The Reserve Bank (RBNZ) is widely expected to nearly double its quantitative easing (QE) programme to $60 billion on Wednesday, in a bid to stimulate the economy.

The RBNZ’s Monetary Policy Committee (MPC) will almost certainly keep the Official Cash Rate (OCR) at 0.25%, having in March committed to keeping it at this level for at least a year.

However, with markets pricing in a cut for before then, all eyes will be on whether the MPC provides even the smallest hint at whether it’s willing to cut the OCR before March 2021.

RBNZ watchers will also be interested to see if the MPC provides additional guidance around its QE, or Large Scale Asset Purchase, programme.

While most economists believe it will continue to commit to spending up to a certain amount on New Zealand Government Bonds, the MPC could also indicate how it would like to see these bonds priced.

ANZ chief economist Sharon Zollner believes the RBNZ won’t go as far down this path as the Reserve Bank of Australia has, in essentially saying, ‘We will buy as many bonds as is required to keep the yield on 3-year Australian Government Bonds at 0.25%’.

She said it wouldn’t make sense for the MPC to do this on top of saying, ‘We will buy a total of up to $60 billion of New Zealand Government Bonds over 12 months’ for example. However, the MPC could provide some looser guidance on where it would like to see the yield curve.

Bazooka required

Jumping back a step, the MPC in March and April committed to buying up to $30 billion of New Zealand Government Bonds and $3 billion of Local Government Funding Agency bonds over 12 months on the secondary market (IE from investors who already own these bonds).

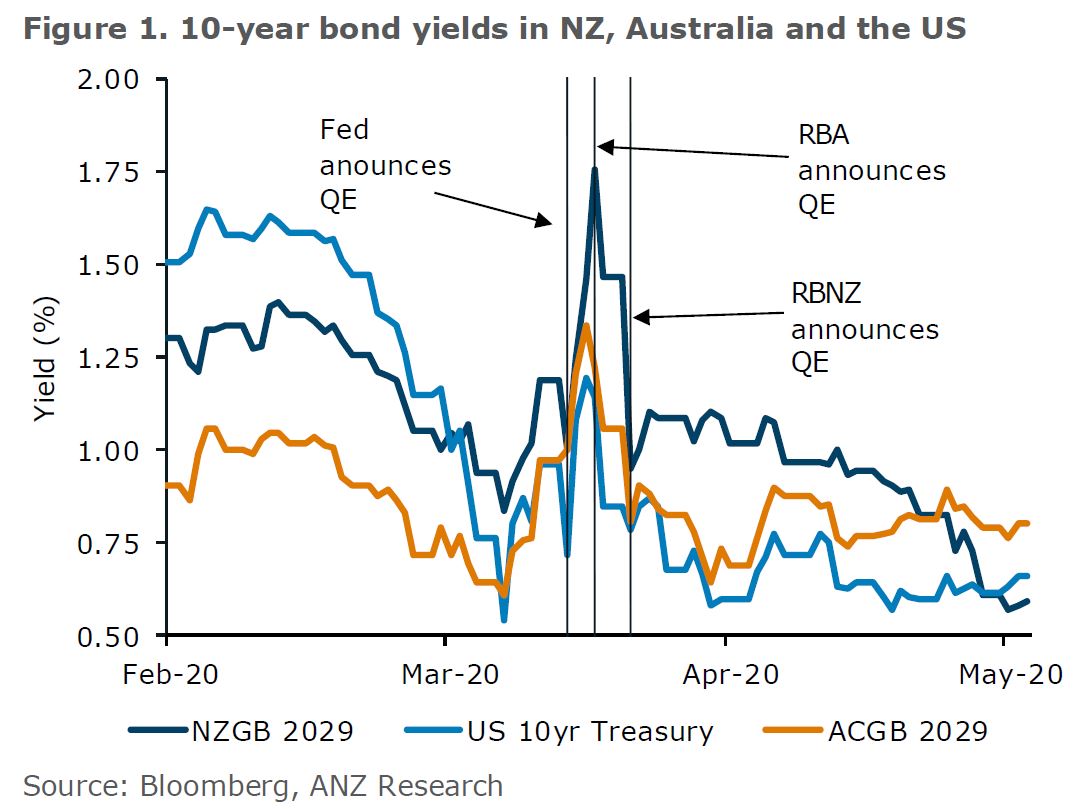

The aim of these commitments is to keep interest rates, and thus borrowing costs, low, to encourage economic activity. With a very active buyer - namely the RBNZ - in the market, it makes it easier for investors to sell government bonds. This pushes their prices up and yields down.

So far central banks’ efforts have been successful, as per this graph from ANZ economists:

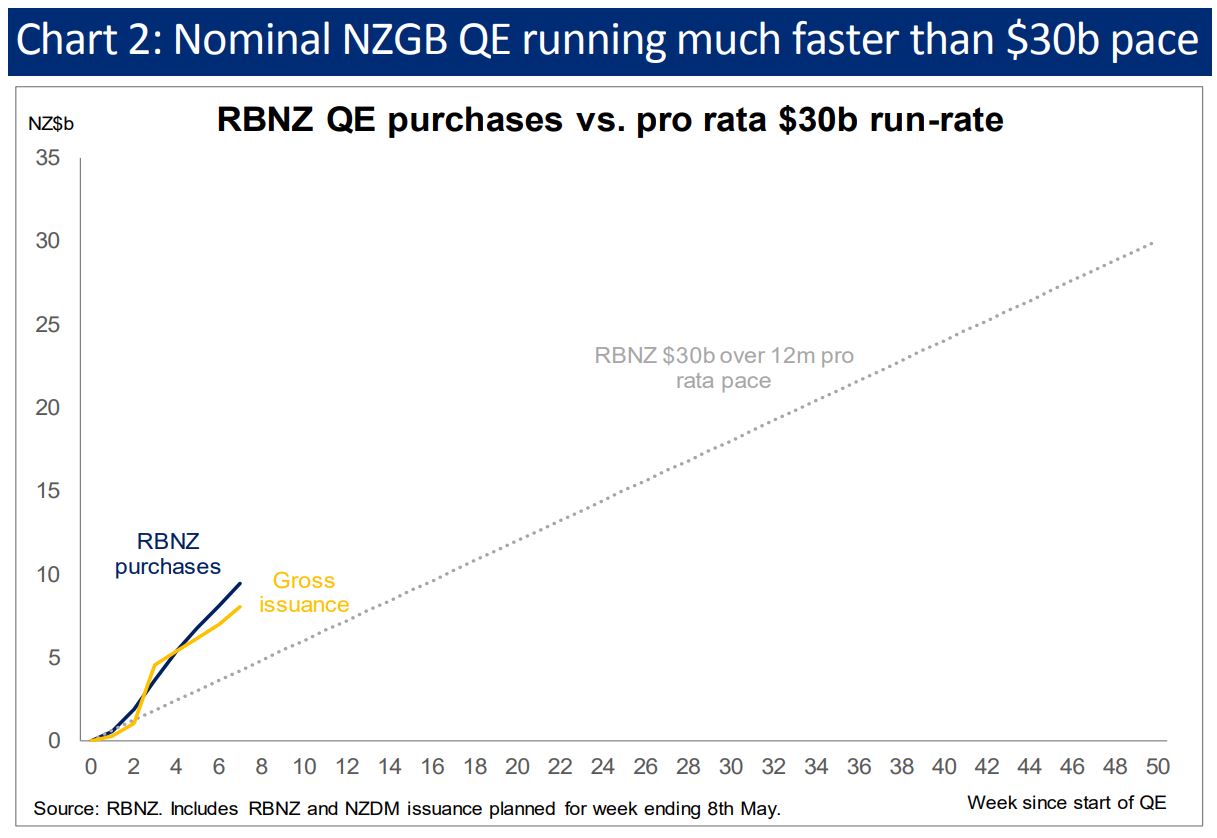

To date, the RBNZ has bought a lot of New Zealand Government Bonds. If it keeps buying at the rate it’s going, it will have accumulated around $70 billion of these bonds by March 2021 - way more than its $30 billion limit.

