New Zealand banks are unlikely to enjoy the same strong loan growth in coming months as they have during the pandemic so far, but tougher economic times may see loans staying on their books for longer, KPMG's Head of Banking and Finance John Kensington says.

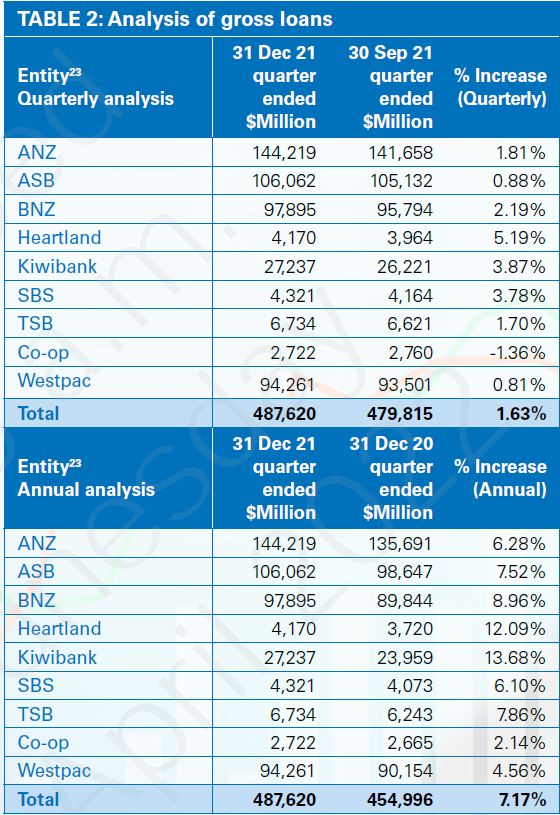

Kensington was speaking to interest.co.nz following the release of KPMG's Financial Institutions Performance Survey (FIPS) for the December 2021 quarter. It shows banks increased net profit after tax almost 7% from the September quarter to $1.614 billion, getting close to the bonanza $1.643 billion recorded in the March quarter of last year. The banks grew gross loans by 1.63% to $487.620 billion in the December quarter, and by 7.2% in the year to December.

Against the backdrop of the ongoing Covid-19 pandemic, high inflation, Russia's invasion of Ukraine and businesses operating below capacity due to staff shortages, Kensington says he doesn't see banks continuing to experience the same level of loan growth as they have over the past couple of years.

"I don't think they're going to enjoy the loan book growth in the sense of the number of loans they write, or the level they're going to write them at. I would say if you look at a house that was sold or financed two, three, four years ago, it might've been a $1.5 million house. If it was financed between the beginning of Covid and now, that same $1.5 million house might've been financed at $2.5 million. I don't think that upward trajectory's going to continue," says Kensington.

"But one thing that may assist or help is people were paying loans off at very low interest rates so that their household income was covering everything. There were many things they weren't able to spend on like travel and entertainment. So lower interest rates, lower outgoings, meant they had more money, and many mortgages were being paid off quickly."

"When the reverse happens and you get inflation, and you get rising interest rates, I think loans might be a bit more sticky. I think they might stay on the books a little bit longer so that the banks mightn't need the same growth. In that way their pool of loans that they've got on the books, the dollar value of them, might not change," Kensington says.

"So I think we'll still see some periods of reasonably strong performance by the banks."

Whilst there has been "a massive phenomenon" over the past couple of years of borrowers being able to pay off loans faster than required, Kensington doesn't see this continuing.

"In the past a bank might've had $80 billion of loans on the books, let's say, and it might've churned off $10 million a year but it might've added $11 or $12 million. And the next year it might've dropped $15 [million] and it might've churned on $16 or $17 [million]. I don't think you're going to see the same rate of churning because I don't think people will be able to pay loans off more quickly," says Kensington.

'I think they'll still perform well but maybe not at the record levels'

Whilst low unemployment, at just 3.2% in the December quarter, reduces the risk of a significant number of borrowers not being able to meet their loan repayments, Kensington says businesses operating below capacity also helps those in employment. Businesses struggling to get the volume of and/or qualified staff they want means they probably have to pay the staff they've got more. Banks are no exception to this.

"I think going forward they're big businesses, they'll still always be big. They earn a margin, and so that will give them a base level of income as a result. If they have some challenges it'll be around getting people, what they have to pay to get people, it'll be around what inflation does to their costs. So I think they'll still perform well but maybe not at the record levels," Kensington says.

FIPS figures show banks reduced loan provisioning another 5.3% in the December quarter to $2.44 billion. It was the fifth consecutive quarter of net impairment writebacks as provisions raised early in the pandemic continued to be unwound. Banks' combined cost-to-income ratio came in at 39.7% in the December quarter, down from 43.1% in the September quarter. Net interest income increased 3% to $2.9 billion.

Helped by a $1.69 billion reversal in impaired asset expense, NZ's banks posted combined annual profit of more than $6 billion for the first time in the September 2021 year. (There's more on banks' December quarter financial results here).

The banks included in the December quarter FIPS are ANZ, ASB, BNZ, Heartland Bank, Kiwibank, SBS Bank, TSB, The Co-operative Bank and Westpac.

