The Reserve Bank (RBNZ) is upping its bond buying, as financial conditions tighten and markets bet on rising inflation and interest rates.

The central bank plans to buy more New Zealand Government Bonds via its Large-Scale Asset Purchase (LSAP) programme this week than it has every week over the past five weeks.

Its “indicative schedule”, published online, is to buy $630 million of government bonds on the secondary market this week - an increase from the $570 million a week it has been buying since the beginning of February.

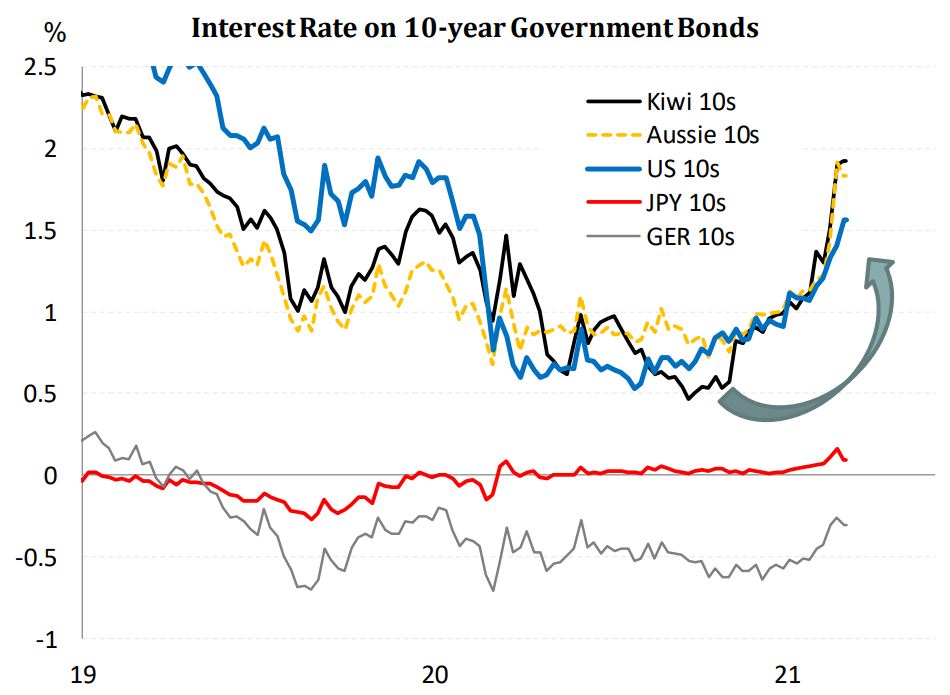

The tweak comes as bond yields in New Zealand and around the world rise (as per the Kiwibank graph below) and financial conditions tighten:

This is the opposite of what the RBNZ is trying to achieve through its monetary stimulus - IE it cutting the Official Cash Rate to a record low, and launching an LSAP programme worth up to $100 billion and Funding for Lending Programme worth up to $28 billion.

Monetary policy stance unchanged

It’s important to note RBNZ staff, not the Monetary Policy Committee, are responsible for adjusting weekly bond purchases.

A RBNZ spokesperson confirmed to interest.co.nz this is done for operational reasons and maintaining market functioning, and does not signal a change in the stance of monetary policy.

“There are many factors that will determine the amount of bonds purchased under the LSAP, including the size of the government bond market in June 2022,” they said.

Lower govt debt issuance a constraint

The RBNZ’s move to up its bond buying follows the Reserve Bank of Australia much more aggressively doubling down on its purchases via its version of New Zealand’s LSAP.

However, the RBNZ is somewhat constrained by the fact an indemnity provided to it by the Crown restricts it from buying more than 60% of New Zealand Government Bonds on offer.

It's bought $45 billion of New Zealand Government Bonds to date, which is equivilent to 40%-50% of the bonds on issue.

Because Treasury is issuing fewer bonds than it planned to issue when the LSAP was launched last year, the RBNZ might hit this 60% cap before it hits the $100 billion cap on the programme.

In other words, it might have no choice but to slow its bond purchases. Also, purchasing more bonds now reduces its optionality later.

