The world is seeing a "capital drain" into the United States at the moment, Reserve Bank Governor Adrian Orr says.

He told an NZ Council of Trade Unions function in Wellington on Monday that the fall in value of the Kiwi dollar - it's currently worth around US56.3 cents - was due to the fact that US interest rates were being pushed up strongly to fight inflation.

This was prompting a capital drain from the rest of the world into the US to where the highest yield is and was also leading to broader uncertainty that was prompting people to want to have capital back in the US - a "safe place" - as opposed to effectively the rest of the world.

"When you see the Kiwi dollar at the moment, it is vis a vis the US dollar in terms of a declining New Zealand dollar. Almost every currency in the world is declining against the US dollar as they [the US] look to disinflate along with the rest of us," Orr said.

"It's just that they matter more on the way through."

Orr noted the very high rates of inflation at the moment, particularly in Europe.

In a "relative" sense New Zealand is in an excellent position, he said.

The RBNZ has been rapidly hiking interest rates, having raised the Official Cash Rate from just 0.25% as of October last year to 3.0% now. And a further 50-point rise is universally expected by the marketplace when the next review takes place on October 5.

"We've come through this extremely well. It doesn't mean that 7.3% inflation [as of the June quarter] is acceptable - no it is not. But in that relative global shock, just giving it some perspective.

"Obviously at 7.3% this central bank has got work to do," in terms of getting inflation back into its targeted 1% to 3% range, Orr said. So, the central bank has been "renormalising" the level of interest rates from the Covid lows.

"We were noisy about it, because the more people have low inflation expectations the easier it is to achieve low inflation expectations.

"We believe we still have some work to do - but the good news is, because we've done so much already, the tightening cycle is very mature. It is well advanced.

"So, we've got a little more to do before we can drop to our normal happy place, which is to watch, worry and wait and look for signs of inflation up or down - at the moment we feel we are still too close to some sense of neutral but well on course to achieve that."

The RBNZ has defined the level of 'neutral' interest rates - where they are neither stimulatory, nor restrictive - as about 2%, but has indicated that the real neutral rates may be getting higher. And it is doing some work on that at the moment. Economists have suggested the real level of neutral may now be about 3%.

Orr said the real challenge ahead for NZ is productivity, when it comes to the labour market.

"This is the time to be thinking about, can you do better things? Or can you do the same thing better?"

"I believe it is a great opportunity for doing the same thing better."

He said the country needs to look at achieving better output per person.

"That is the huge necessary opportunity that sits in front of us - how we can think about that."

103 Comments

"When you see the Kiwi dollar at the moment, it is vis a vis the US dollar in terms of a declining New Zealand dollar. Almost every currency in the world is declining against the US dollar as they [the US] look to disinflate along with the rest of us," Orr said.

In a "relative" sense New Zealand is in an excellent position, Orr said.

You are seriously joking. It's in such an excellent position that the NZD ranks as the 2nd worst performing currency in the last 1, 3 month and 6 month (just behind the GBP) cycles. Overperformance indeed.

https://www.barchart.com/forex/performance-leaders?viewName=chart&timeFrame=6m

In fact, he's 'overperforming' on a YTD basis against almost all currencies - https://www.barchart.com/forex/all-forex-markets/New_Zealand_Dollar/NZD?viewName=performance&orderBy=symbol&orderDir=asc - except the pound and the Turkish lira. Someone give this guy a raise (but definitely not in NZD)!

NZD has dropped approx 10% against AUD so far this year.

Orr has developed a disingenuous habit of half truths ("temporary supply inflation", "RBNZ OCR is not responsible for house price inflation"...)

It's not a half truth when it's a blatant lie.

What is the other half of a half truth?

A half lie?

Or a half don't have a clue?

Or a bit of both?

Yip we're starting to live in Orwell's 1984. Government agencies have become ministries of truth.

Why are we surprised, RBNZ are no different than the Govt in that they are totally convinced they can just blatantly lie to the people of NZ and then walk away giving themselves a pat on the back for a job well done. Absolutely insane but when no one is ever able to be held accountable, thats what you get.

Welcome to the current government culture, allowed to form and mature due to it's leader showing it is perfectly ok for the govt to mislead the public they are supposed to serve, especially when it benefits those at the top.

Adrian has certainly left himself plenty of room to 'to do things better".

It is called the US dollar hegemony,.

One cannot gain hegemony while still hiding from the viruses created in ones own labs.

No Xi its trust even though the US is not wholly trusted compared with The Euro/Yen/Yuan/Ruble etc etc its trusted. But there is an agenda which has started with liquidity withdrawal on top of rising interest rates will ensure structural changes in the global economy but the winner & losers are not certain and NZ seems unlikely to be in the winners box unless the recession/depression comes in mid 2023 and we elect a Govt of competence which by comparison with the current collection of clowns should not difficult but will the voters see that or fall for hand waving and a toothy grin - again??

In am not sure there is a Govt of competence in waiting?

Dollar milkshake theory (Brent Johnson) appears to be playing out. Everyone runs to the USD and then everyone runs from the USD!

