Credit rating agency Fitch says it shouldn't be a difficult task for New Zealand's big four banks to meet the Reserve Bank's proposed increased capital requirements.

The Reserve Bank proposals suggest New Zealand banks would need about $20 billion more capital than they held as of March 31 last year. The increase would all need to come from Tier 1 capital such as ordinary shares or retained earnings, and be phased in over five years.

Fitch director Jack Do told interest.co.nz NZ's four Australian owned banks - ANZ, ASB, BNZ and Westpac - are well positioned to meet the Reserve Bank proposals.

"From where we're coming from, we see the proposals put forward as a credit positive for the standalone profile of the banks. Whilst the amount that they're asked to increase their Tier 1 and Common Equity Tier 1 equity ratios [by] is a significant increase from where they are, for these particular four banks given the strong profitability they generate, we think that they could meet them," Do says.

"It's not going to be a difficult task for them. They could meet that essentially just through profit generation over the proposed five-year timeframe period. In that respect when we say they're well positioned, they won't need to do anything extraordinary to raise it. [But] it will probably require a rethink of their current dividend distribution back to their Australian parents."

Between them the four banks last year paid combined dividends of $3.39 billion. That was equivalent to 66% of their combined annual net profit after tax, down from 73% in 2017. Fitch describes the big four NZ banks as having "strong earnings and balance sheets relative to many international peers."

Fitch suggests the four banks, which hold a combined 85% of NZ banking system loans, could use their strong competitive positions to increase borrowers' interest rates or ration credit to help them maintain profitability whilst working towards the Reserve Bank proposals. However, Do notes such moves would be against the backdrop of a low interest rate environment.

"There's probably not that much more they can cut on the deposit side," says Do.

NZ banks require deposits to help them meet their Reserve Bank enforced core funding ratio (CFR) requirements. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum CFR for each bank - on a daily basis - is 75%.

"We think that by increasing the capital that they need to hold there will be an impact on pricing [but] the quantum is not clear at this stage given we're not sure how it all will play out. If the amount of capital they need to hold is higher they have the ability and the marketshare to influence market pricing. It's likely they'll take that opportunity if they need to in order to maintain their profitability," Do adds.

Like rival S&P Global Ratings, Fitch says if implemented the Reserve Bank capital proposals would strengthen the four banks' standalone credit profiles, which it currently has at 'a' for all four banks.

"Our view at this stage is an increase in capital is credit positive for these banks," says Do.

Fitch has issuer default ratings of 'AA-' on all four banks. The outlook for ANZ NZ and Westpac NZ is stable, whilst it's negative for ASB and BNZ due to issues at their parents Commonwealth Bank of Australia and National Australia Bank. (See credit ratings explained here).

See interest.co.nz's three part series on the Reserve Bank capital proposals here, here, and here, plus an interview with Reserve Bank Governor Adrian Orr on the proposals here. The final date for submissions on the proposals is May 17 with the Reserve Bank saying it will make final decisions in the third quarter of this year.

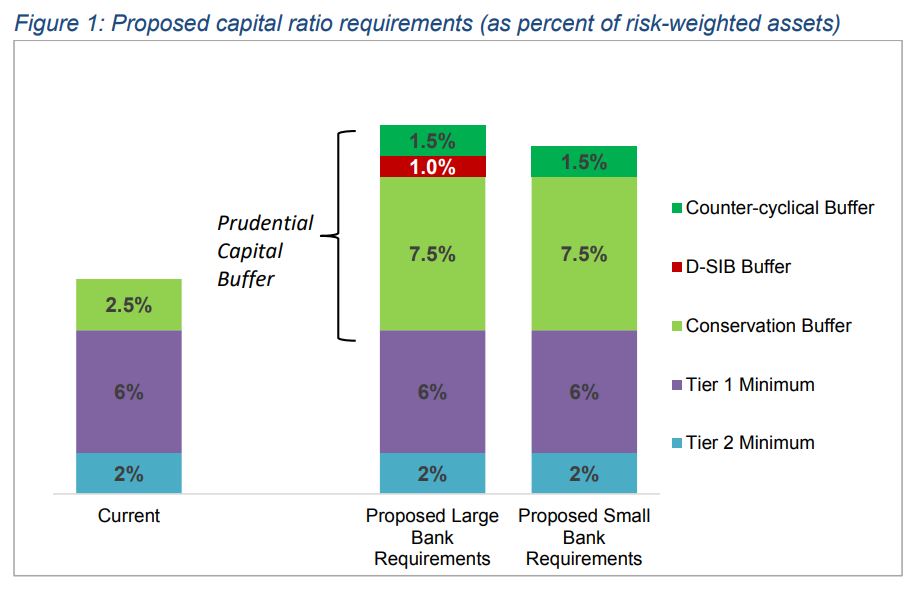

Figure 1 below comes from the Reserve Bank.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

2 Comments

My thoughts exactly. All the wheeling & squealing from The 4 is just noise. We all now know how greedy your average Australian Bank is. It's an A on the Greed Scale.

In its current form it will have considerable consequences for not only borrowers, depositors and shareholders, but the economy itself. It isn't just the Big Four pointing this out strongly, but the majority of those doing independent analysis, and the many NZ corporates who are also rapidly submitting submissions to the RBNZ desperately trying to get it moderated - don't let the uninformed comments such as the other one on here delude you into thinking anything else - fortunately I get the feeling that the RBNZ knows its got alot of it wrong, and although it won't be like a complete Labour CGT back flip, we're going to see a far softer version come the Sep RBNZ final decision.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.