The Reserve Bank’s (RBNZ) decision to impose tighter restrictions on banks’ mortgage lending is expected to make it exceptionally difficult for anyone with a deposit of less than 20% to get a mortgage.

The RBNZ on Thursday announced it's forging ahead with its proposal to halve the portion of mortgage lending that’s allowed to go to owner-occupiers with deposits of less than 20%.

From November 1, only 10% of banks’ mortgage lending to owner-occupiers can go to this riskier cohort of borrowers.

Someone buying a median-priced home for $850,000 will struggle to get a mortgage with a deposit of less than $170,000.

The RBNZ acknowledges the change will mostly affect first-home buyers, as banks tend to use up much of their riskier lending, or high loan-to-value ratio (LVR) allowances, on these borrowers.

High LVR lending likely to be well below 10% limit

Jim Reardon, CDS Consulting managing director and former Westpac treasurer, was one of the majority of submitters to the RBNZ who opposed its proposal.

He said quite a bit less than 10% of banks' mortgage lending could end up going to borrowers with small deposits, as banks typically create buffers to ensure they don’t breach their allocations of high LVR lending.

Since LVR restrictions were reinstated earlier this year, 13% to 14% of new mortgage lending has been going to borrowers with deposits of less than 20%.

Removing mortgages exempt from the restrictions (IE for new builds) from the data, only around 11% of new lending has been going to borrowers with small deposits - a portion well below the 20% allowance.

Reardon maintained that even if banks use smaller buffers when the allowance halves to 10% in November, they're unlikely to have internal limits of more than 5%.

“An operating limit of 5% would effectively leave most first-home buyers out of the housing market," he warned.

"With the introduction of higher limits on investors, first-time buyers now make up around 75% of high LVR lending.

“Restrictions on first-home buyers would have long term social impacts as a generation of potential homeowners are destined to become lifetime renters.”

The RBNZ said banks "may choose to stay below the regulatory limit to reduce the risk of inadvertent breaches" and it is up to them "to decide how much of a buffer they are comfortable with".

There may be an initial drastic drop in high LVR lending

The retail banks that submitted on the RBNZ’s proposal also warned they may need to really tighten their lending to meet the RBNZ’s requirements as abruptly as proposed.

The RBNZ suggested the new rules apply from October 1, but after consultation, pushed this out to November 1.

The New Zealand Bankers’ Association asked for the first reporting period the rules will apply to, to be extended by three months to March 31.

“Without this period, banks will need to temporarily slow high LVR lending in a much more dramatic way to meet the new requirements,” the Association said.

“A dramatic slowing of high LVR lending will adversely impact first-home buyers and create uncertainty in the property market, particularly when this strategy will only be temporary and will moderate again in the next reporting period.

“A longer first averaging period allows banks to select sustainable acquisition settings that reduce availability of high LVR lending without creating a yo-yo effect.”

The RBNZ responded to this feedback, saying it’s historically given banks three months from announcing a proposed LVR change to implementing it.

Given the proposal was announced on August 8, a start date of November 1 should give them enough time to prepare.

Are first-home buyers really threatening the financial system as a whole?

The RBNZ’s harshest criticism came from Reardon and other consultants.

They argued the small portion of lending banks are doing to borrowers with deposits of say 10% or 15% isn’t actually posing a risk to the financial system.

Ian Harrison of Tailrisk Economics, who has worked for the RBNZ, International Monetary Fund and Bank of International Settlement, said, “The Bank has suppressed lending to housing investors following the Minister’s [Grant Robertson] wish to give first-time homebuyers a better chance of securing a property. Now that this demand has emerged the Bank wants to choke it off.

“This is based on an almost irrational obsession with housing lending risk.”

Geof Mortlock, who consults for the likes of the International Monetary Fund and World Bank, said “there is no evidence at all that a fall in house prices would cause financial system instability” and banks have enough capital to address the risks in question by the RBNZ.

“One is left with the impression that the real reason the RBNZ is embarking on this path is for some kind of ‘welfare’ purpose – i.e. to protect highly leveraged households from a fall in house prices,” he said.

“That is not part of the RBNZ’s statutory mandate. It has no role to promote the financial resilience of households; its sole mandate is to promote the resilience (and efficiency) of the financial system.”

Interest.co.nz canvassed this argument in a piece a couple of weeks ago.

