 0.25 percent until early 2021.

"It was noted that discussions with financial institutions about preparing for a negative OCR are ongoing."

Deflation on the horizon

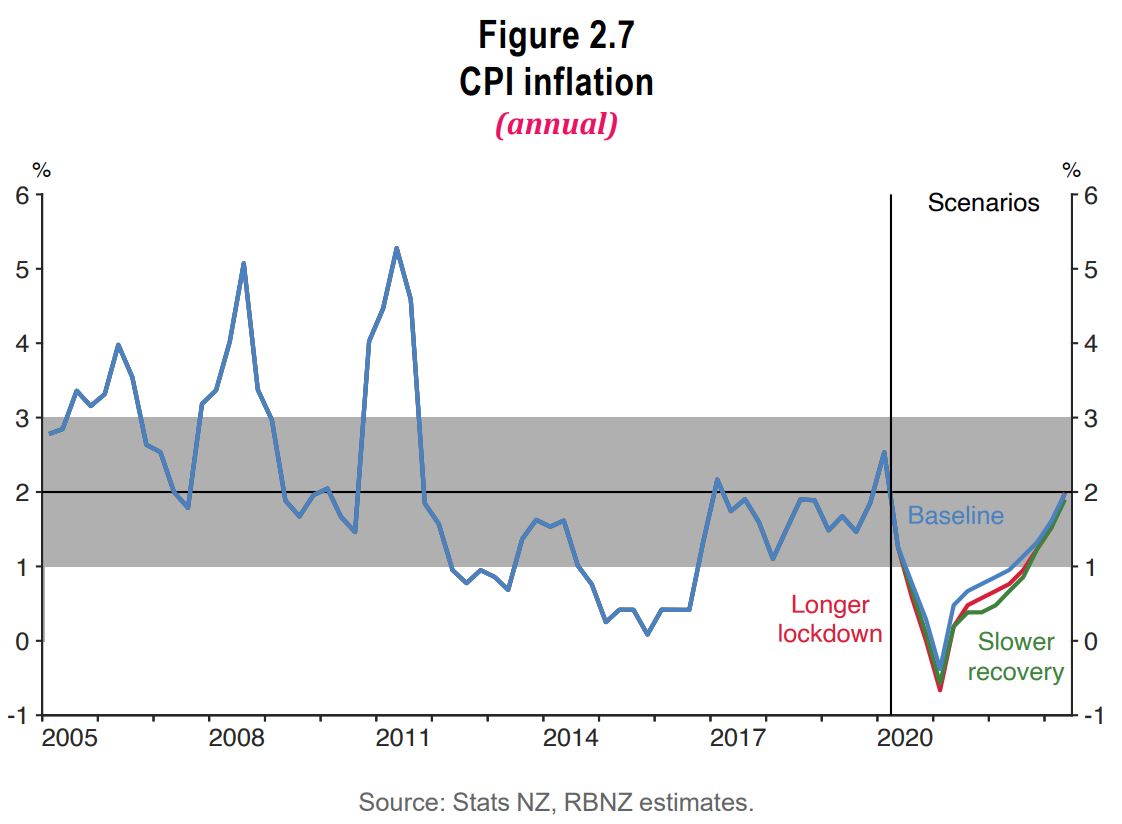

The MPC didn't include foreacasts in its statement - rather it included economic "scenarios".

Under its baseline scenario, it sees deflation occurring in the March 2021 quarter.

The MPC sees annual inflation getting progressively weaker, falling from 2.5% in the March 2020 quarter, to -0.4% by the March 2021 quarter. It only sees inflation recovering to 1% by the June 2022 quarter.

The MPC is tasked with keeping inflation between 1% and 3%.

The New Zealand dollar fell in response to the RBNZ's announcement to US60.3 cents from US60.8c.

See a copy of the MPC's quarterly Monetary Policy Statement here.

Here’s the MPC’s media statement:

The Monetary Policy Committee has agreed to significantly expand the Large Scale Asset Purchase (LSAP) programme potential to $60 billion, up from the previous $33 billion limit. The LSAP programme includes NZ Government Bonds, Local Government Funding Agency Bonds and, now, NZ Government Inflation-Indexed Bonds.

The global economic disruption caused by the COVID-19 pandemic is expected to persist and lead to lower economic growth, employment, and inflation both in New Zealand and abroad. Even if New Zealand successfully contains the spread of disease locally, reduced world activity will mean lower demand for many of New Zealand’s exports.