This graph put together by BNZ interest rate strategist, Nick Smyth, demonstrates this:

For this reason, and because the Government is expected to issue a lot more bonds to help pay for the COVID-19 response, economists expect the RBNZ to increase its purchase programme significantly.

Treasury will on Thursday provide an update to its bond purchase programme alongside Finance Minister Grant Robertson releasing the Budget.

Getting the mix right

The RBNZ has indicated it’s willing to buy between 40% and 50% of all New Zealand Government Bonds on the market.

Most economists believe the RBNZ won’t buy too many more Local Government Funding Agency bonds. But Smyth believes it will add $2 billion to $3 billion of inflation-indexed government bonds to the mix.

“This would help liquidity in the market considerably. It would also reinforce the RBNZ’s commitment to get inflation back to the 2% midpoint of the target range, because it would have a financial exposure to inflation on its balance sheet,” Smyth said.

It’s important to note that Treasury (IE taxpayers) will eventually have to repay debt from the QE programme to the RBNZ. The RBNZ could technically write-off this debt, but this could have implications for money supply and erode confidence in the system.

Robertson: Direct financing unnecessary now, but ‘never say never’

While some economic experts are calling for the RBNZ to buy bonds directly from Treasury - instead of forking out more to work through the market, Robertson isn't keen on this - yet at least.

On Friday he reiterated his position: “At this point in time we don’t see the need for that… The bond markets continue to operate well and they [the RBNZ] are intervening at what I believe is the appropriate point.

“Both the Reserve Bank Governor and myself have said ‘never say never’ on the direct purchase, but for now there is no need for that. The financial system in New Zealand holding up very well.”

Keeping inflation buoyed remains the goal

By buying bonds, the RBNZ supports liquidity in the market. Nonetheless, any action the MPC takes must be done with the aim of keeping inflation between 1% and 3% and maintaining maximum sustainable employment.

The RBNZ’s Survey of Expectations - a quarterly survey of New Zealand business managers and professionals, last conducted at the end of April - recorded record low inflation expectations.

Survey participants saw the inflation rate falling from 2.5% to only 0.74% in a year’s time, and 1.24% in two years’ time.

Will we still need an OCR cut this year?

Yes…

In order to prevent deflation, Westpac chief economist, Dominick Stephens, is among those who believe the MPC will have to go back on its word and cut the OCR to -0.5% in November.

He maintains the most likely scenario is that the MPC on Wednesday says something like it “intends” to (rather than it “will”) keep the OCR at 0.25% before in August more clearly signalling a cut could be on the way before March 2021.

The RBNZ in March said it couldn’t yet take the OCR into negative territory because banks’ computer systems aren’t ready to deal with this. It put a one-pager on its website explaining these issues.

It last month also pointed to international research that suggests asset purchases worth 1.5% of a country’s gross domestic product (GDP) equate to 25 basis points of monetary easing. So the RBNZ’s $33 billion bond buying programme should have a similar effect to cutting the OCR by 150 basis points.

… No

Unlike Stephens, Zollner doesn’t see rates going into negative territory anytime soon.

“Quantitative easing would in some sense have to be seen to be tapped out, or at least inadequate,” she said.

“This could be either because the economic situation takes a severe turn for the worse, or QE starts to hit its limits or lose its efficacy at keeping long yields down, with the economy still in dire straits.

“Even then, there would be other options that we think would be effective and considerably less risky than negative rates, such as yield curve guidance.”

Zollner said timing is also key, pointing out that making it even cheaper to borrow wouldn’t be that helpful at the moment, as firms are looking for working capital, not credit for expansion.

She also said negative rates, which discourage people from making bank deposits, “severely impact the health of the banking sector and therefore may impair the free flow of credit over the longer run”.

She said global credit markets would need to be in decent shape, which they aren’t right now.

“Negative interest rates severely damage bank profitability and therefore might mean that the cost of raising funds in a severely risk-off environment is higher than otherwise.”

Furthermore, Zollner said, “Negative rates inflate asset prices and encourage excessive risk taking and leverage, not all of it for economically productive purposes.”

208 Comments

What's the point of cutting the OCR when banks have been reported to be barely lending to businesses under this new finance guarantee scheme so far? Only lending about 24 mil out of about 6 billion available so far. Many businesses seem to need that money now. Or is it to try and continue to keep house prices high? The more the housing bubble was allowed to inflate, the bigger the bang when it pops IMO, and our house prices in NZ are far too high compared to other countries and our low incomes. Why incentivise more people to get into debt at times when job security is potentially low for many? Also this is the time to save, but the rates at banks and no guarantee is a problem. Especially for elderly who need somewhere safe and rely on the interest to supplement their super. I see in Oz where they do have a largish deposit guarantee, that people were withdrawing a lot of cash over there. I hope to see a guarantee scheme introduced here for banks without caps, like there was for the GFC to protect savers including the elderly. A lot of people lost money, including me, when finance companies collapsed.

Hi Rob, I just want to clarify for readers that while banks haven't lent much at all under the Business Finance Guarantee Scheme, as you say, they have been lending a lot to businesses outside of this scheme. They've provided $7.2 billion of new business lending since March 26. You can keep tabs on their lending here.

Banks expect more businesses to take out loans under the Business Finance Guarantee Scheme once their immediate working capital needs have been met.

Tell me it isn't so .....

Wonder how much of that $7.2 billion (new lending?) is simply substitute lending. The smart money currently with (say) $10 million business loan bank debt paying 9%, can borrow from the Business Finance Guarantee Scheme at 0% for 1 year and use it to liquidate the "business loan" - I would

It was my first thought.

I understand the declaration covers that contingency, it must be for overhead etc. , we will see on Monday...

Next question: how is even more debt a solution to anything from this point? :)

The number of zombie firms - where earnings don't cover interest payments - being kept alive by a reckless Fed is now alarming: that means capital tied up in stagnating technologies and past-their-use-by-date business models, and not available to innovative firms and new blood and is the death by 1000 cuts to a free market economy. I suspect we're now creating zombie firms in NZ to add to our existing stable of zombie dairy conversions being managed by the banks: start with Air New Zealand.

Really, we just need to be back working. Treasury's claim that 75% of our economy is back under level 3 shows how all the talent has left that building - it's a laughable notion: just because firms could go back to their premises and twiddle their thumbs doesn't mean they're working. All that is happening on level 3 is some very small level of goods are being sold online, nothing even approaching normal, as most SMEs will not have set up an online presence because it would've been pointless: it takes years of branding to get customers to your site. (Which is why every article against commercial property because of online sales taking over retail space is wrong, and every article suggesting remote working to replace office space is also wrong (office sector will see productivity fall off a cliff with remote working). Which was a round about way of saying we need to go to full level 2 next week. We don't have the luxury of waiting.

Notice the '1965' is gone from the end of your account name... so you did get banned.

"most SMEs will not have set up an online presence because it would've been pointless: it takes years of branding to get customers to your site"

Once again sounding off about things you have absolutely no understanding of. Setting up a simple Shopify store takes a few hours depending on complexity of the business and setting up a basic Google Ads or FB campaign takes maybe an hour. Even a semi complex business could get a functional system set up and making sales in about a week. It's not hard.

But by all means please tell your Boomer friends to keep investing based on your fantasy understanding of how the digital world works.

No idea why the 1965 is missing: I've changed nothing nor been banned. Are you stalking me.

The majority of SME's who had no internet sales facility pre lockdown, and that's most of them, will have sold nothing during level 3. Guaranteed. People have to find you online. In rural small town NZ, this is farcical.Proof: sales. Through this event, Briscoes, whose brand is one of our biggest, who sells online, their sales nevertheless collapsed.

I buy staple items online. No interest in buying most items online.

Jeez I'm sick of you. And stop stalking me. Go get a life.

Oh, and welll done. As ever, you attack me, but never even try to speak to the content of this thread. I still have no idea why the editor allows your pointless bile.

Also for editor: what did happen to my 1965? Out of curiosity.

I'm guessing your Mark Hubbard 1965 account got banned, i recall that one was only a few months old whereas the one you're posting on now is over 9 years old.

