ANZ New Zealand CEO Antonia Watson says the growth of housing lending as a percentage of the bank's overall lending isn't a problem, but she would like to see more investment confidence among business owners.

ANZ NZ, the country's biggest bank, posted an 18% rise in interim net profit after tax to $930 million on Wednesday.

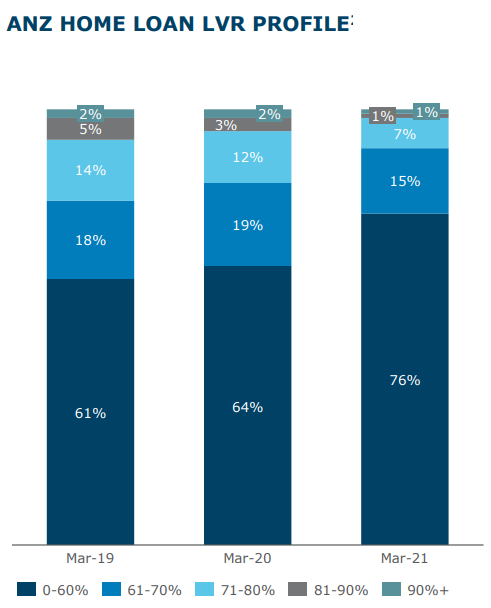

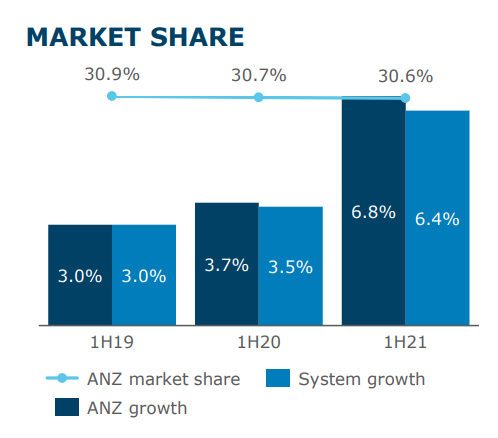

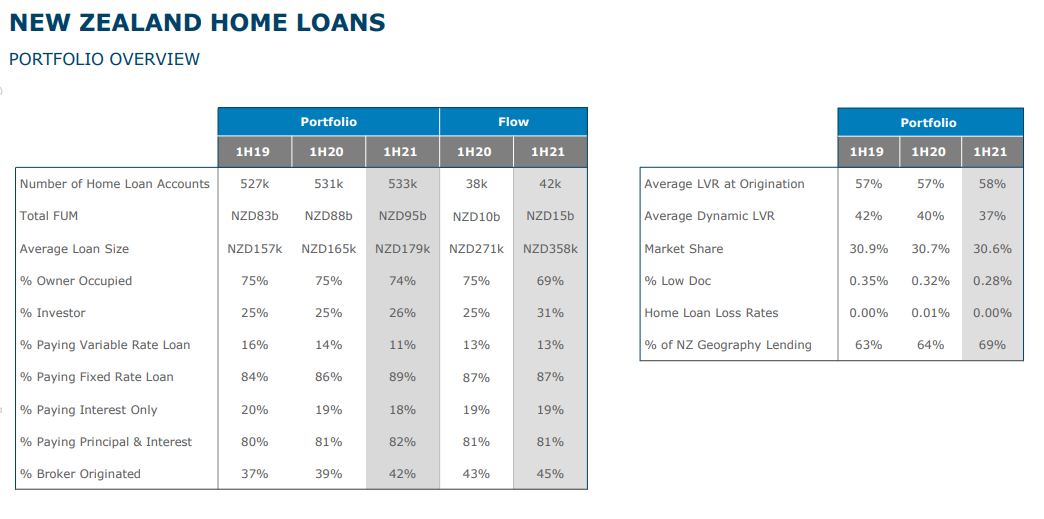

Figures released by parent the ANZ Banking Group show housing lending as a share of its total NZ geography lending at 69% at March 31. That's up from 64% a year earlier. Total home loans were up $7 billion to $95 billion, albeit ANZ's NZ market share was down 10 basis points to 30.6%.

Asked whether this sort of increase in housing lending, as a percentage of the bank's overall lending, was sustainable, Watson said it's not a problem but she would like to see more activity in the business sector.

