By Gareth Vaughan

Banks' financial rewards have been greater than the risks they've taken, and the Reserve Bank's proposals for banks to hold more capital would bring the reward down to something that better justifies their risk, Reserve Bank Governor Adrian Orr says.

"For every risk there should be a reward and when you look at the banking system globally that reward has been greater than the risk taken. And that happens because banks can take the returns, they don't have to wear all of the losses because the losses are socialised through bank bailouts and failure management and all of the things that we're still struggling to recover from in the GFC [Global Financial Crisis] globally," Orr told interest.co.nz in a Double Shot interview. (The video above is part one of a two part interview).

"So that reward has been in excess of the risk. We're saying 'let's better balance that.' Let's bring the reward back down to something where that better justifies the risk. So we're doing two things at once, we're lowering the risk through more capital, and if investors are struggling to say 'while there's a lower risk,' they should expect to get lower return."

"When I was running the NZ Super Fund we wanted to be rewarded for the risk taken. If we could find excess reward that was fantastic, let's go there. But for the banking system as a whole it's too critical. The fear of failure would create failure so we're saying 'let's reduce the risk,' and hence expected returns on equity would probably decline."

Society's risk appetite

In terms of what's being proposed by the Reserve Bank, Orr says the central bank and prudential regulator is working from the perspective of society's risk appetite, not any particular bank's risk appetite.

"We're trying to calibrate it to society's risk appetite rather than the risk appetite of a particular financial institution," says Orr.

"We know that society's risk appetite is less than a bank's risk appetite because banks get to privatise their earnings but get to socialise their losses. If they fail it's us, it's taxpayers, current and all future citizens, who have to pay for that bank failure. So we're trying to get a better balance. More capital means a safer bank. It means a lower risk bank, which means that they will have a better credit rating themselves, and it means that society is in a better, safer and more efficient position."

Asked about criticism of a lack of cost-benefit analysis in the Reserve Bank consultation paper Capital Review Paper 4: How much capital is enough?, Orr said the fact the Reserve Bank has talked about potential for higher mortgage rates, lower deposit rates, credit rationing by banks and an impact on Gross Domestic Product shows it is thinking about the benefit-cost analysis.

"What we're saying is that we believe more capital, and better quality capital, could cost a bank something. And we're not hiding from that. We think around 20 to 40 basis points additional premium between the costs at which they borrow and lend will be passed on because of them having to raise equity rather than just leveraging debt. So we're not hiding from that," Orr says.

"But the wider benefit is that their total risk is lower, their ability to attract equity will be cheaper because the investors will have a lower expected rate of return because they are a safer institution, and then beyond that the cost to the economy because we have more capital, safer institutions, our whole credit rating will be better."

"Our interest is the total cost not the [lending] margin. So yes, it may come at some impost to banks, but that is part of the game," Orr adds.

'We set the level of interest rates, banks set the margin and their profitability'

He also reiterates a point made in last week's Monetary Policy Statement about potentially using monetary policy to stimulate the economy during the proposed five-year transition period banks would have to phase in higher capital levels.

"If we see interest rates being too high for our purpose, i.e. some unexpected event happened, we can lower interest rates. Likewise we can raise interest rates. We set the level of interest rates, they [banks] set the margin and their profitability. So that has to be remembered across the country. They talk about their margin, we talk about interest rates as a whole," Orr says.

"Banks can retain more earnings, we estimated 70% of retained earnings over the next five years would get to the capital requirement. They can issue more equity, or they can start pulling their business back. And if they start pulling their business back there are other businesses who may fill those gaps. There's no shortage of people wanting to grow their balance sheets. Likewise the bigger end of town could issue their own debt. It doesn't always have to go through the banking system. So there are so many other things that could happen. It's not a 'hold everything else this will happen'."

"Also we've said we don't want you to get there tomorrow. If we agree that that's where we're going, we are saying 'at least over the next five years and we will talk with each of you individually because some banks have more work to do than others.' A lot of banks are already there, some are north of the number in terms of total capital," says Orr.

Five years for the phase-in period was a timeframe "plucked out of the air" and some banks could potentially have more time, he says.

