By Gareth Vaughan

The Reserve Bank of New Zealand's proposals to significantly increase the amount of capital New Zealand banks must hold should be a good thing for both banking competition and NZ taxpayers.

If adopted the proposals could challenge the near complete dominance of NZ's four Australian owned banks, which are among the world's most profitable. The proposals suggest a long-term focus from the RBNZ, somewhat akin to the long-term investment focus at the NZ Superannuation Fund, where RBNZ Governor Adrian Orr used to be CEO.

The RBNZ proposals announced in December would see NZ banks - led by ANZ NZ, ASB, BNZ and Westpac NZ - required to bolster their capital by about $20 billion over a minimum of five years. (For background and detail on the proposals and bank capital in general, and the nuts and bolts of what's proposed, see our three part series here, here and here. Additionally the RBNZ proposes to designate the big four as systemically important banks meaning they'd have capital requirements above and beyond other banks).

Get set for opposition from the big four banks and their allies, including business lobby groups and professional services firms, to ramp up in coming weeks. Key questions to keep in mind are who pays for increased bank capital, shareholders or customers? And who's on the hook if a bank fails, shareholders or taxpayers?

Make no mistake. The big four banks are very grumpy about these RBNZ proposals. This much is clear even though little has been heard from them publicly to date. The only big four CEO who has spoken publicly on the proposals so far is ASB's Vittoria Shortt. Speaking after ASB posted record interim profit of $630 million on Waitangi Day, Shortt warned of "unintended consequences" from the RBNZ's proposals, being "pricing changes" (read higher interest rates for borrowers and lower ones for savers) and "credit rationalisation," or banks limiting the amount of money they lend.

With ANZ, BNZ and Westpac reporting interim financial results in early May when their CEOs give media interviews, and submissions on the RBNZ proposals due on May 17, we're set to hear more from the other big banks.

The narrative will go something like this: The RBNZ's sums don't add up, NZ banks are very safe, banks don't need as much capital as the regulator is proposing, and if they're forced to make such significant capital increases, their Australian shareholders will invest elsewhere meaning all New Zealanders will suffer, risking the economy grinding to a halt.

NZ owned banks have a different view

A key factor that will become apparent though is there's not universal opposition to the RBNZ proposals across all of the country's trading banks. Far from it.

Kiwibank CEO Steve Jurkovich is already on the record as backing the RBNZ's capital plans. This is because they would largely remove the significant capital advantage ANZ, ASB, BNZ and Westpac currently enjoy over their NZ-owned rivals such as Kiwibank.

The Australian owned banks' capital, and thus profitability, advantage over their competitors is because they are allowed to use what's known as the Internal Ratings Based approach to credit risk measurement. All other NZ banks must use what's known as the standardised approach. This means the big four set their own models for measuring risk exposure which they must then get approved by the RBNZ. In contrast NZ owned banks, and other foreign owned banks operating in NZ, use the standardised approach with their credit risk prescribed by the RBNZ.

The upshot of this is the big four are able to stretch capital further than their smaller rivals, boosting their profitability. I spelt out the significance of the RBNZ's proposed levelling of the capital playing field in this article in December.

Interest.co.nz understands other NZ owned banks, such as The Co-operative Bank, SBS Bank and TSB, will - like Kiwibank - also back the RBNZ's proposal for a levelling of the capital playing field in a submission.

All up NZ has 17 banks registered with the RBNZ that offer retail banking services, - ANZ, ASB, Bank of Baroda, Bank of China, Bank of India, BNZ, China Construction Bank, Heartland Bank, Industrial and Commercial Bank of China, Kiwibank, Kookmin Bank, Rabobank, SBS Bank, The Co-operative Bank, HSBC, TSB and Westpac. Yet just four of them - ANZ, ASB, BNZ and Westpac - hold 88% of banking system assets, and also 88% of banking system liabilities.

RBNZ's proposals challenge big four's returns

Fundamentally the RBNZ's capital proposals spell lower returns for the big four banks, which last year made combined annual profit of $5.128 billion and paid their Aussie parents dividends of $3.39 billion.