Yep. There's a top coming. The signs are there.

Why would "everyone run from the USD" IO, can you please elaborate?

When the world realises that the US is bankrupt and will default on its debt obligations.

Technically, the US is bankrupt now (deficit spending far exceeds productivity/tax take), but its ability to print money is keeping it afloat (think about the difference between the US now and what Weinmar/Zimbabwe experienced when creating money while not the reserve currency). And it has to print money/create money to inflate away its excessive fiscal deficit. But printing that money is going to make things worse for everyone who doesn't have a swap line to USD with the Fed (i.e. they will hyperinflate their own fiat currency in order to maintain parity with the USD unless the Fed helps them or if not experience hyperinflation, will have significant drops in their living standards).

At some point, it could be this year, it could be this decade, or it could be the next 50 years, people will realise the game is up - as have been the case for every global reserve that over extends with spending as it attempts to maintain its standard of living and global military force. The US is just one of many reserves that have found dominance, and will eventually lose dominance.

Have a look on youtube about Brent Johnsons dollar milkshake theory and Ray Dalio's long debt theory combine with 'Changing World Order'.

An eventual run from the USD makes sense if you understand these theories.

This was a good read, more for those of us less educated on the historical aspects.

I believe he’s a financial analyst for Fintec.

https://docs.google.com/document/d/1552Gu7F2cJV5Bgw93ZGgCONXeenPdjKBbhb…

I-O,

As with Mark Twain, reports of the death of the US$ have been much exaggerated. it may well be overdue, but right now, there is no realistic alternative.

I would bet heavily that you are not going short of the US$.

That's right, short term. But if one conflict doesn't go their way, you may see a serious back pedalling of international confidence of the USD. And if there is an alternative at the time that enables other countries to trade energy in, the USD will quickly find itself under a lot of pressure.

For instance, say the US rushes to defend Taiwan with a couple of carrier groups from a Chinese invasion. China could lob an overwhelming number of cruise/hypersonic missiles at the carrier groups and destroy them. The backlash within the US would be enormous, either they would go directly to nuclear war with China or negotiate for peace. Nuclear war and we don't even have to think about it anymore as we are all dead. Negotiated peace and it would mean ceding Taiwan to China. And the international community would suddenly realise the US is not unbeatable. Then do you want to trade in the currency of the nation that has just taken a beating? The USD would plunge as it's all based on confidence.

Of course that's not forgone conclusion. The US could defeat China and impose serious consequences including naval blockades which would send China into the dark ages. But in doing so, it would damage it's own economy significantly due to it's reliance on China which may lead to other similar consequences internally in the US.

As opposed to the massive confidence I feel in NZ🤔

The US is now energy independent. They are effectively Thier own little universe.

They won't default. They Will Just evolve and make up new rules. The rest of us Will follow.

There is alternative...hardest money ever created

Not doing too well in the last few weeks

No I hold USD of course....but in time, it wouldn't surprise me to see the US implode from the inside out. And I can see what Putin is attempting to do to speed that process up (same with the Euro).

Thanks IO, I understand your point which is well made. I thought you were talking about "running away from the USD" in the foreseeable future. Yes the US are technically bankrupt but I cannot see any currency (fiat or digital) replacing the USD any time soon. I'm familiar with Ray Dalio's theories but not Brent Johnson's milkshake theory, I will google him tonight, thanks.

IO -good valid points but Belgium is officially Bankrupt, Italy & Spain close to and the EU debt will be repaid by who when the ECB/EU collapse.

They simply run from the USD when it hits the top back into your own currency and take the profit. Its pretty obvious now that the best investment this year was the USD, looks like you could have made 20% returns by the end of the year, that certainly outstrips everything else that's tanking.

There's more to it than that Carlos! You're talking about short term speculation for a gain.

I'm talking about the mechanics of the entire global financial system over hundreds of years.

My Hatch account is looking pretty good right now 😁

Yes listened to him a year of more ago on this and he has nailed it. Note he is a gold fan and gold is crazily on sale at the moment.

Gold is only down against the US dollar. In most other currencies it is up. At the start of covid(2020) it was around $2300, and was close to $2900 overnight NZD. That is 26%. During the same period it is almost flat against the USD. People arent getting rich off gold. But they arent losing their shirt either. A tactical nuke, rise of the European right wing, the collapse of China and Taiwan...all reasons to hold something outside the fiat system. Then there is the UK and Europe's depenence on Russia. Russia and China are driving the direction at the moment through their withdrawal from the global 'play nicely' club. They are also buying gold.

"When you see the Kiwi dollar at the moment, it is vis a vis the US dollar in terms of a declining New Zealand dollar. Almost every currency in the world is declining against the US dollar as they [the US] look to disinflate along with the rest of us," Orr said. [my emphasis]

Hmmmmm..