"We want to all agree where we want to get to and then we can talk about what makes sense getting there. The interesting thing of course is that markets are forward looking ...we want to work with you, we want a sound and efficient and profitable financial system just as you do. Let's work through this properly. The current situation is sub-optimal, let's get to an optimal situation in a way that doesn't kill us on the way there."

For full details on just what the Reserve Bank is proposing for bank capital, see interest.co.nz's three-part series here, here, and here.

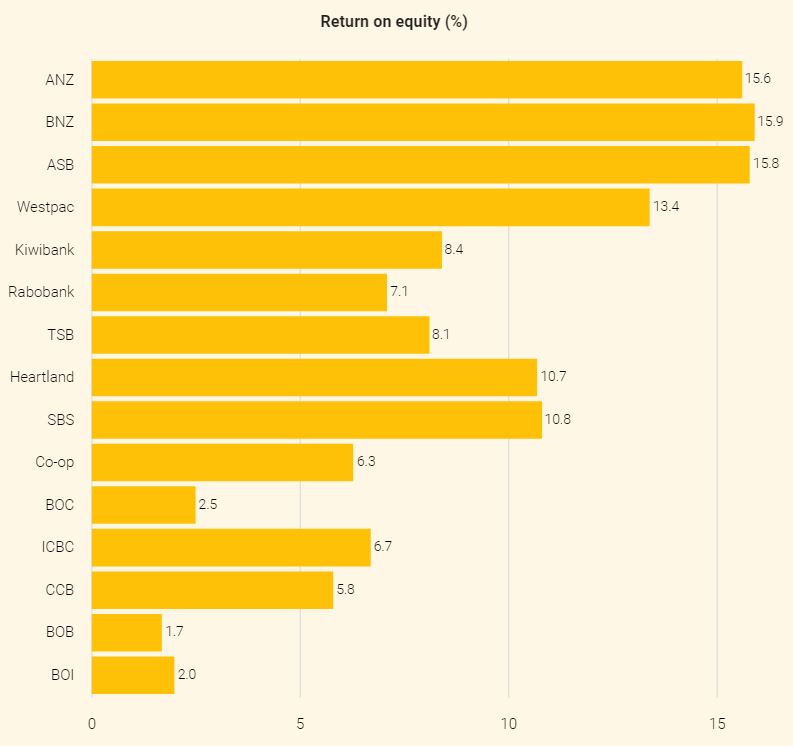

The chart below, from the Reserve Bank's Dashboard, shows banks' return on equity for the September quarter.

The Reserve Bank is seeking feedback, or submissions, on its bank capital proposals by Friday, May 3. It then aims to publish final decisions in the third quarter of 2019.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

53 Comments

I'm a little conflicted here. The risks that banks face is largely driven by their own behaviour, in that they lend out on high risk items without properly understanding the risks, or plainly just ignoring them. Or they invest impridently, not to mention paying exorbitant salaries to their executives. Why doesn't Orr just recommend or make rules that make the banks more accountable for the consequences of their own actions? Being liable for the customers deposits for one would do it in spades. For those who say that there is less risk then the banks will pay out less - they've rarely paid out for the level of risk to depositors anyway, so very little if anything will change. It still looks like Orr and the RBNZ is fiddling on the verge while the banks laugh at him.

Agreed

I dont know of any RBNZ head that has ever PLUCK A CAPITAL RATIO TIME PERIOD OUT THE AIR BEFORE.

ITS A DISGRACE and if this is the way the RBNZ is going to go about setting monetary policy it might as well hand it over to a local vote along with council election!!!!

THIS IS A TOTAL AMATUER HOUR FARCE!!!!!

the ratios up till now are based on the old gold standard of 6%. increasing the ratio is to complement the lack of regulation of finance industries by governments.

if you increase the ratio to far the economy will simple grind to a halt.

Like ships staying in port because it looks a bit windy out at sea.

Now the RBNZ which sent me a note saying point taken are trying to save face. it was a mistake to take this public so soon but its a clement Atlee moment for sure.

Bye Bye the economy of new zealand. Not a place to invest in anymore.

6 feet 4 inches.. is that a new record for the dummy spit here on interest.co.nz?

I think the issue lies in the fact that the big four are "too big to fail" or at least "too big to let fail", when the s#$% properly hits the fan we can demand they be accountable but by then it's too late - we (the tax payer) will end up carrying the can either way. Lifting capital requirements at least reduces the probability that things will get that far.