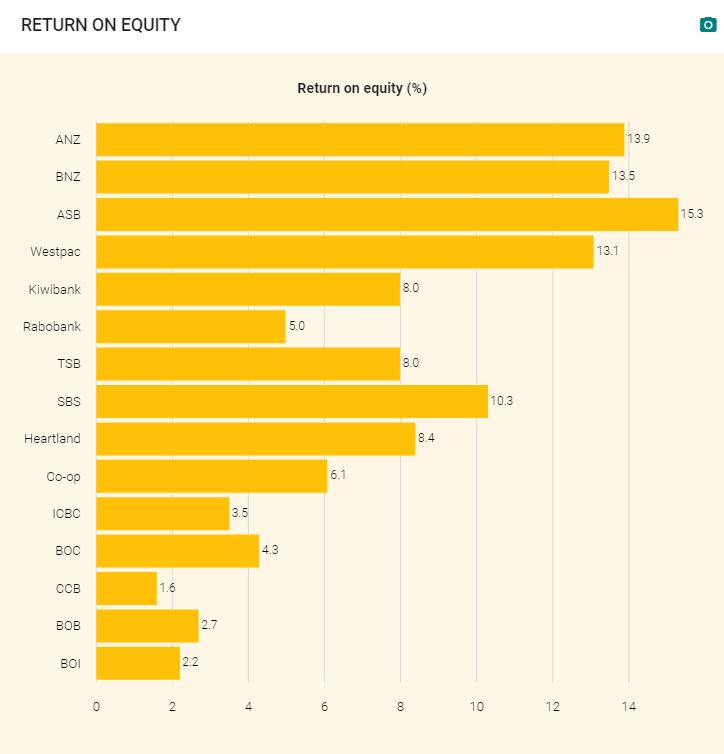

UBS banking analysts Jonathan Mott and Minh Pham suggest the RBNZ's proposals mean ANZ NZ, ASB, BNZ and Westpac NZ's shareholders would have to accept a return on equity of about 10% to 11%, significantly lower than where it has tended to be in recent years in the mid teens, or even high teens. The argument is that the big bank shareholders aren't interested in accepting returns on equity as "low" as the RBNZ capital proposals would inflict upon them given they can make better returns in Australia.

The RBNZ chart below covers the quarter ended December 31, 2018.

You can only charge what a market is willing to bear

Mott and Pham estimate the big four would want to increase their residential mortgage interest rates by between 80 basis points and 125 basis points, and probably also hike loan pricing for small businesses and dairy farmers, to maintain existing return on equity levels.

With the RBNZ proposing to phase in the increased capital requirements over a minimum of five years, perhaps NZ borrowers could absorb interest rate increases of that magnitude over that timeframe. However, right now the housing market in the key Auckland market is weak and the dairy farming sector is heavily indebted. Pushing through significant interest rate increases would slow the housing market further and risk fuelling an increase in banks' bad debts and potentially loan defaults.

The latest Real Estate Institute of New Zealand figures show sales volumes in Auckland were down 18% in March year-on-year, with the median price down $24,000, or 3%, to $856,000. And this is against a backdrop of assistance for the market from historically low mortgage rates (see chart below).

Neither dairy farmers nor SME owners appeal as borrowers that could quickly absorb a major increase in interest rates either. Federated Farmers latest banking survey shows farmer satisfaction with their banks at its lowest level since the survey began, with the Feds saying the Government's planned Farm Debt Mediation Bill would be "a useful tool in the tool kit." (Also see; Keith Woodford explains the decisions and behaviours that have led to dairy’s debt-laden pickle).

Meanwhile, SME owners not using their home as security are likely to already be paying close to double digit interest rates, and at least two non-big four banks - Kiwibank and Heartland Bank - are keen to grow their SME lending.

As Deutsche Bank banking analysts put it, (see more from them below), you can only charge what a market is willing to bear.