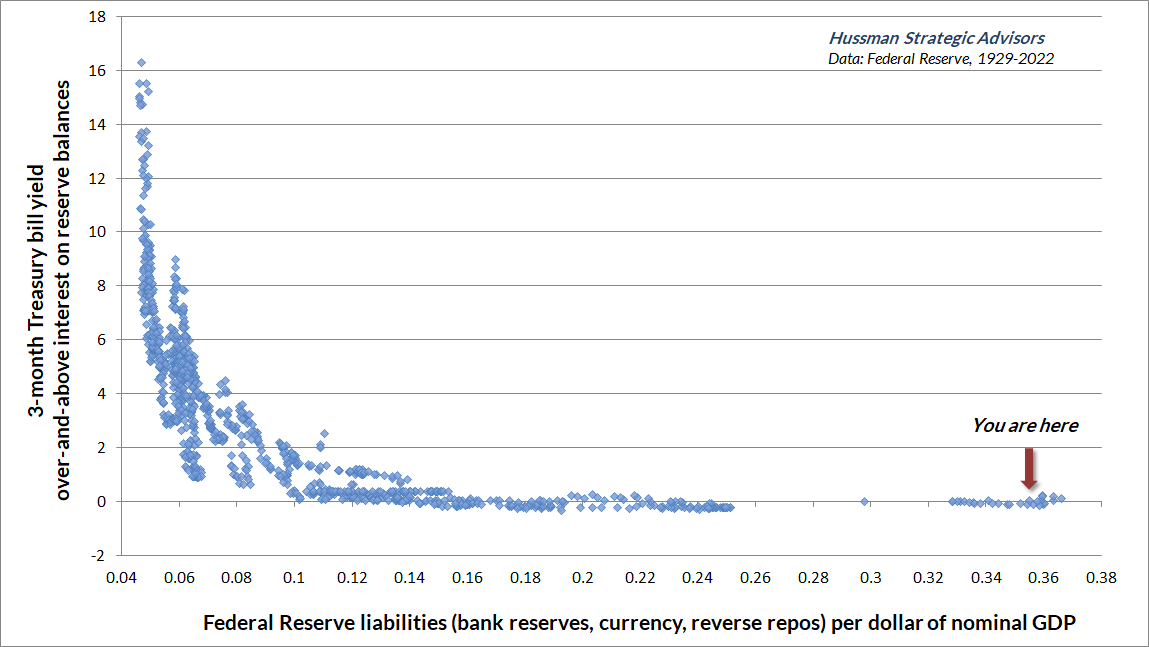

Diary of a deranged “ample reserves regime”

We are embarked on shrinking the balance sheet, and the test will be back to levels that satisfy the public’s demand for our liabilities – that’s currency, and reserves, and things like that – but also with reserves maintained at a level that is consistent with our ‘ample reserves regime.’ So the balance sheet is substantially larger now, obviously, and consequently the runoff process is designed to be substantially faster than the last cycle; on the tune of a trillion dollars of runoff per year, once it’s up to full speed. As far as returning to a scarce reserves regime, I guess I would say that I think our current operating framework is a better one, and I don’t see a case for returning to scarce reserves.

And why is that? So, the world has really changed as a result of the global financial crisis and the pandemic. The scarce reserves framework would be challenged to work in a world where there’s very high and sometimes volatile demand for safe and liquid assets, central banks may have to rely on large-scale asset purchases from time to time in response to severe shocks, and remember that the large financial institutions hold very large quantities of safe assets now as a liquidity buffer, and that includes a lot of reserves. So the bottom line is that the quantity of reserves is just so much higher that it would seem to be impractical to try to manage scarcity, and demand will be volatile too. We think the current system works well and it provides a lot of liquidity, so it’s kind of a net gain.”

– Fed Chairman Jerome Powell, Cato Institute Monetary Conference, September 8, 2022

Let’s take a closer look at the atrocity the Fed is defending as its “ample reserves regime.” The chart below shows total Federal Reserve liabilities as a fraction of nominal GDP, along with the 3-month Treasury bill yield over-and-above the interest rate that the Fed (now) pays to banks and other financial institutions that hold these liabilities. The chart is our version of what economists know as the “liquidity preference” curve. I’ll explain it in greater detail after you catch your breath, but it’s worth noting at the outset that in the entire history of U.S., Fed liabilities never materially exceeded 16% of GDP (0.16 on the horizontal axis) until 2010, when the Fed went full-tilt loony tunes with quantitative easing. The discontinuous leap to a balance sheet greater than 25% of GDP occurred when Powell doubled down, literally, in 2020.

What Powell describes as a “scarce reserves regime” is actually the policy environment that operated under during the entire existence of the Federal Reserve prior to 2010. It worked like this: in order to influence short-term interest rates and the money supply, the Federal Reserve would go into the open market and purchase Treasury securities, gold (mostly prior to 1970), or other government-backed assets. In return, the Fed would create “Federal Reserve liabilities” – currency and bank reserves – to pay for them. You can see what a Federal Reserve liability looks like by reading the top line of a dollar bill. The terms “Fed balance sheet,” “Fed assets” and “Fed liabilities” are often used interchangeably, because they’re different sides of the same coin.