The Monetary Policy Committee is committed to achieving its employment and inflation objectives. The main support for the economy in this environment is appropriately being provided through increased fiscal spending. However, monetary policy will continue to provide significant support through keeping interest rates low for the foreseeable future.

The balance of economic risks remains to the downside. The expansion to the LSAP programme aims to continue to reduce the cost of borrowing quickly and sharply. This is preferable to delivering a smaller amount of stimulus now, only to risk later realising more should have been done.

We expect to see retail interest rates decline further as lower wholesale borrowing costs are passed through to retail customers. It remains in the best long-term interests of the banking sector to promptly maximise the effectiveness of our LSAP programme.

The Official Cash Rate (OCR) is being held at 0.25 percent in accordance with the guidance issued on 16 March. The Monetary Policy Committee is prepared to use additional monetary policy tools if and when needed, including reducing the OCR further, adding other types of assets to the LSAP programme, and providing fixed term loans to banks. The Committee’s decisions are guided by the Reserve Bank’s mandate and our decision making principles on the use of alternative monetary policy instruments.

Here's a summary of its meeting:

The Monetary Policy Committee noted that the economic situation has deteriorated since the previous policy meeting. The COVID-19 pandemic is affecting economic activity throughout the world. The unprecedented health crisis has led many countries to introduce measures to contain the spread of disease. In New Zealand, activity has fallen sharply as a result of the pandemic and containment measures. The sharp contraction in activity is expected to reduce inflation and employment below the Bank’s objectives for several years.

Members discussed the significant uncertainties surrounding the economic outlook. The pandemic and restrictions on the movement of people are uncharted territory for modern economic policy. Here, and overseas, there is uncertainty about the impact of containment measures on economic activity. Monetary policy is using tools which have not been deployed before in New Zealand, and their degree of success is something that will become evident over time.

To help understand the uncertainties, the Committee discussed several different scenarios for the economic outlook. Members agreed that the situation is too uncertain to allow any one scenario to be treated as a central projection. Three scenarios were discussed, including what could happen if extended containment measures are required. Members noted that the baseline scenario was the most optimistic of the three. All three scenarios involved a significant and unprecedented decline in economic activity and employment.

The Committee noted that more stimulus is needed to support a medium-term recovery in economic activity, employment, and inflation. Members noted that the main thing needed to support the economy is fiscal stimulus, given that fiscal policy is best placed to directly support households and businesses. The role of monetary policy is to support the economy by ensuring that interest rates remain low, which will complement the effects of fiscal measures.

Members discussed the fiscal assumptions in the economic scenarios. It was noted that the government has publicly announced that $52 billion has been made available for pandemic recovery packages. This figure is used as the core fiscal spending assumption in each scenario.

Members agreed that a ‘least regrets’ monetary policy approach is needed, delivering stimulus sooner rather than later, and thus minimising the risk that the stimulus delivered turns out not to be enough.

The Committee discussed the world economic situation. Members noted the global environment is volatile and uncertain. Some commodity prices are strong, but many of New Zealand’s trading partners are experiencing economic disruption and declining activity. Despite pockets of relative strength, conditions in trading partners will be a drag on domestic activity.

The Committee discussed the balance of risks around the baseline scenario and agreed that the risks are to the downside. Activity could be lower than expected as a result of containment measures having more severe economic effects than assumed. Another risk is that the pandemic itself lasts longer or has more severe effects on trading-partner economies than assumed. There is also uncertainty about the impact of monetary policy actions on the economy.

Members noted some chance that activity could be higher than expected. There is some possibility that trans-Tasman travel could restart earlier than assumed, or that a return to alert level 1 could happen sooner than expected. Either of these events would result in spending and employment recovering faster. Another possibility is that supply-chain disruption leads to relative price shifts for specific consumer products, keeping average inflation higher than expected. Members agreed that these possibilities were not material enough to shift the overall balance of risks around the baseline scenario.

The Committee noted evidence on the effects of the Large Scale Asset Purchase (LSAP) programme so far. Members were pleased to note that both wholesale and retail interest rates have fallen. The functioning of markets has also improved – a secondary goal of the LSAP programme. Further declines in retail interest rates would be needed to fully deliver the stimulus. The Committee noted that long-term interest rates in the government bond market are also sensitive to a number of factors outside the LSAP programme, including bond issuance and foreign bond yields.

