Credit rating agency S&P Global Ratings says if strong house price increases continue in New Zealand, so will the risk of a "disorderly correction" in house prices.

S&P recently revised its Banking Industry Country Risk Assessment (BICRA) economic trend for NZ to negative from stable mainly due to strong house price growth. It says this could be a bellwether for its outlook on other countries.

"We note a recent re-intensification of economic risks in New Zealand, a country by global standards barely affected by COVID-19. In New Zealand, economic trends recently reverted to negative from stable because of soaring house prices. Instructive is that this action reversed our previous move of economic trends to stable, from negative, only a few months prior," S&P says in a mid-year global banking country outlook report.

"Residential real estate represents a material share of many banks' loan books and house prices have been increasing strongly in many banking jurisdictions. Low interest rates are fuelling housing price increases. In some jurisdictions house price increases are contributing to economic imbalances that may hit bank credit."

"A case in point is our recent action in New Zealand where, on June 25, 2021, we revised our BICRA economic trend to negative from stable mainly due to strong house price growth. While house price growth in New Zealand has been exceptionally strong, our action in New Zealand could point to the possibility of negative changes in other jurisdictions where it becomes challenging to reconcile house price increases with ongoing banking sector stability," S&P says.

S&P's BICRA is designed to evaluate and compare global banking systems. BICRAs are grouped on a scale from 1 to 10, with 1 being the lowest-risk banking systems and 10 the highest-risk. S&P has NZ at 4.

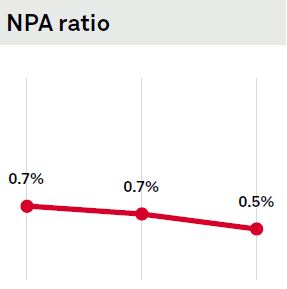

This, Barrett says, could result in higher credit losses in the longer term. S&P's NPA ratio chart to the right shows non-performing NZ bank assets (loans) as a percentage of banking system loans. Left to right 0.7%, 0.7% and 0.5% show the actual 2020 figure, S&P's 2021 estimate, and 2022 forecast.

"Unprecedented house price growth of 30% in the past 12 months is exposing financial institutions to rising economic risks, in our view. While the government and the regulator have taken various actions to mitigate the risks to financial system stability from the resurgent house prices, these initiatives have so far been less effective in restraining house price inflation than we previously anticipated," says Barrett.

"Risks remain around the funding profiles of New Zealand banks. The banks' significant dependence on offshore short-term borrowing, the country's persistent current account deficits, and its exposure to fluctuations in commodity prices, all make New Zealand vulnerable to external shocks."

With the Westpac Banking Corporation having recently reviewed its ownership of Westpac NZ and decided to keep the kiwi subsidiary, Barrett says NZ bank subsidiaries will remain a core part of their Aussie parent groups.

"This will support the credit quality of these New Zealand banks, which account for over 90% of the industry's assets."

She goes on to say that S&P's "base case" expects successful regulatory and government actions to curb house price growth.

"Measures include the reinstatement and subsequent tightening of loan-to-value [ratio] restrictions, a tax-driven housing policy package, and potential introduction of debt-serviceability restrictions in the coming months. If this is not the case, downside risks to financial institutions will continue to rise with the rapidly increasing house prices in the country," says Barrett.

Property data company CoreLogic said on Friday the NZ housing market may be at a turning point as affordability pressures, mortgage lending restrictions and changes to tax rules for residential investment properties start to bite. S&P currently has "AA-" credit ratings with a negative outlook on ANZ NZ, ASB, BNZ and Westpac NZ. See credit ratings explained here.

Meanwhile, S&P notes NZ is faring better than most advanced economies.

"We forecast real [NZ] GDP growth to reach 4.6% in the year ending Dec. 31, 2021, driven by consumption and investment, including residential construction. In addition, timely and coordinated monetary support from the central bank has alleviated bank funding and liquidity risks, in our view."

48 Comments

Don't worry guys. Adrian and Jacinda will bail out all banks with tax payers money. Keep buying houses and spectate more. What a ridiculous situation.

Not before they bail-in my unsecured house deposit (which is currently losing money in an ANZ acc)

Honest question: do readers here consider Kiwi Bank to be less of an OBR risk (to depositors) than any of the Big 4 Aus Banks?

I've got a sizable deposit being inflated away in a normal savings account (stopped bothering with TD's when the rates fell below 1%). I don't think the govt or RBNZ would ever let any of the big banks fail. If the housing market is too big to fail, imagine what they'd do to prevent banks from going bankrupt. Running a bank is a one-way bet. Socialise the losses, as they say.