Historically (until QE) Fed liabilities did not earn any interest. Banks and individuals were still willing to hold them because they provided immediate liquidity. Equally important, varying the “scarcity” of these zero-interest liabilities was precisely how the Fed set short-term interest rates. As the quantity of currency and bank reserves (base money) becomes more plentiful, investors become uncomfortable with all that zero-interest liquidity, and begin seeking alternatives that might offer a greater return. Their closest alternative is Treasury bills. So as the quantity of base money increases, Treasury bill prices are bid higher, and their yields are bid lower. This process continues until investors are indifferent between holding zero-interest base money or low-yielding Treasury bills.

Put simply, when the Fed floods the system with reserves, the public tries to get rid of the excess, and will accept dismally low T-bill yields to get a “pickup” over whatever reserves are paying (historically, zero). When reserves are scarce, the public is hesitant to get rid of them, and holders need the incentive of high T-bill interest in order to part with them. That, in a nutshell, is how Federal Reserve operations impact short-term interest rates.

A critical feature of this process is that once a dollar of base money has been created, someone in the economy has to hold it, at every moment, until it’s retired. It can pass from one holder to another, from the buyer of T-bills to the seller of T-bills, from the buyer of stocks to the seller of stocks, but there’s no way to get “out” of zero-interest base money in aggregate. Until the base money is retired by the Fed, somebody has to hold it, even if nobody wants it. It’s a hot potato.

You can see in the chart precisely how Paul Volcker crushed inflation in the early-1980’s. Volcker cut the Federal Reserve’s balance sheet to less than 5% of GDP. That scarcity of Fed liabilities did two things. First, investors and banks who needed immediate liquidity became willing to sell Treasury bills at lower prices in order to obtain base money, and holders of base money became very reluctant to give up their liquidity unless they were compensated by a very high interest rate. As a result, Treasury bill yields briefly shot above 15%. More importantly, however, Volcker’s restriction of the money supply convinced the public that the Federal Reserve would not passively finance government deficits, restoring confidence in fiscal stability and stable prices that was lost a decade earlier when the U.S. abandoned the gold standard, closed the gold window, and ushered in floating exchange rates.

As Nobel economist Thomas J. Sargent has observed about severe inflationary episodes, “once it became widely understood that the government would not rely on the central bank for its finances, the inflation terminated and the exchanges stabilized.” Sargent also observes that severe inflations have been driven not simply by the quantity of central bank liabilities, but instead by “the growth of liabilities that are unbacked, or backed only by government debt, for which there was never a prospect to retire.” Governments can typically expand their debt in line with the growth of the economy itself, without inflationary consequences, provided that the overall debt-to-GDP ratio is serviceable. But once the public loses confidence in government restraint, because of unrestrained government deficits, overly accommodative monetary policy, or both, inflationary expectations can become embedded. That’s particularly true if the economy also faces supply shocks. It’s also why Section 2A of the Federal Reserve Act mandates that the Fed “shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production.”

In the Federal Reserve’s arrogant defense of an “ample reserves regime” and dismissive regard for the so-called “scarce reserves regime” that has defined monetary policy for a century, the Fed is telling the public that it has no interest in restraint.

As investors, we’ve already addressed this prospect by abandoning our reliance on previously reliable “limits” to speculation – becoming content to align ourselves with prevailing market conditions, particularly valuations and market internals. But our concern is also for the public interest, and I remain convinced that the Federal Reserve is willfully ignorant of the consequences of its actions, both on yield seeking speculation and on the public confidence in government liabilities.

{kind=link}

Link : Now Comes the Hard Part - Section: Diary of a deranged “ample reserves regime”

Wonder how our dollar would look if we'd started lifting earlier and faster, instead of leaving our OCR on the floor for months longer than it should have been, and only lifting in fits and starts when the rest of the world is starting to look at 100bps hikes as a bare minimum?

Wasn't our OCR higher than pretty much every other developed nation over the past decade? Isn't it still significantly higher than many?

I'm truly impressed Adrian still has his job. Bravo sir, Bravo!

... we can forgive him for talking to the trees ... but , if he does a " Gideon Gono " and turns us into Zimbabwe , arouse the villagers , storm the RBNZ citadel ...

Orr's credibility is on a similar trajectory to the NZD.

No. His cred is going down way faster than that.

Funny thing is most people wont learn how badly he has messed NZ up ... until we are in the middle of a serious economic crisis.

The problem the world faces is that the global reserve currency has too much debt relative to GDP. And it is going to make the rest of the world suffer for its own lack of productivity (or living beyond its productive capacity/means). It can only do that while is holds reserve status. If/when this advantage is removed, it could be a quick fall from grace for the US, with significant global geopolitical instability, and a large fall in living standards for US citizens. Creating more money to inflate away their excessive fiscal deficit spending (to maintain their standard of living and global military superiority) is going to become a nightmare for everyone around the world.

The US could become very much unliked on the world stage after this has all played out - the opposite of WW2.

Putin appears to be onto it - not that I like Putin or what he stands for. But he appears to understand macroeconomics quite well - much better than the democratic party of the USA or the leaders of the Eurozone.