And then there's savers. There's not likely to be much room for the big banks to squeeze depositors much more. In this low interest rate world, term deposit rates are already historically very low (see chart below). And NZ banks need deposits to help them meet their RBNZ enforced core funding ratio (CFR) requirements. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum CFR for each bank - on a daily basis - is 75%.

At the time of writing the local five-year swap rate was just 1.77% with many economists predicting the RBNZ will have cut the OCR from its record low of 1.75% at least once by the time the RBNZ's expected to release its final bank capital decisions in the third quarter. Cutting interest rates on much needed deposits risks driving savers off in search of higher yielding investments, perhaps in the share market or property.

Fixed mortgage rates

Select chart tabs

Term deposit rates

Select chart tabs

Anyone fancy a haircut?

Another argument has been the Australian owners may sell some shares in, or all, of their NZ subsidiaries given the RBNZ capital proposals would lead to reduced returns for them from NZ. The problem with this argument is potential buyers of these businesses will understand exactly why the shareholders are selling, if any choose this path. Thus the price fetched for the NZ banks could be expected to be at a lower earnings multiple than the Aussie shareholders currently value their Kiwi subsidiaries at. In financial terminology that's called taking a haircut.

The big banks might "ration credit" in response to new capital requirements, slowing both the economy and their own business down. Something to keep in mind is if the RBNZ proposals go ahead, and the big four banks all act in unison in response, shouldn't the Commerce Commission be interested given their market dominance and hence market power?

Ultimately the best option for the big four banks to retain something near the status quo is to convince the RBNZ to water down its capital proposals.

How about lower dividends?

The focus of the proposed capital increase is so-called Tier 1 capital, which the RBNZ views as high quality capital, such as ordinary shares and retained earnings. In contrast to what UBS says, the RBNZ estimates the big four banks could meet the proposed new requirements by retaining about 70% of their expected profits over the five-year transition period, with no need to slow down the rate they've grown lending in recent years. It also estimates the increase in lending margins due to its capital proposals, the difference between bank lending and borrowing rates, will be 20 to 40 basis points assuming bank shareholders settle for a lower return on equity due to their bank’s lower risk profile.

Jack Do, director of credit rating agency Fitch, recently told me the big four banks "won't need to do anything extraordinary" to raise the proposed new capital, but suggested a rethink of their current dividend distribution back to their Australian parents would be required.

And Deutsche Bank analysts Matthew Wilson and Anthony Hoo note the unique NZ banking market structure generates oligopoly-like returns, given the big four banks "print an average return on equity of 15% and remit 65% of earnings bank to their parents as dividends." Wilson and Hoo argue that every time big Australasian banks confront an external threat to the industry structure they use alarm as a point of negotiation. By some estimates the RBNZ proposals would see NZ overtake Norway to have the highest bank capital requirements in the developed world. But given the NZ market structure, the Deutsche Bank analysts say the RBNZ action "appears quite sensible."

Reducing leverage

In a February speech Geoff Bascand, RBNZ Deputy Governor and General Manager for Financial Stability, spoke of how highly leveraged banks are compared to other businesses, arguing this isn't in the best interests of New Zealanders.

"When we talk about bank capital, we are talking about where a banks gets its money. Banks get their money from two sources – either from the bank’s owners, its shareholders - or by borrowing it, from people like us, often in the form of deposits. The money banks get from their owners is the bank’s capital. The rest is borrowed – it is ‘other people’s money’. The average New Zealand bank gets around 92% of its money by borrowing it. Compare this with the average business in New Zealand, for which this figure is about 55%."

"It is not clear to me why this discrepancy between banks and other businesses is so large, but perhaps at least part of it can be explained by the fact that, historically, governments have been much more reluctant to allow a bank to fail than other types of businesses, which may lead banks to operate closer to the edge. We believe that this balance of funding sources is not in the best interests of New Zealanders, which is why we are proposing change," Bascand said.

The RBNZ, he added, wants bank shareholders to have more skin in the game. Thus should the proverbial hit the fan, bank shareholders take a bigger hit meaning taxpayers face a smaller one.