The Committee discussed the secondary objectives of monetary policy. Some members expressed concern about financial stability due to the economic disruption of the pandemic. The Committee noted that the banking system is sound and markets are functioning satisfactorily. Members agreed that all policy areas – monetary, financial stability, and fiscal – are mutually reinforcing in this environment, all working to achieve complementary goals.

The Committee discussed the range of monetary policy options. Members noted that there are policy tools available that have not yet been used. The Committee agreed that it will stand ready to deploy further tools as needed, should the need for stimulus continue to increase. Tools available include further reductions in the OCR; a term lending facility; and adding other asset classes, such as foreign assets, to the LSAP programme.

The Committee noted that a negative Official Cash Rate (OCR) will become an option in future, although at present financial institutions are not yet operationally ready. The current goal of monetary policy tools is to reduce borrowing rates for New Zealanders, and further OCR reductions at this stage would not be effective in achieving that. Consequently, the Committee reaffirmed its forward guidance that the OCR will remain at 0.25 percent until early 2021. It was noted that discussions with financial institutions about preparing for a negative OCR are ongoing.

Members agreed that an expansion to the LSAP programme is the most effective way to deliver further stimulus at this time. The Committee noted advice that adding inflation-indexed government bonds (IIBs) to the LSAP would improve both market function and policy effectiveness. The Committee agreed to add IIBs to the LSAP.

The Committee discussed ways to measure how much stimulus is delivered by a given volume of LSAP. It was noted that while more purchases will deliver more stimulus, it is not easy to translate this directly to an OCR-equivalent measure. The Committee noted that the size of the LSAP programme needed to be sufficiently large to keep interest rates lower across the yield curve. Members agreed that the LSAP programme can be scaled as needed in future. Members noted that additional LSAP purchases are covered by an updated Crown indemnity, which represented a ceiling, not a target, for the total volume of LSAP.

The Committee reached a consensus to:

- expand the LSAP programme to purchase up to a maximum of $60b over the next 12 months;

- delegate to staff the composition and pace of purchases within the LSAP programme, across the eligible asset classes of NZ Government Bonds, NZ Government Inflation-Indexed Bonds, and Local Government Funding Agency bonds; and

- hold the OCR at 25 basis points.

131 Comments

This brings the value of the RBNZ’s Large Scale Asset Purchase programme up to $60 billion - in line with market expectations.

As BNZ noted this morning - "which also happens to be lower than its current annualised rate of $70bn"

The Committee noted evidence on the effects of the Large Scale Asset Purchase (LSAP) programme so far. Members were pleased to note that both wholesale and retail interest rates have fallen. The functioning of markets has also improved – a secondary goal of the LSAP programme. Further declines in retail interest rates would be needed to fully deliver the stimulus.

Interest rates can fall below zero and the credit status of ordinary New Zealanders will not rise to a level that makes any bank believe they can pay the principal back in the current environment.

The focus of monetary policy needs to move away from rewarding the small minority who can afford to buy RBNZ LSAP eligible securities on a rotation basis out of Treasury tenders into RBNZ ledgers repeatedly.

Make no mistake, this isn't monetary policy stimulus as no one benefits from 3 and 10 Year NZGB falling a few bp, this is purely funding the new issuance coming down the pipeline. And there you have it, debt monetisation.

Well described TK

Given that QE is deemed nothing more than an asset swap, surely Treasury is obliged to redeem the bonds purchased and held to maturity at the RBNZ so it can honour the banks' claims to reserves? It seems to me there is no new net injection of money into the economy. Initially, bank created investor savings were swapped into the government's bank account in exchange for government bonds. The government spends the proceeds into the economy - deficit spending - explained here.

If you're referring to the Banks Savings Guarantee insurance then they should have had that in place years ago, along with the rest of the Western world. Hard to believe that we still don't have this and lets hope that the banks don't collapse in the mean time.

$60 billion is only $12000 new debt for every man woman and child in the country...

Sigh.

But! For anyone who still thinks we're getting out of this without hiding, have another raed of the above.

It's going to get REALLY nasty, and if I had anything left to sell, I'd be selling it!

"Inflation is going to be lower". Sure is! It's going to start with a capital D, and no amount of 'stimulation' is going to head that off.

I reckon it starts with a S

Could be. The old 'Inflation is every thing you need; Deflation in everything you own.'