Are you not conflating separate issues IO? Isn't the US$ the reserve currency because the US is currently the world's largest economy? and wouldn't that be true for the previous reserve currencies?

Also why do you think Putin is on to it? PDK seems to think this too, but to me it just looks like coincidence?

But I would suggest that the real problem is that the US bought into the 'free market' economic model and 'globalisation' too much and has tried to print too much money to paper over the cracks and it is all starting to come back to bite them. They lost sight of the fact that it is a Government's role to manage and regulate an economy, and when it doesn't do this, bad things happen. Those bad things are starting to pile up a bit now.

"Are you not conflating separate issues IO? Isn't the US$ the reserve currency because the US is currently the world's largest economy? and wouldn't that be true for the previous reserve currencies?"

I'm not sure what your point is - could you clarify what you mean?

Perhaps ask yourself - why are the Portuguese, the Dutch, or the Spanish, or the French, or the British are no longer the global rulers in 2022 (but each experienced global power over the past 500 or so years...but no longer do). The world isn't in a fixed state and over time, each global power creates too much debt to enforce is will on the rest of the world - with the advantages that come from holding reserve currency status and having military and trade superiority. They have to run fiscal deficits to fund their military and to maintain the high level of living they become accustomed to. But in the process they bankrupt themselves. Its a natural cycle.

Fundamentally the core value of the US$ is backed by the sheer size of the US economy. (It is undermined to an extent by money printing) So if the world collapsed tomorrow, the US is one place that the internal economy would continue to function to a degree greater than most if not all other places. Thus that value is well supported and can be viewed as essentially stable and secure.

In the examples you provide, Portugal, Nederlands, Spain, France and Britain, all at some stage have been viewed as the world's largest and most stable economies ( in part due to their military and political power (colonisation)). Consider the events that stopped them being the reserve currency and I'd suggest it would have been the loss of that power and size? Your second paragraph spells it out to an extent. I agree that the US is pushing the outer boundaries and risking collapse, but what would trigger that.

The Euro was created to compete with the US$, but never quite made to cut. Is that because the US is one contiguous economy while Europe and the European Union is not?

Yes, but if the BRICS get together and decide to make a Euro-esque currency... they will represent an alternative bloc similar in size to the West, economically and population based and probably future potential based. Once energy is traded in non USD denominated currencies, it's game on, the US will push aggressively for this to not happen as it undermines their global reserve status. At which point we could quite quickly see a rearranging of the world order... with us probably at the bottom, which isn't surprising given our size. It would probably also mean a bunch of sort term conflicts, usually in in-between states, much like Ukraine, to avoid real destruction to each blocs economies, due to how interdependent they are. As a country we would probably need to not burn bridges with either bloc and act as a neutral state, hoping one of the big boys doesn't see us as an strong enemy that needs to be put down. We could trade our way out of it with food products everyone needs in return for the things we don't produce.

Not that the BRICS currency is guaranteed, that would require some serious cooperation from states that don't really trust each other (Euro is a good example). And they would all need to commit to it at the same time both economically and militarily to defend each other. Quite a big ask and they aren't there yet.

You get it blobbles.

BRIC stands for Brazil, Russia, India and China

the only country in that lot that has not given itself self inflicted damage is India- but Climate change is hurting and is going to hurt India with a billion mouths to feed.

For a central currency to work you need economically stable countries with common interests - that ain't BRIC in the next 5 years

You make sense, but what would it take for oil, for example, to not be traded in US$? Except that I don't accept that it would be the BRICs because no one trusts them (not that there's much more reason to trust the US these days, but when the US$ became the reserve currency it was a more reliable country).

Why don't OPEC countries accept payment in their own currencies now?

It's already happening, by demanding payment in rubles for Russian gas and oil. A BRICS currency may not be close, it would have to have lots of those nations involved form very strong bonds, but current circumstances where the US has essentially tried to economically cancel Russia may push them to forge ahead. TBH, they would be stupid not to, given the bloc could out trade/grow the US hegemony in fairly short order. But as you point out, there are a bunch of their own trust issues between them that they would need to sort out before it happened. And they all may want to grow militarily to enable them to back up such an arrangement. None of that is going to happen fast.

"Nobody trusts them" doesn't matter if you are screaming out for energy (see Europe who definitely doesn't trust Russia, but will still buy as much gas off them). What may happen is one of the already oil majors (Saudi Arabia, for instance) might take up a middle man role even more than it currently does and enable payment in any currency, the Ruble/USD/BRICS/whatever. Again it would be a smart move, if they wanted to remain on everyone's good side and make a lot of money doing it. But it would be a dangerous place to be you would have to be nobodies friend or enemy.

OPEC countries have a pretty weak military so have to pander to whatever the current global reserves are, they simply couldn't demand payment in anything else as they couldn't back it with a decent military. If OPEC suddenly decided it was going to demand any one of it's own currency for payment the US would invent a reason to attack them, if they couldn't dissuade them through peaceful means.

I'd suggest that you take Putin's demand for Roubles in payment for Russian oil out of the equation. That was a move by him to prop up the value of the rouble when the world was turning their backs on Russia after his invasion of Ukraine, and so far not one copied by other oil exporters.