'We’d expect jaw-boning to be the primary method of influencing market interest rates'

ANZ senior strategist David Croy, and senior economist Liz Kendall, made these points in a note they wrote last week.

They said that should the Monetary Policy Committee (MPC) wish to use the LSAP to more aggressively lower bond yields and thus interest rates to boost inflation and employment in line with its mandate, the Committee would need an emergency meeting.

“If the MPC is concerned that yields have risen prematurely and might unduly weigh on the outlook, we’d expect jaw-boning to be the primary method of influencing market interest rates,” they said.

“Swap market intervention is also a possibility, given the current lack of headroom to meaningfully ramp up the LSAP.”

However, Croy and Kendall said the MPC would need to be confident this would be effective.

Asked on March 4 for his response to the rising bond yield situation, RBNZ Governor Adrian Orr said: “We will be assessing how economic conditions unfold and whether we need to be doing anything with our monetary policy stance.

“At present it is far too early to have any concern over what we’ve observed. We’re still in the watching and waiting game.”

RBNZ could intervene in the name of financial stability

Croy and Kendall said it would be easier for the RBNZ to intervene in the bond market wearing its financial stability hat (rather than its monetary policy hat), by employing its hardly-used Bond Market Liquidity Tool to address dysfunction in the bond market for example.

They concluded: “Given the RBNZ’s limited firepower, and the high hurdles to action, it is difficult to see the RBNZ attempting to alter the medium-term trajectory of New Zealand Government Bond yields, which are heavily influenced by the direction of global (in particular, US and Australian) yields.

“Given the Federal Reserve’s apparent comfort with higher yields and the Reserve Bank of Australia’s caution, that speaks to New Zealand bonds potentially outperforming US Treasuries but underperforming Australian Commonwealth Government Bonds.”

Interest.co.nz last Tuesday talked to RBNZ Assistant Governor Christian Hawkesby about how the RBNZ might respond to rising bond yields:

55 Comments

and the market manipulation goes on, and on and on and on.

So when people say capitalism has failed you must correct them and say What capitalism?

That’s what I say. This ain’t capitalism. Where’s the creative destruction? Where’s the accurate pricing of risk? Where is price discovery? The system has been destroyed by unbridled financialisation and then by central bankers.

Capitalism replaced by creditism, 'Balance Sheet Usage', wealth effect mentality/ bubble surfing. Frolicking in the fantasy that we can borrow our way to prosperity, says Charles Hugh Smith, who talks about disruptions in supply chains and insolvencies being a Catalyst to reduced money supply and reverse wealth effect

Or you could look at the RBNZ as a 'market maker'.. both views have some truth.

Of course the creeping momentum to the 60% bond ownership ceiling is the real story. At which point [if we get there] bond yields could spike as their main purchaser; the RBNZ is removed from the market. Stating the obvious I know.

We must keep the housing market functioning. I heard it was breaking down in Tauranga.

I heard it was even worse - dysfunctional.

They need more Balance Sheet Usage.

"we’d expect jaw-boning to be the primary method of influencing market interest rates" - LOL; King Cnut (Orr) looking more desperate by the day to keep the housing Ponzi alive. Higher interest rates are coming, like it or not.

Higher interest rates are not coming anytime soon they are buying bonds to keep the bond interest low. Increasing the OCR increases their interest debt which they can not afford to do because their income tax take is shirking. So you are right its a Ponzi scheme and to keep the Ponzi scheme going they print more money because it can be created from nothing. So the RBNZ creates money from nothing prints it and then goes and then pays the government with it to buy its bonds which is then classed as an asset held by RBNZ. Its actually counterfeiting and highly illegal if you or I did it but its ok for the RBNZ to do it.

Great post Mr Pink

MrPink... do you believe that the RBNZ has complete control over the OCR? Of course they announce and set the rate but.....

RBNZ is not god, they don't have complete control of the situation. If they have, then GFC would've not happened. Yes, they can not afford to increase OCR. But sometime it's not about what they want to do, it's about what they have to do.

You expected the RBNZ to prevent the US sub-prime crash?