I went Kiwibank with 1/3rd of our TDs. Why, spreading risk and the naïve belief that a bank developed at the bequest of a politician (Anderton) and backed by Clark and Cullen, with Gov as a principal share holder would be more likely to be bailed out. Moving out of WPAC (they p@sss me off) and going to Kiwibonds.

The new law allow banks to use depositors' money to bail themselves. If there's a banking crisis in NZ, it won't be the government doing the bail out, the government will likely only step in if depositors' money ain't enough.

But doesn't someone has to pay it back? I would think the government will rush in a governemnt guarantee like they did at the GFC, if banks start to get a run on them again

I used to work with KB. Unlikely govt would let them go bust but just as much a contender for OBR as anyone. No carve outs for OBR.

Better to send some cash to Aus domiciled banks if you have an account there as 250k per bank deposits are guaranteed in Aus.

https://www.rbnz.govt.nz/regulation-and-supervision/banks/prudential-re…

kiwi bank only has a fitch and moody's rating. Maybe S&P didn't want to rate them.

For S&P, AAA > AA+ > AA > AA- > A+ > A > A- > BBB

Spectate or speculate? There's quite a difference

The thing about a spiral is, if you follow it inward, it never actually ends. It just keeps tightening, infinitely.

I think it's not Orr's fault, a mentally challenged person never know what is the problem with his decisions.

It's the responsibility of the guardian to control that person, before he take nuisance to next level. But as a country we are still not sure house price is under mandate of RBNZ or not.

That's only true if the spiral is an infinitely thin line.

What are they talking about?

Risk to banks is 0%. Gov't, be they Labour or (looking unlikely right now) National, will step in if they get the wobbles and bail out anyone and everyone.

Risk to banks is 0%. Gov't, be they Labour or (looking unlikely right now) National, will step in if they get the wobbles and bail out anyone and everyone.

Correct. Zero risk to banks, except a prick to the ego. Labour and National are both cut from the same cloth. No difference between them regarding the monetary system.

Well Labour have stated they don't want house prices to decrease..

given Labour have just presided over the largest wealth transfer in modern NZ history, wouldn't the government/RBNZ just 'print' to re-capitalize our Retail Banks and effectively put their bad debt on the RBNZ's balance sheet?

This of course would be conditional on the Retail Banks not pursuing foreclosures and the RBNZ would likely reduce interest rates to zero or negative. Labour would then ramp up it's motel and [pre-existing] house purchases to ensure 'price stability'.

"You will own nothing and be happy" - is now what I'd call a "sarcastic axiom".

The following is a SHORT video of Labour talking about financial bailouts:

https://youtu.be/dvYvQeNeq3A

Jacinda lost my vote with the comments about how people expect house prices to increase. Housing was the one issue I voted for labour for and this blew it out of the water. I wasn't expecting a lot but certainly wasn't expecting them to want them to keep going up from these levels.

In percentage terms [and dollar terms it seems ??] house prices always increase most under a Labour government.

I wonder if the vendors of the storied '8.1 Million Motel' will now invest in residential housing. 8.1 Million might not buy many houses outright.. but it's a lot of 40% deposits.

When I heard her start using real estate industry virtue word propaganda terms like "property ladder", I knew this government was a failure.

"S&P says continuing strong house price rises would increase risk of a disorderly correction.."

Gaureth, everyone is aware except people who can make a difference as it does not suit their vested biased interest AND now Orr's and Robertson's have created a Monster that cannot be touched.

Anyone trying to stop the runaway train is bound to derail, so this people willingly have allowed themselves to be blackmail as this is how they wanted under the excuse - panademic.

Can it continue forever....only if they keep on pumping free and cheap money.......Orr's of the world are doing more harm than good.

Leeches worried there's not enough blood left to go around.

Import more blood!

Thank you Mr Orr - with your dumb ultra-loose monetary policy you have now created a monster that is threatening the financial stability of the whole NZ economy.

Stop this madness now and start raising rates urgently, before it's too late. A managed decline in house prices, driven by rising interest rates, is the only option left. The other option is to let this house of card inflate until it burst completely and it takes the whole NZ financial system with it.

It is time to follow your mandate, Mr Orr, or resign and give your role to somebody who knows what is doing.

Yeah, and ahhhhhh, financial stability is a big part of the RBNZ's mandate.....

The other option is to let this house of card inflate until it burst completely and it takes the whole NZ financial system with it.

IMO, the only option. Let it rip. Only then will the ruling elite be motivated to do anything.

Breaking News: WATER IS WET. More soon...