Me --> looking at analytics dashboards for 50 SMEs every day.

You --> Boomer reading news and pontificating.

I know for a FACT you are wrong.

Speechless, we do not recommended that Google Ads or FB campaign is a good use of the marketing budget for small businesses, we analyse all that data for our clients, many 100's of sites day in day out. Good search engine optimisation and improved rankings are much cheaper and always lead to more actual follow through sales and exposure.

But, and its a big but, NZ has some of the worst websites and online shopping i have ever seen. Even the big brands have appalling shopping structures and services compared to almost anywhere else. Many websites still have the functionality and speed of the 1990's in other countries).

There is a very long way to go for NZ to catch up!

We have a population of 5 million people. It's an incredibly small and insignificant market. While it is getting cheaper to develop shopping websites these days. (Shopify, WooCommerce etc). It's not viable for many retailers and brands to invest the necessary amount for a top quality shopping experience, invest in eCommerce staff, as many won't make it back on their investments. I have heard of some major companies here spending millions on websites to return a fraction of that in revenue.

Whereas in other markets (ie US, UK and Canada), the market is larger, more competitive, and lucrative so you can better ROI for the same amount you'd need to spend on solid shopping site in NZ.

It's the same with advertising in this country. Advertisers charge big country rates to reach 5 million people. Hence the investment in measurable cost-effective platforms like Google & Facebook Vs endemic NZ media.

I am sorry but I could not disagree strongly enough. You can get a functional e-commerce website working for very little money, way cheaper than the overheads of setting up a physical shop. You don't need to pay anything for advertising if you get yourself organically on the first page of google after identifying the key search words that would lead to organic sales and traffic.

Your stance on the digital economy is very representative of the NZ mentality though. Kiwis are often convinced that there needs to be a huge outlay on e-commerce and spend a fortune on a huge, expensive bespoke website, which are often nothing more than costly status signalling. We have this argument with our Kiwi clients ALL THE TIME. They have this irrational belief that they have to throw huge sums of money at their online business. Meanwhile, there is some Mumpreneur having a basic word press website tweaked, following SEO recommendations and bingo. profits and growth. If you can stick it in the post and to your customer within a few days, if you can respond to emails quickly...you're golden. Our younger Kiwi clients intuitively understand this. We tend to have to turn down work from older Kiwis because they just don't get it and we can't in good conscience take their money to build something they don't need and will never make back their money on. Our reputation is built on provable data, we send monthly reports and analytics. That's our model. We are not into sales, or schmooze or networking, we will provide evidence of what worked or didn't work. That's an anathema to a lot of older Kiwi's. Kiwi's only make up about 5% of our client base though, and most of those don't even know we are doing work for them, because we have some expensive designer or developer who doesn't have a clue how to do any of the back end stuff paying us to do it, while they on-charge thousands for lots of fancy sounding features.

Spot on. We did a digital literacy survey of CBD businesses about 24 months ago. Most had no website, email address or FB presence. Absolutely staggering... They were basically all operating off 1990s business models of exist and wait for the customer. Over 90% had no active frontage presence for their business and wonder why no one was walking in. The level of business acumen in NZ is so low. Many are just struggling from day to day. I sincerely hope the lockdown has been used as an opportunity to modernise business practices and get people to actually start working on their business rather than sticking to same old same old processes and expecting better results.

Trying encourage spending but no one wants to spend. This government needs to realise they can not save everyone, I fear that the group they will try and save isn't the group that produces the greatest benefit to the economy.

Indeed. Can't encourage spending by taking interest income away from pensioners and by signaling to savers that it's time to hunker down.

Exactly - its just leading us closer to disaster! Think Expat the other day said he was now looking at buying another property because of the way things are working out! We need to be making other forms of investment attractive - I think of my grandparents in their retirement..mortgage free on the house, own a small amount of shares and bonds, then the rest was just savings/term deposits which through the '80s and '90s provided a reasonable return and a comfortable, safe, low risk retirement.

Now we appear to have boomers speculating on a housing bubble right at the point of retirement and competing with the next generation for a home...its an absolute recipe for disaster. All I can say is the leadership and management from this current generation has significant room for improvement - and at a guess, we're about to see the outcome of self interested, short term thinking and planning. Mass unemployment and expensive houses! What a combo!

Has there been any utilitarian perspective to their thinking? Any thoughts to the future? Any prudence? Or is it me, my housing portfolio and my retirement.

True, true.

I see Simon Bridges saying with a startling lack of self-awareness

"Irresponsible economic management will put a mortgage on our children and grandchildren's future."

Where was this sentiment when they were mortgaging the future of children and grandchildren to enrich asset holders over the last decade? When this mortgage on the future of children and grandchildren was being called "a sign of our success" and "a good problem to have"?

Crocodile tears.

Pretty much everything National has said since the election can be summarised as, "All these problems we created are really bad! But we totally didn't create them, Labour did!"

From the party that literally spent its entire 9 years in government blaming every problem on the previous government.

Yeah, through 9 years in power, they really messed up. They blindly followed other countries and encouraged more people to take on debt to blow this property buble, but disencouraged people to save money to be prepared for this sort of crisis. See where we get to now? Large percentage of people are carrying huge mortgages, yet we are forced to lower our OCR and encourage them to increase their spending to stimulate economy. The OCR could go negative. But banks will suffer because of this. Can't we see that it's not sustainable? I am glad this government didn't touch the surplus we've had a while ago which national strongly against it. If we did, then we would be in a worse situation.

I'm staying well away from buying a house until this has really kicked in.

An articial on TV1 last night of lady saying it's looking like a good time to buy due to low interest. Wait and you'll pay a lower price for a house and also have lower interest. Win win..

I would prefer to pay higher interest on a lower priced house and effectively have the same monthly amount going out, than a high price on a house with a lower interest rate, as is the current situation. This is because higher interest rates encourages people to save a higher percentage for their house, as they aren't having to save as much for a bigger percentage equity in the house value. Back on the 80s when house prices were relatively low compared to earnings and interest rates were double digits, it meant that people were incentivised to pay off their mortgage quicker due to those high interest rates. I think it is partly a psychological thing. People don't want to be paying 20 percent interest to the bank. Real estate agents have definitely benefited from this current situation because if house prices double over 5 to 10 years, their commission also largely doubles as most earn commission at a percentage of the sale price

Also the period of high interest rates coincided with high wage inflation.

True. The problem we may now be facing is very low interest rates, but rising inflation, and then wages not increasing enough to match that. Who is going to pay for the higher wages that are needed?

Kezza

Good to see a constructive positive comment - low interest rates, falling house prices, lack of LVR as a hurdle to sufficient deposit - and you are considering making the most of opportunity when it presents itself. Too early to make a call to the extent of the fall in house prices or when it will bottom out, but whenever it stabalises you appear to be open to that opportunity.

Anecdotal information I have is that locally there is renewed interest and talk by a number of property investors; quietly waiting rubbing their hands together over the low interest rates, falling house prices, and lack of LVR as a constraint. Some posters will choke on that but taking opportunity (and the associated risk) is why they are successful and why renters continue paying their mortgage off for them.

The reality is that home ownership for 25 to 35 year old has fallen from 65% to 35% over the past 35 years and there is nothing to suggest that is trend is going to get better. That is not the situation that we want, but individually, success doesn't come from moaning, but rather making the most of the situation and opportunities that present themselves.

Richie McCaw success was based on this; if the refs interpretation was different to his, the opposition wasn't playing to his liking, or the weather was rubbish - he never moaned but adapted, played to the situation and looked for and made the most of opportunities.

The problem is not the greed, because let's face it, humans are humans. The problem is that as a society we find certain forms of selfishness abhorrent, but for some reasons property speculation is ok, and no one has been willing to tax these j*rks fairly to slow down the fat cats weight gain most of which is misguidingly concentrated above their necks

SolveIt

Income at least is taxed.

I entirely agree with you though - a CGT is essential with losses ring fenced and carried over.

While a supporter of property investment I have never known a investor - whether it be in property, equities or business start-ups etc - who hasn’t taken into account capital gains as a factor. To deny this they are lying.