IO makes a good point that the US is technically bankrupt, but they only get away with it because of the international demand for the US$. I think you make a fair point that a major exporter could become a middle man, and Saudi is a good choice, but politically that will never happen in the near term, as the middle east is too riven by religious based politics and Saudi is too dependent on the US for defence needs. I find it ironic that for all their hatred of the infidel west, the oil wealth in the middle east has led to a hedonistic lifestyle which mixed with their religious cultural bias's makes them far worse (in attitude and the way they treat others) than anything the west has ever done. The only thing that has saved the west would be that their autocratic leadership tends to stifle true inventiveness and creativity.

Russia may be the last country to hold significant oil reserves in the end, but i doubt people will want to deal with them with the type of leadership they tend to produce, so your model of a middleman will be necessary long term for them to profit from much of their resources.

I doubt the US would or could invent a reason to attack OPEC, but consider that OPEC would only take such a move if they felt sufficiently strong to withstand the diplomatic and economic pressures if they tried. While the need for oil remains (too) high, that will change overtime as we move to alternative energy sources (it will take a while), and as that happens, OPEC's power and opportunity will wane. In this day and age it may even be possible that the economic gain of a war over oil in the ME will be less than the cost of that war making it essentially pointless.

Also remember the US is the worlds largest economy when measured in USD terms. That's not the right measuring stick, kind of like me having my own ruler with shorter CM markings and therefore claiming I am the tallest person on earth. At the moment we are all defacto based on USD though so there probably isn't a better measuring stick, though many argue China is already far bigger than the US, if you measure in different ways.

The USD is the default currency more because it's only what most cross border transactions are based on and most of that is energy. That's partly because of them being the winners of WWII and being almost completely untouched by the conflict has enabled them to have a massive military based on a lot of money printing debt, backed by their petro dollar trade status of the USD. And they defend this because they know the petro dollar is key to their hegemony (see Libya military actions, seizing Iraq oilfields illegally, their cozy relationship with Saudi Arabia - a regime they would decry as evil if it wasn't a petro dollar friend). It's kind of circular, but basically enables them to be the worlds default until (as IO points out) either their debt causes other states to realise it's all hocus pocus so they lose confidence and/or another player emerges which challenges the hegemony, which we are possibly seeing with BRICS. And those events are likely to play out over the next few decades.

It will be a real shock to people in the US when they wake up to realise they actually don't have privileged status anymore, with Euro style gasoline prices and a hollowed out real economy, plus probably trillions of $$ that they have to actually pay back without printing more, else mass inflation. I doubt they have the leadership to navigate it (Trump or Biden don't appear to be there).

This is basically right. It's also worth bearing in mind that the US will not give up its reserve currency status without a (literal) fight; it has already happened in some of the conflicts you mention, and there will certainly be more to come.

Good post Blobbles. I'm curious what other measure could be used to measure an economy? There has been many on this site which indicate GDP is not a good one? China, by virtue of it's population size, should to all intents be the largest economy (and as you indicate could be argued to be so now). Is it 'value' that makes an economy? So how do you set an internationally recognised, stable 'value' index that becomes independent of currency? As I write this, I realise that all the 'economic' activity that occurs in China, and even India could easily mean those economies are bigger than the US. But does stability of the style of Government also become an influencing factor. Is 'trust' a part of the equation? This becomes an extremely complex issue, because all those factor would also impact the agreed 'value' of a floating currency. For that universal measure, should the currency unit be a floating one or fixed? If so, to what?

IO- for comparison check this chart out - https://croakingcassandra.com/2022/09/26/decline-and-fall/#respondhttps…

Us was no1 for GDP per capita in 1939 and 1952 and is still no 6 ahead of Germany, the puzzle is Belgium which is Bankrupt despite being no 5 so improved productivity is not the benchmark of trust. Other large EU countries below US and NZ falling from no2 to no 21 but still a decent debt to GDP ratio and I believe NZ is still a well trusted country in terms of reliably returning investors funds. For NZ the chart clearly shows for the last 80 years Govt policies have not improved the living standards of it people and continuing such policies will not change the direction but are voters ready to accept the radical policies necessary to reverse direction, improve productivity and real GDP per capita - not holding my breath.

no worries then,just another tweak at the next meeting. keep gliding on.

In a "relative" sense New Zealand is in an excellent position, he (Orr) said.

OMG, com'on Mr Orr, NZ is in a terrible position. I'm no economist but it seems pretty clear to me, and many other commenters on Interest that:

- Inflation is too high in NZ

- The OCR needs to be raised further to lower inflation

- The raising of the OCR and interest rates generally (also due to swap rates) is going to throw NZ into a serious recession in 2023 (my view)

- We'd like to avoid a deep recession by not having rapidly surging interest rates but we can't do that because our currency, the NZD is plummeting, thus increasing our tradable inflation.

So you, Mr Orr, have no choice but to keep increasing the OCR, thus throwing NZ into a deep recession in 2023, at which point inflation will drop significantly but the damage will have been done, businesses will close down, employees will lose their jobs and NZ will be a mess.

