BNZ has posted a 12% increase in half-year profit as its net interest margin fattened by six basis points with income up, and expenses and its loan impairment charge both down.

Net profit after tax for the six months to March 31 rose $60 million, or 12%, to a record high of $550 million from $490 million in the equivalent period of the bank's previous financial year. BNZ's profit was boosted by the sale of its 25% stake in Paymark to France's Ingenico Group. BNZ won't disclose what its gain on the Paymark sale was. However on Wednesday ANZ said it made a $39 million gain on the sale of its 25% stake in Paymark.

Operating income increased $32 million, or 3%, to $1.302 billion with net interest income up $76 million, or 8%, to $1.034 billion. Operating expenses fell $50 million, or 9%, to $492 million. The bank's credit impairment charge dropped to $46 million from $48 million.

BNZ's half-year net interest margin came in at 2.30%, up from 2.24% in the same period of last year. Its cost to income ratio dropped 120 basis points to 37.8%.

Over the six months from September 30 to March 31 BNZ grew gross loans by 3% to $84.9 billion, and customer deposits increased 2% to $59.7 billion.

"Operating revenue growth was supported by strong housing and business loan growth and improved net interest margin. Statutory net profit was impacted by the gain on the sale of BNZ's 25% shareholding in Paymark," CEO Angela Mentis said.

"In the first half of this financial year BNZ has increased its share of the housing loan market by 1.2x the market growth rate and helped more than 7,500 New Zealanders realise their home ownership goals, with 2,500 of those being first home buyers," Mentis said.

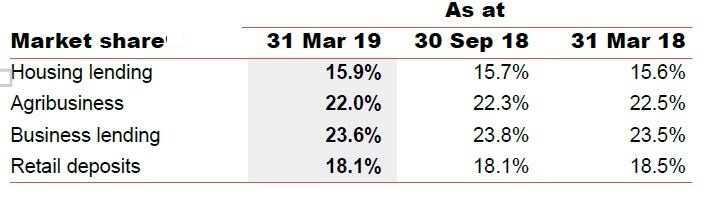

The table below shows BNZ market share figures, from parent National Australia Bank. This shows BNZ's share of the home loan market at 15.9% at March 31, up from 15.6% a year earlier. NAB itself posted a 7% rise in cash earnings to A$2.954 billion, with its return on equity unchanged at 10.5%. It's paying an interim dividend of A83 cents, down from A99c in the same period of last year, giving a payout ratio equivalent to 77% of cash profit.

'Repricing and/or reducing lending'

On the Reserve Bank of New Zealand's proposals for banks to hold more capital, NAB says based on BNZ's balance sheet at March 31, it would require a $4 billion to $5 billion increase in Tier 1 capital, or a 25% to 35% decrease in BNZ's balance sheet (risk weighted assets).

"Where risk-adjusted returns are not sufficient, BNZ will need to consider repricing and/or reducing lending," NAB said. Chief financial officer Gary Lennon also told analysts NAB could potentially constrain investment into BNZ as a result of the Reserve Bank capital proposals.

And here's NAB's interim results.

1 Comments

This is more evidence that the RBNZ capital requirements changes are going to be the driving factor in house prices over the next few years.

Internal models allowed the big four banks to allocate relatively low amounts of capital when lending to high LVR/DTI borrowers. So it remained profitable despite the high risk.

With a standardised model they will have to allocate significantly more capital to high risk borrowers (making it less profitable). So banks will be far less willing to lend unless you have a lot of equity and good income.

As with Australia it will be the flow of credit that triggers the price correction.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.