Negative equity a risk for recent buyers, not the system

While a 20% fall in house prices would see 22% of mortgage lending done to first-home buyers in the year to July in negative equity, it would only see 5% ($5 billion) of all mortgage lending done in that year in negative equity.

That $5 billion is equivalent to only 1.6% of banks’ mortgage books.

Reardon noted, “While negative equity does present a less than ideal scenario, in of itself this does not directly lead to mortgage defaults.

“Negative equity has meaningful outcomes for lenders in the event of a default, however the likely level of defaults that New Zealand banks would face even in a scenario as dramatic as a 20% fall in housing prices would not lead to bank losses beyond which their current profitability and capital base could withstand.”

Reardon also argued the bank housing loan drawdown data the RBNZ uses overstates the prominence of high LVR lending, as these high LVR loans tend to be paid down fairly quickly so borrowers can access lower interest rates on offer to lower risk borrowers.

Small impact on house prices

One might argue that curbing banking lending will reduce demand for property, which will slow house price inflation - to the benefit of first-home buyers.

However, Mortlock maintained the change would “not make much of a difference to house price inflation”.

“At best, it will only make a marginal difference to buying pressure in the housing market. However, it will hurt the very people who are already suffering from house price inflation - first-home buyers,” he said.

Better government policy required

Harrison addressed the elephant in the room, saying, “The easiest and most effective solution to the identified problems would be to increase housing interest rates.”

Mortlock said government policy was needed to address the housing crisis.

He suggested an interest rate surcharge on lending to residential property investors, a stamp duty or transaction tax on house sales, freeing up urban land for development, relaxing building consent requirements, and upscaling managed isolation to let more builders into New Zealand.

Reardon also noted that serviceability tests, like debt-to-income ratios, could be useful. The RBNZ is due to start consulting on implementing these in October.

A number of submitters had a go at the RBNZ for a "sham" of a two-week long consultation on LVR restrictions, which ended less than a week before the RBNZ announced its final decision.

For more on the RBNZ’s case for tightening LVR restrictions, see this story.

35 Comments

This is super good news for rents.

We ourselves couldn't lock in FHB hopefuls longer than their ability to buy their own, now that we have the country's own machinery to do that job for us, it's nothing short of a call for celebration for every landlord in this country.

Positioning for rent revision.

Be quick.

Yawn. If trolling is your game, be clever and witty about it. This is not much higher than juvenile.

Usually it's the real trolls that feel the sharpest pain on every rent increase.

Enjoy.

Think your confusing 'trolls' with 'serfs'.

So are you saying renters feel the sharpest pain - i.e. your customers?

So you take pleasure out of inflicting pain from renters, your customers.....nice business environment.

I'm referring to those who can't stand others making money- except for themselves though.

When you live to my age, you'll understand that without some pain, pleasure becomes underappreciated.

Struggle is good; it gives life a purpose.

If you've been flipping 31 houses a year on average....then perhaps your problem is that you don't know when you've made enough money at the expense of others (that being renters/first home buyers).

But of course...everyone is just envious of your success right?

(let me go get a bucket...)

When you start making good money, not just you start to get competition but also outright enemies. It's just the nature of the beast, regardless of what you do to make money.

Your income will always be someone else's expenses, this basic law stands true for every occupation- even if you're a monk.

Oh well keep doing what you're doing and I'm sure it will bring you great joy - young and vulnerable people will thank you for it (yeah nah?)