As I suggested, Sell!

You to late I guess. Who wants to buy.

Stagflation anyone?

Hi bw,

You write, "..... if I had anything left to sell, I'd be selling it!"

You could try selling your soul, if you haven't already done so.

Things may not turn as nasty as you wish......

Certainly, scaremongering is not helpful to any country battling a major biological crisis.

TTP

My soul is just fine!

It hasn't relied on scalping fellow citizens of their future income to sustain it.

The alternative would have been to sacrifice my integrity in the name of personal enrichment; which I could have done on a HUGE scale but chose to do otherwise. But then again, that's another story :)

Oh. And as for "what happens if things don't turn out to be as nasty as I expect?" Nothing! It just means I have to repay the cash Offset debt that I've accumulated; am running at $zero cost, and admit to myself "I was wrong!". How bad is that! Words. Many, if not most are going to lose more than words and opinions. They are now going to lose pretty much all they have. Have another read of this RBNZ statement and tell me you don 't think that Committee thinks the same!

Besides, I advocated 'taking precautions' way before Corvid19 hit. If it frightens some people now, they should have been frightened before. Now; is too late.

Comment of the day - well said.

Agreed. "Scalping..." comment of the day.

The alternative would have been to sacrifice my integrity in the name of personal enrichment

Hmmm..not sure what you're trying to suggest here. That somehow the lead-up to the current economic scenario is creating wealth? Don't be so sure about that.

?

I would be selling my soul if anybody is buying it.

Nothing wrong with selling soul during the crisis to feed my family.

Well said bw

"You could try selling your soul"

You'd be the expert on that. Maybe you can launch Soul Brokers after Property Brokers collapses in a screaming heap?

Why would you convert assets into money that will deflate also? People selling everything (and not buying anything) causes deflation. In the meantime, people with money buy from suckers who are selling and get rich later on. Story of the 20th century - most people took a hiding while the rich got richer.

If your timing is right, you sell at the peak then wait for asset prices to crash. Because you have plenty of cash now, you sweep up cheap assets at a fraction of the price. Thats my interpretation, anyway.

Just have to catch that falling knife.

Every reward comes with risk

You have a bit of a PR problem when it comes to giving insight to be fair

Maybe I have a future in politics?

possibly, but not branding!

Thanks guys, had a great chuckle.

The stock market is a falling knife, the property market is a slow moving train smash. Property will be falling for the next 12 months, plenty of time to find a bargain for anyone currently cashed up. Recovery will be so slow that even buying on the way up will not be a problem.

Right on point.

All that money will find a home and it ain’t going to be Bonds.

Prescient comment. Do you remain confident that NZ banks are a safe place to store cash (well, lend to, I suppose)?

60 billion is roughly equivalent to all the gold mined in the south island in the last 150 years. Should have just printed up the money then!

Point taken but ridiculous suggestion. :) I like Gold too .. It's been my second best performer this year, after Bitcoin of course.

Yep, I have gold and bitcoin too. Its funny because the collapse in the NZD this year seems to have done as much to boost their price as the fundamentals

I know right *thumbs up*, yet we both seem magnanimous about wanting the best for NZ, after all, I for one live here.

While Reserve Banks worldwide are Quantitative Easing (printing currency), holding quantitative hard/harding money like Bitcoin, Gold and Silver is a no-brainer - Supply & Demand 101.

Gold prices have been falling steadily. Is there any reason to expect they won't continue? After all, their worth is only slightly less dubious than fiat money. Real assets are better. After all, everyone needs a place to live

It's about percentage allocation, not either or. In a situation this volatile, diversification makes more sense than ever.

Gold can't be printed. And has also been a store of wealth for centuries. Historically, it beats fiat for stability.

"Gold prices have been falling steadily. "

Hmmm it seems you have turned your graph 90 degrees...

Jan 2019 - $1250 per ounce

Jan 2020 - $1500 per ounce

May 2020 - $1700 per ounce

Definitely falling steadily.

Gold, silver, BTH, ETH, XRP, BCH, LTC, XMR, BNB. We started mining 8 or so years ago back when network difficulty meant you could mine with USB kit.

Good on you, I'm just a purchaser - hosted a node once. I've never mined though, but remember the wild-wild-west of mining when dudes were spaying their over-heating-mining-rigs (graphics cards, no ASICs back then) with coolant and the like, lmfa0 .. dem were the days lol.