I think you are right, but Orr's actions tends to put all the liability on the tax payer, rather than the banks. The risks are still thoroughly socialised. Making the banks liable for depositors funds will change that.

Additionally the timeframes will give the banks ample opportunity to either figure out, create a way to avoid this burden or lobby against it when Orrs tenure as RBNZG is up.

Banks are liable for depositor funds; what do you actually mean, making the executives personally liable?

Correction, all deposits are the banks funds. The bank is your creditor.

Simple, any money deposited into a bank is by law the banks property. Some commenters use the language that it is a"loan" to the bank. However this is not correct as there are no terms that protect that "loan" for the depositor. The depositor simply becomes an unsecured creditor of the bank. At the very bottom of the list to be paid back if the bank gets into trouble. Worse - under the OBR, banks have the right to give depositors a "haircut". That is to legally take a portion of any deposit the save themselves, and reduce their liability to the depositor. They do not have to seek agreement in any way from the depositor. It is assumed to have been given when the deposit was made.

A simple test to check the balance in any relationship - take your mortgage document, and rewrite it to make the bank the mortgagee and yourself the mortgagor, in otherwords, reverse the relationship, and ask the bank to agree to it with respect to any deposits you have with them, and see what their response is. They are guaranteed to reject it out of hand. Indeed every bank will. There is simply very little to no legal protection for ordinary depositors. All the legal protection is to preserve the bank.

Banks are private business's. No other private business can do this with their customer's property. Ask yourself why?

No, its a loan banks are not liable for it.

murray86,

This is tinkering at the margins. Lord King,formerly Governor of the BOE laid out a way forward in his book, The End of Alchemy,Money,Banking and the Future of the Global Economy.

Very briefly,his proposal can be summarised thus; the aim is threefold. First to ensure that all deposits are backed by either actual cash or a guaranteed contingent claim on reserves at the central bank. Second,to ensure that the provision of liquidity insurance is mandatory and paid for upfront. Third,to design a system which in effect imposes a tax on the degree of alchemy in the financial system-private financial intermediaries should bear the social costs of alchemy.

Agreed Link. I struggle to understand why the powers that be just can't do their job properly.

murray86,

I believe that you are wrong and Professor Werner correct on the issue of a deposit as a loan,though few think in these terms. Of course,no loan papers are issued,nor the terms set out,but should the bank fail,the individual is treated as an unsecured creditor having made in effect, a loan without specified security.

This is correct I believe, ie its a loan.

Great interview thanks, Adrian Orr makes a lot of sense.

So basically going from the chart above, the big 4 Aussie banks are creaming it. I'm in full agreement with Orr, the banks should be able to stand on their own two feet and weather any form of GFC and never need bailing out.They are making money by just moving money about, they don't manufacture anything physical and can quickly tweek rates to make profits. I'm all for a stronger banking system where the "Profits" don't disappear but are fed back into the actual business in the form of a "Reserve" for when, not if things turn to s@$t..

Yeah but you've got to keep paying senior management multi million dollar wages each year for moving that money round - hiring the staff is an expensive business at a bank because they're highly skilled and there obviously aren't many people who could do their job...

Good interview Gareth. I found it interesting that Mr Orr brought up the subject of banks being 'bailed out' without mentioning anything about the legislation that means before they got to breaking 'depositor funds' would be bailed in... It's a bit of an oversight.

an acknowledgement of what would really happen

Great interview Gareth. Very interesting answers from Adrian Orr. It really shows he is actually looking to design a system that puts New Zealanders first, via lower systemic risk (to society) more competition (less of a competitive advantage for Australian banks), instead of looking out for the big four banks profits.

The bigger question is "Why is Adrian (the RBNZ as a whole) looking to change anything at all?"

If it's not broken, then don't fix it etc.

We've collectively had 10 years to do something about banking, and we haven't. We hoped an answer to what nearly killed us last time would come along, and it hasn't. In fact. the problem is bigger now than it ever has been.

So Adrian is doing something about it now ( and an answer to the bigger question is) "Because he's worried!"