"Put simply, skin in the game refers to the concept of having to bear the consequences of one’s own decision-making. By having minimum ‘skin in the game’ requirements, banking regulators ensure that the owners of a bank have something at stake, something to lose. I would like to note that banks themselves lend on these very same ‘skin in the game’ principles, for example, by requiring mortgage borrowers to provide a deposit," said Bascand.

In an interview in February Orr told me bank shareholders' reward has been in excess of their risk. And, Orr says, the RBNZ is working from the perspective of society's risk appetite, not any particular bank's risk appetite, making the assumption New Zealanders are not prepared to tolerate a system-wide banking crisis more than once every 200 years.

"For every risk there should be a reward and when you look at the banking system globally that reward has been greater than the risk taken. And that happens because banks can take the returns, they don't have to wear all of the losses because the losses are socialised through bank bailouts and failure management and all of the things that we're still struggling to recover from in the Global Financial Crisis globally," Orr said.

Whilst, unlike the US and UK there's been no banking crisis in NZ in recent years, BNZ required a bailout as recently as 1989-90. And there have been a series of banking crises in NZ, as detailed here.

The cats who got the cream

For many years the Bank for International Settlements (BIS), the central banks' bank, measured the profitability of major banks in a range of countries across a series of measures. For six consecutive years until 2017 interest.co.nz crunched the numbers for NZ's big four banks and added NZ to the BIS bank profitability benchmarking table. (We weren't able to do this in 2018 as the BIS annual report didn't include the bank profitability benchmarking table).

This exercise consistently showed the NZ banks near the top of the pack when compared to their counterparts from both advanced economies and major emerging economies, and ahead of their Aussie parents. Our articles on this can be found here.

The owners of NZ's big four banks have been the cats that got the cream over the past decade. The RBNZ's capital proposals threaten to end, or at least disrupt, their halcyon days. Should the RBNZ proposals go ahead unchanged there could be some short-term pain for borrowers and savers. Given the market power of the big four banks it's difficult to rule this out. But a level capital playing field ought to boost competition in NZ banking, and longer-term, should we face a banking crisis, taxpayers ought to be less on the hook than they would be under the current bank capital regime.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

42 Comments

“The RBNZ, he added, wants bank shareholders to have more skin in the game. Thus should the proverbial hit the fan, bank shareholders take a bigger hit meaning taxpayers face a smaller one.”

Taxpayers shouldn’t be on the hook for any business. This is nothing other than a systemic and regulatory failure that brings us to this unhealthy point. The RBNZ’s proposals would of course be unnecessary if banks didn’t create money/credit and were actually intermediaries anyway. Without correcting that, might win this battle but we will still be losing the war.

This connects to a conversation before easter about limiting credit creation and therefore growth. I asked then why we must have inflation as opposed to a stable system with neither inflation nor deflation. If the RBNZ were to require capital reserves, particularly tier 1, in a direct proportion to their loan books, in other words to the amount of credit they are giving, then a restrain by stealth would be placed an the perpetual growth assumption driven by the banks. as long as the ratio of captial to credit was less than one there would still be some growth, but at a ratio of 1:1 Stability should be achieved. Shareholders would then likely to have something to say on that, as profits would definitely suffer, as would the share price. but then survival of the planet is at stake....

A) Inflation is a form of compulsion in regards to consumption and purchasing thus “stimulating” growth. B) it erodes the value of our debts otherwise we couldn’t pay them back as most of our debt isn’t used for productive ventures. C) it is a stealth tax stealing the value of savings and taxing us more through bracket creep and gst.

Basically, at this stage not having inflation would be kicking the legs out from our economy and it would result in a lower tax take which is not politically favourable either. Great system eh?

I only agree partially with your points Withay. C is totally correct. B - partially. This is because banks have largely encouraged unwise borrowing, but private borrowing is essentially pledging future earnings. Borrowing for an over priced house, farm or other product is unwise, but well priced and stable, and therefore predictably valued items can lead to better spending. A stable system doesn't have to undermine the tax system or any other part, but it will change the way some parts of our economy do business.

But you are correct, the system has bought into the banks flawed view of the world and therefore is it's own biggest enemy. Changing it will take some courage.