The RBNZ can do whatever it wants as long as we are in line with our trading partners monetary stimulus. We have discussed this before, if the RBNZ is more aggressive then the NZ$ will weaken on a trade weighted basis and vice versa. Most commentators evaluation of the RBNZ is blinded by their resentment on house prices, but it's little different to Aust, UK, Europe, USA etc. The RBNZ still have a lot of tools to stimulate the economy. The average Sydney auction price is $1.7m - so NZ$2m with stamp duty.

"The RBNZ can do whatever it wants as long as we are in line with our trading partners monetary stimulus. We have discussed this before, if the RBNZ is more aggressive then the NZ$ will weaken on a trade weighted basis and vice versa."

At least someone round here understands. There's little point in getting too hung up on what the RBNZ are doing, rather keep an eye on the fed and the rba. Breaking the ponzi will create upheaval and they'll do everything in their power to avoid it.

Sorry did you just say that the RBNZ is now actively suppressing interest rates? my understanding is that buying bonds reduces interest yields

bonds are super important because they are benchmarks for risk

Was all of the RBNZ trained in Ben Bernankes masterclass? aka the giant experiment...? I suppose if the whole world does it then its ok right?

The fundamentals have changed to the central bank will bail us all out every time - when does it all become "too big to bail?"

Must be different this time...

Central Banks have been slashing and suppressing interest rates since the GFC, manipulating markets to artificially raise asset prices - in order to induce their beloved ‘wealth effect’. They’ve induced the biggest debt binge in history, an absolute house of cards.

The tweak comes as bond yields in New Zealand and around the world rise (as per the Kiwibank economists’ graph below) and financial conditions tighten:..

This price service claims the 10 yr closing price today is ~1.90%. A significant fall in price from a low yield recorded at 0.498% on 13th May 2020, despite non stop LSAP actions from $10.377 billion on that date to $48.478 billion today.

What's the chance of Wicksell's prognosis coming to fruition?:

A high level of liquidity preference, the low level even lack of economic growth to provide opportunity causes investors to seek refuge in what they consider to be safe liquid assets. The consequential rise in sovereign bond prices reduces term interest rates, which in turn increases the discounted present value of cash flows associated with all assets and liabilities, but not much else.

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

"[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar.

Friedman pointed out the basic, non-trivial distinction between a liquidity effect and an income effect. Low rates can be stimulative in the short run (the liquidity effect), but over the long run their persistence means something far different. A yield curve is supposed to be upward sloping given the core time value of money and investing. That arises from opportunity cost, meaning the more plentiful the opportunities the greater the time value and the steeper the curve (the income effect). Yield and/or money curves (the eurodollar curve and even the history of the OIS curve) that collapse and remain that way unambiguously demonstrate that "stimulus" deserves only the quotation marks.

The more only the government can borrow, the more only the government does borrow. And the more the government does borrow, the harder it is to get the economy growing The more difficult it is for meaningful growth, the more banks will only lend to the government. Link

A quote from your other link, worth repeating:

Jerome Powell .... declined to say that rising bond yields are inconsistent with the central bank’s objective. That essentially gives the market a free rein to push yields higher, keeping Treasuries as the potential source of volatility for other markets.

High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar.

And of course this created the very few, very wealthy families/class in the US arising out of the GD.

Orr just cancelled his laxative order

Print, baby, print! We're going to send this asset bubble to the moon.

Doom loop leading to doom vortex...... For anyone who follows George Gammon on YouTube he’s just uploaded a video explaining how the FED will attempt to control the yield curve and what the implications are. Either way it’s bad!

There is no need to print... As banks are awash with customer deposits which means the economy is strong...

Was it last week that Hawkesby said that they are in the 40%-50% range of total bond market already? Love to know more about where exactly that sits. Will be interesting if they are hurtling towards that trying to beat the market.

Here's a chart from ANZ showing which NZ Govt Bonds the RBNZ holds the highest shares of. It already owns around 50% of the 2027s, 2029s, 2031s, 2033s and 2037s.

And yes, Christian Hawkesby last week said the RBNZ was getting to around 40-50%.

Confirm their mandate is no more than 60% for the market to function correctly?

I get a strong feeling this will end up in a textbook one day detailing a complete disaster.

When the real world comes knocking the RB and central banks around the world will have no ammo left as they've been too busy thinking they know best. Do we really need LSAP? Markets seem to be doing just fine.