He should be. Yes, additional capital might help; but not in 5 years time - now!, The fundamentals of banking are the problem, not the amount of insurance additional capital might give.Tinkering with capital ratios in't going to do all that much Adrian. You need to change 'how banks operate' ( and I'm sure you know that) but New Zealand doing so on it's own? Nigh impossible, unless YOU are the CEO and Chairman of all onshore banks ( nationalise them in other words, and enforce procedural change uniformly. You don't have to stage an economic coupe and wipe out shareholders etc. Just bring in uniform regulations that change ALL bank behaviour). But that isn't going to happen.

So add more capital to the balance sheets by all means. But I doubt it will help all that much if it's ever called on.

Fair points bw. I have a feeling that this will blow up before we get to 5 years. Aussie banks now under the watch of the rating agencies as house prices continue to scream lower.

"Because he's worried!" interesting observation. My view is I am petrified, I think the risk of a huge loss is certain and no amount of extra propiing up will help.

Meanwhile we as a society/economy continue to insist on more and more extraction of profit even on a system that is failing, bound to end well.

Common taters above are saying the banks should be liable for depositors funds. I agree totally. But but but. They are liable already, but if they go broke, there is no cash to meet that liability. Which is exactly why we are now expecting them to build a better reserve. Hopefully a much much better reserve.

Too many times they have taken the profits and socialised the losses. Executive's mostly don't care, the bank goes broke, misery for many customers, and they waltz off elsewhere.

A number of bank CEO's who were responsible when mortgage lending was growing rapidly in NZ have left the scene already

1) BNZ's new CEO started in November 2017

2) ASB's new CEO started in February 2018

3) Kiwibank's new CEO started in July 2018

A few have been around longer.

Westpac NZ's CEO started in February 2015

The ANZ NZ CEO was warning about property prices in Auckland in June / July of 2016.

KH, how are they liable? Depositors at best are only unsecured creditors, and what about the OBR "haircut" provisions?

I sometimes think that bankers, financial planners and tax accountants should indeed be held criminally liable if their advice and/or is proven to be negligent. Of course how do you prove negligent? from my perspective I expect a financial collapse ergo any "professional" advice is moot really, failure is certain.

Very interesting article. This is either going to make the RBNZ regulator of the decade or it’s going to be a costly theoretical mis-step. (MCI esque). If NZ banking is so profitable (which it is), why can’t the smaller banks cross the chasm and replicate this success? Perhaps the scale benefits are under estimated? Also, in theory, safer banks should pay less for deposits which will compensate for the additional capital they have to hold.

"Also, in theory, safer banks should pay less for deposits which will compensate for the additional capital they have to hold."

But in reality the big four get to use their own internal models, enabling them to hold less /pay less..

Internal vs standard model explains most of the chasm. The deposit reference is that if a bank is less risky(holding more capital) the risk premium it pays for deposits should be lower.

Noone is disputing the focus of ensuring NZ taxpayers are protected from having to bail out a bank... a notion that all nz taxpayers and all bankers would agree with.

Perhaps this will come in the 2nd half of the interview but I still haven't received a compelling rationale as to why the NZ banks are so inherently riskier than every other banking system in the world that warrants such a higher level of capital to anywhere else.

I would like to know why the RBNZ have thumbed their nose at the broader international direction for banking supervision which places greater emphasis on banks managing and understanding risks and instead put forward a regime that puts the RBNZ front and centre by defining a broad set of cookie cutter risk standards that all banks risks must fit in to.

I am not questioning the RBNZ's nobility or sense of purpose.. I am merely asking all to consider why do the RBNZ know more than other bank supervisors? What if the RBNZ are wrong?

Because the banks (here and overseas) have repeatedly demonstrated they are not capable of self regulation...and overseas regulators have not ben up to the job either.. Do you remember 2007.. Pepperidge farms remembers.. so does Orr.

Pragmatist is exactly correct. The banks have repeatedly demonstrated their inability to control their risk. So they have to be put on the leash.

Perhaps the banks have been on a leash... the RBNZ just forgot to hold on to the other end?

Again...let me make this abundantly clear.... I am not arguing for nothing to be done. Capital levels must increase.

The banking supervisors of the world have designed a complex and thorough risk and capital framework that is to be implemented prior to the RBNZ's. I am asking why the RBNZ have decided they know better than anyone else.

What reservations do the Reserve Bank harbour with regards the G20's BCBS proposals? What exactly are their concerns in regards to the FRTB framework?