'Orr told me bank shareholders' reward has been in excess of their risk'

Not on a total investment returns basis it hasn't. Aussie bank share price gains have been only mediocre over the last decade relative to many others, even before the Haynes effect. The populist 'cream' and 'halcyon days' narrative doesn't match the reality for investors. The risk cited by the banks of loss of shareholder support is valid as their shares begin slipping out of investors 'blue chip' category.

How important is shareholder support? The banks are private business's which are highly profitable. Raking off huge profits year after year cannot continue ad infinitum. Shareholders need to be concerned about the big picture not just huge profits. Banks provide a service to society, and are a part of society. If the banks are not concerned about the total effect of their business they are shooting themselves and their societies in the foot. the total banking model needs to change, and if that means the sharehiolders have to change their attitude, so be it. suck it up, it is time to be accountable.

Take an example, the CBA share price is in the vicinity a $70+. If it tumbled to $20, or even $1, what impact would there be on society if no other factor of the bank's business changed? Bugger all. Yes i understand that the share price is taken by many to be a measure of the health of the business, but the question is; is this necessary? I don't think so. There are many ways to measure the health of a business, and a lot of these are largely ignored. Take for example how can a business be healthy if the very society it operates in is ultimately threatened by its business and/or practices? Banks have acted as parasites for too long with little to no accountability. Time to change.

Murray86. Worthy sentiments but simple risk and return (capital and dividends) will continue to inform most investment decisions. The viability of any institution is dependent on ongoing shareholder support. Lose that support and you may be able to struggle on a for a bit with wounded but locked in shareholders but sooner or later you will need more capital and that's when the price is paid for the tub thumping politician and journalist anti bank campaigns.

Any business must be profitable to survive, and therein is the source of capital. shareholders raking off profits to line their pockets is something that must change. In banking especially, shareholders must be cognizant of the effects of their business on the economy, and ecology, and the resulting impacts on the business. they cannot continue to pillage profits without consequence. The insurance industry should aslo be required to maintain more capital too, as they too have evolved into a flawed model.

i dont think inflation is any of these things...in very simple terms it is the result of supply and demand . It is not a Tax of any kind.

I support any move that makes these banks safer. They are a key component. I don't really care that it's a change for the shareholders, because that's the business they are in, they have done very well and accordingly need to accept the downside.

KH. Yes, shareholders are well known for passively 'accepting the downside' aren't they. While your confidence they will do is endearing, it's regrettably not how it works. Haynes significantly knocked bank shareholder confidence and support, this will further rattle them. How much is yet to be seen but I suspect the patronising mindset towards NZ of many aussies will see most ignore Orrs bluster until the banks either downgrade guidance or tap shareholders for a capital raise. But to propose the banks will impose most of the cost of this on shareholders and that the price of borrowing will not increase substantially because of debt stress risk, is naive.

Appropriate time to re post the accurate Irishman.

Brilliant! thanks Rastus.

The sentiments in the video are accurate and would be dismissed by NZers in power ('the Irish situation was fundamentally different to that of NZ'), but the reality is that that no other industry has the privileges gifted on it like banking in the Anglosphere (which is arguably at the heart of the developed world's economic ills). I would go as far to say that the banks themseleves have created instability and strengthned their grip as the 'be all and end all' simply bcause of their power and ability to egineer 'noney into thin air' with a moral hazard that can easily be 'socialized'. The problem as I see it is that NZ (and Australia) is in a situation where the housing market is the foundation for our economy. And that is potentially worse than Ireland where construction activity was far greater leading up to the GFC. Ours has simply been about goosing the monetary sum in the house sale transaction.

Honey in the AIR? im amazed at the stuff people dream up here.

..... and not to mention the hardworking savers who will have their savings stolen by the banks in the case of a bank bail in!

Why is it stolen, have you ever read a term deposit PDS? You are an unsecured creditor and earn interest above the risk free rate because there is.....risk. There are ways to mitigate this risk if you are uncomfortable with it. I doubt you would argue (nor should you) bank shareholders should be inured from capital loss. Same institution, different position in the capital waterfall.