I generally agree and have skin in the game as a property investor. However if the current trend of declining home ownership continues, then it's going to get nasty. The non-home-owning bloc will gain a majority, gain solidarity, and become apoplectic with rage over their poor financial situation. NZ generally goes over the top with everything so the policy response will be scorched earth for property investors.

If you do any reading on the likes of the end of serfdom or the French Revolution you come to realise that landlordism is a great gig while you have the support of the most powerful ruler/s of the serfs, but when they (the serfs) realise they're being robbed and actually hold the power, the pitch forks come out and the landlords need to flee or risk having their heads chopped off.

Many that post here seem to be hoping for a collapse in house prices so they can buy at a level they see value at. I’m coming at this with a different position. I have a mortgage free home and cash savings. If I budget well, and my savings keep their value, then I can retire early when the likely redundancy occurs. I have withdrawn cash for a few months expenses and invested in Kiwi bonds. I’m largely immune to a bank run, but am exposed to a devaluation of the currency value long term. This QE scares the heck out of me. Buying property in the likely dip could help preserve the value of my savings.

I understand some banks expect a15 percent drop, and banks tend to be quite conservative. Employment rising and less jobs imo are a concern

On the way up conservative would mean projecting lower gains, and on the way down bigger falls.

15% is nothing. The correction will be larger than this I reckon

Talk is cheap and you are tops

This has happened before - in a country, in Asia, starts with 'J'... end in 'apan'

Yeah but just because every other country that had a housing bubble had a crash doesn't mean NZ will! /sarc

Cycles of boom and bust have happened for ever. But Japan does seem to be an exception case in monetary terms at least. Their central bank actions must have resulted in monetary inflation, yet it has not over such a long time. This is the exception to most other crisis and one many people try to explain with many different theories. So, I am not sure Japan is a very good example as it not very well understood why they are different (at least to my limited knowledge).

It about saving them up to the election:)

Rob, you say house prices are too high in Nz?

What would you say a reasonable house price should be if you think they are too expensive.

How much for a stand-alone house on 600m2 and the house 100m2

How much for a 200m2 stand-alone home?

Look forward to your answer

You don't look forward to anyone's answer....your cup is already full. No room to learn others views.

My 50 year old house of 135sm has a CV of $250,000 and a land value of $800,000 - I think a fair price would be $400,000. So your property with old house about $250k and a new house $400k.

Bought mine for 41K....a fair while ago. Fair do's. Can still buy one in Europe...for same. But it will buy a Chateau....if I flog it...to death today.

Irony is...the bubble is popping there too. Best be quick.

Hi Lapun, I will pay you $500k for your house as long as its in Auckland. $100k more than your fair price. No agent commision, no marketing , etc. Im happy to rent it back you at $500 a week. Win win cheers

Well sales last month were about CV but price of a house is what the most enthusiastic will pay for it. When I visited family living in a suburb of Las Vegas 10 years ago my cousin had a colleague who had paid $250k for a $750k new high quality property. That was just after Auckland CBD apartments could be bought for $150k that had been advertised two years earlier for $350 (mine cost $179k and has been a little gold mine) - must have cost more to build it but it was being sold by a bank repossessed from a bankrupt builder.

Doesn't matter to me what my house is worth other than any impact on rates and insurance. It is a home not an investment. I would like to see prices in Auckland that were fair for the sake of my children.

Lapun, that makes no sense, you mean an improvements of $250k and land value of $150k, therefore $400k?

That 250k and 400k is just for the house value and not land?

We have bought good property residential property in CHRISTCHURCH between 152,000 and $480k so are house prices too expensive in Christchurch or not.

Rents are from $380 to $595 per week for the residential!

Is this too much for residential?

Since we own the home I'm hoping pries will stay unfair. But this was taken at random from Google ""The median price of homes currently listed in Atlanta is $319,000 while the median price of homes that sold is $275,300."" OK the US dollar is worth more than the NZ$ but US incomes are also much higher. I think Atlanta is larger than Auckland and I suspect their houses are larger than your 100sm so prices in NZ are out of kilter.

You say that US incomes are higher than NZ. What's their minimum wage, 7.25 ph and in Atlanta Georgia its 5.15ph unless "subject to the Fair Labor Standards Act must pay the $7.25 Federal minimum wage" whatever that means.

No one in NZ or the US is buying a house on minimum wage. US is 6th in GDP per capita is $65K USD. NZ $40K USD.

Their housing outside of some major centres (ie New York, Seattle, San Francisco) that are home to massive multi-hundred billion $ companies like Apple, Amazon, Google, Microsoft etc is affordable compared to income. (Atlanta is a good example. I went there and the nicest street in the entire city had homes for $1-3M). The US is more in tune with supply/demand & economic conditions. They can also write off the interest portion of their mortgage in their personal taxes, so it's even cheaper to own a house.

As a country, their investments are indexed more towards the stock market than property. Whereas this country is obsessed with owning property, low yield rental income, topping up mortgages & capital gains.

Going to be very interesting.

I'd say that NZs GDP/ capita is low because of lots of small shopkeepers who magically breakeven year after year after year and those on the bene

Or it could be that the "money" go round buying and selling and renting houses and stocks does nothing for GDP per capita.

Lapun, your house has a replacement value: the cost to prepare a similar piece of land, the cost of needed infrastructure (roads, schools, police, hospitals, shops, etc), the materiel, the labor to build the house, the compliance costs, the finance costs etc. All of these costs, except financing costs, have a labor cost component (e.g. material prices include labor, compliance include labor etc). So unless you expect minimum wage to drop, then it is very unlikely you can a piece of land at anything under $150k and building material and labour under $200k. So it will cost at least $350k.

Now, if there are surplus houses, then the "replacement value" is off very little consequence. If people are going to leave the area as there are no jobs, and there are 1000 houses and 800 families to occupied them (an extreme example) then this replacement value is of very little relevance and the houses have lost a lot of their value and can only hope to sell for a fraction of cost. But if there are demand, then the replacement cost is very relevant. So from city to city, it will be very different mid term depending on the actual long term demographic dynamics and available housing stock. Just saying

Here is a perfect example of all that is wrong with our insane housing market. Developers began building soviet style hellholes in Tauranga during the latest greed rush. The homes don't even get any light. The ripped off new owners may be in for a bit of pain I feel.

https://www.trademe.co.nz/a/property/residential/sale/listing/261865574…

FB

So, what are you personally doing?

Lots maybe wrong but there is also a point where one needs to look at one’s situation and do something.

Moaning has its place, but continuing moaning and pointing out all what is wrong as you do (albeit with some justification) achieves nothing other than risking providing a self justification for doing nothing. After all in the past three years according to RBNZ figures, over 75,000 FHB homes (120,000++ people?) have purchased first homes.

From previous comments - e.g. “landlords are leeches” - suggest that you are a renter and you aren’t happy with that. I also wouldn’t be pinning my hopes or any confidence on more than a 50% fall in house prices as you have posted.

Boomer blames Millenial for not having the chutzpah to single-handedly overcome systemic problems Boomer created.

F-king YAWN.

Speechless

Over 120,000 FHB last three years.

Shift the blame - another common excuse.

This is not a boomer initiated problem.

Probably the biggest driver of house price inflation over the past decade has been low interest rates. That was about RBNZ aim for economic stability and - as QE currently - that was as much about supporting businesses and in particular your job security.

Easy cheap baseless shot to blame Boomers.

Just like Trump - rather than owning some personal responsibility look for someone but ones self to blame.

So forget the blame game, take some individual responsibility, and look for some constructive solutions.

So now that businesses and employment are falling apart under record low interest rates - what is next?

IO

I think that maybe Robertson could have been throwing tremendous amounts of money supporting both businesses and employment in all manner of subsidies.

The economy could easily have opened up earlier and businesses and employment would not be falling apart. DOH advice to govt was to have many more businesses open using contactless trading during L4. So why didn't the dumbos JA and GR do that? No they wanted to control everyone in their homes and have most traffic off the roads. Instead of using cops to monitor they made it so that neighbours would report. How dumb is that, this has now cost the country and taxpayers 30 billion and counting that could have been put to good use. Excuse my rant but it is highly frustrating.