You say the banks have repeatedly demonstrated their inability to control their risk. By the same token, have the RBNZ not repeatedly demonstrated their inability to supervise the banks?

You could just as easily ask the question what did any generation of banking regulators know that the previous one didn't as capital was progressively lowered from 100% backed to today's 2-3%!

"What if the RBNZ are wrong?"

What if the RBNZ is right?

The cost to society of the RBNZ being wrong is much less than the cost to society of the RBNZ being right.

What are the costs if the RBNZ is right?

Look at what happened to the banking system and consequences of failure of banks due to large asset writedowns, which then required bank recapitalisations:

1) in Ireland, and its subsequent impact on society, and the subsequent impact on the government finances

2) in US, and its subsequent impact on society, and the subsequent impact on the government finances

3) in Iceland and its subsequent impact on society and the subsequent impact on the government finances

4) in Greece, and its subsequent impact on society, and the subsequent impact on the government finances

5) in Cyprus and its subsequent impact on society and the subsequent bail in by depositors. The bank depositors took losses.

Would you as a bank depositor be willing to take losses on your deposit in order to recapitalise the bank? This is what the RBNZ is trying to prevent.

Just look at the losses by those depositholders / debenture holders in the finance companies during the finance company failures in NZ. I know quite a few retirees who lost their savings and are now struggling in retirement..

If the big banks fail in NZ and required depositor bailin, this would have a much bigger impact than the impact that the finance company failures had.

Recall, in the late 1980's the New Zealand government recapitalised the BNZ twice, due to their large exposures to corporate loans, and loans on commercial real estate at the time. Bank depositors were fortunate not to have had to bail in to recapitalise the BNZ. Look at the impact on the economy subsequently - there were business closures, and staff redundancies.

Imagine that you own a house. Do you choose not to insure it? You may think that the cost of insurance is too high and choose not to insure it as you do not think the costs are worth the benefit. Some others may choose to insure the house. Then something unexpected happens to your house - a flood, an earthquake, a landslip, a tornado, a hurricane, a fire, etc. If you chose not to insure your house, now do you wish that you had? It is too late ... Now imagine that the whole community chose not to insure their houses - imagine the impact on society as a whole ...

As the old adage goes - an ounce of prevention is worth a pound of cure.

The risks inherent in the NZ banking system are in the bank's loan book - in particular, residential mortgages - 60% of the loan assets of banks are residential mortgages. Look at the potential risks and vulnerabilities in residential real estate in NZ, and the leverage of households in NZ. Highly leveraged households are less financially flexible to deal with an adverse economic environment. A significant fall in the price of the underlying collateral for residential mortgages combined with a higher default rate could erode a significant chunk of bank capital given that banks are leveraged..

What are the costs if the RBNZ is wrong?

Due to higher capital requirements, banks make a lower return on equity, bank shareholders make a lower return, and senior bank executives get a smaller compensation. This is a much smaller group compared to the cost to society in NZ of a bank failure which would affect all NZ taxpayers.

One's perspective may be influenced by a person's own interests - perhaps a banker who stands to collect higher bonuses may be more focused on that and that may be of higher importance to a banker when compared to the overall long term welfare of society of NZ.

CN - Whilst it may well be a cost worth paying, I think its more than a bit naive to consider that bank executives and bank shareholders will be the only ones adversely affected by the new requirements - unquestionably it will also, and more so, impact deposit rates and lending rates for borrowers - the only question, a big one, is how much, and in what customer segment of lending in particular?

You continue to be disingenuous about this issue. Internal models are about reducing costs. Has an internal model ever identified the need for a Bank to hold MORE capital? No.

Internal models allow the big 4 banks a competitive advantage, while transferring the long tail risk to the deposits/taxpayers. Shareholders get the profits and the bank pays nothing for the additional risks.

As for overall capital requirements, NZ is a small country and has a highly indebted household sector. Why would we need to hold more capital? Why was Greece was treated differently from larger countries when they encountered a debt crisis? If NZ banks (internationally) are not too big to fail, they will be allowed to fail. Where banks in large more systematically important countries won't.

The globally proposed new internal capital models will require banks to hold more capital.

Yes internal models reduce capital relative to the standard method, but .. and here is the big issue, the banks must be able to evidence to the RBNZ that the internal models represent the risks more accurately than the standard model.