She said ANZ NZ is doing business lending, but businesses are in some cases using alternatives such as debt capital markets. And Watson doesn't believe historically low interest rates are driving decisions.

"Businesses are doing well and I think you'll hear that from others as well. But two concerns we hear are on supply chain and labour shortages. So ... if we get vaccinated and [have] the ability to open the borders, [that] may help with that [business] confidence as well," Watson (pictured above right) said.

'I'm not going to turn them away'

Under pressure last October, having removed loan-to-value ratio (LVRs) restrictions and seen the housing market take off, Reserve Bank Governor Adrian Orr said rather than reining themselves in "the [banking] industry always just wants to have it done to them." Interest.co.nz asked Watson about this comment, and why banks can't or won't rein in their housing lending.

"If someone comes to me with a good deposit and wants to buy themselves a home, I'm not going to turn them away. What I am going to make sure is that they've got a decent deposit and I've got some equity and some protection in their loan. I'm going to make sure that they can afford to pay a higher interest rate because that's always one of the risks that interest rates go up and your serviceability gets different. So we make sure customers can pay around 6%. And the other issue is often losing your job, so we also have conversations about income protection insurance and that sort of thing," Watson said.

"So I see the need to make sure our customers know what they're doing, that they understand they've probably got a bigger debt than they've had in the past in dollar terms, and that they're also positioned to be able to pay it off. And understanding that being able to pay it off as quickly as they can is a good thing for them. So that's the way that we do it. We do everything that we can to put our customers in the best position possible when they take out that lending."

ANZ NZ increased deposit requirements for investors to 40% in December, ahead of the Reserve Bank reinstating LVR restrictions on low deposit lending.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

43 Comments

"If someone comes to me with a good deposit and wants to buy themselves a home, I'm not going to turn them away."

Sounds like banks are wanting to be a law unto themselves and with defy the central bank and government if push comes to shove. Given that these are foreign owned entities with such a cavalier attitude, we must now be very careful. Now is the time for tighter regulations and greater capital requirements. We don't want a 'cowboy culture' developing, particularly when it is NZ's economic future at stake and we are on the hook for the bail-in's and the bail-out's when things turn ugly.

Nice straw manning.

"If someone comes to me with a good deposit and wants to buy themselves a home, I'm not going to turn them away."

1 : It is not someone but everyone ( may be a little bit for business on side) is comming for housing loan

2 :, Deposit - It is FHB who needs hard cash for deposit and investor can use their equity and with such a gain - even 40% is no problem deposit is no problem.

3 : Why would any bank turn them away specially in NZ only economy is housing economy

4 : Knows that have rbnz and government support - gurantee which is missing in business.

5 : Even for business loan first step and right step is first to get house loan and than to use equityfor businessloan.

If anyone has any doubt, why first priority should be housing loan can see the resistance from Mr Orr to contain the ponzi - comming out with silly reason and excuses that are so hollow that anyone can see through it but Mr Orr who is so blinded by his faith to support speculative demandto support NZ economy, only mantra for success known to Mr Orr.

During the GFC, houses devalued. Largely due to banks unwillingness to lend at the old criteria. But it was a great time to buy if you were qualified to do so.

Hi Antonia,

TTP here. Show me the colour of your money, please.

TTP

Tom - I agree and would suggest best monetary tool to reduce house price growth is imposing quantative credit guidance on banks to control lending by banks. As noted by Philip Soos on Twitter recently, its removal by financial deregulation (in the 1980s) is the largest single cause of runaway household debt and house prices. See also Richard Werner you tube video and book Princes of the Yen.

Interesting comment regarding income protection insurance...has anyone been required to take this out when acquiring a mortgage?

I was required to get mortgage protection insurance when I took out my first home loan (at 95% LVR) in 2001 but not income protection.

Yes Ive heard of requirements to have mortgage insurance for high LVRs but not income protection

Mortgage Repayment Insurance is just another form of income protection insurance. And both can have redundancy cover add ons with some insurers

Ridiculous suggestion as IP doesn't usually cover redundancy which is a common reason for job loss.

Mortgage insurance in Australia is very common though.

