A survey the Reserve Bank watches very closely when making interest rate decisions has recorded record low expectations of future inflation.

And expectations of unemployment have rocketed.

And expectations of house prices over the next year have reversed from an expected 5.65% gain just three months ago to now a drop of -5.49%. Prices are expected to recover in the following year, however.

GDP is seen as being down nearly 5% over the next year before recovering the following year.

The RBNZ Survey of Expectations is a New Zealand-wide quarterly survey of business managers and professionals. Nielsen conducts the survey on behalf of the Reserve Bank. Respondents are asked for their expectations of future outcomes of a range of key macroeconomic data. This survey was conducted towards the end of April, so captures much of the impact of the lockdown.

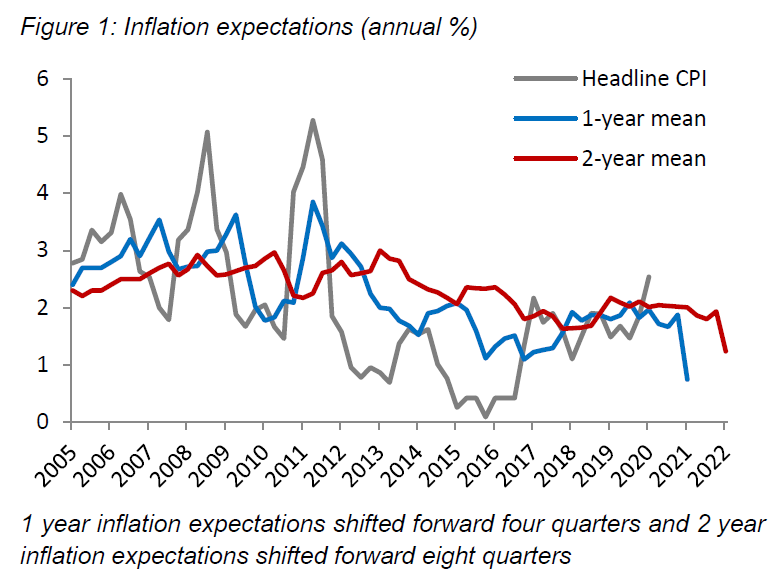

The most closely watched results are those for inflation expectations. And in the latest quarterly survey these expectations have just tanked compared with three months ago as the virus-led economic crisis has become fully blown.

Survey participants now see a rate of inflation in two years time of 1.24%, down from 1.93%, while the drop is even more extreme for the next year. The one-year out expectation is for inflation of just 0.74% down from 1.88% in the last survey.

Survey participants see unemployment a year ahead of 9.41%. This is up from 4.26%. The two-year ahead expectation for unemployment is 7.05%, up from 4.36%.

The RBNZ pays close attention to this survey. In the past if this survey has shown a big shift in inflation expectations then the central bank has responded with interest rate moves.

Of course, that won't happen this time as the RBNZ has already said, after slashing the Official Cash Rate to 0.25%, that it will leave it there for a year (although there's growing expectations that at some later date the RBNZ may drop the OCR negative levels).

But right now all eyes at next weeks RBNZ Monetary Policy announcement will be on whether the bank increases the amount of quantitative easing it does, from the already announced $33 billion bond buying programme.

A common expectation is this level of purchasing will be increased to perhaps $60 billion - and the latest survey results tend to back up such a course of action.

Clearly businesses are pointing for the RBNZ to keep providing the stimulus.

And, indeed, as one commenter on this article has already noted, this survey will likely add further fuel to speculation that the RBNZ will look to employ a negative OCR at some stage.

Here are some of the key details in the survey:

- Inflation expectations for one year ahead have decreased since last quarter’s survey from a mean of 1.88% to 0.74%.

- The previous low of 1.09% was reported in Q1 2016.

- Expectations for two years ahead decreased from 1.93% to 1.24%.

- The previous 2 year ahead low of 1.60% was reported in Q2 1994.

- The mean expectation for the five year ahead inflation rate decreased from 1.97% to 1.80%.

- The mean expectation for the one year ahead unemployment rate increased from 4.26% to 9.41%.

- The two year ahead expectation increased from 4.36% to 7.05%.

- House price inflation to fall one year ahead 5.49% before rebounding in two years’ time by 3.23%.

- GDP to fall 4.87% one year ahead before rebounding in two years' time by 3.21%

41 Comments

Given that the RBNZ take this survey seriously, it raises the question as to whether it adds impetus to the idea of taking the OCR negative.