I agree in theory, in practise though we are essentially forced to use banks one way or another. We don’t have the option to deposit money into any bank that is actually secure forgoing the outlined risks.

In the case of an OBR bail in, would term deposits and saving accounts held money be used first (given they are interest returning and therefore riskier) before non interest returning transaction/cheque accounts?

Deposits are effectively stolen Te. They become the property of the bank when the bank takes possession of them, with little to no accountability to the depositor, hence the unsecured creditor bit - right at the bottom of the pile. Also remember the "haircut" provisions of the OBR where in times of strife the liability to those depositors can be reduced without any comeback. While the detail obfuscates this, the fact is this is legalised theft of depositors funds by PRIVATE business's with little or no accountability for the banks or the authorities. A preferable state would be that the depositors funds remain the property of the depositor, being on loan to the bank with the bank fully accountable for how they manage them.

As to the interest rates - what is the risk free rate of interest? Interst rates are so low at the moment, bank deposits are barely worth any return, and that interest IMHO certainly does not reflect that risks that are apparent from bank behaviour and how the worlds economics are going.

Bank with Kiwibank then. They are better capitalised then the Aussie banks and are, for all intents and purposes, NZ Govt. owned.

And still I wait for a compelling argument as to why the RBNZ is smarter than every other bank regulator by proposing a dumbed down capital regime that goes completely the opposite direction of ALL other bank regulators, including APRA.

All regulators are wanting increased capital and banks have conceded that globally, but all I have heard (and has been confessed by Orr) is that the RBNZ don't want to and cant be bothered ensuring banks systems and processes are up to scratch.

We will all end up paying more for the RBNZ's dereliction of duty.

Its more NZ is in a unique situation compared to other countries rather than every country should have the same regulation and Adrian saying ours is best. Somehow we ended up with the OBR and no deposit insurance scheme in place at what could be considered the end of a credit cycle. If NZ had chosen to build up a government backed fund to bail out bank depositors over the last 30 years then I think we would be a lot more tolerant of the risk of bank failure but right now there is nothing so this the chosen way out of situation and everyone but those with vested interests in the big 4's profitability seem to favor it or are at least ok with it.

Anyway andyb, I'm still looking for a compelling argument as to why our current regulations are suitable.

Not saying our currents regulations are suitable.. they are not... but the point I am making is global regulators are proposing new standards and a new methodology that raises the level of capital. Australian banks, including the NZ subsidiaries will have to hold more capital against their trading books from 2022 based on global standards which APRA are adopting. The RBNZ haven't been at the table, have concluded its all too hard and have taken the soft option of a dumb downed version rather than skill up and get on board with what is being proposed globally.

Maybe we should do away with the OBR and have deposit insurance. Fall in line with global standards.

Do we think that the dominance of 4 banks in the NZ market is so vastly different to other jurisdictions?

I think this quote sums up APRA's stance (and in doing so highlights RBNZ's error) "There are too many examples of financially sound institutions that frittered away their strength through poor risk management and reckless decision-making to suggest we can rely on stronger prudential metrics alone to deliver the requisite levels of safety and stability that the community expects"

Where do bankers get the idea that APRA has a good track record and should be used as an example of successful regulation? Do you consider Australia to have better managed its morgue lending?

Its too late to insure deposits without it effectively being a taxpayer funded bailout. If the Aussie or our own property market takes down one of our banks it will be in the next 5 years and their is no enough time to profit during the safe period (build up the payout fund) beforehand to cover much.

I'm also not a fan of compulsory deposit insurance either as it would reduces returns on deposits that are already low and I believe I can manage my own risk.

You only have to look at the RBNZ board and senior management to know they are definitely not smarter than everyone else. Mostly career bureaucrats with only limited commercial exposure. Only time will tell as to what the impact of these changes will be, certainly they haven't bothered to spend much time modelling them. I'm conflicted, I have little affection for the Australian banks but even less for sub-standard research on such an important issue. I'm left with the conclusion that this is being done to level the commercial playing field in NZ banking rather than a need to make NZ safer per se, the view is too much profit is leaving the NZ system for the risk being underwritten. I don't see this being a smooth transition.