Wake up Mr Orr!

I could also add that NZ has a terrible trade account deficit, which I believe is currently being financed by foreign investment. This foreign money could dry up pretty quickly in the current environment, what then Mr Orr?

The foreign money is already starting to dry up otherwise we would had the sell off in NZD overnight.

currently being financed by foreign investment

I've seen this statement thrown around a bit now. Can you elaborate on this? Is the gap essentially plugged by capital inflows from investment in Govt and or corporate bonds and our stocks?

Western leaders have become a bit like the ministry of truth from Orwell's 1984. If they say something, the 180 degree opposite is probably the truth.

(Not that Xi or Putin are any better....but in the west we like to say we are the leaders of the free world - which no longer feels particularly free or truthful).

It's possibly primarily about managing the potential for panic in the population.

I agree - or the ministries are feeding false information to ministers who don't really understand what is going on around them. Having worked in Wellington before, the latter is quite possible. You end up in a situation where the blind (ministers) are leading the blind (voting population who don't understand what is happening).

This government has had sound advice that has been intentionally disregarded by both the prime minister and health minister. My wife worked at the Ministry of Health until recently and couldn't bare to stay after everything that had gone on.

I agree - or the ministries are feeding false information to ministers who don't really understand what is going on around them.

Having worked in government Hanlon's Razor (Napoleon edition) does all the explaining you need:

Never attribute to malice what can adequately be explained by incompetence

YVIL - I agree but there is a silver lining, as the NZ$ depreciates exports are more affordable and imports less, so in a recession exports will naturally decrease with growing unemployment and increasing local non tradable expenses, the trick is to use this advantage to reset NZ and improve its productivity but Politicians seldom recognise the wood for the trees.

There's no silver lining. Just check out the trade deficit - NZ imports more than it exports. Even the stuff that it exports requires inputs that are imported.

Kaumatua Orr would never let himself face people who could ask the hard questions. The media is not going to ask those questions because they're probably be risking their careers in the economics and political reporting / comms positions they perform. Who would hire them in a media role or in some comms role in the public sector if they were seen as asking difficult questions?

So all you will get are these rear-view mirror speeches telling people what they already know; attempts to minimize any responsibility on his or his orgn's part (no wonder most of the RBNZ senior staff have already jumped ship); and the ol' "relatively better than the rest of the world" spin.

In the present case, the ol "relatively better than the rest of the world" spin is an outrageous lie, clearly borne out by the sheer terrible performance of the NZD vs almost every other currency.

So in other words, ocr won’t / can’t go up much further! Backed into a corner with massive household debt from a messed up housing market. The damage was done last year.

I think the Fed and RBNZ have two options:

1. Protect the respective currencies but trigger a very deep recession with large falls in asset prices and potentially increases in unemployment.

2. Fail to protect currencies and we see very high inflation for a long period of time while asset prices are protected (in nominal, but not real terms) and unemployment maintained to politically agreeable levels.

It's not really the RBNZ's decision to make. They just follow their CPI mandate which in theory leads to option 1. It is really up to the government to intervene and amend the criteria on which our monetary policy is based to select option 2.

Western governments need to drop fiscal spending! But they're not doing it. They're flooding the economy with money when inflation is already too high, making the problem for central banks even worse. They are fighting each other at present, not working in harmony.

I can't remember a day when I agreed with so many of your comments IO!

Great that we have some common views.

So in other words, ocr won’t / can’t go up much further! Backed into a corner with massive household debt from a messed up housing market. The damage was done last year.

If you said the last 30 years (about the damage), you'd probably be more accurate. The last few years is just the most insane periods. Manipulating the price of capital through the central bank mechanism and USD hegemony has been a recipe for disaster. But who knows? Could all be OK after a nice hot cup of tea.

The demolition starts 2023.

Those that jumped the RBNZ ship must be happy...I wonder how Yuong Ha's sons cricket team is getting on? I'm sure it's performing better than Orr and the NZD...

Orr "Yuong Ha, our chief economist, has chosen to go into a far more challenging role. What are you going to be doing?"

Ha, who was sitting next to Orr, responded, “Coaching my son’s cricket team, taking a break.”

https://www.interest.co.nz/public-policy/113432/grant-robertson-unconce…

Just a wild guess, but judging from the comments above, most people now 'get it'.

And even worse, they're starting to get that queezy feeling in the pits of their stomachs; one that may not have been there up until now - that a previously unthinkable set of events is right in front of us.

Pity it took so long for so many to wake up. Many of us 'got it' when the absurd amount of borrowed cash was pouring into the non productive housing bubble.

The recession was baked in many years ago...just kicked down the road at each election cycle.

Key had the financial skills to see it...and chose not to. Jacinda and co haven't the ability.

Geez, I wish Key had done something about it. That's why I voted for him, twice, because he campaigned on doing something about 1) the housing crisis, and 2) the productivity problem. The big problem was when he about-faced and National started calling them "good problem to have" and "sign of our success", kicking the can down the road for the next government.