As if the mining industries we already had weren't sufficiently environmentally catastrophic, we had to invent an artificial one to consume additional physical resources (electricity) in an effort to produce a dubious store of value. Spectacularly mad, in hindsight.

You'd obviously mine where power is cheapest .. so a solar farm incapable of storing power or a hydro-dam producing too much electricity. That's why you don't see mining in New Zealand but do see solar mining in Australia.

Also Bitcoin is easy to send across boarders so Bitcoiners are actively funding and building solar generation capacity in Africa, etc, etc. Bitcoin uses as much energy as Christmas light usage over a year. Don't be a Grinch lol.

I think if you look up the resources used in mining you'll find that your christmas light estimate isn't even close to correct.

I was meaning all the Christmas lights in the world, used over the Christmas period (months) is equivalent to ALL the power used to mine Bitcoin annually - going by the Bitcoin hash-rate and average miner's power requirement .. as at appox 6 months ago.

I was surprised at how much people love fairy lights too.

I guess that could be true. But if so, it's more of a shocking fact about fairy lights than a reprieve for bitcoin's unnecessary power draw!

Some alternative cryptos use almost no energy at a price of less security. If you look at the total energy used by other sectors, including gold production, physical money production, the banking system - even the fashion industry, all use vastly more energy than bitcoin.

Bitcoin has the carbon footprint of a medium sized country, roughly speaking:

https://digiconomist.net/bitcoin-energy-consumption

Yes other industries use more. On the other hand, lots of people actually use physical money, the banking system, and the fashion industry. What fraction of the population do you reckon has ever made a bitcoin transaction? 0.1%?

I would be very much in favour of cryptocurrencies without the energy footprint.

Ripple, EOS, Nano, Tron, Stellar, Cardano and Ethereum (after its new upgrade) will all use proof of stake which is dramatically more energy efficient. (Actually, not Ripple but that one is not really a true crypto)

They may have to find the other half still buried

Tena koutou We are going to buy 80% of bonds on issue, Ka kite

Kiwi sharply lower, mission accomplished.

I knew this was coming today, but still forgot to buy my £GBP this morning. Quickly refreshed, and suddenly it'll cost me an extra $1k. Ouch.

That has been my life since 2016. GBP/NZD has been a rough ride and I have permanent bruises.

Yeah I know and try getting in touch with Customer Services with a UK bank at them moment, it's almost impossible. It looks like the UK and probably the rest of the world will ramp up their QE programs too so it's likely to balance out with the exchange rates.

Use "transferwise", they save you money, allow you to hold multiple currencies, and transfers are quick. They have a great section explaining how their system works. Why not have a look. I've been sending money overseas and receiving for more than 20 years, i started using these guys about 8 months ago, and I have found them to be the best. And no, I have no shares in them and I get no commission in giving this recommendation.

Never use a bank, TW are very very good

I send money to my son in London for birthday's etc using TW.

Hardly beyond recent ranges.

Do you feel it's as straightforward as a move lower the value of the NZD? That's it?

Does anyone have the Australian equivalent figure? This sounds absolutely insane, wonder if the NZD will fall off a cliff

Really what a panic for no covid. We in best position in the world.

Unless you rely on Air BnB, Tourists, Foreign students, or temp work visa staff to pay of your debt.. Pretty sure Winston was in the press today asking all temp visa holders to "go home" to boot.

Don't have the aus figure, but given the relatively modest falls in NZD, nobody seems too surprised.

Love expressions like "forward guidance". Makes it sound like they have it all under control.

12000$ per person. 48K per family of four.

We need more immigrants to spread it round a bit more..

haha

negative OCR by end of year

At some point of falling deposit rates there will need to be a government guarantee of deposits, otherwise the RBNZ better get some $10,000 notes printed up so they don't run short again when savers give up and move it to the mattress.

Michael Reddell has his doubts (posted yesterday, before the MPC and the High Poo-Bah had rendered their verdict) thus:

One of the incidential curiosities of the bond purchase programme is that at times like this you hear a great deal of talk about how it is a wonderful time to borrow and the government can lock in very cheap long-term funding. And yet what do really large scale central bank bond purchase programmes do? They transform the liabilities of the Crown from quite long-dated to increasingly quite short-dated, exposing the Crown (us as taxpayers) to really substantial interest rate risk. Perhaps at the end of all this the Reserve Bank will have $50 billion of government bonds, with a representative range of maturities. On the other side of its balance sheet, it will have a lot of very short-dated (repricing) liabilities – all that settlement cash (see above). Whether the Bank eventually sells the bonds back into the market – which hasn’t happened a lot in other countries – or holds them to maturity, the interest rate risk doesn’t go away. It isn’t obvious what public interest is being served by skewing the Crown’s (net) debt so short term. Perhaps interest rates will never rise again……but that won’t be the view many people will be taking...