Why are they not so pro active even after acknowledging that house prices are rising on multiple digit on a weekly basis.

Points to Ponder.

One reason that everyone should borrow as much as - come what may Jacinda Arden and Mr Orr has more to loose if individual default and also if the market falls, so let them worry.

Market down for just a week and they are shit scared. Market from now will always blackmail them to support and each time they will, will have to come out with a bigger support BUT for how long.

No one believes in : Let economy takes it own course for healthy market.

Its just a question of time before the FED also increases QE, its not that inflation won't hit but who can actually foresee rates rising in the US when they have a massive trade deficit, a huge debt load, 10% unemployment, and an economy that 50% of its output is useless service sector junk that disappears in the blink of an eye?

US Government default seems like the only way out, or a war.

Or both

Idiots

"Dysfunction" always happens to be defined as prices of the asset in question dropping.

Nevermind that this dropping is a rational response to unfolding data, just the market finding a new equilibrium price of the asset.

Whereas "normal" markets are ones that go up continuously regardless of fundamentals. What a bizarro world.

A normally functioning market is now the thing central bankers must prevent at all costs. Now they’ve created their bubbles they must defeat and destroy the market in order to defend them.

Correct, now market will only function and survive with support from reserve bank a and government or........

Short term narrow mindset responsible for the situation. Did they save the economy or have sowed seed of destruction.

You wonder who they try to confuse.

Excellent. I suspect there're much more easing to come.

There's still plenty of room for real assets upward valuation.

Maybe people might get tired of having so much money that they don't know what to do with it. I suspect quite a few people are suffering from such scenario currently.

House price to double shortly if this continue as already multiply by 4% to 7% on a monthly basis, if not weekly.

Destroyed the economy and market. Damaging in name of coronavirus.

"to address dysfunction in the bond market"

No! The bond market is functioning exactly as it always has, inflation is clearly with us and that makes bonds a bad deal at current yields, hence the selloff.

The govt/RBNZ wants it cake and to eat it too in the form of low OCR and inflation at the same time to inflate away the debt.

End result is financial repression

All this “what about the market” sobbing, Jesus, that is the same ‘market’ that led us to gross inequalities, rampant profiteering, and investors who have come to expect a nice safe Govt guaranteed place (gilts) to put their money. What the last year has shown us is that the interest rate (like the OCR) is a policy variable. It is not set by the markets, not something that Govts have to solemnly observe and meekly respond to; it is determined by Govt. Now can we get on with using that knowledge to tackle housing shortages, infrastructure failings, net zero carbon, and child poverty?

Personal loan and some credit card rates on the way down, more people will be hooked. Happy spending and forever working for the system! Everyone is happy.

True. Private debt as a % of gdp (and rate of change of the same) and affordability of a decent life are the two indicators that actually mean something. But we talk about gdp and unemployment - both of which measure diddly squat in the real world.

The RBNZ cannot print bitcoin.

Think about it.

They also can't print

- houses

- Water

- Food

oh and Tom, Dick, and Harry Coin

Think about it.

Actually they probably could 3d print houses...

or gold

The more they pull the string the harder it will break. It is time for central banks to face reality and admit they have been continuously making the mistake of trying to postpone the problem instead of letting the economy deal with it.

Actually it's past time for that as if they let it go now, there would be a massive explosion, making 2007-10 look like a turtle fart. Now they can just keep doing the same thing and hope it will be different this time.

In many respects central banks are doing more harm than good. A state entity doing more harm than good (of course for many you’d need to see past self interest to see that perspective)

Here is a possible solution to all of this - the original Yield Curve Control "In the early 1940s the Fed put a cap on yields of government bonds across the curve; a policy that lasted for two decades. The Fed printed whatever was necessary to fund the government and inflation was allowed to run much higher than interest rates. The result was deeply negative real interest rates, which washed away the debt relative to GDP"

For the whole article search: Why the Gold Price Is Sinking - The Gold Observer (substack.com)

Rudy....here is a possible solution. The Govt and the RBNZ stop doing everything it can to cause rampant asset price inflation. They might even want to do a few things to stop it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.