Hi Printer8 - You are just way to logical and sensible in your replies.

Suggesting that taking some personal responsibility for one's life and not becoming a victim of the blame game especially blaming the 'Boomers' !

I always maintain we don't don't make the rules, our job is to understand the rules and make our own choices and get on with our lives.

We as a country will bounce back quite quickly, house prices will not collapse, it will be an opportunity to buy in the dip ( 6-9% ? ) those who decide not to again will be even more angry in the future.

House prices are likely to be under more upward pressure in the future as many people around the world witness NZ as a safe and caring Economy/Society.

Some of the 1 million Kiwi's living overseas will bring their return to home dates forward after having very unpleasant experiences UK,USA,Europe.

Jacinda has lifted our profile as a desirable place to live enormously, great marketing !

Happy Mother's day to all Mum's around the country !

9

But we do make the rules! Or do you not vote?

Shoreman

You are the Richie McCaw of interest.co! You advocate playing by (and yes, to the limit) of rules - one makes their own luck.

It does concern me that home ownership has fallen from 65% to 35% for 25 to 35 and that is an issue that we need to address. As previously posted recent Pacific Island immigrants - without qualifications and no capital - were able to achieve home ownership in the 1970-80s so home ownership was within the reach of most.

I am hoping that Robertson's reset of the economy where he is intending to address inequality does that. As many of the boomers have achieved financial security through home ownership I see an emergence of a renting middle class poor.

It concerns me that there are clearly many on this site who are frustrated and angry and look to blame - but personal frustration and anger needs to be directed into solving one's issues rather than becoming discouraged and lack of action and that is what underpins my comments. Unfortunately the repeated comments by some suggest that they re in the later case.

They need to recognise that 120,000 have succeeded in achieving first home ownership. That has probably meant not only a serious commitment to saving, taking risk, and possibly shifting to a cheaper housing region as many have done; if living in Auckland is a choice, then there is a price for that.

Yes, property investors are currently quietly waiting; call them "leeches" as some have done, but they are astute and simply legally making the most of opportunities and that can not be begrudged. Calling property investors "leeches" is no different to opposing sides calling Richie McCaw a "cheat" - it is simply expressing frustration and anger.

How much will property prices fall by and when will the prices bottom out? Anybody's guess - but if the current fall in the NZSX50 is a guide then a similar fall in housing as you suggest could be on the cards, and that is consistent with the bank economist's wisdom as they have suggested. I am waiting to see the first post lock down auction data and sales data.

There are many positive (e.g. cheap money) and negative drivers (high unemployment) but the significance of each in influencing the market is uncertain.

Given the Accommodation Supplement and more on benefits, it is likely to mean that rents are quite likely to remain at current levels. Speaking to a investor here in the Bay, he advertised a property recently for what I thought was quite a high and possibly unaffordable rent; he had well over 30 applicants, most who would qualify for accommodation supplements (meaning a good degree of security for rent payment and not at risk of unemployment) and even a couple of applicants saying they were more than happy to pay a higher rent as it wasn't really going to cost them. Due to the Accommodation Supplement, working couples who are renting are competing against those who are not constrained by income or cost of rent.

So the message for potential FHB is that there is most likely to be some fall in house prices, there are low interest rates seemingly for at least the medium term, the LVR is not a deposit hurdle, and quite possibly should not be expecting either a fall or a discount in rent.

The savvy FHB, like the savvy property investors, will be quietly waiting, watching and looking for opportunity.

You say property investors are astute and then I read TM2's, TTPs and Ashley Church's views and realise that this statement is completely false.

IO, To be fair, we are all very successfull businessmen.

If you don’t think we are astute then that is fine but having a huge net asset figure would tend to confirm, I would say!

You would actually hope for more better people in the older generations, at the same time.

It's shows one level of character and self-awareness to take advantage of a bad situation and make money off it. It shows another and superior level of character to create impetus and vote to change that situation when you know it's bad too. Plenty of people made a lot of money from cheap labour when child labour was legal in Western societies, but at least enough saw the situation's flaws and pushed and voted for change.

Still yet to see the older folk clamouring and agitating for affordable housing for more Kiwis than just themselves.

Shoreman. Thats Perfect

I'd argue that boomers have shifted inflation from CPI (in the 1970's and 1980's) and moved it into assets such as property over the last 30-40 years for their own financial gain.

And I don't see many boomers complaining about it, but more berating younger generations for being lazy and self entitled!

Over to you to decide if that is morally acceptable given the financial pain it will create for many in the future. e.g. the current economy.

IO

Rubbish. Stop being so self-centered and playing the blame game.

Boomers are also suffering financial pain under the current situation over the past decade just as much as millenniums.

There are many retired boomers who ten years ago who had saved a nest egg in anticipation in what was then a safe 6% return from term deposits. Their return is about a third of that, so instead on an extra $15,000 pa to supplement super they are looking at $5,000pa. Quite significant (it would have meet the cost of a few luxuries including a cheap holiday each year) but I don't see them playing a blame game as to how young millennium are benefiting from cheap mortgage rates due to their low term deposit rates.

Get over it - blaming boomers is just shifting the blame.

Funny - I try to make a point and then clearly have a boomer calling someone of a younger age bracket 'self-centered'! This is my point. If you're allowed to label those younger than you self-centered, I feel that I'm entitled to take an equal shot in return (unless the older generations want to be civilised and mature and set the example first? Unlikely...)

You can have 6% return on your term deposits if you want, but we'll probably need the housing market to tank as all those with debt won't be able to service their mortgage?

Or do you want to have your cake and eat it too? Most boomers I know do! (I'm not joking...most I know complain about low returns on savings but love the valuation on their property portfolio).

You can't be the cause of a problem and the solution. I.e. you can't have expensive houses and high returns on your savings....so which is it? Boomers willing to compromise?

Could you explain what I'm shifting the blame from with your last sentence? Your generation created the current economic conditions - I look to the central banks everywhere and they're all run by boomers. You have the power to change it, but bet you won't because you like expensive houses!

I actually think boomers are afraid that younger generations are starting to see through the self interest of the generations that come before them - and its central bank backed self interest - comes from the very top. You're not afraid are you P8 that younger generations are starting to see the reality of what is going on here are you?

IO

You raised the generational argument by dumping - and continue to dump on - boomers. So yes, your argument is self-centred from a millennium's perspective. My argument was that that the current situation is not just affecting millenniums but also boomers.

You probably have also read Obama's comments on Trumps chaotic handling of Covid - the single biggest issue Obama raises is that Trump's handling has been divisive.

Yes, we currently face - and have done so since the GFC - a number of issues that affect all and that includes both millenniums (and as I pointed out) also boomers. However, divisive arguments about "us" and "them" is not going to solve the current problems.

Yes, home ownership for the young is an issue and I have children (and grandchildren) so that issue greatly concerns me also.

However, this blame game - its all the boomers fault is rubbish. As I have already posted, the single biggest driver in house price inflation over the past decade has been low interest rates. Lowering of the OCR by RBNZ over the past 10 years has been for economic stability and stimulus reasons - as with any action it has had both positive and negative costs and consequences. It has encouraged investment in businesses, saved many businesses and saved jobs (including most likely yours); that is not about boomers but rather about "our" economy and "us". Yes, a negative effect for young has been house price inflation, for retired boomers the negative is a fall in term deposit rates.

Falls in the OCR was never initiated by and for boomers; it was about "us" - you and I.

The current Covid situation is not one we want; considerable amounts of money is being thrown about to lessen the consequences for all (including millenniums) and will be a future cost. Personally, as a boomer I stand to gain nothing.

Will future generations blame the subsequent cost of negating the effects of Covid all about protecting millenniums and that is not fair? Hopefully not.

In all this debate about "me" and "you" overlooks one very, very important factor - the appreciation of previous generations who have left considerable infrastructure for following generations. I know I look and appreciate the power schemes, the roading, the wharves, airports, railways, parks, public buildings including art galleries and museums, schools, national parks, . . . . . that my generation have inherited from my parents and grandparents generations. You need to do likewise.