These bankers are a little bit thick quoting figures to 2 decimal places. I would think the margin of error in these type of estimates is a little larger than 0.005. (Much, much larger in fact)

Really if their understanding of numbers is at this level we are in the shite.

Oh they definitely know, they're just trying not to startle the horses.

interesting when you think of 160 billion on deposit that was once earning 10 billion now going to earn next to nothing, probably along with share dividends and other investment. That's like taking out Fonterra x 2, we need to get back to where people can pay a decent amount interest again or we are toast.

When the govt announced small business loans the other day everyone here was freaking out over zombie companies. What they don't seem to realise is that we have an entire zombie industry already. The real estate sector has been zombified since the GFC - without cheaper debt, higher house prices and tax rorts it immediately implodes and takes the rest of the country with it. Unfortunately the plan seems to be to double down. But the RBNZ can't 'create' demand, it can only pull it forward from the future - the total doesn't change but the curve becomes a higher peak with a much more precipitous drop on the other side of it.

Nothing can be fixed until that gets fixed.

" people can pay a decent amount interest again" 'people' or banks Andrew? The people have been paying interest, albeit relatively low rates while the banks haven't been paying any. And those low rates have been used to market cheap money to get more and more into debt, and now as we know that approach will bite as many lose their ability to pay even the low interest rates. Really the banks have been cruising on easy money for a long time but as many have identified before their approached carried some significant risks.

Hmm. House prices down 5.49% doesn't provide much relief to us FHB, considering my area has risen almost 30% in the past 3 years.

It's frustrating when these expected home value falls put us where we were 1 year ago.

Wouldn't read too much into that estimate, it's likely to be at least 8-10%, and more in some places/markets.

Hopefully the government demonstrates how ineffective they are in controlling house prices so the market takes us to where it truly sits.

Until we know where this pandemic goes everyone is just guessing.

Hey Since when did any govt control house prices. Always comes down to indivduals desire to aquire.

Well, isn't the RBNZ technically part of the branches of government? And they've been pushing up house prices since the GFC by dropping rates. In addition, when even they began to realise it might be a problem and asked for tools to enable them to stimulate the economy without blowing asset bubbles, Bill English refused them a DTI tool that might have enabled it. Not to mention John Key trying to turn NZ into a tax haven and dragging his feet on anti money laundering legislation.

Thus you have both RBNZ and the legislature perpetuating house price rises. Feather-bedding some folks' wealth at the cost of young and old savers.

I'm willing to eat my hat if house prices don't drop by 10% and my best guess based on previous recessions in other countries is 40% but it could easily be worse than that. The bottom will hit sometime late next year but then littleor no change. For example after the 1929 recession there were house prices and section prices in Florida that did not recover for about 50 years.

My hat is not edible - remind me next Easter and I'll post a link to my eating it.

And it doesn't really matter what you, I or Blind Freddy think of the future of house prices in NZ.

It only matters what the lenders to facilitate the transaction think

I wonder what they'd say today to anyone who wandered in and said they'd agreed to pay 5.49% less than the current owners paid last year, and "Can I have some of your money to buy it with please?"

I'll whip you up a batch of homemade feijoa chutney to go with that chewy hat of your Lapun. House prices in NZ hardly blinked post gfc and I don't see much changing even with covid to cause major price drops. Main reason being kiwis are indoctrinated to put their money into only housing assets, so they by nature very rarely abandon their one and only asset class for any other asset because in their minds there are literally no alternatives to decamp for. Having said that, it is going to be interesting to see if any of the multiple suspected money laundering property purchases that occurred in that foreign buyer wave around the middle of the last decade end up hitting the market as operators look to free up some cash for further....activities.

What money? Locals don't have money, they have debt. The 'money' gets created when they use it to buy a house.

Ive been tracking trademe residential listing numbers since halfway through lockdown and they are rising, will be interesting to keep and eye out see if they skyrocket. Obviously there will be more as we move out of lockdown but good to keep an eye on them as the months pass.

There was a guy on here tracking a few items including 2nd Hand Ford Rangers and he was seeing a bit of movement.

I'm tracking baches on a couple of sites, I think being a major disposable item they will really highlight issues. Normally sales are quiet going into winter. I have noticed auctions have been discarded completely for fixed prices.

Auctions went the way of the dinosaur about 2 years ago. I tracked all property listings in the country, Auction listings used to make up > 50% of all listings, last I looked they were < 10%.

