By Gareth Vaughan

The Reserve Bank (RBNZ) proposals to significantly increase bank capital requirements are sensible given New Zealand's unique market structure, say banking analysts from Deutsche Bank.

In a report on the RBNZ proposals, Deutsche's Australian-based analysts Matthew Wilson and Anthony Hoo note the NZ banking system is highly concentrated with four foreign (Australian) owned banks controlling 88% of system assets.

"This unique market structure, we are yet to find another one, generates oligopoly-like returns. The four banks print an average return on equity of 15% and remit 65%, or NZ$3.25 billion, of earnings back to the parents as dividends," Wilson and Hoo say.

They go on to say each time the big Australasian banks - ANZ, ASB's parent Commonwealth Bank of Australia, BNZ's parent National Australia Bank and Westpac - confront an external threat to the industry structure they use alarm as a point of negotiation.

"E.g. may cause funding problems, may lead to credit rationing and may de-stabilise the economy. We heard this in the lead-up to the Murray Inquiry, in response to its key final 'unquestionably strong' [capital] recommendation and in the lead-up to, and during, the more recent Hayne Royal Commission. The same tactic is being used in response to the RBNZ call," say Wilson and Hoo.

They estimate the RBNZ proposals would cut the big banks' return on equity by about 300 basis points. To hold return on equity steady Wilson and Hoo suggest the banks would need to increase their margins by 50 basis points, but note "you can only charge what a market is willing to bear."

Thus in response the Deutsche analysts suggest the big four banking groups will transfer what excess common equity tier one capital they have in Australia to NZ. Additionally they will "more sharply manage" the shape and size of their NZ balance sheets, consider a partial NZ share market listing of the NZ subsidiaries, and cut their "unsustainably high" dividend payout ratios.

"Whilst a partial listing would likely be welcomed by NZ investors and the broader NZ economy, it creates some capital/tax inefficiencies for the parent and thus may not be the most preferred outcome," Wilson and Hoo say.

The Deutsche analysts also note changes by the Australian Prudential Regulation Authority (APRA) to its related parties framework, prudential standard APS222. This restricts exposures between the big Aussie banks and their related entities. Currently the standard sets the restriction at an aggregate exposure limit into each subsidiary, whether debt or equity, of 50% of the Australian parent's level 1 tier 1 capital. However, in July last year APRA released a discussion paper proposing to lower the requirement to 25% of the Aussie parent's level 1 tier 1 capital.

Wilson and Hoo point out this increases the sensitivity of related-party investments.

"We expect the major banks to actively consult with APRA on this proposal...at level 1, the New Zealand major banks are deconsolidated and the capital investments into these subsidiaries risk weighted at 400%. This is particularly relevant when dividends are upstreamed and then reinjected as equity capital in the subsidiary."

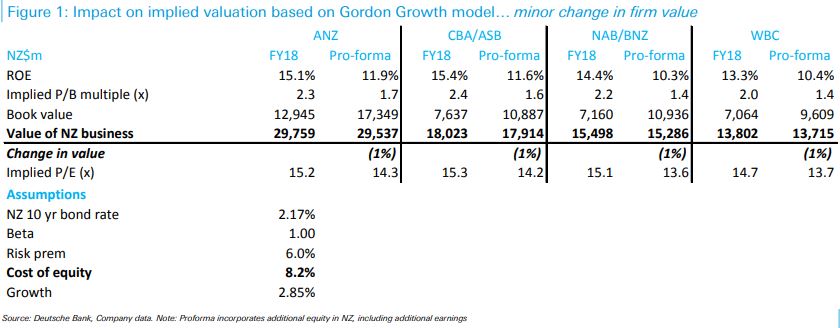

By Wilson and Hoo's estimate the increased capital requirements would reduce the big four NZ banks' valuations by just 1% (see table below). Given the entire value of share market listed NZ equities is NZ$130 billion, the Deutsche analysts suggest only a partial listing of the big four banks would be digestible. A partial NZ listing of certain banks might be a "sensible and well received outcome," they say, adding weight and certainty to the NZ equity market plus creating a vested interest in a bank's customer base.