Yes lucky we got rid of the National government as they were going to sell all of our property to foreign buyers - so you most certainly wouldn't be a National voter then based on above?

And by milleniums I assume you mean those pesky avocado eating millennials, not a few thousand years?

#boomernomics.

IO

For what it is worth, I have actually previously posted reasoned argument as why I intend voting Labour - and that is hopefully about Robertson’s claim of a reset of the economy.

It actually is not about nine years of National but rather a compounding result of Rogernomics competitive economic society following Muldoon interventionist philosophy. The obscene high salaries of CEOs, and the depressed wages of many workers can be traced back to the Rogernomics philosophy which underpins the 1991 ECA. I also see both selling property to FB and a lack of a CGT also as part of that.

This philosophy has especially led to the increasing divide. You appear to be a casualty of that divide.

And no, I am not into generalisations about lazy avocado-eating millennials; as mentioned I have children and grandchildren and I am impressed with their and their mates’ work ethics. I am also especially in awe of both their work and recreational skills; e.g. I see the extreme sports skills they posses which were not common in my generation.

There is a need for a reset of the economy just as we saw with Lange’s government following the Muldoon interventionist induced crisis. And I hope that is what we see that following this crisis.

However, this is about us - not about a divide between millenniums and boomers.

If you are going to focus on that you are going to miss seeing what the real problem is, what is the cause, and how best to fix it.

In the meantime this the game conditions so simply moaning and blaming achieves nothing.

Get over this fixation of this divide and the blame game.

Agree - we need utilitarian approach to resolving this. In the end I think it might be out of our control now - too much debt in the system that can’t be serviced and don’t think monetary or fiscal response will be effective.

I’m more worried about international conflict rather than generational if people feel left behind or are crippled under the debt load.

All the best P8 - I enjoy the debate!

Printer8 . I think you are looking at loan numbers for your figures rather than the aggregate of loans that make up most New Zealand mortgages. Particularly first home buyers.

Here's the formula:

Current house prices - unsustainable debt load = sustainable house prices

Rob how much do you think is reasonable for a home in NZ if they are too dear now?

Historical measurements of affordability would suggest house prices should fall by 50%.

Hmmm.

I think it's dangerous to go by historical norms whether you are a bull or a bear.

Not a believer of reversion to mean? Or ‘new normal’ now

I think it's dangerous to extrapolate bubble trends to the moon. Agree to disagree.

Geez if you are right then I will be able to get 12% returns on new buys.

Based on an income ratio. Currently they seem to be based on how much people can afford to borrow and service, due to a lack of supply, due to our increasing population.

Because the current system only functions with ever expanding debt. Deleveraging destroys money and any chance of inflation expectations. I wonder if the world will come knocking on our door to blame us for inflation targeting, yep it was lil old NZ that first came up with the idea of targeting 2-3% inflation - unfortunately they forgot to factor in credit creation For non productive asset purchases into the inflation basket.

"Issue as much liquidity as necessary! That will produce inflation and eat away at any debt created in the process."

Sounds good, in theory ( doesn't everything!).

But it's doomed to continued failure when we have an aging demographic; falling productivity; increasing and sustained unemployment and a globalized World in the process of the re-individualization of nations.

The era of waste, greed, fraud and living on borrowed money is dying. Its passing was inevitable, for any society that squanders its resources is unsustainable. Any society that makes private greed the primary motivator and priority is unsustainable. Any society that rewards fraud above all else is unsustainable. Any society which lives on money borrowed from the future and other forms of phantom capital is unsustainable.

We know this in our bones, but we fear the future because we know no other arrangement other than the unsustainable present.

The most zealously guarded power of government is the creation of money, for without money the government cannot pay the soldiers, police, courts and administrators needed to enforce its rule.

Once the government's ability to sustain its enforcement with money created out of thin air vanishes, the entire order vanishes along with it. The destruction of the value of central bank-created "money" is already ordained, for there is no limit on human greed and the desire to maintain control, and so governments will create their "money" in ever-increasing amounts until the value has been completely leached from the phantom digital entries.

The outlines of a better world are emerging, an arrangement that prioritizes something more than maximizing private gain and institutionalizing the corruption needed to protect those gains. We will relearn to live within our means, and relearn how to institutionalize opportunity rather than corruption designed to protect elites.

The Fed's essential role; serving the few at the expense of the many, under the cover of creating currency out of thin air will be repudiated by the implosion of the economy as all the Fed's phantom "wealth" evaporates.

The outlines of a better world are emerging.

(CH Smith)

ín the GFC -- we avoided mass printing and QE - and as a result performed way way better than our global competitors -- imported goods became cheaper for Kiwis - whiteware cars - -etc as the dollar strengthened -- despite worries about exporters - not only did they survive but they thrived -- with meat wine dairy kiwi timber all growing massively - not to mention tourism and the education sectors and Kiwis ability to travel globally -

Grant R = talks a lot about what a good position NZ is in regards to debt -- but none of that is his doing -- its all the result of the previous 9 years fiscal policy before he arrived -- which means our dept to GDP ratio was so strong -- as was the structural surplus he inherited but has worked hard to dismantle

huge debt issuance and QE will have to be paid for - NZ is not the UK / Japan /China or America - we can and will be allowed to fail and collapse - like argentina /brazil / iceland - the worlld will not bail us out or allow us the huge levels of debt --

there has never been a better opportunity for us to take our medicine on obscene inflated house prices -- reset the whole economy - finally focus on infrastructure and R and D -- and rebuild for the next 30 years not th last 30

So true, but unfortunately we've turned into a society who avoids any discomfort at all costs. And not just the economy, almost every area of life. People have forgotten life is a zero sum game, filled with struggle and no one gets out alive.

There is part of society that think its possible to have their cake an eat it too. They've been doing that and now wondering why they've got indigestion but don't feel guilty yet, in fact becoming more delusional and want more cake! But don't worry, the Dr can fix it and is going to serve them more cake...

It reminds me of that scene from Monty Python where the obese guy keeps ordering food until he explodes...that represents a society (banks, property investors) consuming debt, the restaurant the central banks...and I think we're approaching the 'f#$k off I'm full' but 'its only wafer thin' moment.

That is a good point. But we were relatively lucky in the GFC. In the UK that had to use austerity measures and also had to bail out banks. I hope we don't have those issues here.

Central banks have this dangerous notion that by pulling a bunch of monetary policy levers they can outsmart the boom / bust cycle.

However, the RBNZ has been dropping rates ever since the GFC to prop things up.

Kpnuts... I agree with most of that, but you need to Google our government debt chart over those 9 years you mention. And remember that Key was also selling the family silver while racking up that huge increase in debt. And household debt was also heading to the moon because house prices were encouraged to go the same way.

House prices rising were an issue well before Key got anywhere near the levers, and it was acceptable then because it made people feel richer even though they were being slugged 39 cents in the dollar for every dollar over $60K.

Agree GV27 - what pissed me off about Key was his stance of 'we're going to fix unaffordable housing' to 'holy shit getting people rich on paper with housing is actually quite a political hit, so lets celebrate how expenses our houses are, oh now I think the market has peaked, I'm out, off to sell my house to a Chinese buyer. later!'.

I went from voting National to actually quite despising what the party stood for - still quite like BE, but think what is left of the party at present is a bit of a joke with a few exceptions (and I'm not arguing that Labour are any better). I haven't decided who I am voting for this year yet (but probably not National unless there is a change of leadership/policies).

... and one fewer spy.

Echoes my own experience. Prior to that point I had only ever voted for National.

Same boat. You can't win. Missed out on the hugely oversubscribed affordable housing ballots that the Nats ran while Labour accused them of doing very little as they hyped Kiwibuild, and then watched Kiwibuild provide even fewer houses while people insisted this was somehow better than National.

During the TV debates I was screaming at the the set begging Bill English to offer an acknowledgement that house prices were an example of market failure that needed urgent intervention. They had the know-how and the financial nous to set up a decent state housing provider, even if it was just massively expanding the Axis programme. But he didn't. If they had done something, anything, then they would still have been in power, and I suspect a vast number of people would have been better off under his social investment approach than they would ever care to admit.