Percentages interest and amuse me. compounding interests and amuses me.

Percentages need reference to a starting point and how the timeframes are used. A note about the absolute number associated with them is often left out.

$700k house goes up 10% in one year = + $70,000 = $770,000. Goes up another 10% over another year = + $77,000 = $847,000

$847,000 house goes down 10% in one year = - $84,700 = $772,300. Goes down another 10% in another year = - $77,230 = $686,070.

So your $700,000 house that went up 10% per year for 2 years and then went down 10% per year for 2 years is now worth $686,070 or $13,930 less than when you started. Maybe no biggie. Maybe it is. But without the absolute number probably overlooked.

Most people that hear something went up 10% per year and then down 10% per year think they have what they started with.

So reverse compounding is more to be feared than compounding? How about you repeat the above exercise with a $500k mortgage on that $700k house assuming a stable interest rate and show the debt:equity changes. It could be a more break even exercise than it looks

More Stable.? I don't think so.

He started with 200K equity and finished with $186,070

Thats a 7% loss in equity over the time, the outgoings (principle and interest) being roughly equivalent to rent over the same time.

Not that simple as there would have been principal and interest being paid off over that two years. It would be more like a 6% drop in equity, not the on paper 7%, which is 14% less than the simple calculation. Another interesting percentage

"the RBNZ to keep providing the stimulus."

What exactly has the RBNZ stimulated with its misguided monetary policy interventions?

Nothing of real value to the economy, that's for sure.

Their interventions can at best be described as a bail-out of the speculative aspects of our economy. But stimulus? No.

I'm not sure if CPI will fall as much as people anticipate. A lot of substantial items, like food, actually seem more expensive while fuel costs have largely remained flat.

Spending will fall a great deal when layoffs kick in and home prices in six months when loan "holidays" expire.

Yep, those CPI forecasts will prove to be woefully inaccurate. Hell Pizza a great example, recently raising prices in a supposedly deflationary environment. Every social distancing measure adds frictional cost to the economy in terms of time and productivity. Cafes for example will have to raise prices to make up for the reduced throughput.

They might be able to pull the wool with their CPI computation methods, but the reality is the essentials of life will become more expensive.

It's the inevitable result of thinking that pumping money into an inoperative economy is a viable strategy. History has shown us a thousand times that it isn't. We are in stagflationary hell already.

Money printer goes brrrr.

The crooked and unelected RBNZ will stop at NOTHING to ensure house prices don't drop to realistic levels.

It's important to protect a few folks' money vehicles. If it takes sacrificing old pensioners and young savers to do so, well their sacrifice is one we're prepared to make!

5.5%. Ah well there's no sport on, I guess we will have to settle for RBNZ vs Reality.

@TAB - listening?

Hell you don't even need to place a bet to lose money on this one...

We might be facing a few supply constraints out of China - clothes, electronics, tooling - in the near future. If China has a revert to authoritarianism period the world's factory stutters and slows down. Then our inflation switches from being demand to supply driven and the models the RBNZ currently employs are probably useless. It is possible that inflation could hit double digits by 2021.

I wouldn't be so sure. Chinese factories whirring back to life to produce for... who? Their consumers are in lockdown. So they are building inventory.

Sure hope so or as someone said on this medium, expect $400 toasters. Ha

I think that'll show up eventually as the supply chains fully decouple but that will take a while. There are temporary disruptions to supply chains and the longer term decoupling/deglobalisation/relocalisation of production. The first I don't think will be as inflationary as people are expecting but the second will.

Please don't buy the Chinese toasters. You'll just have to buy another one in a few months after it breaks.

If it's like the one my parents had, they may have bought it soon after they were married but we were still using it 25 years later.

We are still using a toaster my grandparents received as a wedding gift. Things really were well made in time gone past.

This is what I struggle with. Massive global money printing coupled with less and less produced surely must lead us to inflation?

Any got the answer to this conundrum?

Asset prices inflate. Goods measured in the CPI don't. Monetary policy has never affected the price of a bottle of milk at the supermarket. The only conundrum is why anyone thinks it would.

The other conundrum is whether they really think it does, or whether they are simply happy to inflate asset prices given their place in society.

It's funny how the inflation, or even hyperinflation of house prices is overlooked or brushed aside (with respect to CPI) on the way up, but if there's even a suspected projected decline of 5% then suddenly the words "house prices" and "inflation" find their way into the same sentences at the RBNZ and government level.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.