Yes, folk would've felt a little less rich without being able to foist massive debts on following generations and being expected to create value instead, but our economy would've been on a more stable footing.

We may not have seen massive government and Reserve Bank welfarism dedicated to propping up the property market when COVID hit, had our economy been refocused on value creation.

I did likewise.

If I have to give Key the benefit of the doubt, it comes with that innocent comment he made on late night US TV - "You don't get out of Debt by Borrowing more Money!" he said, and was probably later ushered into a small, dingily lit, back room and The Fed to have the Facts of Life explained to him.

Although that statement is wrong. It's fine to borrow short-term to invest in systems that will improve productivity long-term.

Except your investment cash flows, principal repayments and cost of capital are unlikely to be aligned.

short term rates can be more expensive due to liquidity premium.

Ah yes, the economic response to an event three years after Key left parliament is somehow Key's fault, despite a flailing government making similar promises about sweeping reform and then abandoning them between then and the onset of Covid.

All the leaders across the western world are complicit over the last 20-30 years.

But then again, the mechanics of the long debt cycle mean they have little option but to all do what the Fed dictate, until they implode as the global reserve currency.

Only then can stability be found - because the Fed is going to have to continue to create money to inflate away their excessive debt...and that is going to cause headaches all around the world until they are forced to stop (which is what Putin appears to be trying to do with his war in Ukraine).

Why are you blaming the leaders? We voted for them and then forced them to inflate the housing market and avoid investing in the long-term future of the country. This is on us.

Good call…they are mere pigs at the trough.. wielding the lolli scramble that is democracy

Lol - if you say so!

I voted for Key and Adern based on promises to address housing affordability and inequality. But as soon as they were in power for a term they decided they no longer had any interest in acting upon their election promises and instead decided those issues they wanted to fix, were actually features they could use for their own political advantage.

It would appear the system is toxic as its impossible to change the rot.

Yes, it's a fundamentally flawed system for managing tribal animals. 3 or 4 year terms and human nature sets us up for vote buying.

Read my post again. Key had the skills and did not act. Jacinda doesn't have the skills, so it's a bigger ask.

So who the heck does one vote for?

They're guilty of their own about-face just as Key is. Nowhere in my post did I say their actions were Key's fault. Feel free to point out where you think otherwise, if you like. Also, I did not vote for Labour or Ardern, while I did vote for Key / Nats.

Orr is shameless character. Not all currencies gone down by 25%. He needs to step down.

because we've done so much already, the tightening cycle is very mature. It is well advanced.

So, we've got a little more to do before we can drop to our normal happy place

Sounds like a flip-flop is coming soon...

Only when Powell allows it. So if you think the Fed are about to flip-flop (whatever you mean by this) then sure.

If they Fed pivot, while inflation is still at 8%, then it could be the end of the USD as the global reserve currency.

I read that funny too. It doesn't quite make sense does it?

Will all the US dollars going home cause more or less inflation in the US? Imports will be cheaper, but where will the money be parked. Who can borrow it a these high interest rates. Sounds like a major crash is on the way!

Farmers will keep NZ afloat as they have always done when the NZD tanks!

In a "relative" sense New Zealand is in an excellent position...

Relative to...?

I have concerns that by allowing our currency to plummet we will import inflation and ultimately have to endure even higher rates. Our long-term outlook needs to be more balanced.

RB Governor says almost every currency in the world is declining against the USD. Thats nice...but who cares about every other currency? Whats being done to stop/slow the NZD declining.. let me guess...nothing at all...lol

He's right. What he has missed out 'conveniently' is that NZD has declined the most (2nd only to the GBP). In other words, as all the other currencies are declining against the USD, NZD is declining against the USD faster than all of them and also against all of them. And obviously he has done nothing at all - no emergency rate hike, no policy posturing, no forward guidance. Zilch, and he has the gall to make the statements that he has made.

Grant Robertson has also disappeared.

Inflation and a component in NZ's inflation. Are we not shooting ourselves in the foot?

https://www.newshub.co.nz/home/world/2022/09/ukraine-invasion-joe-biden…

Biden pushed back against Russian complaints that Western sanctions are harming its exports,

stressing that US sanctions explicitly allow Russia to export food and fertilizer and that it was "Russia's war that is worsening food insecurity."

Yet in NZ we have a 35% import duty on all Russian goods. Check out MBIE website. I did not locate an exemption.

What's going on here?

Productivity, productivity, productivity. that hoary chestnut. Certainly something to think about as Orr says. Put it back on the poor old worker. Who is already working long hours etc. We are told that businesses need to invest in engineering and technology to improve productivity. Unfortunately because most of our exports are in primary produce from small run holders there is not much room to move. Where can this increase in productivity come from?

More ag robotics. Next 25 years many a low wage job will vanish.

Double post

Productivity comes from brave decision-making & some balls to see it through. It has to be high tech, even with food. We have to do this. Now's good.

With Adrian virtually doubling the size of the Reserve Bank over the past 4 years with no discernible increase in the quantity or quality of outputs, is he really the right guy to be lecturing us about productivity?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.