Instead we got what we got. Nothing has functionally changed, we're just seeing politicians ignoring a different problem (Kiwibuild) instead of the one it was meant to address (affordability). We've swapped people who were more than capable of actually doing something but didn't want to for people who talked about doing something but now either don't care or simply can't.

Some people seem to think that's a vastly better outcome. I remain unconvinced.

"During the TV debates I was screaming at the the set begging Bill English to offer an acknowledgement that house prices were an example of market failure that needed urgent intervention. They had the know-how and the financial nous to set up a decent state housing provider, even if it was just massively expanding the Axis programme. But he didn't."

You seem to still be under the illusion that bubble growth under National was an accident and not the goal. The National Party is an organisation that exists to further the interests of a tiny elite of locals, and the CCP. That's it. As soon as you understand it through that lens everything makes sense. It's your run of the mill banana republic setup. The middle classes with inflating houses are just there to make up the numbers.

And the bubble growth under the Clarke labour gov before that?? It’s not the parties that are the problem. It’s our monetary system, Nat and Lab just take turns driving the train.

Broadly I agree and I've said before that NZ is just a little beach ball on the ocean of debt so local policy probably could not have changed the overall direction of things. The difference is that the Nats actively poured fuel on the fire and bullied the population into doubting their own sanity if they dared to question the property cult. The argument that "both parties are the same" is patently not true in NZ's case.

National Party Founding Principles 1936

“To promote good citizenship and self reliance; to combat communism and socialism; to maintain freedom of contract; to encourage private enterprise; to safe guard individual rights and the privilege of ownership; to oppose interference by the State in business and State control of industry”

Sid Holland, National Party Founder

If ever we need those principles, it’s now !!

Speaking of communism: https://www.youtube.com/watch?v=VumEIYSQLyI

According to the leaked political poll 29% of voters were willing to overlook National being beholden to Chinese donors. 75 years today since VE day... I wonder what our soldiers would think of that Simon.

Tribalism over policies. To such an extreme length they're willing to overlook being beholden to a communist party...

I am probably voting with my feet....If only I could find out somewhere, what real money is worth.

Debt is so last year.

Every defence I've seen you make for National has been some variation of "But but but Labour did it too!"

I tend to make that point to people who think John Key personally invented every social ill this country suffers from and everything was just fine up to November 2008.

To anyone who wants to actually talk about history, I'm quite happy to talk about the many, many disappointing things National didn't do, had they actually wanted to.

"everything was just fine up to November 2008"

That's a bit of a strawman, no one is saying that. It's still not an argument for why it's all good that they spent 9 years actively making things worse for the average Kiwi, in particular young Kiwis, and lying through their teeth about it.

Thanks, I'll keep that in mind for when I'm actually arguing that it's all good. But if you're done lecturing me about strawmans and want to re-read what I've actually said, I think you'll find I'm not saying that at all. Unless this is some higher form of irony that I'm not familiar with.

Fair enough, happy to hand shake and accept we missed each other on the nuances.

Nice try at re-writing history kpnuts. The previous National Government inherited low to zero public debt from Helen Clarke's labour government. They then borrowed 60 Billion to fix Christchuch & the effects of the GFC....... So I would say that New Zealand's good debt position had very little to do with the previous National Government.

Zombie economy here we come!

At this point, given every economy in the world is doing it the thinking must be - what have we got to lose?

Last call for drinks folks. The bar is closing.

The aim of these commitments is to keep interest rates, and thus borrowing costs, low, to encourage economic activity. With a very active buyer - namely the RBNZ - in the market, it makes it easier for investors to sell government bonds. This pushes their prices up and yields down..

BNZ had this to say:

The RBNZ’s aggressive QE stance is NZD-negative as the Bank’s actions continue to drag NZ rates down, with falls to record low levels across much of the curve – NZ’s benchmark 10-year government rate (2031) closing down 4bps to 0.73% and the 3-year bond trading down to just 0.07%. The 5 and 10 year swap rates fell 2-3bps to record lows of 0.31% and 0.69% respectively. Many are beginning to question the RBNZ’s strategy here, given the overwhelming distortions it is generating in the market[my bold]. Link

When the RBNZ offers to buy these bonds via LSAP operations authorised RBNZ counterparty bank traders purchase them from the owners and credit them with savings deposits - bank IOUs. Thereafter, the traders sell the bonds to the RBNZ in exchange for reserves (IOUs) which act as an offsetting asset against newly created deposits for the bond sellers.

The minority rentier bond trading cohort can now reinvest, once again, in Treasury tendered bonds to front run the RBNZ's bond purchases for profit.

Unfortunately, no further bank lending is necessarily extended to the general population of taxpayers and their productive enterprises because they are not considered creditworthy in current circumstances, no matter how low interests rates plummet.

On market QE is simply a hand-out to the "registered participants"

As for off-market QE, how long before the "registered participants" jack up and refuse to participate in future

They need their daily injection

The only conclusion I can draw is that the effort to 'freeze' businesses, preventing restructuring or bankruptcy, will also delay our labor market restructuring so productivity will continue to decline. Consequently we should expect a low inflation environment until such time as businesses can resume normal activity.

You are seeing larger businesses remove 10-20% of their workforce as preliminary moves towards ensuring they remain solvent.

In many cases, the workers staying behind are on reduced pay with no firm assurances it will ever go back to what it was, and if it does, marginal consumers who were marginal on big-ticket items before aren't going to be taking the plunge. There is simply no model that fits this kind of change in retail environment in such a short time frame.

60 Billion QE? Here's a stupid idea, divide that by every NZer over 18 and give it to them. $16k each (very rough calculations). Now that's stimulatory!!! Tax it back out if things become too hot inflation wise. We'll have to pay it back anyway but this would see better outcomes for lower and middle class NZers than QE.

But that's not fair, the rich deserve more.

QE is monetary policy. It is an asset swap. You give me bonds. I give you reserves. You're not really any richer, you just have more liquid assets. Giving 16K to every NZ citizen is called "fiscal policy". And you are right, it would be very very stimulatory. That's cause fiscal policy works and monetary policy is far less effective generally.

Same thing overall though. Money is created and entered to the system then removed by “paying it back” both through taxes. Just the entry point, timeframe and beneficiaries are different

I like this idea.. And no, not just because the quote for a new roof came back at ~$16k.. lol.

Is that all... Must be a small roof!

That's an expensive roof. We get 100sq m roofs done around $5k corrugated iron, full warranty.

I'd assume thats before GST? Thats not a lot more than the cost of materials I priced up online, and then you have to add $2k of fall protection if you pay someone to do it. Considered doing it myself, but people keep telling me its much harder than it looks. Feel free to pass on the details of who you use.

$5k incl gst and edge protection and warranty.

Any chance you can send the name of the company thru to segid85962@inbov03.com?

20k for 130m2 in Northland. Got quotes from every provider up here.

Must be quite a complicated shape?

I do it myself so I know it won't leak.

Be under $6k for materials for coloursteel I reckon.

Not complicated. I know the materials are only 6k odd as I have a friend in the industry. Labour, h&s and profit make up the 14k. I understand it's the same more or less across the whole country. My roofer mate told me its just what they, the whole industry's in on it, and not to let the cat out if the bag.

"It’s important to note that Treasury (IE taxpayers) will eventually have to repay debt from the QE programme to the RBNZ. The RBNZ could technically write-off this debt, but this could have implications for money supply and erode confidence in the system."

MMT here we come. Who still has confidence in the system? I think if there was a viable alternative we would all jump ship pretty quick but alas, we are more or less forced to use fiat.

It’s important to note that Treasury (IE taxpayers) will eventually have to repay debt from the QE programme to the RBNZ. The RBNZ could technically write-off this debt, but this could have implications for money supply and erode confidence in the system."

Treasury will redeem the RBNZ's holdings of purchased bonds at par if they are held to maturity. The difference between the price Treasury issued the bonds at and what the RBNZ paid for them is a space for possible net losses.