Brock Landers, This is the comment :)

Shocking development: Bears do in fact shit in the woods

I think the danger here is clearly stated "If they continue to rise". The risk profile changes dramatically if they stop rising and we get back to pre-covid levels of annual house price increases. The warning bells are ringing, hopefully Orr is not still wearing those class 5+ earmuffs.

Jun 2015 to May 2016 - Total Lending $72b (RBNZ C31)

Jun 2016 to May 2017 - Total Lending $67b

Jun 2017 to May 2018 - Total Lending $60b

Jun 2018 to May 2019 - Total Lending $64b

Jun 2019 to May 2020 - Total Lending $65b

Jun 2020 to May 2021 - Total Lending $95b

"Credit rating agency S&P says 'exceptionally strong' and 'unprecedented' NZ house price growth increases risks for banks"

F$#@ Banks, What about average Kiwi / FHB.

Biggest crime committed by Orr and Jacinda....not rising house price but KILLING the dream / Aspiration of average Kiwi to ever own a home for themselves to raise a family.

Only if this self centered #@$& could look beyond themselves and their childern.

The last time a bunch of people who bet against S&P in '06 - '07 got a huge payday. You only have to be right once to make it big, no difference this time round.

What's the best way of shorting the housing market?

There're more ways to do that than what's on offer in SkyCity and that also depends on your budget. But seriously, if you need to ask on the internet, you shouldn't be.

List them...

Short the banks. Some big investors did that 2 years ago in Australia (in the ballpark of a few hundred million), anticipating a housing crash. Guess how that turned out...

ANZ is buying back its own shares, good luck with that.

Oh I would never short the banks. I actually have ANZ shares. I don't think any of the big ones will be allowed to fail in the next decade (or more).

1) Borrow house 2) Sell house at peak of market 3) Market crashes 4) Offer to buy the house back 5) Get rejected 6) Cannot give house back to original owner.

Yvil was kinda shorting the housing market wasn't he? Selling at the peak and trying to buy in at the trough.

He sold well short of the peak

All facetiousness aside, I think S&P are genuinely misunderstanding the situation here.

This is not the US, where circumstances that leave mortgage-holders unable to continue repayments lead to defaults, mortgagee sales and bank impairments.

This is New Zealand, where property ownership is the Alpha and Omega of political clout *and* the only way to escape mortgage obligations is bankruptcy.

There is *no* conceivable contingency short of global nuclear war -- and I am not joking -- in which a NZ government allows a number of unwilling mortgagee sales large enough to materially affect prices. The relevant precursor is not USA '08, but Japan '90... grinding decline rather than a pop and reset.

When you put economists and quants in room, the result you get is an ineffable number that they tell you describes risk. Modern educated divination.

All facetiousness aside, I think S&P are genuinely misunderstanding the situation here.

Are you aware of their culpability in causing the GFC? They're doing exactly what they exist to do: paint a picture as the financial overlords want. Not too hot; Not too cold. If S&P says the risk level is only 4/10, it is likely to be far higher. Maybe like 7 or 8.

Risk of disorderly correction? Who will be impacted?

Why would any one be impacted if they would have used their mind and made intelligent decisions. And this includes banks who have been giving money to everyone as of money grows on trees.

But people don't think when they get carried away by rat race in which rat follows rat in the dark into the river.

This is a mess created by half witted decesion makers who just opened the doors for printing press to print the dollars and let everyone have it for free. ( not literally).

The best part is no one can hold them responsible for their actions.

Why aren't these statements from S&P brought up at question time with the government? Either by reporters or the opposition parties.

National MP's own lots of property and many probably have mortgages. As they're 'out of power' their salaries have been reduced. They are turkeys and as such are unlikely to vote for Thanksgiving. You won't hear any housing policy from them. They also get a lot of donations from people affiliated with real estate.

The Maori Party are into identity politics and reparations.. they think papering-over-cracks, combined with woke-secular-psychology, wrapped in Maori culture and targeted at Maori is the answer to everything.

ACT are probably the best on housing during question time .

"Credit rating agency S&P says 'exceptionally strong' and 'unprecedented' NZ house price growth increases risks for banks"

A more apt statement would be:

"Credit rating agency S&P says 'exceptionally strong' and 'unprecedented' NZ DEBT growth increases risks for banks"

Why focus on the symptom of frivolous debt accumulation (increased house / asset prices), why not state the obvious? The continued availability and distribution of cheap debt into a non-productive finite asset class presents risks to banks, the wider financial system and New Zealand's current & future economic wellbeing.

And yet the regulator (RBNZ) see nothing wrong with the situation, pumping MORE money into the current situation. Beggars belief.

And yet the regulator (RBNZ) see nothing wrong with the situation, pumping MORE money into the current situation. Beggars belief.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.