I'm not liking this new constricted NZ where:

- businesses are not allowed to fail

- people are not allowed to hug

- people are not allowed to die

- people are not allowed to travel

- asset values are not allowed to fall (edited, thanks IO)

- the government decides what's best for everyone

What happened to let the normal course of life unfold?

At the risk of being hanged, drawn and quartered after the police enter my house without a warrant, it's called technocracy, and is a favourite of the left. Failed spectacularly in Russia, and is messily beginning to unravel in the EU.

Ideology alert ideology alert warning warning

Both the left and the right were squandering the planet at unsustainable levels. They just differed a little in which cohort they though should profit.

Lucky me - an idle centerist.

Both National and Labour are left of centre. Labour is just more left

we have not got to pushing doctors out windows yet when they speak out.

the worrying thing is the NZ police now using face recognize tech, policeman and technology do not go well together

i think there will be a push back on liberties later down the line

We've had face recognition tech by law enforcement for a heck of a long time, not to mention numberplate recognition at service stations etc. What I grew up thinking as big brother has turned into loyalty cards... and don't even get me started on prefentiality combined with recog... we're a very long way behind on privacy rights in the commercial sector, so state is simply playing catch-up...

Just wait until we go quantum stateless..

Funny how this wasn't a concern when people started having to put off a family later and later. Why is that, I wonder.

Just have to remember society only needs to be enjoyable and prosperous if you're of a certain age group. Everyone else is a slave to the lord, even the children.

You missed asset prices aren't allowed to fall.

But agree, I'm starting to think that financial markets are fake news but hopefully the other points slowly start returning back to normal slow time this year as the virus allows - although was reading last night they think 18 months the earliest for a vaccine if at all so not what society is going to look like at all!

Good point, added to my list now

Nobody likes being constricted but they might prefer it to;

- rapidly spreading new virus

- people hoarding and food rationing

- loved ones dying

- healthcare staff dying

- living in fear of all of the above

Yes Yvil appears to be describing a communist/socialist state while having a dig at the current government, yet the opposition government (National) look like they can wait to get right back into bed with an actual communist state (CCP). So the opposite of what he is having a dig out, may result in it actually happening for real here in NZ, including a red flag. It quite bizarre.

national over there history have never been a civil liberty party, car less days, wage freezes, who can forget the dawn raids, if you look back it was roger douglas that opened up a lot of our society, and when he created his own party one of its founding principles was individual freedom, personal responsibility.

That individuals are the rightful owners of their own lives and therefore have inherent freedoms and responsibilities

That the proper purpose of government is to protect such freedoms and not to assume such responsibilities

its a pity they have moved so far away from that

Ginga, one single word in your comment explains it all: FEAR, fear of everything which stops us from thinking rationally (surprisingly even an woman of your intellect) and makes us surrender our freedom to others

Mate if you are that desperate to find out what unchecked spread of the virus looks like I am happy to shout you a one way flight to Brazil if you can convince them to let you in.

Yavil have you considered moving to the US? I think you would be a lot happier there then here since you seem to appreciate financial gain over saving lives. Have to admit that tactic hasn't been working out well for Trump so far. BBC Coronavirus: The lost six weeks when US failed to contain outbreak.

https://www.bbc.com/news/av/world-us-canada-52622037/coronavirus-the-lo…

Reserve banks have policy of. Solution for polution is dilution.

Money printer goes brrrrrrrrrrrrrrrrrrr

They will need a negative ocr if they are to have any chance of hitting their inflation range target...

the 1yr/1yr swap rate is -5 bp's.....

So Figure 3.1 in the MPS shows in a nice diagram the transmission mechanism for monetary policy. We have:

NZ Exchange Rate decreasing -> import prices down, export revenue up

Retail Lending Rates down -> Saving down, borrowing up

Risk Free Rates down -> Asset prices up, yields down, wealth up

Inflation Expectations up

Yet, our exchange rate seems stuck in it's current band largely unaffected by the already unprecedented policy response. Our savings rate is going through the roof and borrowings are heavily curtailed. Inflation expectations are hideously low. The only piece left is asset prices, every other transmission mechanism is broken. And yet the RBNZ has just doubled it's already astronomical LSAP program.