NZ banks must currently meet a minimum total capital ratio of 10.5% of their risk weighted assets. The RBNZ is proposing to increase this to 18% for banks identified as ‘systemically important’, ANZ, ASB, BNZ and Westpac, and 17% for all other banks. Within this proposed increase from 10.5% to 18%, it's proposing to increase the minimum capital requirement for tier 1 capital from 8.5% to 16% for systemically important banks and 15% for all other banks. The RBNZ additionally has a minimum capital requirement of 2% for tier 2 capital. However, the RBNZ is questioning whether this lower quality Tier 2 capital is needed.

Also see interest.co.nz's three part series on bank capital here, here, and here, plus our video interview with RBNZ Governor Adrian Orr on bank capital here, The deadline for submissions on the RBNZ proposals is Friday, May 3. The RBNZ then expects to publish final decisions in the third quarter of 2019.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

11 Comments

"Sensible". Then lets do this.

Thanks for the endorsement.

https://www.stuff.co.nz/business/world/88527342/deutsche-bank-to-pay-us…

I was banging about this last year in Tauranga with Grant Robertson at breakfast meeting.He appeared to concur and wanted to receive the recommendations from the RBNZ.

Now get on with it is all I can say.

Note in particular:

“each time the big Australasian banks - ANZ, ASB's parent Commonwealth Bank of Australia, BNZ's parent National Australia Bank and Westpac - confront an external threat to the industry structure they use alarm as a point of negotiation:

- Funding problems;

- Credit rationing;

- De-stabilising of economy”

There is no basis for these alarming claims, hopefully the RBNZ will not lose its resolve to implement its (long overdue) proposals.

The banks wouldn't want to overplay their hand. Their license could be taken away if they present themselves as a threat to the nation. Also given the state of the Australian banks they need the income from New Zealand badly. How badly we will have to wait and see.

At last some sensible commentary from bank economists that are not captured. The capital proposals are absolutely on point and about time. Only good can come of this for the NZ financial system, and NZ in general. Like CGT, vested interests will bleat and complain, but this change is not only warranted and necessary, it is fundamental to developing a New Zealand that has a future.

Sensible so long as the majority of NZers are happy to pay the price to cover that one in 200 year event that the RBNZ describes its designed to cover - its the same as saying let’s double the premiums insurance companies charge to ensure that an insurance comopany can never fall over - if thats what you need, yes pay the price

And yet...Ian Harrison, Tailrisk Economics, has this to say:

The Bank’s assessment that the banking system is currently unsound is at odds with rating agency assessments and borders on the irresponsible The rating agencies’ assessment of the four major banks is AA-, suggesting a failure rate of 1:1250. The Bank is now saying that, at current capital ratios,the banking system is ‘unsound’ because the failure rate is worse than 1:200. Or in other words the New Zealand banking system is not too far from‘junk’ status.The international evidence does not support the Bank’s contention that the probability of a crisis is worse than 1:200.The Bank has ignored the fact that banks will need to hold an operating margin over the regulatory minimum,and has not adjusted New Zealand capital ratios to international standards to make a fair like-for-like comparison.

We've never known rating agencies to get it wrong, either.

Is this just so much eyewash, or is it real?

NZ banks must currently meet a minimum total capital ratio of 10.5% of their risk weighted assets. The RBNZ is proposing to increase this to 18% for banks identified as ‘systemically important’

Er, but isn't "risk weighted assets" just code for "magic made up numbers that look good"? Is this yet more smoke and mirrors and deception?

Alan Greenspan recently said that he now thinks all this stuff is nonsense and the only thing that might work is equity of 20% to 30% of the unadjusted loan book.

All is not well down on the Kiwi Debt Farm. The livestock are getting restless. The oligopoly of Aussie bankers and their captured pet poodle the RBNZ have inflated house prices to silly levels and thus destroyed our confidence in our democratic institutions. We thus argue amongst ourselves, exactly as Lenin intended and as Keynes warned us back in 1919.

R W,

Your comment on 'risk weighted assets' is on the money. Have none of the lessons of the GFC been learned? As Mervyn King pointed out in his book The End of Alchemy,that house of cards collapsed when credit dried up and trust evaporated. Leverage ratios would have been a great deal more useful.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.