Andyb, I'm still waiting for a compelling argument as to why ANZ, ASB, BNZ and Westpac should be able to maintain a significant capital advantage over all their competitors...

There is a compelling argument, it's that no NZ institution has shown the leadership, vision and risk appetite to step in and really compete. Kiwibank's execution hasn't been great (technology for example), but with $1b $2b of additional capital they would have the scale to move over to internal model and really compete. The capital is there, I just don't believe the average Kiwi cares.

Wow, thanks, amazing summary, Gareth. Can't see any reason either, why they should maintain a significant capital advantage over the competitors. But some pretty scary short-term pain scenarios. What's the old saying, could the cure be worse than the ill?

They have a capital advantage over the other banks as they have proven, to the RBNZ's satisfaction, that their internal modelling of their risks and exposures is better than the standard model used by other banks.

These banks have invested (and continue to invest) in their internal models and risk methodologies to ensure these models remain fit for purpose. I'd much rather have my bank invest in understanding its own risks rather than seeking to exploit the deficiencies of a broadly applied standardised model.

yes im afraid your right and that what we have here is that forcing a change in only 5 years time is just to short a time frame. These are not private banks but public companies and if they dont pay 4.5% to 5% dividends they will lose there shareholder funding base and basically start a slow road to no shareholder support. You might as well sell the banks to KIWI BANK.

The banks will fight back in ways that will be cruel to the market. The next time there is a problem in the diary market those farms will be sold up faster than labour drops policy under the table.

Not us.. not our policy!!!

Your farm is gone SON!!! GONE GONE GONE. Sorry we cant afford to carry your debts any longer.

Blame the reserve bank!!! We simply cannot afford to carry your debt laden shitty cow business any longer!!!

You cant change a business model this fast without a lot of PAIN for the borrrower and the COUNTRY.

The facts are they are PRIVATE banks. Their shares are publically traded, but not owned at all by the Government. that makes them private business's.

You are right that the business model cannot be changed quickly without pain, but that business model must change, as their practices about what they would loan on have been far too risky, but they have put the vast majority of that risk onto the borrower and depositor rather than being responsible for it themselves.

Sorry, where is the evidence that lending has been far too risky? ANZ, the largest NZ bank by far, just released the following today.

"The bank's credit impairment charge dropped to $32 million from $70 million, which was attributed to improvements in credit quality and a benign credit environment"

Mortgage loans on horrifically inflated house prices, without any consideration of the downside, and the same for farms. Those credit imparirment charges will skyrocket if the interest rates start going up.

That's your personal view on the future, however the results of NZ's largest bank show otherwise.

so you don't believe house prices were over inflated, or farms for that matter? Where have you been for the last few years?

so you don't believe house prices were over inflated, or farms for that matter? Where have you been for the last few years?

I believe in reality and facts over my own beliefs if that's what you mean. If the largest bank in NZ says credit conditions are benign, then they're benign.

You're own (and my) view on whether house prices are over-valued is irrelevant.

"The facts are they are PRIVATE banks."

WRONG on every count.

A private company and a public company are not the same. These are not private businesses but PUBLIC COMPANIES.

Edit; You are correct by a googled definition. I always understood a public company to be one owned by the taxpayer, but the definition is about the number of shareholders. I stand corrected. However that should not change the rules by which they are governed.

this is painful...generally speaking, "public vs private company" refers to whether the common equity is publicly traded or not. Public companies are listed on stock exchanges while private aren't. Different regulations (exchange listing rules) but in all other aspects the same.

Not painful at all. It is about learning, and sometimes what is learnt is a surprise.

However whether of not the share are publically traded to me is largely irrelevant. Yes I understand that shareholder support may be necessay to get some changes to the business axcross the line, but that is essentially about voluntary changes. I have been suggesting for a long time that due to their position and importance to society, Banks need to be very robustly regulated. In otherword, do not give their sharholders a choice!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.