They are clearly, shamelessly, trying to blow up asset prices. Personally, I seriously doubt even this transmission mechanism will remain open to them. Happy to hear others thoughts on this.

You think that it's going to stop working soon, or that it's not working now? The former, I don't know, but looking at the NZX over the last couple of months suggests it's working ok at the moment. Similarly for US equities and the Fed's efforts.

I think it's going to stop working soon, and economic reality is going to have to catch up with the current financial eutopia. Certainly up until now it has been a roaring success at dislocating markets from reality.

I'll add that when the correction does come, it will be all the more painful because of actions like this one. It's completely irresponsible behaviour on behalf of the central bank to continue to blow asset prices up in a market already at horrendous multiples.

Predictions seem to lie somewhere between massive inflation and roaring deflation. The prediction confidence envelope is about as wide and useful as covid predictions, which has a certain irony to it.

Think stagflation...but may see deflation initially.

Listen Adrian, do whatever you have to do..... just DO NOT let house prices go down!!!!!

I've staked my whole retirement on 5% capital gains ad infinitum! PRINT MAN PRINT!

Seeing as selling houses to each other at increasing multiples of income is our economy I think you're fairly safe. Government are the biggest existential threat to property investment, if they ever normalised the tax structure across investment classes it would mean a flight of capital to other investments (shares, businesses etc.)

I wonder if you are right on this particular point, in NZ all capital gains are exempted from tax. So unless you mean only tax property capital gain, I do not see how introduction of capital gain will cause such a flight.

All capital gains other than those caught by 'the brightline test'

House prices will still fall along with nearly everything else except our debt levels

Any commentators currency traders (present or ex)? Would love to get some educated views on where they think NZD is heading/time frames etc.

FWIW, if any economy can come out of 'this' well, it should the New Zealand one.

But much will depend on how we approach reconstruction.

So what Grant come out with tomorrow, will be crucial.

Any thoughts how low we could go against USD?

Currencies trade in pairs. The NZD could remain stable while the other side of the pair can go up or down according to events in the other side's country. The NZD will appear to appreciate or depreciate relative to movements in that other currency. If the current global situation deteriorates their will probably be a flight to safety in the USD versus all other currencies. The USD will go up. The NZD will go down against the USD. In the meantime the NZD is down 1¼ cents or 1200 pips against the AUD in response to the MPS announcement

Any thoughts how low we could go against USD?

LOL - the only way to make money in the FX market is to run a book at a big bank - flow gives you advantage beyond any expectations or forecasts.

Some of the larger currencies have been QEing for a while without major falls. Be interesting to see if our NZ dollar can hold up. Faith is all, i am considering Bitcoin as a survivor now.

Yeah you might want to check out who is actually investing in Bitcoin. I think you'll find it's mostly the Chinese who have been using it as a way to get their money out of China for a while (Like around 90% of users). Not only that but the Chinese Government is currently test piloting it's own digital currency so you can imagine what could happen to cryptos when China enforces it's citizens to adopt their new currency.

Wired article: Inside China's mission to create an all-powerful cryptocurrency. "Bitcoin miners face severe regulation in China. Instead, the country is creating its own digital currency – and it could be adopted at a fast rate". https://www.wired.co.uk/article/china-digital-currency-crypto

Wall Street Journal article: China Rolls Out Pilot Test of Digital Currency "Milestone for world’s biggest central banks in path toward launching electronic payment system." https://www.wsj.com/articles/china-rolls-out-pilot-test-of-digital-curr…

The biggest buyer is by far Grayscale Trust - previously buying 21% of all newly mined BTC. Now, combined with Square, they are buying up 52% - this was BEFORE the halving. These are for institutional USA investors to buy (at a huge premium): https://bitcoinist.com/bitcoin-institutional-grayscale-buying-supply/

As for China, they prefer to use stable coins like Tether. Stable coins are up 70% in total market cap this year to 10 billion as more are minted to keep up with supply

If you think $60 billion sounds a lot check out what's happening in the UK. "Since the beginning of the pandemic, the BOE has cut rates twice from 0.75% to 0.1% and announced £200 billion ($247.55 billion) of new quantitative easing, bringing its bond buying program to a total of £645 billion."