I am surprised it isn't common in NZ. I think both borrowers and banks could become exposed if there is a correction. I also can't believe that in NZ we can't lock in 25 year mortgages, to secure these low rates, like they can in the US. They can even get 30 year mortgages at these rates. What if interest rates are in double digits in 10 years? Some people will struggle to afford that, but guessing some will move to interest only.

History repeats, and people need to look at past cycles. NZ isn't any different to other countries and we are just a cork on the ocean when it comes to the global economy. 20 years ago people wouldn't have imagined that most finance companies would collapse (about 50 of them) , and NZ savers would lose billions of dollars in thme.

A gung-ho attitude towards lending to the housing market. Never mind if the deposit come off equity on another property and the borrower can only afford an interest-only loan. In other words, even a man of straw could borrow to feed the housing ponzi

ANZ's shareholders must be furious.

https://www.nzherald.co.nz/business/anz-half-year-profit-up-18-per-cent…

I find it extraordinary the level of broker originated mortgages.

Short story

18% profit increase during a crisis. We're onto a good thing and won't step back. Housing crisis/homelessness, what crisis, not our problem.

Good story on RNZ about Axles family and how they came to be in tolaga bay.

I thought residential property investors were business people? No problem then right as property investment is booming.

"Watson said it's not a problem but she would like to see more activity in the business sector"

Who in their right mind would take the risk of taking out a big loan to start up a new business in this type of difficult business environment; where there are still a plethora of border restrictions with so many uncertainties about the future. Definitely not tourism & hospitality.

The only loans that will be taken out will be for real estate. Period. NZ has always been known for that, along with the stigma that housing is always the best investment (especially when you can't get the same yields anywhere else right now in a low interest rate environment).

Interesting to see the 0-60% LVR cohort grow substantially.

Need help to understand something: if you're an Owner Occupier with a mortgage-free PPR valued at $1m and you use $400k of (on paper) equity to buy a $1m investment property with a 40% deposit (the equity), does this mean you have a 60% LVR?

My understanding is that you would have a 60% LVR on your investment property but now also have a 40% LVR on your PPR.

Banks consider your overall financial situation and securities when considering lending, however when considering LVRs then each property and mortgage is considered separately.

Note: From a borrower's perspective, one would want to ensure that when leveraging to buy an investment property one would want a LVR at a level on the investment property to ensure that they are not paying the "low equity premium" and, as a low equity borrower, avoid a rate which is usually 1% higher than what they advertise.

$1m loan and $2m value of security = 50% LVR.

Or borrow $400k on home (40% LVR) and use as deposit on renter for 60% LVR.

HG

Yes to the later.

From my experience separate mortgages (loans) and separate securities - as recorded on each of the property titles. In the example given, they would not be content to hold a security of $1million on one $1million property.

. . . . although separate mortgages and securities, they will come looking for everything if one defaults on either.

I have a mixed portfolio of rentals and owner occupied. I deal with the banks on a portfolio LVR basis but I could see that there would need to be some manoeuvring if LVRs were tight.

Eg. $1m owner occupied with $400k Mortgage. Want to buy $1m renter need to borrow $400k on home (LVR now 80%) to use as deposit for renter (60% LVR).

In respect of structuring you would load up the debt on the renters for deductibility purposes (although that is ending as we speak) and the LVRs were still calculated on the value of all homes offered as security. So in the example you would want the full $1m on the renter to get the interest deductibility but the use of the home as security would give 50% LVR keeping RBNZ happy. I recall reading in RBNZ document that this was all good.

Accordingly, 8014's 60%/40% LVR would have been bad tax planning pre the new changes regarding interest deducibility for rentals.

HG

"you would want the full $1m on the renter to get the interest deductibility but the use of the home as security"

Agreed; for IRD as to interest deductibility in this example one would appropriately argue that you borrowed 100% to buy the property . . . and for properties purchased prior to 27 March still some four years until it is finally phased out.

However, not sure how bank would record the loan as they are restricted by RBNZ LVR provisions (20% of lending over the LVR limits?) so they are unlikely to record the loan as a 100% LVR.

That's my point, the banks would record it as 50% LVR as the loan is $1m and the value is $2m (home and renter). Well that's how Kiwibank, ANZ and Westpac recorded my LVR. The calculation is not limited to the property over which the loan is recorded as it can include other properties provided as security under a mortgage.