*The FIPS shows NZ banks continued increasing housing lending as a percentage of their overall lending during the December quarter, as demonstrated below. KPMG is an auditing and financial advisory firm.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

13 Comments

"I don't think they're going to enjoy the loan book growth in the sense of the number of loans they write, or the level they're going to write them at. I would say if you look at a house that was sold or financed two, three, four years ago, it might've been a $1.5 million house. If it was financed between the beginning of Covid and now, that same $1.5 million house might've been financed at $2.5 million. I don't think that upward trajectory's going to continue," says Kensington.

LOL - which segment of the NZ population is he referring to? Not even the 1%. Just some fraction of that cohort.

“Ultimately there’s no natural income streams to be able to service and repay loans. What you have is capital gains which are contingent on the game continuing. So it’s a Ponzi scheme. says Werner. - https://wire.insiderfinance.io/richard-werner-qe-infinity-707e2c627e03

Market capitalization isn’t “wealth.” It’s the latest price, times shares outstanding. Blotches of ink on paper. Flashing pixels on a screen. If a dentist in Poughkeepsie buys a single share of Apple at a price that’s 10 cents higher than the previous trade, $1.6 billion in market capitalization emerges from thin air. If a single share trades 10 cents lower, $1.6 billion evaporates just as quickly. Whatever happens, every security in existence has to be held by someone until it is retired. Ultimately, the wealth inherent in a security is the future stream of cash flows it will deliver to its holder(s) over time. Price fluctuations don’t change those underlying cash flows. They just provide opportunities for the transfer of savings between investors. High valuations favor the sellers. Low valuations favor the buyers. Investors have never paid higher prices for those future cash flows, or accepted prospective returns so low.

Put simply, the bubble hasn’t changed the wealth, and a collapse won’t change the wealth. What will change is the market cap. I suspect that the erasure of market cap in the coming years, and possibly the coming quarters, may be brutal. Still, no forecasts are required, and our own attention will remain on observable valuations, market internals, and other factors. Meanwhile, even if an investor sells at these extremes, the only thing that will change is who holds the bag. Link

Meanwhile, even if an investor sells at these extremes, the only thing that will change is who holds the bag.

In the case of bank leveraged NZ residential properties that will be the ordinary 99% cohort bank depositor.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Great post. Investing is supposed to be about income streams, and nothing else. That is where the fundamentals lie, and used to be how investment decisions were made.

We then decided to start making investment decisions based not on the fundamentals, but on our perceived ability to sell to someone else at a higher price later on, but we've actually taken it one step further than that. We don't even look at price anymore. Who cares what the price is, when someone else is guaranteed to come along later and offer you even more for it?

We now make investments without looking at fundamentals or value. The only thing we look at is the cost of the debt we took out in order to fund it. This is more than just speculation, it's leveraged speculation, and when the whole thing unravels it will be quite spectacular indeed.

Sounds like a ponzi.

Interesting times -- with so many job vacancies -- its hard to see unemployment being the issue for the foreseeable future - 1000 nurse vacancies in Elder care and another 1000 in teh Auckland DHB's for example --

But the difference is probably that even with a relatively skilled job such as a nurse or teacher -- the bills will still be hard to meet -- never mind discretionary spending -- - so what type of recession are we heading for -

something completely different -- without the long dole queues -- more people working longer and longer hours -- but spending less and less? but like all recessions -- wotn impact the rich and wealthy those who have already paid of their mortgages -- but will smash the poor even more than they have been in the last four years and thats sayign something!

Housing costs are too high for nursing, teaching, policing and many other necessary occupations to be viable for lots of folk. We have been transferring wealth to asset-owners instead of productive work for too long and to too great an extent, and now we are reaching the point it's simply not viable for those we've been taking from to keep going.

It's better to consider the size of mortgages rather than the purchase price of the house. In recent years $500k mortgages are common, back in 2012 it was probably around $250k to $300 (a bit more once the prices seemed to spike up after that time).

If the banks rate of issuing mortgages drops, and mortgages stay on the books longer there will be a downward trend on the bank's mortgage books. The older the mortgages the larger the principle component of the repayment is. Even with higher interest rates having mortgages on the books for longer means less interest income for the banks, and the potential for a static or shrinking mortgage volume will eat into their profits.

It's not the borrowers I'm concerned about but the volume of money being removed from the economy by the loan repayments. At the moment the quantity of money is increasing but the inflection point where that changes will have consequences.

As the mighty Audaxes has pointed out so wonderfully, banks aren't really in the business of lending money. They purchase promissory notes. When the punters go big on a mortgage, they do not receive "money" in their accounts. It's simply a record of the debt. That's how the commercial banks create money supply. So when banks lend, they're effectively creating fictitious customer deposits. The accounting all works but it's dreadful when you think about all the instability and fragility it creates. .

I use the conventional terms like mortgage or loan for the purpose of communicating. The banking license is all about creating money out of thin air via accounting entries. RBNZ is supposed to regulate the creation, or destruction, of money but it's allowing the banks to go hog wild.

I see loans to businesses, agriculture and general consumers all decreasing while housing lending increases as a share of total loans.

Wonderful. We know why the housing lending is increasing, but is it masking increases in size of business loans for example? That would be good news.

Loan stickiness is an interesting euphemism for mortgage prisoners. Borrowers are stuck with their existing lenders because new legislation means they can’t refinance to cheaper rates. Will reduce competition in lending and increase profit margins for banks at the expense of homeowners.

"Borrowers are stuck with their existing lenders because new legislation means they can’t refinance to cheaper rates."

Borrowers cant refinance to cheaper rates because there arnt any...that tends to be the effect of rising interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.