The latest quarterly RBNZ Dashboard data allows us to find the winners, and losers, in the competitive home loan sector.

This is important because this is the largest lending activity in the New Zealand banking system.

It has an advantage in that it is juiced by low capital support requirements. Basically shareholders get leverage benefits when banks deploy capital to this sector. Each $1 of capital can support about three times as much lending as for other lending targets. Over many decades, this incentive has turned most banks into mortgage banks. And the incentives ratcheted up to another level after Basel III came into effect at the time of the GFC.

Since the RBNZ Dashboard was established in 2018 we have had a consistent set of data to track market share changes in home loans. The total market is defined by the data in C5. The share of that of individual banks is revealed in the G.1. Dashboard series.

Over that period, housing loans have increased by +53%. All other lending has increased by just +15%. (C5 data)

The five major banks account for more than 93% of all mortgage lending. And that is the highest share since these consistent records began in 2018. The big are getting bigger.

Making gains in this market isn't easy. There are huge embedded positions. Those positions are relatively easy to defend. If you are a bank and you lose a customer to a rival, you know exactly who to target to get them back.

So market share gains are hard to win. And the change is glacial - even if there is plenty of evidence many more borrowers are comfortable shifting between banks. Most losses are made up by equivalent gains elsewhere.

But over the longer term - eight years now for this Dashboard series - there are in fact winners.

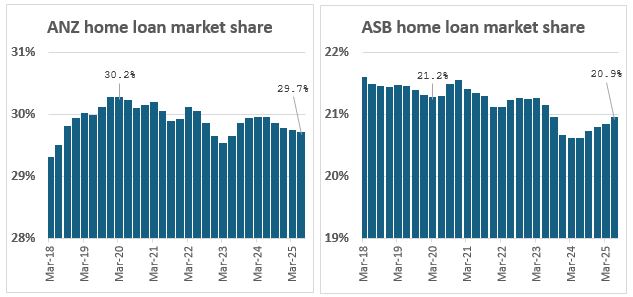

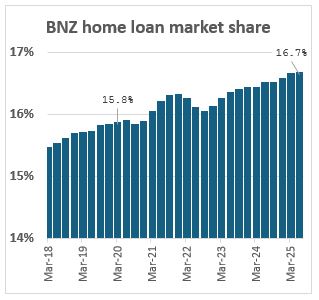

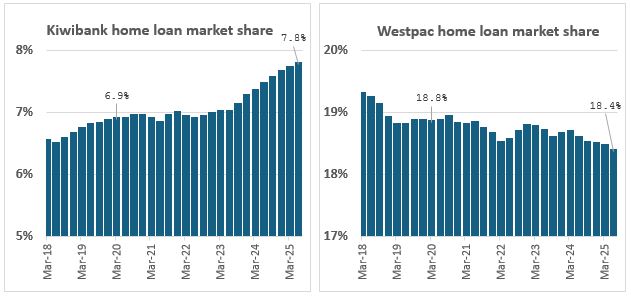

And they tend to be the two banks with smaller mortgage books - Kiwibank and BNZ. Both are making important gains and now both have record high market shares.

In the middle are ANZ and ASB, the two largest home loan lenders. Their share has shifted both up and down. On balance, ANZ has barely held on to its share over the eight years we are looking at. ASB has lost some net share, although like ANZ the change is only fractional.

Westpac is the bank that has given up market share on a consistent basis. On a net basis, the flow is out from them and into Kiwibank and BNZ.

So it isn't a real surprise that Westpac has recently tended to be the most rate-competitive. They have work to do to turn the trend around, and they seem to be taking the challenge seriously. But just like the losses, gains will only come slowly.

Here is the easiest way to watch how these market share changes have evolved so far.

All this data is from the RBNZ Dashboard. Even though the quantum of mortgage lending is quite different between these five lenders, the 3% data range in the above charts is consistent between them all. It shows the relative rises and falls accurately.

We have a tool that uses this data in an easier-to-inspect manner, here.

2 Comments

I'm yet to meet a happy Westpac customer. Always they least service, first to pull down the shutters etc.

I think you are right. We have been with Westpac for a while. But our offspring have moved banks, and question why we are still with them. That said we just refinanced for an extension in recent months. We got options with KiwiBank and Cooperative. But in the most recent dealings Westpac were relatively easy to deal with so we opted to stay with them.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.