The Commerce Commission sees "good reasons" to recommend designation of the interbank payment network to Commerce and Consumer Affairs Minister Andrew Bayly.

In a new consultation paper on the retail payment system, the competition watchdog says; "based on the information we currently have ... we currently consider that there are good reasons to recommend designation [of the interbank payment network of which Payments NZ is a network operator]."

When a network is designated the Commission has powers to decide how prices can be set or expressed. A designated payment system could be one deemed to pose systemic risk, or that's designated to protect the interest of the public or the interest of the integrity of the payment system.

Designation would occur under the Retail Payments System Act, which provides for the regulation of participants in retail payment networks including via initial designations and an initial pricing standard. The Mastercard credit, Visa credit, Mastercard debit and Visa debit retail payment networks are already designated under the Act, with an initial pricing standard set limiting interchange fees.

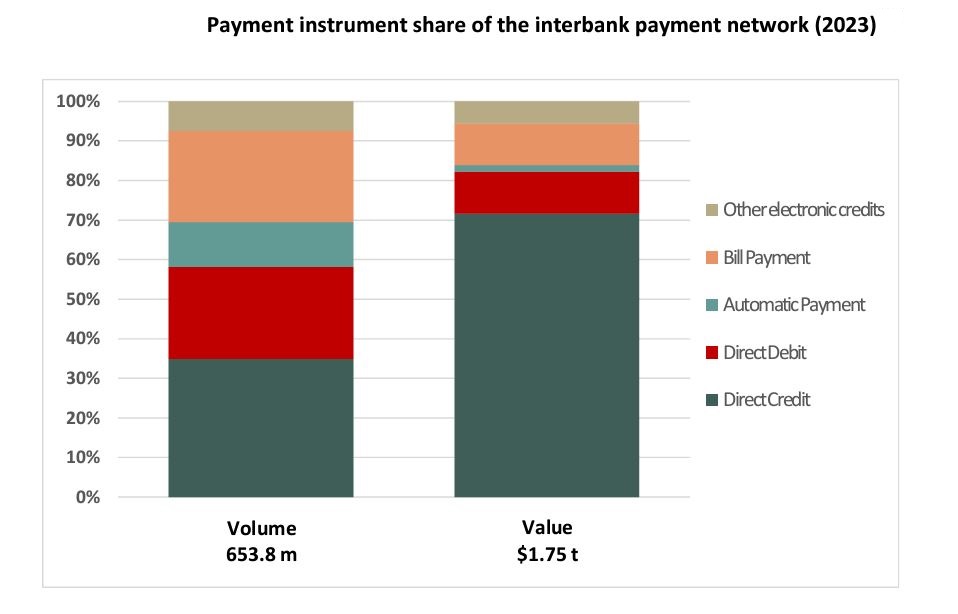

Citing Payments NZ data, the Commission describes the scale of the interbank payment network as significant, saying the value of payments between different bank accounts was $1.75 trillion in 2023.

The Commission is proposing the interbank payment network be defined as; "including all bank payment instruments between registered banks or within a registered bank for the payment of goods or services initiated by either a consumer or a merchant as payee and where payment instructions are sent directly to the payer's bank."

"This includes all payment instruments, such as direct credits and direct debits, irrespective of the method of initiation and, as an example, a consumer either directly or indirectly initiating a payment through a third party," the Commission says.

The new consultation paper comes after the Commission in February cited a lack of innovation in payments between bank accounts, noting it's one of the cheapest payment methods available, and last year said it was considering regulation of the bank transfer network to give New Zealanders more options to make in-person payments directly between bank accounts.

"Designation, without immediate regulation, is a measured and appropriate response to better promote the timely delivery of a thriving open Application Programming Interface (API) ecosystem, particularly as designation would not require further direct intervention if industry delivers in a timely way," the Commission says.

"Designation of the interbank payment network provides an opportunity to increase competition and efficiency broadly across the retail payment system. It is generally accepted that a thriving API enabled ecosystem will provide new methods of making and receiving payments for consumers and businesses that will have significant benefits for them."

"Those benefits include increased choice through more payment options, innovation through increased functionality, improved consumer protections, and increased uptake of innovative methods for consumers and businesses to make and receive payments to and from their bank accounts using third party services," the Commission says.

Changing incentives

It says designation would change the incentives for the banking industry by raising the credible threat of regulation where the industry doesn't deliver a thriving open API ecosystem in a timely way.