Yes and no. Here's how you stop using Fiat today:

*Download toast wallet on your mobile

*Use easycrypto.nz to buy XRP and transfer in and out of your current account

It's not wide spread yet, but it is absolutely accessible and an extremely credible alternative.

I can see the advantages of crypto, I even tried to buy $2k of bitcoin when it was under $60 but that's another story.

The trouble I see with it now is:

-the government can outlaw it if it so desires. They just say its used by drug cartels, sex traffickers, cybercriminals etc.

-its too clunky a system to be used for everyday payments compared with say eftpos

-I am old school and so don't trust the internet much. Already many stories of hacking of exchanges or some such thing.

-there are too many competing cryptos (each with some supposed advantage over the others) so I figure most must go to zero.

-its way too volatile...I wouldn't sleep well if I had much in it.

- its probably a matter of a short time before a government version is rolled out that everyone will be compelled to use.

Can understand the apprehension. There's definitely a lot of unknowns at the moment.

But crypto is here to stay. And governments aren't qualified to deliver it. Did you see how much the ird spent just trying to update their website, and how awful it is. This is bigger than national govt.

MMT is a description of how the system is already operating, it doesn't need to be adopted or introduced, only understood.

This is death by a thousand cuts.

'The RBNZ’s Monetary Policy Committee (MPC) will almost certainly keep the Official Cash Rate (OCR) at 0.25%, having in March committed to keeping it at this level for at least a year.'

When they said they will keep it at 0.25% for at least a year, it always seemed to me that this statement was in regards to any potential increase from 0.25%. ie. they wouldn't INCREASE for at least a year.

Of course, the way it reads it implies it won't be changed, either up or down, for a year.

But things change, and they have quite drastically...

Looks like we'll have a race to the bottom with respect to currency...

Anyone have thoughts on where we might end up NZD/USD wise?

I hold most reserve currencies, will look to bring some back to NZD at some point...just looking for ideas about where people think we might be heading?

Our OCR 0.25% now looks very high. If we cut it down to -0.5% as some experts expect, we would be looking at somewhere between 0.50 and 0.525.

But again, U.S. and other nations might take some extreme measures balancing the rate back to around 0.6.

Sounds great. It's obviously very important that we as taxpayers do a whip around and give money directly to shareholders of Australian banks.

I want to know where we are going to end up NZD - AUD and on a personal level whether to move my aussie super across yet!

I'd keep Aussie super there in Aus if I was you.

0.58 for 2H I've seen from some Aussie banks. I'm holding on with the expectation that the Kiwi will fall.

Reporter: "Will the OCR be cut?"

Bank Chief Economist: "Hypothetically that is a possibility that in all probability should manifest in the aforementioned timeframe, yet as always there are concomitant factors indicating the exact opposite is also a hypothetical possibility with a similar probability of happening before or after the former possibility may occur."

Reporter: "So you're saying you don't know"

Bank Chief Economist: "It is not my job to not say that I know anything without any great conviction."

According to the government plan, OCR will become - 1.25 % before the end of this year.

Which plan?

I've been reading all of Ray Dalio's recent releases and its got me thinking that monetary policy no long matters.

You can offer debt at a lower rate but its like sprinkling water on concrete hoping to grow flowers. You need to fix what you're sprinkling water on first. There's a process that needs to be followed. You're going to need to break the concrete, find the soil, prepare it, then you can start sprinkling...any other order and it doesn't work. Or you can just point a fire hose at the concrete but you end up with a flood (inflation) but still no flower growth that you want (stagflation).

That's a mighty fine analogy

Inflate asset prices some more.

Cool.

They're seriously keen on a revolution aren't they.

We're all going to be millionaires - just like everyone else!

Exactly:

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link-pdf>

Every single recent monetary policy is just so short sighted it is actually becoming criminal.

are people really excited about inflation?

Do we all want our wages to buy less and less?

Inflation is deadly to wage earners and where do we stop, Asian wages?

https://www.zerohedge.com/markets/daily-briefing-may-8-2020

"Zimbabwean Central Bank Satisfied Inflation in 'Targeted Zone' of 10,000%"

Have been thinking that the minimum wage is going to be a distant memory in 12 months time. You'll be able to fill the back of a Ford Ranger with labourers from Papatoetoe for the cost of one current days pay.

Maybe imports without residency that don't want to go home, but not NZers

Basically if things go up in price and wages don't increase to match, businesses will likely sell less, potentially causing more business failures. The economy is a balancing act. One thing changes and it has knock on effects. I think NZs biggest problem is out borders may be closed for 2 years until / if a vaccine comes along and NZs economy had been so reliant on tourism. But this is something outside our control. We have to adapt to it. I see Disneyland China is now opening up in new post COVID world.

It takes two people working to buy a first home, it takes a lifetime of servitude to become a pensioner. ..in Lock-up.

It takes a Super Manager to flog a dead horse and a small business and a large tourist venture and keep an Airline running around the world, keeping safe isolation in the process. Not to be sneezed at. All will be well Andrewj, Weeeeeeeeeeeexr immune...from all Inflation. Print and be damned......buy some Fiats, spread the Word. Money talks.....Bubble Cars are the next big thing.....after Bubble Houses.

Mum and Pop say so...Tis Mothers Day tomorrow.....Fiat money is no good...but Fiat cars......perfect for her......God Bless.

(But cannot go out of Isolation Zone).

I think you're asking the right questions.

You should check out Jeff Booth. His basic thesis is that AI and automation are deflationary forces that eventually overpower all other inflationary forces by an order of magnitude, so we might as well get used to it. Basically the idea is that what happened with previous tech disruptions to the workforce (eg electricity) creating a whole raft of new replacement jobs doesn't happen this time because the tech in this case can not only do your old job better than you, it can also do the new job better than you. This is the short version: https://www.youtube.com/watch?v=w_w-Kij5mag

Full version: https://www.youtube.com/watch?v=F8lfLqnhuGs

It has always seemed counterintuitive to me when people say "housing costs should be x% of your take home pay." I don't really see why that should be a fixed percentage over time. Every other essential living expense has shrunk as a % of total income over the long run. That is basically what the mechanism of improving living standards actually is.

Since Great Recession in 2008, not even one central bank or economists around the world can predict right in terms of rising interest rates. After 2008 we need two persons incomes to buy a house, as one person wages is a thing of the past. Central banks continuously fail to recognise growing debt and inequality within our society. Coronavirus made it worse even further the inequality and becomes a new normal to our economy.

Exactlty:

When the government does everything in its legitimate power, and a great deal that isn’t, to create inflation so as to get out of deflation, the deflation wins. When the government does everything in its legitimate power, and a great deal that isn’t, to defeat inflation it didn’t see coming, the inflation wins.

What the thirties, the seventies, and the 2010’s all show is that during times of serious imbalance authority is extremely limited; what authorities want is immaterial next to what little they can do. The forces gathered just beyond the horizon of awareness (shadow money, in our case) too powerful. Competence is a major part always lacking. Link

Only negative interest rates can restore the confidence in consumer demand in a sagging economy for if the consumer ( always a market maker ) does not come to the market , the sagging market would remain at standstill. The sooner we learn to live with negative interest rate in a borrowing nation like NZ , the better it is for everyone .

how can you get negative interest rates? why would anyone lend? You would need pristine collateral or you would never get a loan.

Yes. This is exactly what has happened where it has been tried in the real world.

Landlord?

Hit the nail on the head.

https://www.stuff.co.nz/timaru-herald/news/121462202/hermitage-hotel-cl…

Some will, some won't, some do, some don't. Some day, some way, we will be Paradise...again.....

Billionaires only, need apply.

I hear talk of negative interest rates a lot lately...

Can someone explain this to me? How would this look to the layman?

In terms of borrowers.. you pay back less than you borrowed. Eg, million dollar mortgage over 20 years, pay back a total of say $960,000 (depending on how negative the interest rate is.

In terms of lenders, you get back less than you lent. Or if you have half a brain you don't lend (to the bank in the form of deposits) , you open a safe deposit box and keep cash or precious metals, crypto.

But who is lending money out, to then get less back than they started with? Am I missing something? Wouldn't it be better just to stick that cash in a safe?

err, that is exactly what I wrote is it not?