CNBC : Bank of England projects worst UK economic slump since 1706. https://www.cnbc.com/2020/05/07/bank-of-england-holds-interest-rates-bu…

+10x the population. 67 odd million people vs 5 million.

Per capita, NZ takes the cake.

Today the "Lord of the Manor" acknowledges that he/she needs his serfs to survive in order to till his lands and so keep paying their tithes without which he/she will not enjoy the benefits to which he has become accustomed

Deflation is a general term brandied about without any specificity, it seems the article refers to deflation in a CPI sense, that doesn't mean deflation of assets for example, time is overdue to have a more specific conversation of what is expected to devalue in $ terms

Deflation of many if not all things:

Housing (prices, rents)

Services

Many goods

Groceries won't deflate though.

I think overall the deflation will be minor.

"Minor deflation" is a bit like "minor brain cancer"

I'm not sure of the validity of that comparison.

You can have low or high rates of deflation, like you can have high or low rates of inflation.

The rate of either informs how great the impact is.

Deflation I believe may be an opaque reference to falling wages.

Since we import most stuff we buy in the shops and our currency is falling it isnt going to be CPI that's falling, imported inflation should take care of that.

So if we see wage deflation then rents and house prices are probably the only things that can give.

In economics, deflation is a decrease in the general price level of goods and services. Deflation occurs when the inflation rate falls below 0%. Inflation reduces the value of currency over time, but sudden deflation increases it. This allows more goods and services to be bought than before with the same amount of currency.

I would be quite interested in seeing some inflation data soon. We have embarked on massive quantitative easing without any guidance made available on the impact of successive packages (e.g. if QE is actually having an impact.)

QE. Great. Fiat currency, gold.

All fiat currencies are on a race to the bottom. No country wants to have a strong currency. The fiat of every nation continuously loses it's buying power. This is why fiat currency is not effective as money, it is not an effective store of value.

If fiat has some intrinsic value, then how about this; the govt prints $100,000 for every household, and simply gives it out. That way, everyone can just live quite ok. Goods and services, we'll just import those. Why not print $200,000, or even better, $300,000, per household, then everyone can live a great lifestyle.

$30bln, $60bln, we already have this system in operation, and taking it to the ridiculous, like $300,000 per household, is a simple way of seeing how ridiculous printing currency is, and why many call it monopoly money. Historically all fiat currencies fail, every single one of them. A piece of gold from 20bc will still buy something today, because it is an effective store of value.

Everyone stops purchasing, deflation. Massively increase money supply, a fast move into inflation. Will it be stopped before hyperinflation?

First we had the bitcoin halving, now we have the NZD "doubling"

Every time central bankers come up with another four-letter acronym, all I hear is one four-letter word in all caps with five exclamation marks after it.

The real story here is the RBNZ has factored a year long lockdown into it's figures. The government has shown it's hand. That's what the police state powers are for. Mark my words, we're not getting out of this any time soon. Enforcement is going to get ugly.

Immigration was one thing Nats used to dig us out of the GFC hole (or put us into a big hole depending on perspective). Will be interesting to see the development of immigration related policies.

I'd be happy if the immigration policy was the one they always said we had - skilled immigrants. Trouble is they tried to identify skill rather than just measure it by how much the employer was willing to pay. Engineers and Doctors earning over $120k pa with an expensive work visa - great; checkout operators not great.

The government now needs to issue $60 billion of bonds to complete the cycle. Reserve Bank buys bonds -> Bond-holders sell bonds to Reserve Bank, buy more from Treasury -> Treasury spends money into the real economy. Otherwise the system is flooded with reserves & no one holding the reserves is willing to spend it on real people. Notice that step 2 uses the secondary markets to hide the fact that the Treasury has the backing of the Reserve Bank to spend whatever it deems necessary. From a consolidated view, the NZ government can always afford whatever is for sale in NZ dollars, and right now there are a lot of unemployed people-hours to subsidise/reimburse/buy.

And there you have it: as of Budget 2020, Treasury "has hiked its forecast issuance for the year to June 2021 to a whopping $60 billion". This "debt" will end up as owed by the Treasury to the Reserve Bank - it's not really debt if you owe it to yourself. It will rightly be spent into the real economy, into the bank accounts of households and businesses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.