"This potential regulation could require participants to adhere to industry-led solutions and expose participants to a penalties regime. With designation, if industry does not deliver a thriving API ecosystem in a timely way, the time required for us to take regulatory action would be shortened. We would be able to intervene immediately after consulting on that intervention. Hence, with the change in incentives, a benefit of designation is that it can be a cost-effective way to bring forward significant unrealised benefit to consumers and businesses."

"We recognise there may be additional costs if the use of regulatory powers is required. Any compliance costs or risk of unintended consequences of regulation would be considered as part of any future decision making process if we considered the use of regulatory powers may be necessary," the Commission says.

The Commission has also expressed frustration with the slow uptake of open banking in New Zealand. Open banking allows financial data to be shared between banks and third-party service providers via the use of APIs. Traditionally banks have kept customer financial data within their own closed systems.

One of the key recommendations in the Commission's recently released interim report in its market study on competition in personal banking is; "the Government should set clear deadlines and work with industry to ensure open banking is fully operational by June 2026."

The Commission says progress towards open banking, which is being overseen by the bank-owned Payments NZ, has been too slow.

"Open banking will help tip the scale for smaller challengers overseas and can be expected to boost innovation and competition for personal banking services. However, progress in New Zealand has been too slow, because the major banks have been left to set the nature and the pace of change. As a result, New Zealand is now falling behind the rest of the world. Progress towards open banking needs to be maintained and accelerated within a clear regulatory framework and with government-set deadlines," the Commission says in the interim report.

In its consultation paper it points to "significant unmet demand for innovative new payment methods enabled by a thriving API enabled payment ecosystem" in NZ. It also refers to concerns about the timeliness, access arrangements, loss of investor confidence, transparency and reasonableness of fees of the API enabled ecosystem that uses any undesignated interbank payment network. Additionally the Commission wants more progress ahead of the pending consumer data right legal framework, which will require businesses holding data to share prescribed data they hold about customers with trusted third parties with the consent of the customer.

ANZ NZ called out

The Commission highlights heel dragging by the country's biggest bank, ANZ NZ.

"To the best of our knowledge, since ANZ provided access to Worldline [formerly Paymark] in 2022, it has not partnered with any other providers. As ANZ is the largest bank, its progress on access arrangements has the greatest impact on the development of the API enabled payments ecosystem," the Commission says.

And on submissions from its previous request for views paper, the Commission says Kiwibank "questioned the appropriateness of open banking for the New Zealand economy, and considered a cost-benefit analysis of the investment is required."

Cost-benefit analysis should consider which open banking use cases would deliver the greatest impact, the appropriate level of investment by industry, measures of success, the distribution of risk between participants, and the best legislative/regulatory vehicle for delivering it, Kiwibank says.

Kiwibank cites "a real risk" Aotearoa’s open banking framework could end up being "inappropriate for the relatively small size of the market, over capitalised, and underutilised."

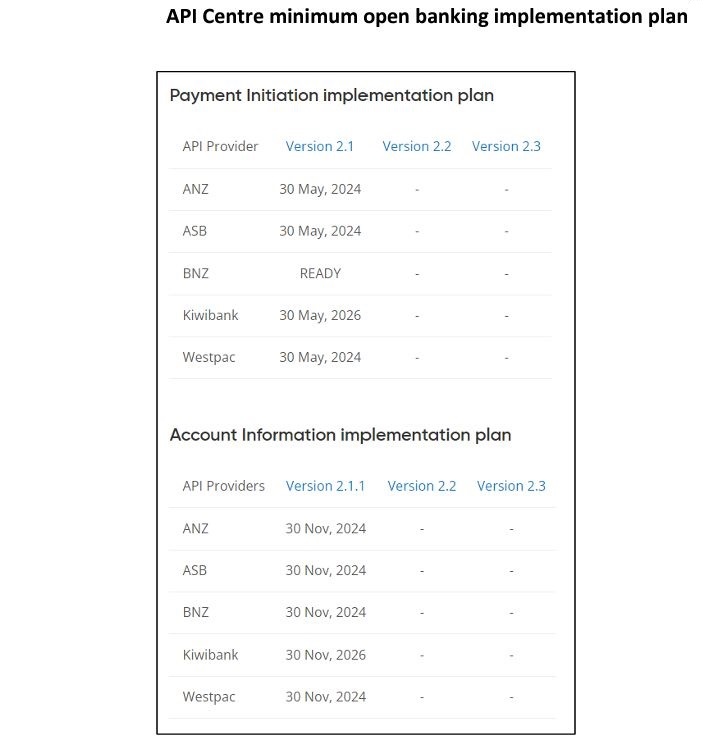

The Commission, meanwhile, highlights a lack of public reporting by the banks on their progress against the timeframes, specifications and guidelines of Payments NZ's Minimum Open Banking Implementation Plan, noting BNZ as an exception having already begun partnering with fintechs when the Plan was set in May 2023.