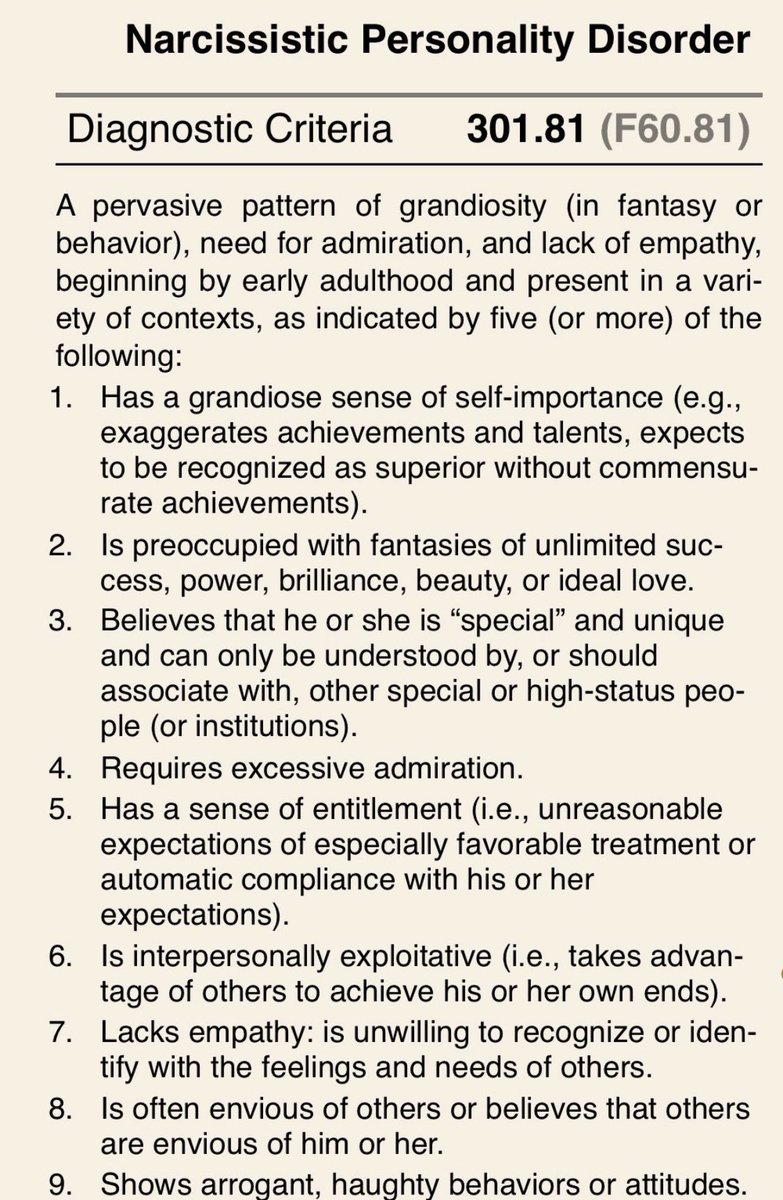

And if you have the thought that people might be envious of your success, just remember the signs and symptoms of narcissitic personality disorder which for some odd reason appear to go hand in hand with self proclaimed 'successful' property types. Points 7-9 in the below seem to fit the type characteristics.

https://pbs.twimg.com/media/ECNOtaOXYAAbjo8.jpg

{kind=link}

If you strictly follow the guidelines in the DSM manual, everyone can be diagnosed with some form of mental disorder- which probably includes you.

Yeah many younger New Zealanders who can't afford a house are suffering with anxiety and depression, while older property investor types appear to be suffering from delusions of grandeur......not seeing they are in significant part, adding to the suffering that other people in society are experiencing.

Not all mental disorders are equal....one of ego, fear and selfishness can cause another of pain, suffering and uncertainty for others.

Your income will always be other people's expenses, but doesn't have to be at other people's expense. There is a difference between a mutually beneficial exchange of goods and services and profiteering (taking advantage of a crisis to exploit the desparation of others to inflate your prices, which by your own description is what you are doing).

To be honest, if you were a housing activist deliberately playing a role in order to foment discontent, you couldn't be doing a better job. Your posts seem deliberately designed to stir up as much resentment of landlords and property flippers as possible.

I wouldn't call it exploitation. It's just supply and demand and like any good businesses we seek to find the price equilibrium to justify our business potential and optimise its performance.

Like what my grandkids used to say, "haters will be haters."

Don't take it personal, it's just business.

Im not surprised you wouldn't call it exploitation. You clearly have a strong financial incentive not to call it that.

if the main purpose of your life is a struggle to get richer than what is necessary, and the gloating of having achieved this at the expense of others, I really and genuinely feel very sad for you, and for whoever has the misfortune of having to share it with you.

Exactly, see what the government is really achieving with every action they take.

CWBW Sounds like you think your are a super villain , but I have been told your just a mini me

You're right. If you people in here thinks flipping a couple of properties was a big deal, you guys haven't met enough people in this country.

"This is super good news for rents." [CWBW]

There's nothing inherently good or bad about rent.......

But I'd rather be receiving it than paying it.

TTP

Jenee, or someone else - are new builds still exempt, or not?

That is, can FHBs still buy new houses with less than 20% deposit?