Apologies if you believe I am being disingenuous if I have failed to make my point.... but I keep stating the same questions with only the same standard rhetoric back about shareholders bearing the burden and nz is a small country. None of this is being disputed by me. I am merely asking someone, preferably the RBNZ, to provide some mathematical proof and logical reasoning into the extent they have stated capital needs to raise.

In the video Adrian Orr concedes the RBNZ doesn't have the resources nor the desire to police and challenge the banks on their internal models. That is startling because they are approved models by the RBNZ.

The boss of the NZTA fell on his sword for not ensuring WOF-issuers were up to mustard, yet we have the RBNZ Governor wilfully conceding they don't have the skills to monitor the 'WOF's' issued on the banks internal models.... and that's the banks fault?

never has so much been risked for the benefit of so few.

Banks can reach these targets in various ways

1) retain more earnings

2) issue more equity

3) pulling their business back - i.e reduce lending ...

Fragile by design

https://www.amazon.com/Fragile-Design-Political-Princeton-Economic/dp/0…

Fragile by design

https://www.amazon.com/Fragile-Design-Political-Princeton-Economic/dp/0…

I think the shareholders should bail out the banks. The good with the bad yeah?

In the event of a significant downturn, shareholder equity would disappear in a matter of months. Cash deposits (unsecured loans to the bank), go next... before a bail out would occur and there is no depositor guarantee in the event of bank failure in NZ.

I'd say a bit more capital seems like a pretty good suggestion, just 10 years too late.

Aussie mortgage delinquencies are on the rise... nothing dramatic yet, but they are going up and its not clear how the reckless Aussie parent could upset the Kiwi subsidiary. yes they are stand alone in principal, but funding could get sucked out of the system in NZ to deal with issues mounting over the ditch.

And then there's China, how much Chinese raised debt sits in our housing market?

By shareholders of the big 4 NZ banks, are you referring to the Australian parent banks?

If the Australian parent banks have problems with their own assets and have significant writedowns, then this may result in inadequate capital and liquidity at the Australian operations. The Australian parent banks may not be in a position to recapitalise their subsidiary banks in New Zealand.

Let it be done currency

I absolutely love that he keeps dropping the anti-competitive threat, a very articulate and forcefully made argument.

Hold on - this doesn't make any sense. Everyone has told me they pile all their money (or actually other peoples money) into housing...you know, bricks and mortar, because its 'risk free'. And given that everyone does it, shouldn't that mean that society has a very low risk appetite? So is housing and its associated debt low risk, or is it not low risk? Can someone shine a light on the truth? Because either society is BS'ing itself, or the banks are, or both society and the banks are BS'ing each other....how delightful.

It’s low risk in New Zealand. Prices double every 10 years, have done for the past 40 years so obviously they’ll just continue to double every 10 years into infinity. How you might ask? Well, mortgage rates will go negative. Try “22 percent” negative. People will be paid to take out mortgages.

Housing is only safe as long as growth is safe ... and growth is dead

Bank capital requirements will do squat in propping up the crash

Money is only a token for some pie

Its the pie thats the issue .... 7.6 billion in a collapsing ecosystem and nowhere to expand to

and Elon cant save us

https://stopthesethings.com/2019/02/11/renewable-storage-myth-busted-el…

The RBNZ role is to ensure banks operate in a way (specially their credit function) that prevents their collapse! Increasing the capital ratio requirement is a very lazy and in all likelihood ineffective response (i.e. in event of circumstances where the current 10% is not enough, it is very likely that the 15% wont be either! specially if there is no link between reserves and liquidity) from the regulator.

In theory you can even require banks to not take more than 50% of their assets in deposits, effectively matching every depositor's dollar with a dollar from shareholders equity. Effectively making the shareholders of a bank underwriters of bank debt to its depositors. However this is contrary to the very notion of a bank.

The issue at present is that the return to the depositors of bank is not really justified as they assume all the risks but the rewards are actually going to the shareholders instead of the depositors . A bank should ultimately belong to its creditors (i.e. depositors) and not "shareholders". Having a company/limited liability model for a bank is just wrong. This alternative ownership model already exists. I dont know why it is so unsuccessful in comparison to the corporate bank model

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.