"We note that there are 24 parties, seven API providers and 17 third parties, signed to the [Payments NZ] API Centre, and that all third party provider start-ups and multinationals need investment to continue developing these innovative payment options. Delays or uncertainty in the delivery of the minimum requirements for a thriving API enabled eco-system are likely to affect the confidence of investors in these innovative payment options to the potential significant detriment of business and consumers in New Zealand. We consider that if there are further delays, this may increase the risk premia on investments in the NZ payment system both for fintechs and for banks. If major banks continue to treat open banking, including a thriving API enabled ecosystem, as a 'nice to have' then future investments will be harder to achieve," the Commission says.

"We recognise industry efforts but are concerned that industry will not deliver a thriving API enabled payment eco-system alone. Industry has made a start but there are features of the interbank payment network and conduct of the participants which we consider mean that the minimum requirements are unlikely to be met in a timely manner without a credible threat of regulation."

"Open banking regimes around the world have required regulatory intervention, often ongoing to some degree, to flourish. Furthermore, as discussed earlier, the more successful API enabled payment ecosystems in the world, UPI in India and Pix in Brazil, have had significant government involvement. We are not proposing involvement of that scale but consider that the availability of more timely regulatory intervention would provide greater confidence in delivery," the Commission says.

Regulatory v industry led

Payments NZ CEO Steve Wiggins told interest.co.nz last year Australia, the United Kingdom and Europe were ahead of NZ in the rollout of open banking because they've been "regulatory led." Wiggins also said NZ wasn't behind simply because Payments NZ is bank owned.

Last year Payments NZ announced ANZ, ASB, BNZ and Westpac must be technically and operationally ready to allow their customers to share financial data with third parties via open banking this year, with Kiwibank to follow in 2026. The idea is that such data sharing should both increase price transparency, and enable comparison services to accurately assess how much a product would cost a consumer based on their behaviour. This could therefore enable the recommendation of the most appropriate products for individual customers.

Formed in 2010 by the banking industry with the Reserve Bank's support, Payments NZ governs NZ's core payment systems and works with the industry leading open banking and the future direction of payments. Its shareholders are ANZ, ASB, BNZ, Citibank, HSBC, Kiwibank, TSB Bank and Westpac.

Commerce Commission Chairman John Small, speaking in interest.co.nz's Of Interest Podcast, says the industry running the NZ open banking push has a lot to do with the slow progress.

"Neither the UK nor Australia have got where they are by leaving it to the industry to design and implement open banking," Small says.

Overseas where there's a lot more innovation in the open payment space than NZ, this "doesn't tend to happen by the established industry disrupting itself."

"It tends to happen by governments getting in behind it and changing the incentives, if you like. And that's the way we see it here too. We think that there's a lot to be said for harnessing the knowledge and expertise that's in the banks. But we think that their incentives need to be changed such that they really want to get on and do it," Small says.

The Commission says it's consulting with the Reserve Bank and has sought its response in relation to the proposed designation. It's seeking submissions on the consultation paper by 4pm on Friday May 10.

*This article was first published in our email for paying subscribers on Wednesday. See here for more details and how to subscribe.

4 Comments

So they're threatening to think about threatening to regulate to be able to threaten them about regulation, I think.

This report will already be gathering dust with the others

For your average kiwi this would be great. resulting in increased competition. Etc etc

However we are run by the elite for whom this would be very bad.. competition is bad for profits of the companies they and their mates run you see ..

Might actually be better if we stop paying for reports.. but thenthey are commissioned to solve a problem that is long forgotten by the time they get published.

The only way that we can circumvent the payment system is by using cash, i.e physical currency rather than electronic currency.

Why would you ever think banks will do the right thing without being compelled.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.