Yes. From the RBNZ's website:

"Under specific circumstances there are exemptions to LVR restrictions. Where a loan falls under an exemption, the loan is not included in the banks’ high LVR ‘speed limits’. Exemptions related to construction, remediation, loan portability, bridging finance, refinancing, Housing New Zealand loans, Kiwibuild, and combined collateral are detailed in the LVR factsheet: A guide for borrowers (PDF 141 KB). Details about the exemption for new home construction are in the Construction exemption Q&As (PDF 101KB)."

Great, thanks for that clarification.

Even so, I think new builds will take a hit because of the huge challenge to build within the Homestart price cap (700k in Auckland)

Better government policy required

Harrison addressed the elephant in the room, saying, “The easiest and most effective solution to the identified problems would be to increase housing interest rates.”

The point made by Harrison above needs to be emphasised as this is urgently needed to make housing more affordable.

In July 2021, previous RBNZ chair, Arthur Grimes warned that NZ was heading for a well-being disaster & said NZ government needs to ditch the maximum sustainable employment target when setting the OCR as this has created excessive house price inflation.

https://www.newstalkzb.co.nz/on-air/heather-du-plessis-allan-drive/audi…

To late Tony, all we can get now is increased rates on top of 30% increased house prices in the last 12 months. Its just going from bad to worse in reality. Banks are now covering themselves in the event of house price drops.

Arthur made these comments here first: https://www.interest.co.nz/news/111369/inflation-targeting-architect-ar…

I find it funny that people like to bash the CCP for making life a misery for parts of their population - yet we've got our own state entity that in many respects if far more oppressive and causes far more damage to its own citizens that the CCP does to its own - and its call the Reserve Bank of New Zealand!

If anyone asked me if I thought the Fed was more or a liability to world stability vs the CCP - i'd say the Fed by a factor of about 10.

And in NZ the RBNZ is NZ's biggest threat to financial and social armageddon despite their mandate being the complete opposite - who'd of thunk.

I like your comments IO but this is a bit OTT!

Especially when many of China's citizens are illegitimately incarcerated.

Having said that, kind of agree with the spirit of your comment.

Well the US has the highest incarceration rate in the world doesn't it? And why is that? Because the Feds actions over the past few decades has caused extraodinary inequality and oppressed significant parts of the US population. Lived there, witnessed it first hand.

I haven't been to China so perhaps I need to live and travel around there to see how it really is first hand.

At least we haven't had the police brutality here in NZ yet HouseMouse....yet if you look to America and Australia... the leaders of the 'free world', the police have been beating their own citizens so that governments and central banks can push forward with their own oppressive agendas of lockdowns and closing businesses and chosing who can come and go from their countries....and stimulus checks....and tracking peoples movements...and arresting people when big brother detects that someone isn't following the rules.....with a central bank setting the price of housing and commodities....not the free market.....it sounds like we've slipped into communism to me. More so than the CCP over its own citizens.

It almost feels as those western countries have become more controlling than those countries that we used to laugh at....like John Key pointed to in his article....North Korea

Look, if covid passes and 'things' get back to normal - we have proper free markets and less government controls mandates...we'll I'm looking forward to that day. In the mean time, it looks like we've slipped further to the left than China has.

Slavery, unjust sterilization & torture is not comparable to homelessness

Harder for FHB ...WHAT ARE THEY DOING TO CONTROL SPECULATION ?

Why not increase LVR to 60% from 40% for investment property.

DTI is must to protect FHB from themselves under FOMO.

The problem us that a DTI locks out FHBs unless there is a serious discussion around what prices should be and how we get them back here.

Current PM is on record as saying 'small increases' are sustainable, so what is the plan for those outside the DTI to ever be able to buy again?

Most of what comes out of her mouth is just mental flatulence.

only around 11% of new lending has been going to borrowers with small deposits

This says it all really! Another announcement to hit the headlines, but when you look at the detail it means nothing.

People need to wake up! This govt/rbnz is screwing over the young...

This is just plain wrong. This government and RBNZ seem hell bent on hurting those they claim to protect. Renters facing higher rents, first home buyers shut out and those lucky enough to win a lottery (that's what over 80% borrowing is) then face higher interest rates and fees. For what? There never has been so called reckless lending in NZ, there is no 'high risk' lending history. 80% of property investors are 'mum and dad' types, now forced to operate with increased costs, passed on to the tenant meaning les money for saving. Well done RBNZ, you have created the perfect storm.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.