See para 4:

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/regulation-and-super…

8014

In response to your observation "Interesting to see the 0-60% LVR cohort grow substantially".

It is particularly interesting as it is counter to the fact that for much of the year LVRs (other than bank self-imposed LVRs) were not in place. Seemingly RBNZ removal of LVRs did no lead to a rush of high LVRs by ANZ.

In the example you provide, leveraging off your PPR, then the mortgage of 60% LVR on your investment property and the consequential mortgage of 40% LVR on your PPR the bank would seemingly record two loans with LVRs of 0-60% for RBNZ purposes (and in doing so possibly avoid you facing a low equity premium and interest rates).

You've described a safer way to borrow an investment with a split loan structure. So you borrow 400k deposit against your own home (if you can but not likely at the moment), take that to another lender as the deposit and borrow the balance 600k being 60% so then you're 100% financed on the rental and 60% on your own home and property isn't cross secured.

Otherwise you leverage up with the same bank with your own home and rental but will be cross secured.

Theoracle

Possible, but a couple of things

- your bank might not be happy to lend you the $400k to take and do business with another bank, and they are not obliged to lend to you; and

- if you do default on one loan and even it is isn't "cross secured" I feel that they will still come chasing you through bankruptcy proceedings which would negate that and they would have every reason to act at the earliest.

Personally, I have always found it advantageous to deal with just one bank as they tend to look after you more. I have never had any financial difficulties but suspect if I did it would be easier working with just one bank.

If you borrowed $400k on your home and paid it as a deposit on your renter wouldn't your LVRS be 40% home and 60% renter? How are you getting 100% renter and 60% home?

Thanks everyone for the responses.

Yep. ANZ Group's share price up 74% over the past 12 months. The housing bubble is a wet dream for those who love bank stocks. And bank stocks are pushed hard across the Tassie because of the fixation on property and the franking credits bonus.

Of course Watson doesn't speak about the ANZ's mortgage lending and its relationship with expanding the money supply. That same money supply is the inflation piece that people don't really or 'kind of' understand. She's a favorite of Lord Key.

And Watson doesn't believe historically low interest rates are driving decisions.

Hmmmmm...

While interest rates are falling it is inevitable today's discounted present value of associated future cash flows will rise for both assets and liabilities. Hence these cash flows will be capitalised upwards by borrowing from the future - bank loans facilitate these actions in respect of asset purchases.

Furthermore:

We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates.

When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

And just in case Watson doesn't get it:

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1….

"It's very well secured [by the borrower's property], so we don't have concerns about it."

INCOME ALERT! Who can realistically afford income protection insurance ....

On the other hand a house can generate Accommodation supplements all by itself ... ahh it would nice to be a bank

I remember voting for John Key after he railed against Working for Families as "communism by stealth" to address exactly this sort of taxpayer subsidising of banks. But he didn't address it, only grew it, then went to work for a bank. Disappointing.

So it's not a problem but it is a problem?

Profitability ... which pays wages ... thats the problem

just not for the banks .... yet

https://consciousnessofsheep.co.uk/2021/05/06/a-crisis-of-profitability/

Just read about burger king on stuff. Perhaps the banks are finding it to hard to find ripoff overseas equity funds with can't lose deals to be able to fund SMEs.

But what happens when the party ends. All of these things have cycles, and if this is truly a bubble, it could pop. Already wages for many will be frozen, yet interest rates could rise if inflation rises. Real inflation is rising rapidly, as per Warren Buffetts analysis. This is also a worrying video if things go bad https://www.youtube.com/watch?v=RYfmRTyl56w&ab_channel=BloombergMarkets…

More business borrowing?????

Notice she didn't say more business lending. It came across as well no business wants to borrow..

Are banks only stress testing borrowers at 6% these days? I thought 8% was seen as a more normal interest rate during normal times?

I can't see them even doing that. When current rates are meaning 30% of income heading to mortgage, 60% seems unreal.

Dear Antonia Watson,

I have a business but no house, please lend me some money for my business.

And this is why I left ANZ. 7 figure profits, and no help avaliable. Sooo so supportive of business... as long as we have hold over non business assets.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.