The ranking of the banks in the home loan market doesn't change much when the basis is the size of the loan books. It has been ANZ, then ASB, then Westpac, then BNZ then Kiwibank for a long time.

But that belies the competitive nature of the market share fight on a week-by-week basis.

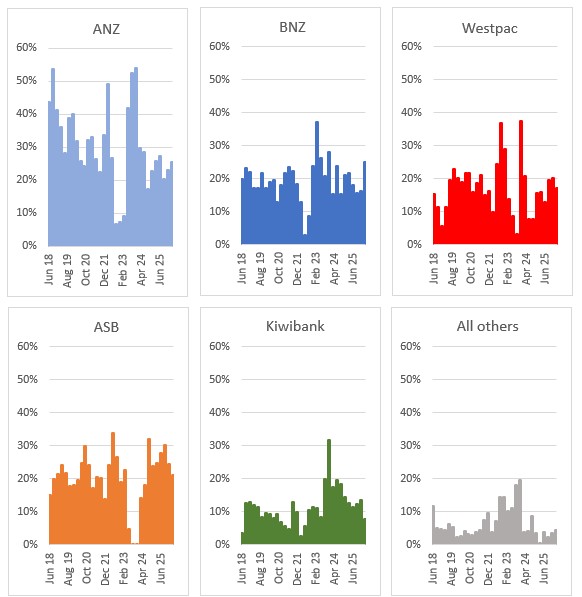

In fact, the quarter-by-quarter shifts in the changes of each bank's home loan book has now moved into an interesting place. New business is now being won on an even basis, each with about a 20% share, with Kiwibank taking about 10% now.

These charts tell the story from early 2018 to the first quarter (Q1) 2026.

All this data is from the Reserve Bank's quarterly Bank Financial Strength Dashboard. What we are measuring here is the quarterly change in each bank's mortgage book and relating it to the change in the Reserve Bank's overall C5 mortgage lending total for banks.

ANZ has the largest home loan base, BNZ has the smallest of the big four Aussie-owned banks. But that didn't stop BNZ scoring the same market share growth in the March 2026 quarter as heavyweight ANZ.

The other thing this eight years of quarterly tracking shows is that all these banks make market-positioning 'mistakes' where they lose share and momentum. Sometimes the recovery itself generates a rise in business recovered but that can be followed by the realisation that winning back new business doesn't always means it was a sustainable result. For example, ANZ pulled back sharply in late 2022 and early 2023, conceding share to BNZ and Westpac. ANZ's recovery push worked, but that may have been mainly because ASB then went into defensive mode. And then ANZ's impetus faded to a position worse than where it started.

The point is, even though the overall market share seems to move very little, there are in fact aggressive dynamics that shift home loan market shares month-by-month.

Over the eight year perspective of this data, ANZ has conceded market share significantly. ASB has built share, BNZ has been less inconsistent and is winning more than its long-term share, Westpac has tended to be a volatile competitor. Kiwibank hasn't been able to get its market share growth goals to perform consistently.

For borrowers, the lesson seems to be to be ready to shift your home loan because whichever bank has the 'best deal' now is unlikely to have it when you need to roll over your loan in one, two or three cycles of fixed rate contracts.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.